- A general denial does not mean you are claiming the debt is entirely fake. It is a legal mechanism that forces the collector to prove their claims with actual documentation.

- Filing a general denial shifts the burden of proof back to the plaintiff, preventing a default judgment and buying you time to build a complete defense strategy.

- While highly effective for the main lawsuit complaint, a general denial does not automatically respond to Requests for Admissions, which must be answered individually to avoid losing your case on a technicality.

The Power of Forcing the Collector to Prove Their Case

During my twelve years working inside collection agencies and debt buying firms, I watched how litigation departments processed incoming mail. When a consumer responded to a lawsuit with a detailed, emotional letter explaining why they fell behind on payments, the collection attorneys mentally marked it as an easy win. The consumer had essentially admitted the debt was valid. But when an envelope arrived containing a simple, properly formatted general denial, the entire dynamic of the file changed immediately.

A general denial stops the debt collection assembly line in its tracks. Most debt buyer lawsuits are filed based on thin spreadsheets containing nothing more than names, addresses, and balances. The business model relies on the assumption that you will either ignore the lawsuit entirely or admit that you owe the money. When you file a general denial, you reject both of those assumptions. You are standing up in the legal process and saying, “I am here, I am defending myself, and I demand that you prove everything you just claimed.”

Understanding what this document actually does, and just as importantly, understanding what it does not do, is critical. A general denial is not a magic wand that makes a valid debt disappear, but it is often the most strategic first move a consumer can make when facing a litigation firm that is unprepared to actually litigate.

The Perjury Fear: Why Consumers Are Afraid to Deny

The single biggest hurdle most people face when considering a general denial is the fear of committing perjury. I have spoken to countless consumers who look at a lawsuit complaint, see a balance from an old credit card they vaguely remember having, and freeze. They think, “I know I had a card with that bank five years ago. If I submit a legal document denying the lawsuit, am I lying to a judge?”

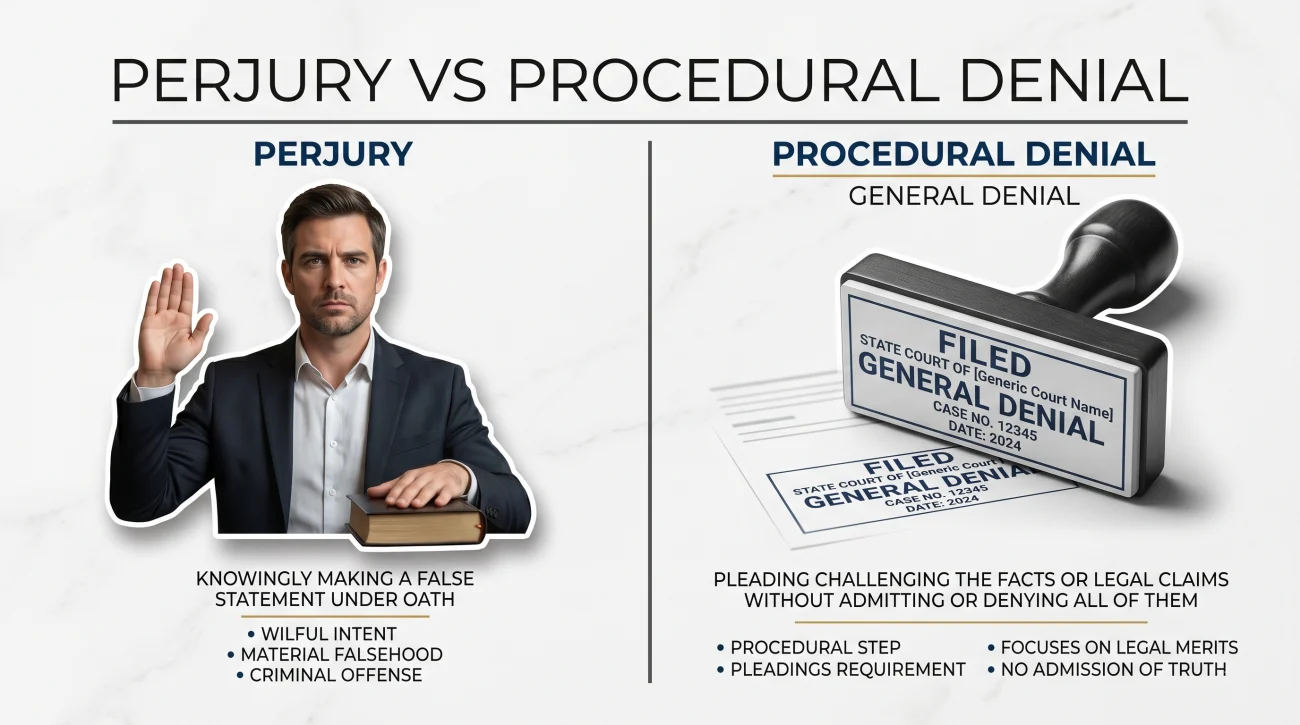

This is a fundamental misunderstanding of how the civil legal system operates. A general denial is not a sworn statement that the debt is a complete fabrication. It is a procedural tool. When you file a general denial, you are not saying, “I have never heard of this bank.” You are legally stating, “I do not accept your unproven allegations as fact, and I require you to meet your legal burden of proving them.”

“A common field observation from debt collection litigation: Collectors rely heavily on the consumer’s fear of the courtroom. They want you to believe that unless you can prove you don’t owe the debt, you have no right to defend yourself. In reality, the exact opposite is true. The collector filed the lawsuit. The law requires them to prove it.”

In a civil lawsuit, the plaintiff bears the absolute burden of proof. The debt buyer must prove they own the specific account, they must prove the exact dollar amount is accurate to the penny, and they must prove they have the legal right to collect it. By submitting a general denial, you are simply holding them to the standard that the law already demands. You are not committing perjury by requiring a plaintiff to do their job.

What a General Denial Actually Is

When you are sued, the collector serves you with a complaint. The complaint is a numbered list of allegations. For example, Paragraph 1 might state who the plaintiff is, Paragraph 2 might state that you opened an account, and Paragraph 3 might state the balance you allegedly owe. The documents you received in the mail serve two different functions, and understanding the difference between the summons and the complaint is your first step in breaking down their claims.

To respond to the complaint, you must file an Answer. You generally have two ways to format this Answer: a specific denial or a general denial.

Going through the complaint line by line. “Defendant admits Paragraph 1. Defendant denies Paragraph 2. Defendant lacks sufficient information to admit or deny Paragraph 3.”

Using one blanket statement to reject the entirety of the plaintiff’s claims in a single sentence, forcing them to prove every single element of their case from scratch.

In many jurisdictions, a general denial is explicitly authorized by court rules. For example, many states explicitly authorize a general denial in consumer debt cases through their civil procedure rules. It is fast, it is legally sufficient in most standard debt buyer cases, and it leaves no room for accidental admissions.

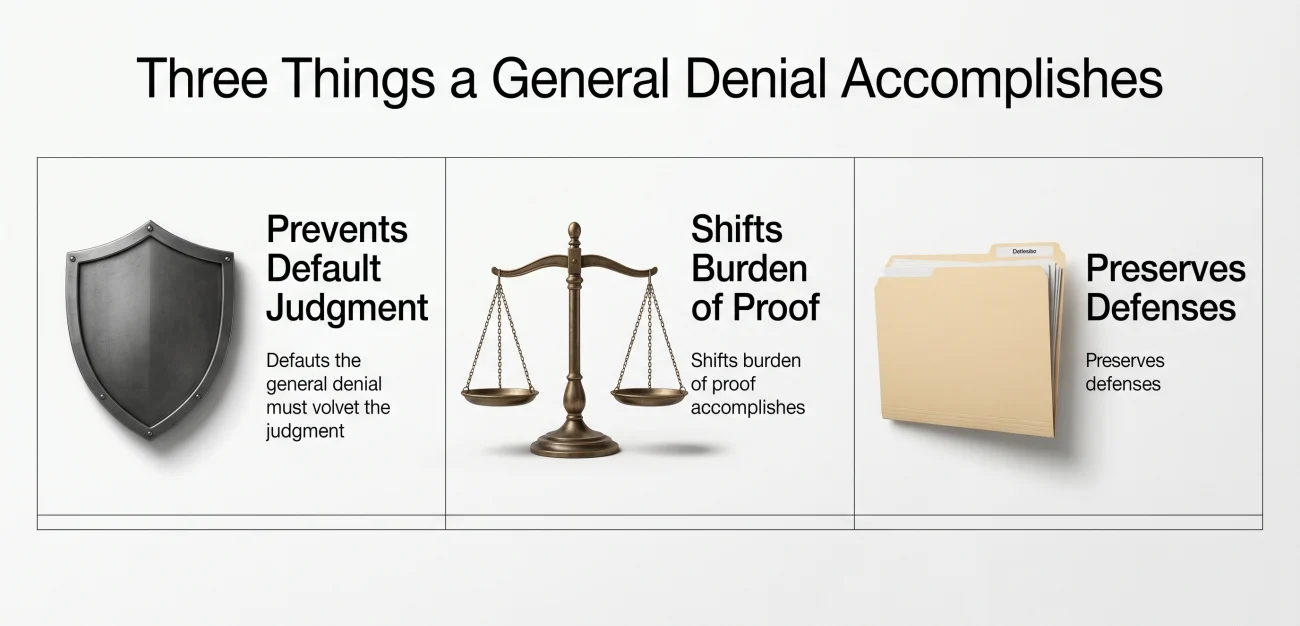

The Three Things a General Denial Accomplishes

Filing this document changes the trajectory of the lawsuit immediately. Once the court clerk stamps your general denial, three specific legal shifts occur.

1. It Prevents a Default Judgment

This is the most critical immediate benefit. The vast majority of debt collection lawsuits are filed with the expectation that you will ignore them. If you do nothing, the collector asks the judge for a default judgment, which grants them the power to garnish wages and freeze bank accounts without ever presenting a shred of evidence. The moment your general denial is filed, a default judgment becomes impossible. The collector must now proceed with active litigation. If you want to understand how this changes the broader landscape of your case, looking at the complete timeline of what happens when a collector sues you provides the full context.

2. It Shifts the Burden of Proof

A general denial essentially wipes the collector’s complaint clean and says, “Start over with evidence.” The collector can no longer rely on their own typed allegations. If they claim they bought the debt from a bank, they must now produce the bills of sale. If they claim you owe $4,500, they must now produce account statements proving that exact math.

3. It Preserves Your Right to Raise Defenses

Filing a general denial gets you in the door. It acts as a placeholder that keeps the case active while you figure out your next steps. Once it is filed, you maintain the right to raise specific affirmative defenses later, such as the statute of limitations or lack of standing, as you learn more about the collector’s actual evidence.

The Exact Language to Use in Your Answer

A general denial does not need to be a ten-page legal brief. In fact, adding unnecessary paragraphs, personal stories, or explanations of financial hardship to your Answer is usually a mistake. Keep the language tight, professional, and limited to the legal standard.

Here is the standard language commonly used to assert a general denial in jurisdictions that permit it:

Sample General Denial Statement:

“Defendant generally denies each and every allegation contained in the Plaintiff’s Complaint and demands strict proof thereof. Defendant reserves the right to assert additional affirmative defenses as information becomes available through the discovery process.”

The phrase “demands strict proof thereof” is the operative part of this statement. It is the legal equivalent of drawing a line in the sand. When you are determining exactly how to write and format your lawsuit Answer, ensuring this sentence is placed clearly below the case caption is your primary objective.

The State-Specific Exception: When You Need a Verified Denial

While a general denial is a powerful tool, it is not a universal shield for every possible argument. You must be aware of state-specific procedural rules regarding certain types of claims. This is where self-represented defendants sometimes stumble.

In certain jurisdictions, specific defenses cannot be covered by a simple general denial. They require a “verified denial.” A verified denial is a specific statement that must be signed under oath, often requiring a notary public’s stamp, affirming that a particular fact is false.

For example, if you intend to argue that you are the victim of identity theft, or that you are absolutely not the person who signed the original contract, a basic general denial may not be enough to preserve that specific argument in court. The court may require you to submit a verified denial explicitly stating, under oath, “I did not execute the contract attached to the plaintiff’s complaint.”

If your defense relies on mistaken identity, forgery, or arguing that a specific document is fraudulent, checking your local court’s self-help center for verified denial requirements ensures you do not inadvertently waive your strongest arguments.

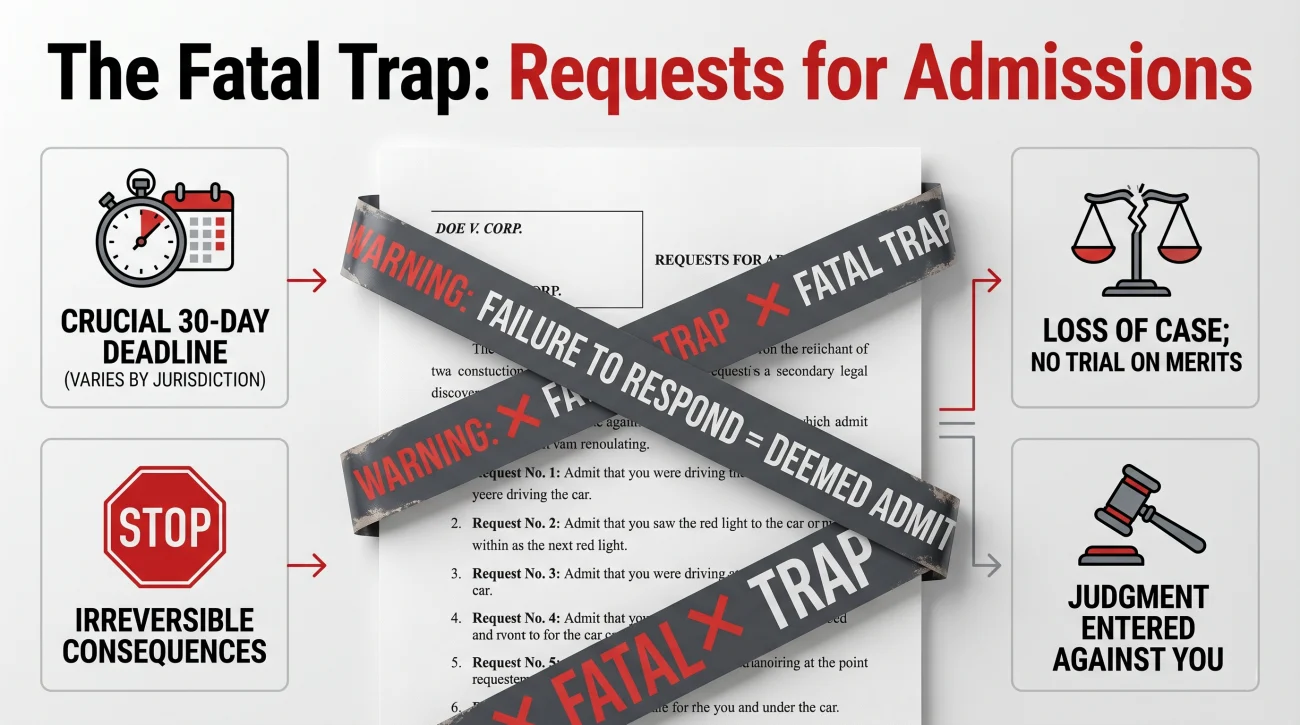

The Fatal Trap: Requests for Admissions

Collectors routinely win easy cases against consumers who file a perfect general denial by exploiting one specific procedural trap.

A general denial only responds to the lawsuit Complaint. It does not cover discovery documents. Often, a debt collector’s attorney will serve a secondary document alongside the complaint, or shortly after, called “Requests for Admissions.”

Requests for Admissions are a list of statements that you are required to either admit or deny individually. They usually look like this:

- Admit that you opened an account with Original Creditor.

- Admit that you made charges on the account.

- Admit that you owe Plaintiff $4,200.

📌 Note: If you file a general denial with the court, but you ignore the Requests for Admissions, the court rules dictate that your silence equals an admission. Every statement on that list will be automatically deemed “Admitted” as true.

Once those statements are automatically admitted, the collector will immediately file a motion to win the case, and they will succeed, because you technically admitted to owing the money by failing to respond to the specific discovery document. A general denial will not save you from ignored discovery requests. To protect yourself, you must understand how to handle debt collection discovery traps the moment those extra documents arrive in your mailbox.

Is Self-Representation Safe When Filing This?

Many consumers hesitate to file anything because they assume the court system requires a law degree to navigate. While complex litigation absolutely requires legal counsel, the initial filing of an Answer is primarily an administrative hurdle.

Filing a general denial is one of the most accessible steps for a self-represented defendant. You do not need to cite case law. You do not need to write a persuasive essay. You simply need to use the correct formatting, include your case number, state your denial, and file it before the deadline. For many people facing standard debt buyer lawsuits, deciding whether to respond without an attorney comes down to following the procedural steps carefully and ensuring a copy is mailed to the opposing counsel.

Combining the Denial with Affirmative Defenses

While a general denial acts as a blanket rejection of the plaintiff’s claims, it is highly recommended to pair it with specific “Affirmative Defenses.” An affirmative defense is a legal reason why you should win the case, even if some of what the plaintiff says is true.

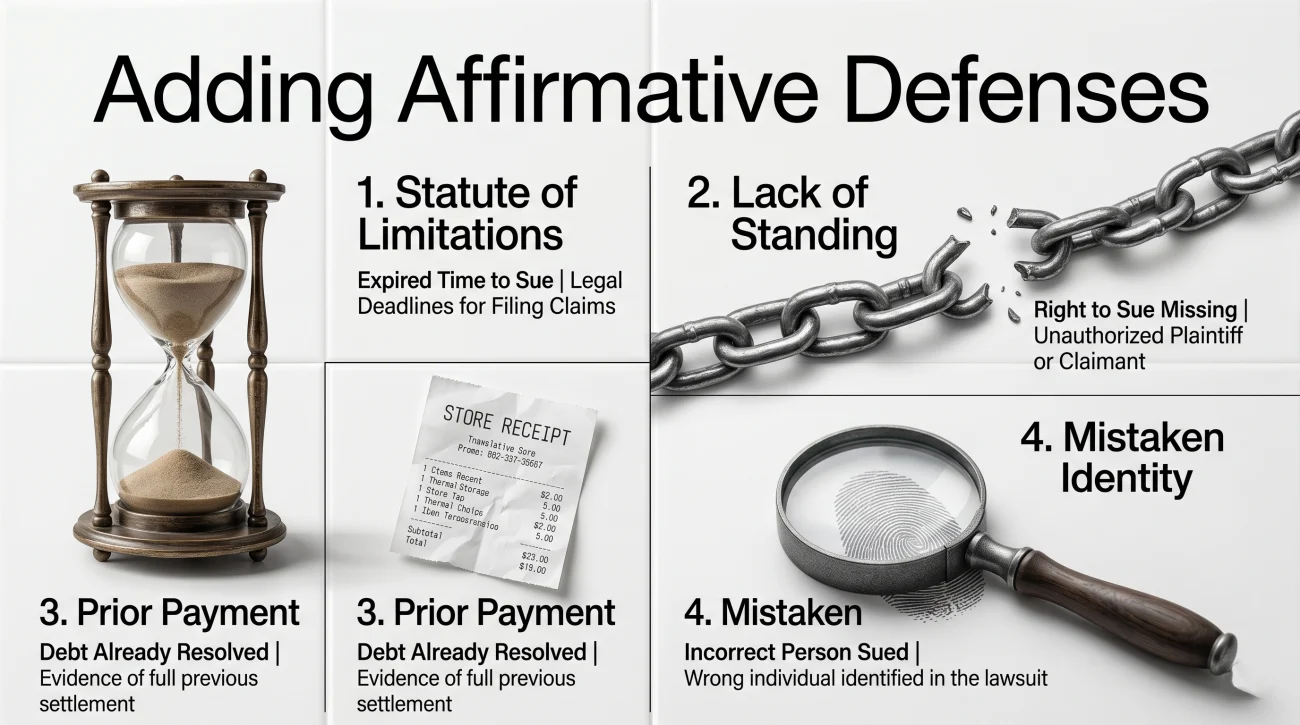

Here are four of the most common affirmative defenses you should evaluate adding beneath your general denial sentence:

- Statute of Limitations: If you know for a fact that the debt is past your state’s legal deadline for lawsuits, you must explicitly state that the time limit has expired.

- Lack of Standing (Chain of Title): You assert that the debt buyer cannot prove they legally acquired your specific account from the original creditor.

- Prior Payment or Settlement: If you already paid the debt, or if it was discharged in bankruptcy, you must state those facts clearly and attach proof if available.

- Mistaken Identity: You state that you did not open the account and the debt belongs to someone else with a similar name, or is the result of fraud.

Structure your document in two parts. First, write the general denial sentence. Below that, create a heading titled “Affirmative Defenses” and list your specific legal protections. By combining the two, you force the collector to prove their case while simultaneously presenting independent legal reasons why their case should be dismissed. Having a clear overview of how the entire response process fits together ensures you do not miss the opportunity to list these critical defenses.

What Happens Next After You File

Filing your general denial does not end the lawsuit, but it fundamentally shifts the collector’s options. Once the court accepts your Answer, you should anticipate one of three paths.

First, the collector may push for a settlement. This is an incredibly common reaction. Filing an Answer shows you are engaged in the legal process, which immediately increases their expected litigation costs. Many debt buyers will quickly shift toward settlement negotiations, often offering significantly lower percentages than they did before you filed.

Second, the litigation process may actively begin. The court might schedule a pretrial conference or a hearing, which you must attend. Alternatively, the collector’s attorney might mail you a packet of written discovery requests. If you receive these discovery documents, you must answer them before their specific deadlines. Finally, if the debt buyer reviews your general denial and realizes they truly cannot locate the original contract or chain of title documents, they may file a voluntary dismissal and walk away from the case entirely.

Signs a General Denial is Your Best Immediate Move

If you are staring at a stack of court papers and feeling paralyzed by the timeline, overthinking your defense strategy can cause you to miss your window entirely. You should stop researching and file your general denial immediately if any of the following apply to your situation:

- ⚠️ Your deadline is less than 5 days away. You do not have time to gather decades of bank statements. You need to stop the clock and prevent a default judgment today.

- ⚠️ The lawsuit is from a debt buyer you do not recognize. If the plaintiff is a company like Midland Funding, Portfolio Recovery, or LVNV Funding, their documentation is likely incomplete. A general denial forces them to produce the paper trail.

- ⚠️ The complaint has no attachments. If the collector sued you with a three-paragraph complaint and failed to attach an original credit agreement or a chain of title, a general denial exposes their lack of immediate evidence.

- ⚠️ You need time to consult a professional. Filing the denial protects your standing in the case while you evaluate your options or gather funds to hire representation.

If you are facing a rapidly approaching deadline, or if the collector’s paperwork appears suspiciously thin, securing your position in the court record is your highest priority. When the stakes are high or the debt amount is significant, bringing in professional legal representation after you have prevented a default is often the safest path forward.

Final Thoughts on Pushing Back

The debt collection litigation machine is designed to process silence. It functions efficiently only when consumers fail to push back. By filing a general denial, you throw a wrench into a system that expects you to surrender.

You are not acting unethically by requiring a plaintiff to present competent, admissible evidence of their claims. You are simply utilizing the exact rules of civil procedure that the debt buyers themselves use to their advantage every single day. A general denial shifts the spotlight off your past financial difficulties and shines it directly onto the collector’s current paperwork. In many cases, that paperwork simply cannot hold up to the scrutiny.

❓ FAQ

🛑 Can I use a general denial if I actually owe the money?

Yes. A general denial is a procedural requirement demanding the plaintiff prove their case. You are not committing perjury by requiring them to meet their legal burden of proof, even if you recognize the original account.

📝 Do I need a lawyer to file a general denial?

No. Many consumers file their own initial Answers using basic formatting. However, if the balance is large or the legal situation is complex, consulting an attorney is highly recommended to ensure you don’t miss strategic defenses.

🏛️ Does every state allow a general denial?

While widely accepted, some jurisdictions or specific types of courts require you to admit or deny each paragraph of the complaint individually. Always check your local court’s self-help guidelines before filing.

⏱️ How long does a general denial take to write?

The actual drafting of the statement takes only a few minutes. The most time-consuming part is ensuring the document contains the correct case caption, court name, and formatting required by your local clerk.

📄 Will a general denial work against the original creditor?

It will prevent a default judgment, but original creditors usually have an easier time proving their case than third-party debt buyers because they still possess the original signed contracts and complete account histories.

📮 Where do I send my general denial?

You must file the original document with the court clerk listed on your summons and mail a copy directly to the plaintiff’s attorney representing the debt collector.

🤷♂️ What happens if I just say “I don’t know” instead?

Stating that you “lack sufficient information to admit or deny” is a valid legal response to specific paragraphs in a complaint, and it generally has the same legal effect as a denial by forcing the plaintiff to prove the claim.

⚖️ Can I be sued for perjury if I file a general denial?

No. Holding a plaintiff to their burden of proof in a civil lawsuit is a standard legal right. Perjury involves swearing to a false statement of specific fact under oath, not filing a procedural denial of allegations.

🛡️ Does a general denial include my affirmative defenses?

No. A general denial rejects the plaintiff’s claims, but affirmative defenses (like the statute of limitations) are separate legal reasons you should win. You must list affirmative defenses separately within the same Answer document.

📞 Will the debt collector call me after I file this?

Once a lawsuit is active and you have filed an Answer, communication should generally occur through the attorneys and the court. Filing an Answer shows you are engaged in the legal process, which often shifts the collector toward settlement negotiations.

What each stage of litigation requires and where your leverage sits.

- What the lawsuit process looks like from summons to judgment

- What to file, when to file it, and what happens if you do not

- The legal arguments that can defeat a debt collection lawsuit

- What a default judgment allows collectors to do and how to fight one

- How to negotiate a resolution once litigation has started

Once judgment is entered, collectors gain tools they did not have before.

- The FDCPA violations collectors commonly commit during the collection process

- How to respond to a debt lawsuit and what defenses are available to you

- How a judgment becomes a garnishment order on your paycheck

- When a collector uses a judgment to freeze your bank account instead

- How to settle before the judgment turns into something harder to stop

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.