- The exact number of days you have to respond is almost always printed directly on the summons document, not the complaint.

- Generic state tables found online are dangerous because your deadline changes based on your specific court type and how the papers were delivered.

- The clock starts ticking on the day you were officially served, not the date printed at the top of the legal paperwork.

- If you miss this exact date, the collector can automatically win a default judgment regardless of whether you actually owe the money.

The Most Consequential Date in Your Collection Case

A stack of court papers just landed on your kitchen counter. Maybe a process server handed them to you at the front door, or maybe you signed for a certified letter at the post office. Your name is on a lawsuit, and panic is likely setting in. You need to know your debt collection lawsuit deadline immediately, but the documents seem intentionally confusing.

During my 12 years working inside third-party collection agencies and a national debt buyer, I saw exactly how the litigation machine operates. We filed hundreds of lawsuits a week, and the entire business model was built on a single, highly predictable outcome. We expected 70 to 90 percent of consumers to simply miss their response window. When they missed that window, we won by default.

You do not need to be a lawyer to beat the clock, but you do need to understand where to look. People waste precious days searching the internet for generic state rules when the exact answer is already sitting in their hands. Knowing exactly how many days to respond to a debt collection summons is the absolute first step in shifting the power dynamic back to your side.

The Fastest Way to Find Your Exact Deadline

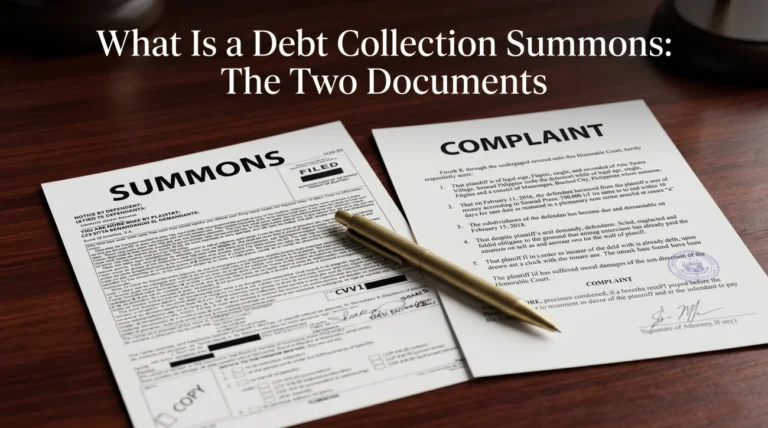

When consumers receive legal papers, they almost always focus on the wrong page. They flip straight to the document that lists the dollar amount, the creditor’s name, and the allegations against them. That document is called the complaint. It is designed to look intimidating, but it rarely tells you when your response is due.

To find your debt lawsuit deadline, you must look at the cover sheet. This document is the summons. It is a procedural notice from the court telling you that you are officially being sued and outlining your strict requirements for answering.

When our firm sent out lawsuit packets, the complaint was often thick with account histories and legal claims designed to overwhelm the reader. The actual deadline was buried on the single-page summons at the very front. Consumers would read the complaint, panic about the balance, set the packet aside to deal with ‘later,’ and completely miss the 14-day clock ticking on the cover sheet.

Look for a section on the summons that uses language similar to this:

Sometimes, instead of a number of days, the summons will state a specific “return date” or a scheduled hearing date. If a specific date and time are printed, that is your hard deadline to appear or file your paperwork. Understanding the difference between these documents is critical to protecting your rights. You can learn more about dissecting these papers in our guide covering what is a debt collection summons.

Why Generic State Deadline Tables Will Mislead You

If you search online for a debt collection response deadline by state, you will find dozens of charts. They might say that residents of your state have 30 days to answer a civil lawsuit. Relying on these generic charts is one of the most common ways consumers end up losing by default.

The reality is that your specific response window is determined by three interacting variables, not just your state line. This is a framework debt collectors understand perfectly, but defendants rarely do.

Variable 1: The Specific Court Type

Every state has a hierarchy of courts. The rules in a general civil court are vastly different from the rules in a small claims, justice, or magistrate court. Debt buyers deliberately file in lower courts whenever possible because the filing fees are cheap and the procedures are accelerated.

- General Civil Courts: These typically handle larger balances. Deadlines are most commonly 20 to 30 days.

- Small Claims and Justice Courts: These handle lower balances and are designed for speed. In many states, a justice court gives you only 14 days to respond.

- Federal Court: Very rare for standard consumer debt, but the deadline is uniformly 21 days from service across all states.

If you live in a state where the civil court allows 30 days, but your specific case was filed in a justice court requiring a 14-day response, a generic online table will cause you to miss your window by over two weeks.

Variable 2: The Method of Service

How the paperwork physically reached you changes the math. “Service of process” is the legal term for delivering the lawsuit. The clock does not always start the moment the papers leave the process server’s hands.

Personal delivery directly to you usually starts the clock immediately on that exact day. However, if the server left the papers with another adult at your home (known as substituted service), many states add a grace period. For example, some jurisdictions give you an extra 10 days to respond if the papers were left with a roommate and then mailed to you, acknowledging that it takes time for the documents to actually reach your hands.

If you were served by certified mail, which is legal in some jurisdictions for small claims, the clock might start on the day you sign the green receipt card, or it might include an additional 3 to 5 days built into the local court rules to account for postal delays.

Variable 3: The State Rules

Finally, the state itself dictates the baseline timeframe. For example, Texas standardizes civil responses to the Monday next after the expiration of 20 days, while New York might give you 20 or 30 days depending on how you were served. But as you can see from the first two variables, the state rule is only the starting point. The court clerk who issued your summons already combined your state’s baseline, your specific court type, and your method of service to calculate the exact date printed on your paperwork.

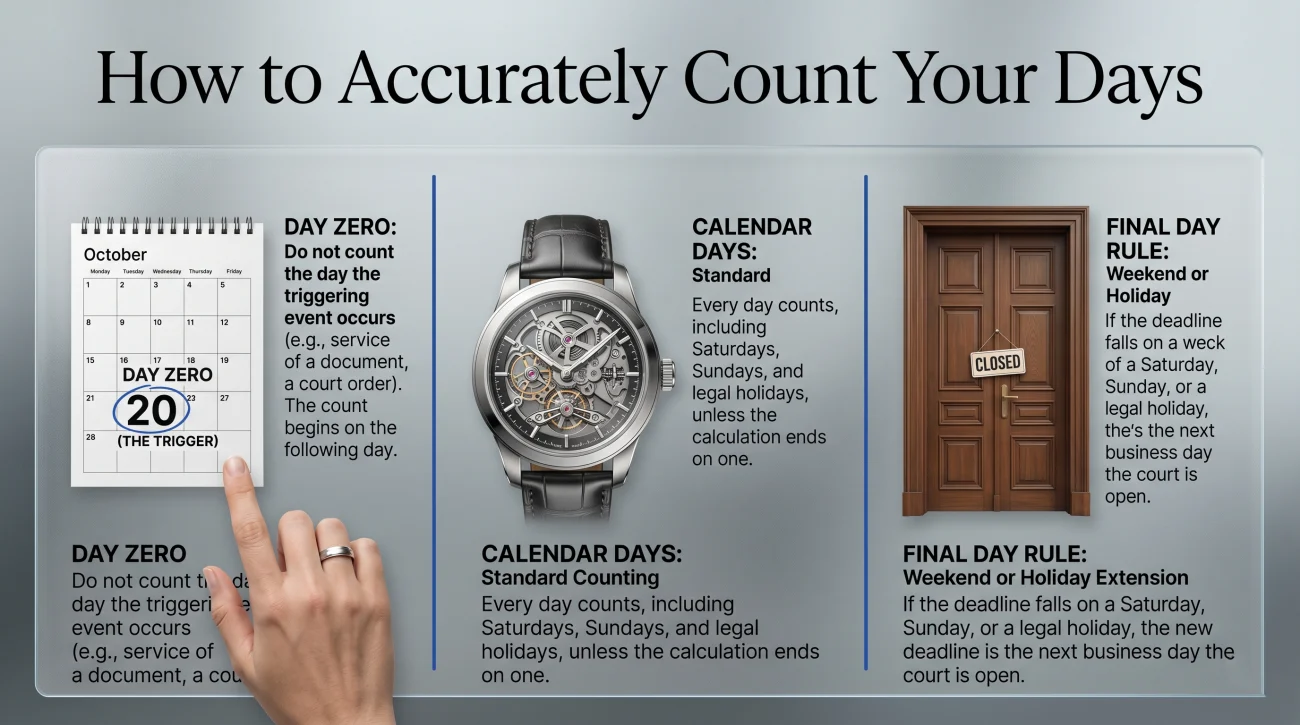

How to Accurately Count Your Days

Once you know you have a certain number of days, you have to count them correctly. A miscalculation of a single day is fatal to your defense. Here is how courts generally calculate time.

Day Zero is the day you were served. Do not count the day the papers were handed to you as Day 1. The clock starts the next morning. If you are handed papers on a Tuesday, Wednesday is Day 1.

Count calendar days, not business days. Unless your specific court rules state otherwise, every single day counts. Saturdays, Sundays, and holidays are all included in your total. A 20-day deadline is 20 calendar days.

The final day rule. What happens if Day 20 lands on a Saturday, a Sunday, or a legal court holiday? In almost every jurisdiction, the deadline rolls over to the end of the next business day when the court is open. If your deadline hits on a Sunday, you typically have until the clerk’s office closes on Monday to file your paperwork.

Looking at the date printed at the top of the complaint (e.g., “Filed March 1st”), adding 30 business days, and assuming you have until late April to respond.

Noting that the process server handed you the papers on March 15th, making March 16th Day 1. Counting 20 calendar days forward to find the exact April date your response must be physically stamped by the court.

Do not confuse the response deadline with a trial date. Filing an answer is simply sending a formal document back to the court saying you intend to fight. It is not the day you show up to argue your case in front of a judge. You must secure your place in line before the real battle begins. If you are unsure of how to format this document, you can review the mechanics in our guide on how to write an answer to a debt collection lawsuit.

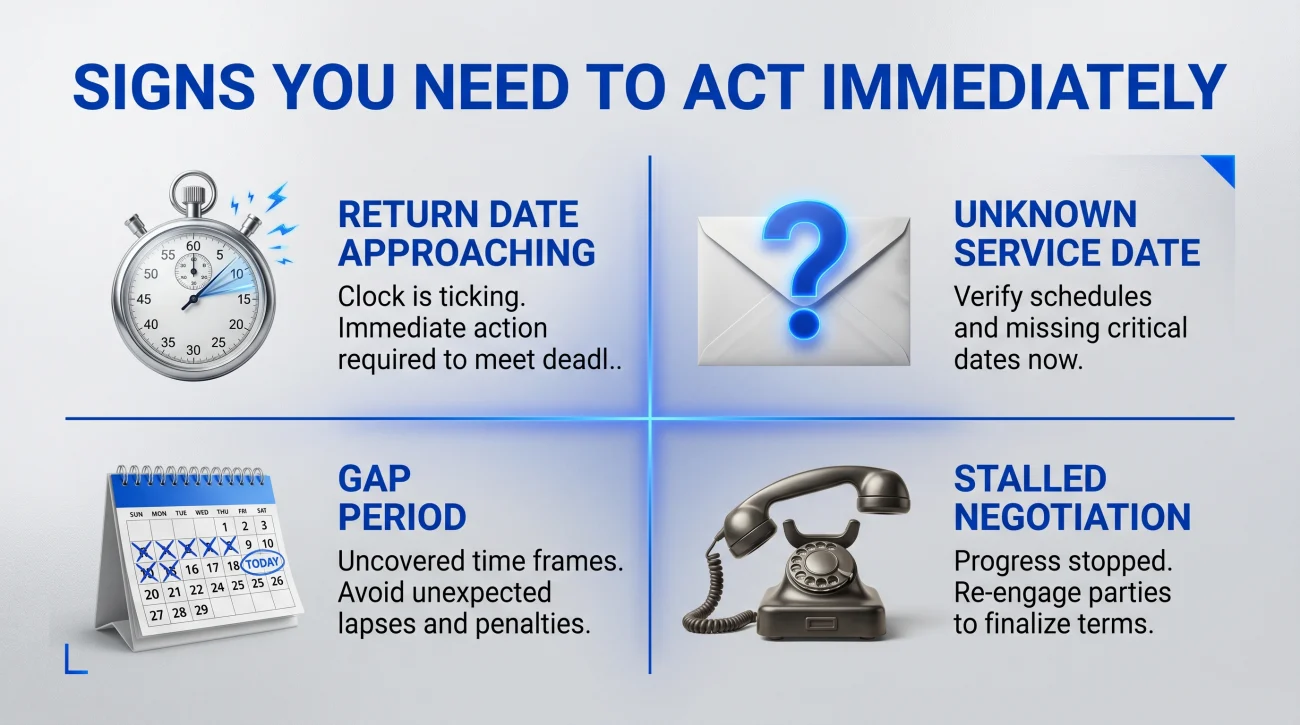

Signs You Need to Act Immediately

Time is the only resource you cannot get back in a collection case. If you are reading this, you are likely already on the clock. You are in the danger zone and need to take immediate action if any of the following apply to your situation.

- The summons lists a specific “return date” that is less than 5 days away – meaning your window is closing regardless of when you were served.

- You discovered the paperwork left with a roommate or family member, and you cannot verify the exact date the process server dropped it off (meaning your Day Zero is a mystery).

- The response deadline on the paperwork has already passed, but you haven’t received a notice of default judgment yet (you are in the critical, narrow gap period).

- You are attempting to negotiate a settlement over the phone, and the 14-to-30 day clock is running out while you wait for their “manager’s approval.”

When the window is closing, trying to figure out the legal system alone is a massive risk. This is the exact moment when bringing in professional help can save your case from an automatic loss. If you are feeling the pressure of a shrinking timeline, you need to consider bringing in a consumer attorney to protect your rights before the clock runs out.

What to Do When the Summons Is Confusing

Sometimes the paperwork is flawed. Occasionally, a debt buyer’s law firm will serve a summons with a blank space where the deadline should be, or the text is so poorly photocopied it cannot be read. You cannot ignore the lawsuit just because the paperwork is sloppy. The court still expects a response.

Your absolute best resource in this scenario is the court clerk. The name, address, and phone number of the court where the lawsuit was filed will be printed at the top of the summons. Call them.

Court clerks are incredibly helpful, but they operate under strict rules. They are allowed to give you procedural information, but they are strictly forbidden from giving you legal advice. You have to ask the right questions.

Key Point: Do not ask the clerk, “What should I do about this debt?” They cannot answer that. Ask them, “I am the defendant in case number 12345. I was served on Tuesday the 12th. Can you confirm the exact date my answer must be filed with the court?”

The clerk can look at the docket, see when the process server filed the proof of service, and tell you exactly what date the court computer shows as your deadline. Write this date down, get the name of the clerk you spoke with, and treat that date as law.

What Happens If You Already Missed the Deadline?

Many consumers discover a stack of mail, realize they missed their debt collection lawsuit response time by a few days, and simply give up. They assume a missed deadline means the police will show up or their bank account will be drained by morning. The reality of the court system is much slower.

Missing the deadline does not automatically generate a judgment the very next second. It simply gives the debt collector the right to request a default judgment from the judge. There is a procedural gap between the moment your deadline passes and the moment the judge actually signs the final order.

⚠️ Warning: If you realize you missed your deadline by just a few days, drop everything and file your answer at the courthouse immediately. In many jurisdictions, if the collector’s attorney has not yet filed the paperwork requesting the default, the court will still accept your late response. Do not self-reject.

If the collector has already moved quickly and the court has entered an official default judgment, the rules change entirely. You can no longer file a simple answer. You must now file a specialized motion asking the judge to undo the judgment, which requires proving you had a legally valid excuse for missing the deadline. It is a steeper hill to climb, but not impossible.

A missed deadline is terrifying, but the entire legal process is built to handle defendants who do not know the rules. If you are terrified that you cannot afford legal help, you should explore what it realistically takes to respond to a debt lawsuit without an attorney, but do so quickly.

Final Thoughts: Do Not Wait Until the Last Minute

Finding your deadline is the easy part. Beating it requires discipline. If your summons says you have 20 days, do not plan to file your paperwork on day 19. Mail gets delayed. Courthouses close early for emergencies. Printers run out of ink.

In the collection industry, we counted on procrastination. We knew that human nature makes people want to avoid dealing with stressful financial problems. We baked that avoidance right into our revenue projections. The most effective way to protect your paycheck and your bank account from garnishment is to file your response the first week you receive the papers. Read the summons, mark the calendar, and get your answer stamped by the court.

Taking action immediately stops the collector’s easiest path to victory. But filing your Answer is just getting in line – it is what comes next that decides the outcome. Once you prevent a default, you force the collector to actually prove their case.

If you are wondering what happens after you assert your rights, you can expect the case to move toward discovery or a hearing – read about what happens after answering a debt lawsuit. If you missed the window entirely and they won by default, they now have the power to pursue wage garnishments and bank levies; see our guide on debt collection default judgments to see if you can undo it. Or, if you suspect you were never properly served in the first place, you might have grounds to challenge it based on improper service.

❓ FAQ

🗓️ How many days do I have to respond to a debt collection summons?

The timeframe is typically 14 to 30 days, depending on your state and whether you are in small claims or civil court. The exact number is printed directly on your summons document. Do not guess; read the cover page of your paperwork.

⏱️ When does the clock actually start for my lawsuit response?

The clock begins the day after you are officially served with the papers. It does not start on the date the complaint was typed or the date the court stamped the initial filing. Day one is the morning after the papers were legally delivered to you.

📅 Does the debt lawsuit deadline include weekends?

Yes. Courts calculate these deadlines using calendar days, not business days. You must count Saturdays, Sundays, and holidays. However, if your final deadline day lands on a weekend or holiday, the court usually extends it to the next open business day.

📬 What if I was never served but found out about the lawsuit?

If you discover a lawsuit against you but were never properly served, the deadline clock technically may not have started. However, you should not ignore it. You must file a response raising “improper service” as a defense to prevent a default judgment from being entered behind your back.

🏛️ Can I ask the court clerk for more time to respond?

Court clerks cannot grant extensions. If you need more time, you must formally file a motion with the judge asking for an extension before your original deadline passes. In debt collection cases, it is usually faster and safer to simply file a basic Answer on time.

📝 What happens if I miss the debt lawsuit deadline by one day?

If the collector’s attorney has not yet filed a motion requesting a default judgment, many courts will still accept a late Answer. You should file your paperwork immediately. Do not give up just because you are 24 hours late.

📞 Will calling the debt collector pause my response deadline?

No. Calling the collector or their attorney to negotiate a settlement does not stop the legal clock. The only way to stop a default judgment is to file a written Answer with the court. Always file first, then negotiate.

✉️ If I mail my response, does it need to arrive by the deadline?

In most courts, yes. The clerk must physically receive and stamp your Answer by the deadline date. The “mailbox rule” (where the postmark date counts) does not apply in all jurisdictions for initial responses. It is highly recommended to file in person or use an electronic filing portal if available.

🗂️ Are the response deadlines different for credit card debt versus medical debt?

No. The procedural deadline is based on the court rules for civil lawsuits in your jurisdiction, not the type of debt you owe. A $500 medical bill and a $10,000 credit card lawsuit filed in the same court will have the same response timeframe.

⚖️ Do I have to pay the debt when I file my response?

No. Filing an Answer is simply a procedural step to tell the court you are defending yourself. You do not have to pay the debt to file. You may, however, have to pay a small court filing fee to submit your paperwork, though fee waivers are available for low-income defendants.

What each stage of litigation requires and where your leverage sits.

- What the lawsuit process looks like from summons to judgment

- What to file, when to file it, and what happens if you do not

- The legal arguments that can defeat a debt collection lawsuit

- What a default judgment allows collectors to do and how to fight one

- How to negotiate a resolution once litigation has started

Once judgment is entered, collectors gain tools they did not have before.

- The FDCPA violations collectors commonly commit during the collection process

- How to respond to a debt lawsuit and what defenses are available to you

- How a judgment becomes a garnishment order on your paycheck

- When a collector uses a judgment to freeze your bank account instead

- How to settle before the judgment turns into something harder to stop

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.