- Debt settlement ads promise massive reductions, but the reality involves strategic negotiation and accepting calculated risks.

- Collectors base their settlement decisions on account age, total balance, and your available funds, not just on your hardship story.

- Programs like Freedom Debt Relief and National Debt Relief are legitimate tools, but knowing if your specific creditors will negotiate requires a professional review.

The Ads Make It Sound Easy. It Is Not.

You have probably seen the ads. They promise to reduce your debt by half. They promise to stop the collection calls immediately. They make the process sound like a simple loophole that banks do not want you to know about.

I have been on the other side of those calls. For twelve years, I worked inside third-party collection agencies and a national debt buyer. I saw exactly what happens when debt settlement companies step in to negotiate on behalf of a consumer.

The truth is that these programs do work. But they do not work by magic. They work through leverage. The settlement company forces a standoff with the collector. Understanding how that standoff plays out is the only way to know if this path makes sense for your specific financial situation.

The Breaking Point of Unmanageable Debt

You are likely reading this because the math no longer works. The minimum payments are barely covering the interest. The letters are piling up on the counter. The collection calls are starting to escalate, interrupting your workday and causing constant stress. You feel entirely stuck.

Collectors know this. They are highly trained to recognize when a consumer is overwhelmed. They apply pressure exactly when you are feeling the most vulnerable.

In the agency, we knew exactly when a consumer was tapped out. We would watch the payment history. When someone started making partial payments or skipping months, that account was immediately flagged for escalation.

You need a way out. But you are rightly skeptical of companies promising to fix everything overnight. Before you make a decision, we need to look at what actually happens behind the scenes when you enroll in one of these programs.

How Debt Settlement Companies Actually Work

The marketing materials often skip the harsh mechanics of the process. If you want to understand if debt settlement companies are legit, you have to look at the raw process.

When you sign up, you stop paying your credit cards and unsecured loans. Instead, you make a single monthly payment into a dedicated escrow account that you control. As those funds build up, your actual credit accounts go further into default.

This sounds terrifying. It goes against everything you have been taught about personal finance. But it is the core strategy of debt relief companies. They are creating leverage.

Trying to negotiate a deep settlement while keeping your accounts perfectly current. The collector has zero incentive to accept less money if you are still making minimum payments.

Building a lump sum of cash while the account ages. This creates a scenario where the collector has to choose between a guaranteed cash payout today or a risky, expensive lawsuit tomorrow.

Once the escrow account has enough money, the settlement company contacts the collector. They make a lump sum offer. The collector then has to make a business decision.

What Makes a Collector Accept a Settlement

Why would a collector accept fifty cents on the dollar? Because they want a sure thing. A lawsuit costs money. Wage garnishment takes months or years to execute.

But they do not accept every offer. From inside the agency, I can tell you that the decision follows a strict formula. We rarely cared about a consumer’s personal hardship story. We cared about the numbers.

[Account Age] + [Current Balance] + [Creditor Litigation History] = [Settlement Leverage]

We looked at specific factors to determine if we should settle or sue.

| Factor | High Settlement Chance | High Lawsuit Risk |

|---|---|---|

| Account Age | Over 12 months past due | Just recently defaulted |

| Balance Size | Small to medium | Large (often over 10,000 dollars) |

| Account Owner | Third-party debt buyer | Original creditor known to litigate |

If your account is with a creditor known to sue quickly, trying to wait them out can backfire. This is exactly why you cannot guess your way through this process. You need to know how your specific creditors behave.

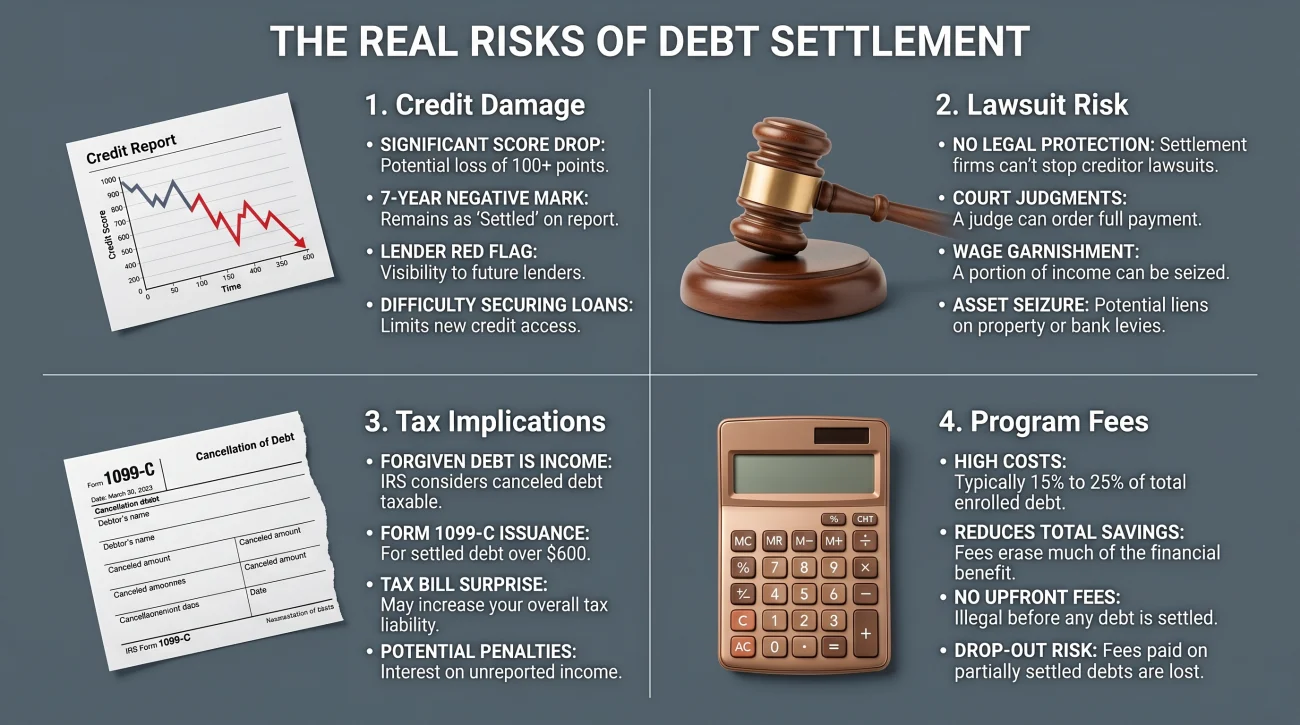

The Real Risks of Debt Settlement Programs

Are debt settlement programs worth it? They can be. But anyone telling you that debt settlement is a flawless process is not telling you the whole truth. You are intentionally defaulting on financial obligations. There are serious consequences.

- Credit score damage. Your score will drop significantly as accounts go into charge-off status. This is unavoidable.

- Lawsuit risk. A creditor might decide to file a lawsuit before a settlement is reached. If they sue, the dynamics change entirely.

- Tax implications. Forgiven debt over a certain amount may be considered taxable income by the IRS. You should always consult a tax professional about this.

- Program fees. Legitimate companies charge between 15 and 25 percent of the enrolled debt. They only collect this fee after a settlement is successfully reached and you approve it.

These risks do not mean settlement is a bad idea. They mean it is a calculated business decision. You are trading short-term credit damage for long-term financial relief.

Who Is a Good Candidate

Debt settlement is not for everyone. It is designed for specific financial profiles.

A good candidate has significant unsecured debt. They are already falling behind on payments. They cannot qualify for a low-interest consolidation loan, and they want to avoid filing for bankruptcy if possible.

A poor candidate is someone with mostly secured debt, like a car loan or a mortgage. Settlement companies cannot negotiate those. It is also the wrong choice for someone who is only slightly behind and needs to maintain a pristine credit score to buy a house next year.

⚠️ Warning: Do not enroll in a program if you only have a few thousand dollars in total debt. The fees and the credit damage will far outweigh the financial benefits.

If you have determined that settlement makes financial sense for your profile, the next question is who to trust with the negotiation. I have seen settlement offers from every major company cross the collection floor. Here is what I actually observed.

Major Debt Settlement Companies Reviewed

If you decide to move forward, you need to know who you are dealing with. People constantly search for debt settlement companies reviews trying to find the perfect fit. How do they stack up from the industry side?

| Company | Fee Range | Minimum Debt | Legal Support |

|---|---|---|---|

| National Debt Relief | 15 to 25 percent | 7,500 dollars | No |

| Freedom Debt Relief | 15 to 25 percent | 7,500 dollars | Yes |

| Accredited Debt Relief | Varies | 10,000 dollars | Varies by partner |

National Debt Relief Review

National Debt Relief is one of the largest in the space. Because of their massive size, they have established negotiating channels with almost every major creditor and collection agency.

When an offer came through from National Debt Relief, it carried weight on the collection floor. We knew they required clients to build actual funds in an escrow account before reaching out. We were not wasting time on empty promises. From a collector’s perspective, an NDR offer meant there was real money on the table right now, which made us much more likely to approve a deep reduction.

Freedom Debt Relief Review

Freedom Debt Relief operates similarly, but they offer one distinct advantage that matters heavily on the collection floor: they include a legal assistance feature.

If a creditor decides to sue you while you are enrolled in their program, Freedom provides legal support to help manage the litigation. This completely changes the cost-benefit analysis for the collector. If a file is borderline for a lawsuit, knowing the debtor has Freedom’s legal backing often tips the scale back toward taking the settlement. Litigating against a backed debtor is expensive, and agencies prefer the path of least resistance.

Accredited Debt Relief Review

Accredited Debt Relief has strong ratings and operates slightly differently by matching you with partner programs tailored to your profile.

Because they evaluate specific debt profiles before placing you, the offers we saw from their network were usually highly targeted. They do not just throw out lowball numbers to see what sticks. They tailor offers based on creditor behavior patterns rather than sending generic numbers, which often led to smoother, faster negotiations on the back end.

Taking the Next Step

You now know the risks. You know how the leverage works. You know what a collector is looking for when they review an account.

The missing piece is your specific situation. Will your specific mix of credit cards and medical bills settle easily? Or are you dealing with aggressive litigators who will reject standard offers?

The window before your creditor decides to litigate is finite. Find out where your accounts stand now before that decision is made for you.

Do not guess. Get a free debt consultation to find out if you are a candidate for settlement and what the realistic outcome looks like for your specific accounts.

Final Thoughts: Making the Decision

Dealing with debt collectors is exhausting. Debt settlement is a viable way to end the cycle, provided you go in with your eyes open. Do debt settlement companies really work? Yes, but they require patience and discipline.

Understand the timeline. Accept the temporary credit hit. And most importantly, do not try to predict how your individual creditors will react based on generic articles. Have an expert evaluate your financial profile before you commit to a strategy.

❓ FAQ

💼 Are debt settlement companies legit?

Yes, the major companies are highly regulated by federal agencies like the FTC. However, there are scams in the industry. Always look for companies that do not charge upfront fees before a settlement is reached.

📉 Do debt settlement companies really work?

They do work for consumers who complete the program. By withholding payments and building a lump sum, they create the leverage needed to negotiate significant balance reductions.

💳 Can I settle my own debt without a company?

Yes. You can contact your creditors directly to negotiate a settlement. However, doing it yourself requires significant time, negotiation skills, and a strong understanding of collection tactics.

⚖️ Can I be sued while in a debt settlement program?

Yes. Enrolling in a program does not stop a creditor from exercising their legal right to sue you for the default. This is a primary risk of the strategy.

⏱️ How long do these programs usually take?

Most programs run between 24 and 48 months. The timeline depends entirely on how much you owe and how quickly you can fund your escrow account.

💰 What happens to my credit score during settlement?

Your credit score will drop significantly. Because you must stop making payments to create leverage, your accounts will be reported as late and eventually charged off.

🏦 Do settlement programs cover student loans?

Usually not. These programs are designed for unsecured debt like credit cards and medical bills. Federal student loans and secured debts are generally excluded.

💸 Do I have to pay taxes on forgiven debt?

Often, yes. The IRS generally considers forgiven debt over 600 dollars as taxable income. You will receive a 1099-C form and should consult a tax professional.

🛑 Will enrolling stop collection calls?

Not immediately. Collectors will continue to call until they are legally notified of the representation, and some may still attempt contact depending on state laws.

📑 What is the difference between settlement and bankruptcy?

Settlement involves negotiating a lower payoff amount without court intervention. Bankruptcy is a legal process that can discharge debts entirely but has a much longer and more severe impact on your public record.

Four areas of the collection process. Start wherever your situation applies.

Some situations have deadlines attached. These pages are written for those situations.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.