- The Answer is the official legal document you file to contest a debt collection lawsuit and prevent an automatic loss.

- Filing an Answer forces the debt collector to prove they own the debt and the amount is accurate, which many debt buyers struggle to do.

- You must find the deadline on your summons, as you typically only have 14 to 30 days to file your response with the court.

- Even a basic general denial shifts the burden of proof back to the collector and completely changes their expected cost calculation.

- You must mail a copy of your filed Answer to the collector’s attorney, a critical step that many people miss.

The Most Important Document You Will File

A stack of court papers just landed on your kitchen counter. Maybe a process server handed them to you at your front door, or perhaps you signed for a certified letter. Your name is listed as the defendant in a civil lawsuit. For most people, this is a moment of pure panic. They have never been involved in the legal system, and the natural instinct is either to hide the papers in a drawer or call the collector immediately to beg for mercy.

During my 12 years working inside third-party collection agencies and a national debt buyer, I saw how this exact moment plays out thousands of times. I know exactly what the debt buyer is hoping you will do. They are hoping you will do nothing. They are counting on the fact that the legal jargon will overwhelm you.

To level the playing field, you need to understand that the document you hold is not the end of the line. It is the beginning of a process. The single most important action you can take right now is to file a formal document called an Answer. This is not a complex legal maneuver requiring years of law school to understand. It is a fundamental right that tells the court you are participating, forces the collector to prove their claims, and completely changes the dynamic of their collection effort.

What an Answer Is and What It Actually Accomplishes

When a debt collector files a lawsuit, they submit a document called a complaint. The complaint lists their allegations against you. They will state that you borrowed money, that you defaulted, and that they are legally entitled to collect a specific balance. To the untrained eye, it looks like proven fact. It is not. It is simply their side of the story.

An Answer is your formal written response to the court and the collector. It officially states that you have been served and you are contesting the lawsuit. Most people assume that responding requires an elaborate defense strategy, but the primary job of your Answer is simply to exist and be filed before the deadline. When you do that, you accomplish four things immediately.

- It blocks the automatic win. If you stay silent, the court hands the collector a default judgment by default. Filing puts a wall between them and your bank account.

- It shifts the burden of proof. You do not have to prove you do not owe the money. The collector has to prove you do.

- It preserves your rights. Filing your response allows you to raise specific legal defenses that protect you from unfair collection practices.

- It changes their cost calculation. A contested lawsuit is expensive for a debt buyer to pursue. An uncontested lawsuit is cheap.

“When I was reviewing accounts at a major debt buyer, the litigation pipeline was completely automated. We would send thousands of files to our law firms. We fully expected 70 to 90 percent of those people to ignore the summons. When a consumer actually filed an Answer, that file was pulled out of the automated stack. Suddenly, a real human attorney had to look at it and decide if our documentation was strong enough to justify the hourly cost of fighting it.”

How Your Answer Changes the Collector’s Business Model

To understand why filing this document is so critical, you need to understand the economics of modern debt collection litigation. It is a volume business.

A debt buyer purchases old, defaulted accounts for pennies on the dollar. They hand these accounts to a collection law firm. The law firm files hundreds of lawsuits a week. The filing fee is a minimal business expense. They file these massive batches knowing that the vast majority of consumers will be too intimidated or confused to respond. When a consumer fails to answer, the court automatically hands the collector a default judgment. That judgment grants them the power to garnish wages, freeze bank accounts, and place liens on property. They gain maximum enforcement power with minimum effort.

This is not a legal outcome. It is a highly optimized business model.

When you file your Answer, you throw a massive wrench into that machinery. Because debt buyers often purchase accounts in massive bulk portfolios, they frequently do not have the original credit agreements, the complete chain of title showing how they acquired your specific account, or the itemized balance statements. If they cannot produce these documents, their case falls apart.

This dynamic is why forcing them to do the work frequently opens the door to negotiate a settlement on much better terms or even results in the collector voluntarily dismissing the case altogether.

Finding the Deadline: The One Date You Cannot Negotiate

In the legal world, timelines are absolute. The clock started ticking the moment you were legally served with the papers. It did not start when you finally opened the envelope three days later, and it does not pause because you need time to figure out your next steps.

You received two main documents in that stack: the summons and the complaint. Readers often focus on the complaint because it contains the dollar amounts and the accusations. You need to look at the summons. The summons is the court’s official procedural notice, and it is where your deadline is written.

Response deadlines are typically 14 to 30 days. This varies wildly depending on your state and whether you are in small claims court, justice court, or general civil court. The exact number of days will be stated clearly on the front page of the summons.

📌 Note: When counting your days, most courts use calendar days, not business days. If your 20th day falls on a Saturday, Sunday, or a legal holiday, the deadline usually rolls over to the next business day. However, you should never push it to the very last minute.

What happens if you have been sitting on these papers and the date has already passed? First, do not assume the case is completely over. Courts sometimes accept late answers if a hearing has not been scheduled or a judgment has not yet been formally entered by a judge. If you are past the date, you need to understand what happens if you fail to respond or already have a judgment against you, as you may still have options to vacate it depending on how you were served.

Signs You Need Immediate Professional Help

While drafting a basic response is highly manageable for many consumers representing themselves, some situations carry too much risk to handle alone. Before you start writing, you need to assess your situation. You should urgently evaluate your options for getting professional representation to handle your defense if you are facing any of the following scenarios:

- Your response deadline expires in less than 10 days and you do not know how to format your state’s required documents.

- The balance claimed in the lawsuit is large (typically over $10,000), making the threat of wage garnishment a severe risk to your livelihood.

- You already know the debt has serious documentation problems, such as being past the statute of limitations or involving identity theft, which an attorney can use to counter-sue.

- You received additional documents called “Requests for Admissions” tucked inside the lawsuit packet. In the collections industry, this is a known trap. If you do not answer them correctly, the court treats your silence as an admission that you owe the money, allowing the collector to win automatically without a trial.

What to Include in a Basic Answer

If you are moving forward on your own, remember that courts prefer clear, concise, factual formatting. Many state courts provide standardized, fill-in-the-blank forms on their self-help websites specifically for defendants representing themselves.

When drafting your own document, you must include a header with your full name, the court’s name, the plaintiff’s name, and the exact case number listed on your summons. After the header, you must address the claims made in the complaint. Look at the collector’s complaint. It will be a list of numbered paragraphs. Your Answer should respond to each of those numbers directly.

The General Denial

For each numbered paragraph in their complaint, you have three ways to respond: you can admit it, you can deny it, or you can state that you lack sufficient information to admit or deny it.

When I sat on the collector’s side, we would routinely receive Answers that were just three-page handwritten rants about a recent job loss or a medical emergency. We ignored the emotion entirely and looked only to see if they actually denied our legal claims. Admitting liability while explaining your hardship does nothing to defend the case legally. You must stick to a factual denial.

Many consumers fear that denying a claim is lying under oath if they know they had a credit card with that bank years ago. When you deny a claim in a debt buyer lawsuit, you are not saying the debt is a total fabrication. You are stating that the plaintiff has not proven their case to you, and you are demanding they meet their legal burden of proof.

In many jurisdictions, the most efficient route is a general denial. This is a blanket statement that covers all the allegations.

Preserving Your Affirmative Defenses

After your denial, you must list your affirmative defenses. These are specific legal reasons why the collector cannot win, even if the debt is yours. If you do not list them in your Answer, you generally waive the right to bring them up later at trial.

From an insider’s perspective, these defenses strike at the core of the debt buyer business model. For example, raising a “lack of standing” defense means you are pointing out that the collector bought a spreadsheet, but they didn’t get the actual contract to prove they own your specific account. Raising the “statute of limitations” defense means you know the debt is too old to legally sue over, and you are calling them out for filing anyway hoping you wouldn’t notice.

You should review a full overview of the debt collection lawsuit process and carefully evaluate which defenses apply to your specific situation before finalizing your document.

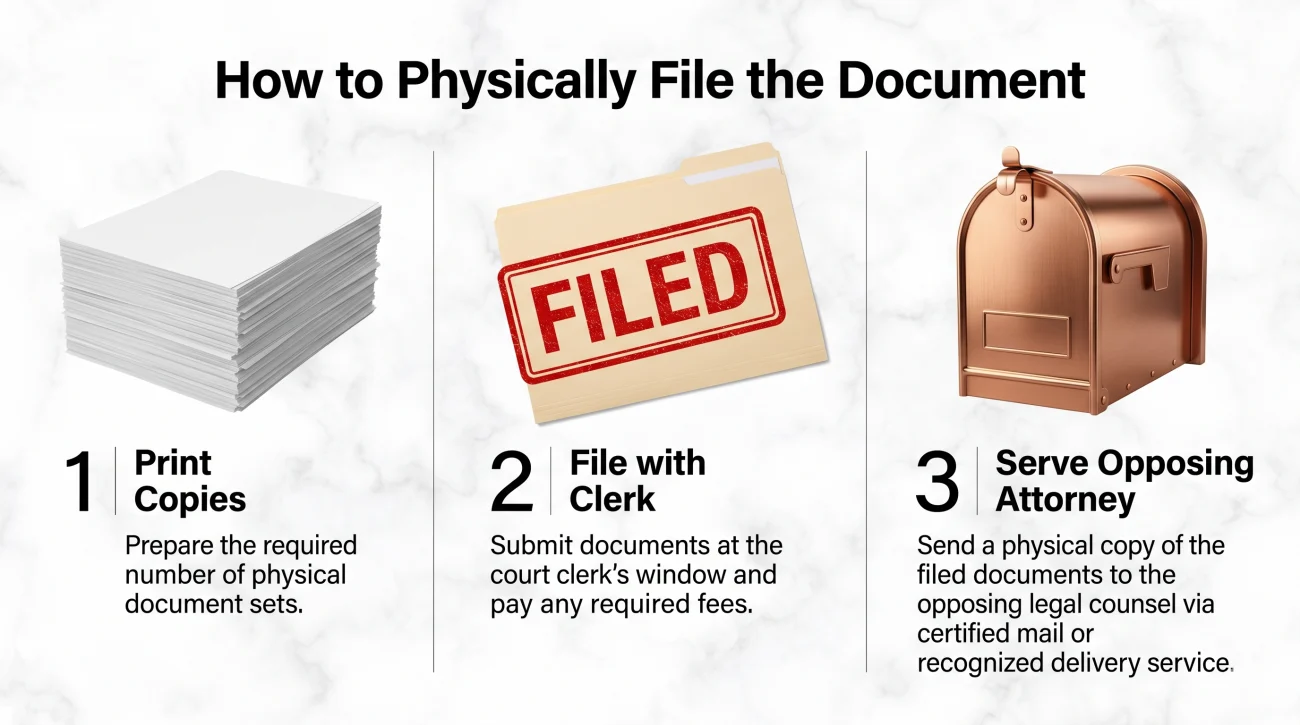

How to Physically File the Document

Once your document is formatted and signed, you have to get it into the legal system. Submitting it requires a specific sequence of steps, and missing the final step is a common mistake that can easily undo all your hard work.

Print copies + File with the court clerk + Serve the opposing attorney

First, make at least three copies of your completed and signed document. One is for the court, one is for the collector’s attorney, and one is for your personal records.

Second, take the original to the court clerk’s office listed on your summons. You can often mail it, but filing in person guarantees it arrives on time. When you hand it to the clerk, ask them to date-stamp your personal copy. That stamp is your bulletproof evidence that you met the deadline. Be aware that most courts charge a filing fee. If you cannot afford this fee, ask the clerk for a fee waiver application based on financial hardship.

Third, you must serve the opposing side. The court does not forward your response to the collector. You must mail a copy of your filed document to the attorney representing the debt collector. Their address will be prominently displayed on the summons and complaint. Send it via first-class mail, and keep a record of the date you mailed it.

In the agency, we loved it when a defendant forgot to serve our attorney. It meant we could often proceed to request a default judgment as if they hadn’t responded at all, forcing the consumer to fight backwards to prove they filed. Some courts explicitly require you to attach a “Certificate of Service” to your court filing swearing that you mailed this copy to prevent exactly this scenario.

Final Thoughts on Pushing Back

The system relies heavily on consumer fear and inaction. Debt collection litigation is designed to look intimidating, but when you strip away the legal formatting, a complaint is just a company asking a judge to give them your money based on the paperwork they provided.

Filing your Answer is how you step up to the table and demand accountability. It breaks the automated default cycle. It forces the debt buyer to spend time and resources they did not want to spend. Whether your ultimate goal is to force a dismissal because their documentation is flawed, or to negotiate a highly favorable settlement from a position of strength, none of it happens if you do not meet that deadline.

Read your summons, find your date, draft your response, and get it stamped by the clerk. That single action shifts the power dynamic entirely.

❓ FAQ

🗓️ How many days do I have to answer a debt collection lawsuit?

The exact timeline is written on the summons document you received. It varies by state and court type, but it is typically between 14 and 30 days from the date you were officially served.

⚖️ Do I absolutely need a lawyer to file my response?

No. Many consumers represent themselves in debt collection cases, especially in small claims or justice courts. However, if the balance is large or the case is complex, hiring a consumer protection attorney is highly recommended.

📞 Can I just call the collector to explain my situation instead of filing?

No. Calling the collector or their attorney does not stop the legal clock. If you do not file a written Answer with the court by the deadline, the collector can still obtain a default judgment against you, regardless of what was said on the phone.

💵 What does it cost to file an Answer?

Most courts charge a filing fee, which can range from $20 to over $200 depending on the jurisdiction. If you cannot afford the fee, you can request a fee waiver application from the court clerk based on financial hardship.

🚫 Can they garnish my wages just because they filed a lawsuit?

No. A lawsuit is just a claim. A collector cannot garnish your wages or freeze your bank account until they actually win the lawsuit and a judge grants them a court judgment. Filing an Answer is how you prevent them from winning automatically.

🤷♂️ What if I actually agree that I owe the money?

Even if you recognize the original debt, a debt buyer still has to prove they have the legal right to collect it and that their math is perfectly accurate. Filing a response forces them to prove ownership and prevents them from adding unauthorized fees.

📝 What is a Certificate of Service?

It is a brief statement you attach to your Answer, signed by you, swearing to the court that you mailed a copy of your response to the collector’s attorney on a specific date. Many courts require this to prove you notified the opposing side.

What each stage of litigation requires and where your leverage sits.

- What the lawsuit process looks like from summons to judgment

- What to file, when to file it, and what happens if you do not

- The legal arguments that can defeat a debt collection lawsuit

- What a default judgment allows collectors to do and how to fight one

- How to negotiate a resolution once litigation has started

Once judgment is entered, collectors gain tools they did not have before.

- The FDCPA violations collectors commonly commit during the collection process

- How to respond to a debt lawsuit and what defenses are available to you

- How a judgment becomes a garnishment order on your paycheck

- When a collector uses a judgment to freeze your bank account instead

- How to settle before the judgment turns into something harder to stop

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.