- Filing an Answer does not end the lawsuit, but it successfully prevents an automatic default judgment against you.

- Your case will generally take one of four paths next: a settlement offer, a court hearing, formal discovery, or a voluntary dismissal by the collector.

- Debt buyers frequently abandon lawsuits (voluntary dismissal) when a defendant responds, especially if the collector lacks the original account documentation.

The Waiting Period After Your Answer Is Filed

Dropping your legal response in the mail or handing it to the court clerk often brings a massive sense of relief. You met the deadline. You did what you were supposed to do. But almost immediately, a new kind of anxiety sets in as you wonder what happens after answering a debt lawsuit.

Many people assume that once the court has their document, a judge will read it, see their side of the story, and cancel the case. That is not how the civil court system works. Filing your Answer does not end the litigation. Instead, it is the exact moment the case becomes real.

During my years working inside third-party collection agencies and a national debt buyer, I saw the backend of this process daily. Debt collection law firms file hundreds of lawsuits a week expecting 70 to 90 percent of people to ignore them. When you file an Answer, you break their business model. You move from the “easy default” pile into the “active litigation” pile. Understanding what happens when you are sued by a debt collector helps you anticipate their next move.

Once your paperwork is processed, the collector’s legal team has to make a choice. Depending on the strength of their evidence and the policies of their agency, your case is now heading down one of four specific paths.

Path 1: The Settlement Offer

This is the most common outcome, particularly if you are being sued by a debt buyer rather than your original credit card company. After receiving your filed Answer, the collector’s attorney may reach out to negotiate a settlement.

To understand why this happens, you have to look at their cost calculation. Before you responded, the collector expected to win by default. They spent a small filing fee and assumed they would get a judgment allowing them to garnish your wages. By filing an Answer, you proved that you will not default. Taking a contested case to trial requires hours of attorney time. For a debt buyer who purchased your account for pennies on the dollar, paying an attorney to argue in court over a $3,000 balance is often a losing financial proposition.

“In my time reviewing accounts for litigation, the receipt of a filed Answer with a general denial almost always triggered a settlement review. The firm’s goal was to close the file profitably, and an early settlement was much cheaper than paying an attorney to prepare for trial.”

If they reach out, you will typically receive a letter or a phone call offering to settle the balance for a reduced lump sum or offering a payment plan. You are not required to accept their first offer. Because you filed an Answer, you now have leverage that you did not have before.

Path 2: A Pretrial Conference or Hearing is Scheduled

Depending on your state and whether your case is in small claims or civil court, the court may automatically schedule a date for both parties to appear. You will receive a notice in the mail indicating the date, time, and location of a hearing or pretrial conference.

This is usually not the final trial. A pretrial conference is often a brief meeting where the judge or a mediator assesses the case, asks if the parties have tried to settle, and sets a schedule for the rest of the litigation. In small claims court, the hearing might be the actual trial, but it is typically informal. It takes place in a standard room, there is no jury, and it often lasts less than twenty minutes.

You do not need to wear a suit to these informal hearings, but you should dress neatly. When the judge speaks to you, keep your answers brief, factual, and focused on your defenses. Do not argue with the collector’s attorney. Direct your statements to the judge and simply repeat that you are requiring the plaintiff to prove their case.

If you receive a notice for any court date, you must attend. Failing to appear after you have filed an Answer can result in a judgment being entered against you anyway. You can learn exactly what to bring and how to act to prepare for a collection hearing in our dedicated guide.

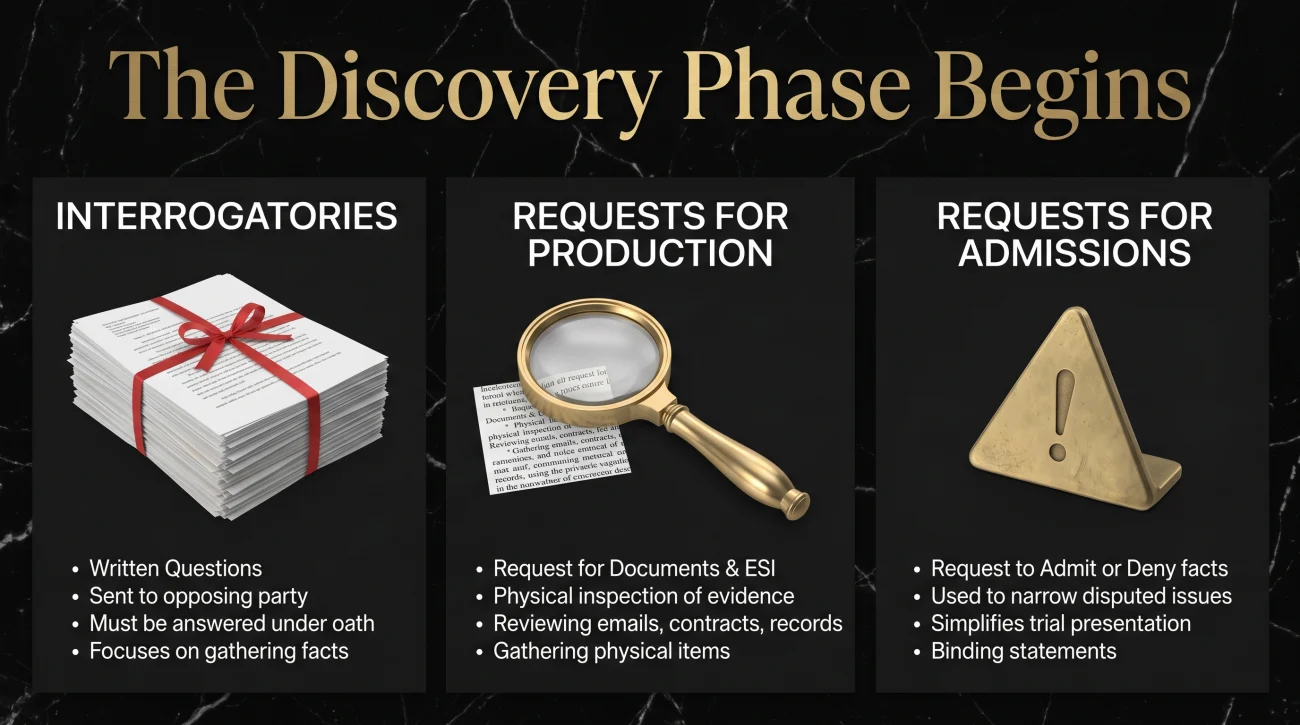

Path 3: The Discovery Phase Begins

If the collector intends to push the case forward, their next step is typically the discovery phase. This is the formal legal process where both sides exchange information and evidence before a trial. You will receive a thick packet of paperwork in the mail from the collector’s attorney.

This packet is designed to be intimidating. It will likely contain interrogatories (written questions you must answer under oath) and requests for production (demands for documents like bank statements or payment records). You must respond to this paperwork within the strict deadline, usually 28 to 30 days.

⚠️ Warning: The most dangerous document in a discovery packet is called a Request for Admissions. This is a list of statements, such as “Admit that you owe the Plaintiff $5,000.” If you do not respond to this specific document by the deadline, the court automatically assumes you admit every statement is true. The collector will then use your silence to win the case immediately.

Discovery is not a one-way street. You have the right to send your own formal discovery requests to the collector. You can demand that they produce the original signed credit agreement, a complete chain of title showing they own the debt, and a full itemization of the balance. Many debt buyers cannot produce these documents.

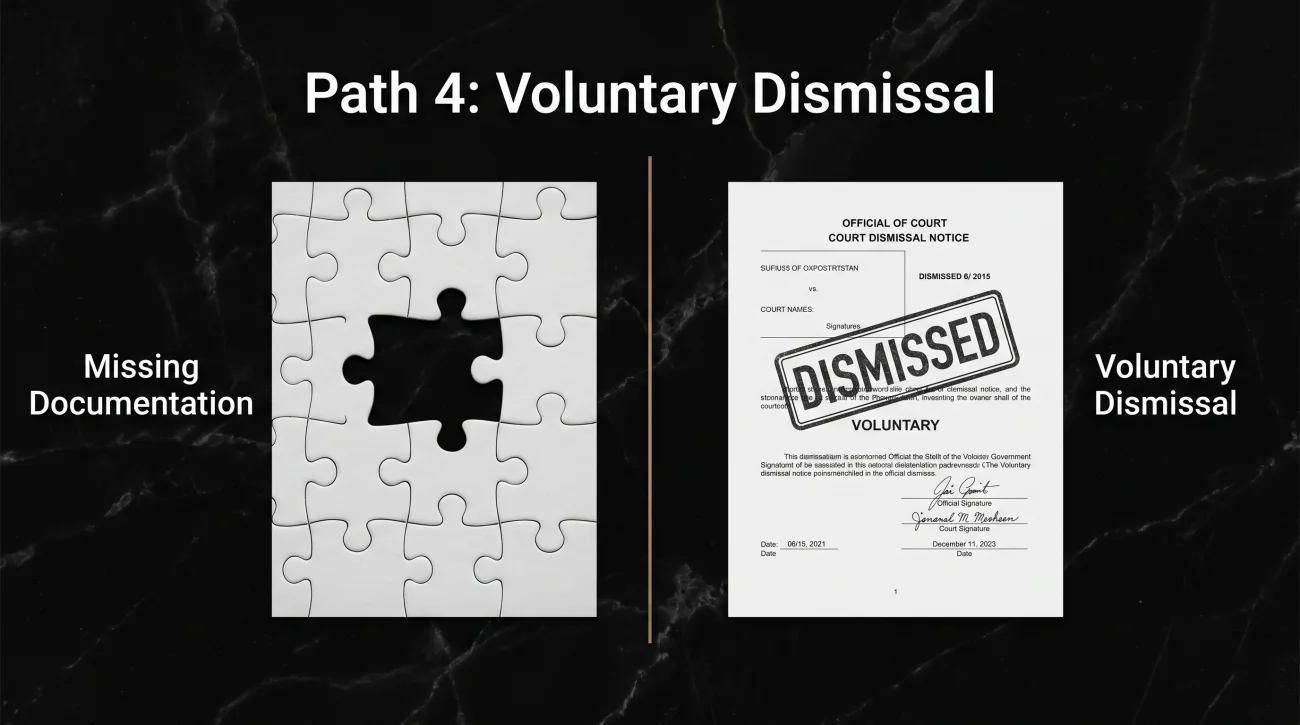

Path 4: Voluntary Dismissal

This is the outcome that most people do not know exists, but it happens frequently in the collection industry. After you file your Answer, the collector’s attorney reviews the file. They look for the original contract. They look for the bills of sale connecting the original bank to their client. If the documentation is missing or flawed, they know they cannot win at trial.

Instead of going to court and losing, the collector simply files a “Notice of Voluntary Dismissal” with the court. The lawsuit is dropped. The calls stop. You receive a copy of the dismissal in the mail.

Debt buyer law firms evaluate each case against litigation costs after an Answer is received. Accounts with documentation problems, small balances, or accounts that are very old are frequently abandoned at this stage. This is exactly why your initial response matters so much. A basic Answer to a debt lawsuit forces them to check their own paperwork, and often, they find that their documentation is not good enough to proceed.

Realistic Timelines and What to Do While You Wait

The legal system moves slowly. After you file your Answer, weeks or even months might pass with absolute silence. This is normal. It does not mean the case was dismissed, and it does not mean they forgot about you.

In small claims or justice courts, cases typically move faster, and you might receive a hearing date within 30 to 90 days. In general civil court, contested cases can take anywhere from 6 to 18 months to resolve. While you wait, you need to establish a strict documentation discipline.

- 📌 Check your mail daily for court notices.

- 📋 Keep physical and digital copies of everything you send or receive.

- 💻 Monitor the online court docket to track your case status.

You can usually check the status of your case online through your county clerk’s website. Search for your case number once a week. This ensures that you do not miss any filed motions or scheduled hearings if a piece of mail gets lost.

If the collector takes absolutely no action for several months after you file your Answer, the court itself may eventually dismiss the case for “want of prosecution” or “lack of prosecution.” However, always assume the case is active until you have a document from the court explicitly stating that it has been dismissed.

Signs Your Case is Heading Toward a Resolution

Waiting for the next step is stressful, especially when you do not know how to interpret the silence or the letters you receive. In most cases, certain patterns indicate that the leverage is shifting in your favor.

- 🤝 The collector’s attorney reached out with a settlement offer shortly after your Answer was filed. This means your response successfully shifted their cost calculation. They now prefer a quick deal over an expensive trial.

- ⏳ There has been no activity on the court docket for 60 or more days since you filed. This often indicates the collector’s firm is struggling to locate the original account documents required to move the case forward.

- 📑 You sent discovery requests demanding the original contract, and the deadline has passed without them providing it. When a debt buyer cannot produce the contract, their legal ability to win a judgment severely collapses.

- ✅ You received a Notice of Voluntary Dismissal from the court. This is the ultimate win. They evaluated your defenses and chose to walk away rather than risk losing in front of a judge.

If you have received a settlement offer, or if your case is actively moving into the discovery phase and you are unsure how to answer their legal questions, you need to evaluate your next steps carefully. A misstep in discovery can ruin a good defense. If you are dealing with a large balance or feel overwhelmed by court documents, finding professional representation for a debt lawsuit can level the playing field and protect you from procedural traps.

Final Thoughts on the Post-Answer Process

Filing your Answer was the critical first step to protecting yourself from an automatic loss. However, you must remain vigilant. Whether the case ends in a settlement, proceeds to a hearing, or is quietly dismissed by the collector, you are now a participant in a legal process.

Stay on top of every piece of mail from the court or the opposing attorney. If you are ever unsure whether you completed the filing process correctly, call the court clerk to verify that your Answer is on the docket. Keep your documents organized, show up to any scheduled dates, and remember that you have already taken the hardest step. By answering the lawsuit, you forced the collector to play by the rules instead of winning by default.

❓ FAQ

⏳ How long after I file an Answer will I hear back?

It depends heavily on the court and the collector. In small claims court, you might receive a hearing notice within a few weeks. In civil court, it is common to hear nothing for 30 to 60 days. Monitor your mail and the online court docket regularly.

📞 Can the debt collector still call me after I file an Answer?

Once a lawsuit is filed and you have responded, communication should generally go through the attorneys. If the collector is represented by a law firm, their firm will contact you. If an agency continues to harass you by phone during an active lawsuit, log the calls carefully.

⚖️ Does filing an Answer mean I definitely have to go to a trial?

No. Most debt collection lawsuits never reach a formal trial. They are frequently resolved through negotiated settlements, voluntary dismissals by the collector, or rulings based on written motions before a trial date is ever needed.

🗂️ What is a Request for Admissions?

It is a legal document sent during the discovery phase asking you to admit or deny specific facts, such as “Admit you owe this exact balance.” If you fail to respond to this document within the legal deadline, the court treats your silence as an admission that the statements are true.

❌ What happens if I miss a court date after filing my Answer?

The judge will likely strike your Answer and enter a default judgment against you, causing you to lose the case automatically.

🤝 Should I reach out to settle, or wait for them?

There is no strict rule, as it depends on your leverage. If you recognize the debt and have a lump sum available, reaching out to the plaintiff’s attorney early can initiate a fast resolution. On the other hand, if you raised strong defenses based on the collector’s documentation gaps, waiting to see if they offer a low settlement or dismiss the case entirely is often the stronger strategic move.

📫 How do I know if the collector voluntarily dismissed the case?

You will receive a document in the mail, usually titled “Notice of Voluntary Dismissal” or “Stipulation of Dismissal.” You can also confirm this by checking your case status on the court clerk’s online portal.

What each stage of litigation requires and where your leverage sits.

- What the lawsuit process looks like from summons to judgment

- What to file, when to file it, and what happens if you do not

- The legal arguments that can defeat a debt collection lawsuit

- What a default judgment allows collectors to do and how to fight one

- How to negotiate a resolution once litigation has started

Once judgment is entered, collectors gain tools they did not have before.

- The FDCPA violations collectors commonly commit during the collection process

- How to respond to a debt lawsuit and what defenses are available to you

- How a judgment becomes a garnishment order on your paycheck

- When a collector uses a judgment to freeze your bank account instead

- How to settle before the judgment turns into something harder to stop

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.