- The Fair Debt Collection Practices Act (FDCPA) is a federal law that dictates exactly what third-party debt collectors can and cannot do when trying to collect money from you.

- Collectors rely heavily on consumer confusion. Threats of arrest, public humiliation, and continuous harassment are completely illegal.

- You have the right to force a collector to prove you actually owe the debt (validation) and the right to demand they stop contacting you entirely.

- The FDCPA applies to third-party collection agencies and debt buyers, not to original creditors like your bank or hospital.

- Understanding the boundary between a collector’s legal limits and their high-pressure tactics is your strongest defense against harassment.

The Reality of Debt Collection Laws and Consumer Leverage

Most consumers think they know their rights when dealing with debt collectors. In my experience, most are wrong. During my twelve years working inside third-party collection agencies and a national debt buyer, I saw firsthand how the industry operates. The truth is that debt collection laws are highly specific, collectors know them far better than the general public does, and the gaps in your knowledge are exactly where the pressure gets applied.

When your phone starts ringing from an unknown number, or a demand letter arrives in the mail, the natural reaction is panic. But debt collection in the United States is not the Wild West. It is heavily regulated by the Fair Debt Collection Practices Act, commonly known as the FDCPA.

This federal law is the shield that protects you from abusive, deceptive, and unfair collection practices. However, a shield only works if you know how to hold it. Knowing what a debt collector can legally do gives you clarity. Knowing what they cannot do gives you the power to push back and regain control of the situation.

Who the FDCPA Actually Covers (And Who It Does Not)

The single most common mistake people make is assuming that the FDCPA applies to anyone asking them for money. It does not. The law is very specific about who is considered a debt collector, and understanding this distinction dictates how you should respond to a call.

The FDCPA strictly applies to third-party debt collectors. This includes collection agencies acting on behalf of someone else, and debt buyers who purchase delinquent accounts for pennies on the dollar. The moment your original creditor gives up and hands the account over to an outside agency, the federal law kicks in.

The Original Creditor Blind Spot

Here is the critical blind spot: the FDCPA generally does not cover original creditors. If the bank that issued your credit card, the hospital that treated you, or the dealership that financed your car is calling you directly, they are not bound by the FDCPA. They have their own internal policies, and they are regulated by other banking and consumer finance laws, but they do not have to adhere to the strict contact and validation rules of the FDCPA.

The in-house collections department of your credit card company calling you 45 days after a missed payment. They can generally be more persistent and have fewer federal restrictions on communication.

An agency named “Midwest Recovery” calling you six months later because the credit card company sold your account. They are strictly bound by every rule in the FDCPA.

State laws often add layers of protection. While the FDCPA is federal law, many states have enacted their own consumer protection statutes that mirror the FDCPA and, in some cases, extend those rules to cover original creditors. This means that depending on where you live, you may have state-level protections that restrict original creditors even when federal law leaves a gap.

The Four Types of Covered Debt

The law also cares about the nature of the debt itself. The FDCPA protects consumers dealing with personal, family, and household debts. This covers the vast majority of what everyday people struggle with. The four primary categories are:

- Credit card debt

- Medical bills

- Auto loans

- Student loans and mortgages

Business debt is explicitly excluded. If you took out a commercial loan to buy equipment for your LLC, or if you are a freelancer who incurred debt strictly to fund your business operations, the FDCPA does not protect you from the collectors pursuing that balance. Those accounts operate under completely different commercial collection rules.

The Boundaries: When and How They Can Actually Contact You

Debt collectors do not contact people randomly. Every channel they use, the timing of their calls, and the frequency of their outreach serve a specific psychological purpose. The law draws very clear lines around contact methods to prevent harassment.

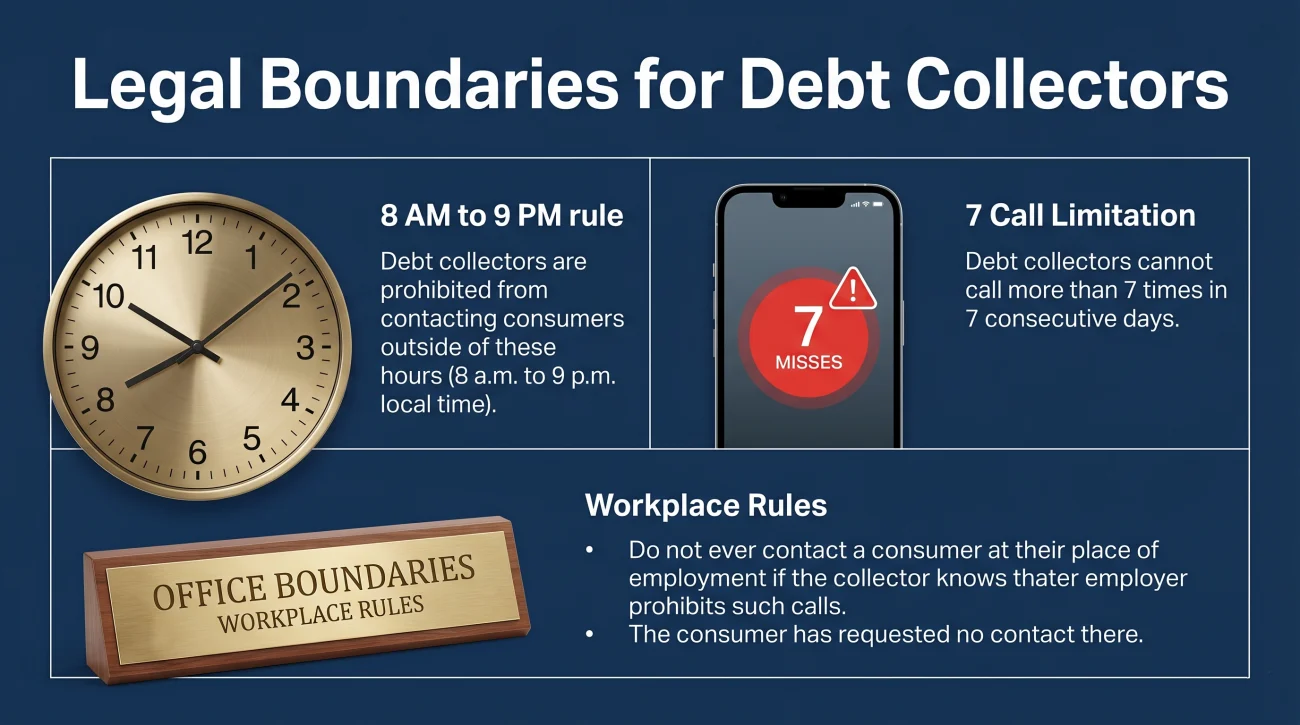

The 8 AM to 9 PM Rule

Under the FDCPA, a collector cannot call you before 8:00 AM or after 9:00 PM in your local time zone without your explicit consent. This applies seven days a week, including weekends and holidays.

“In the agencies I worked for, calling at 8:01 AM was a deliberate strategy. People are often stressed, rushing to get to work, or just waking up. A consumer who is caught off guard is much more likely to make a hasty promise to pay just to get off the phone.”

If a collector calls you at 7:45 AM or 9:15 PM, it is rarely an innocent mistake regarding time zones. It is a compliance failure, and it counts as an FDCPA violation.

The 7-Call Limitation

Recent federal rule changes put a specific number on phone harassment. A collector is presumed to be violating the law if they call you more than seven times in a seven-day period regarding the same debt. Furthermore, if you actually answer the phone and speak with them, they cannot call you again about that specific debt for another seven days.

However, this is where operational tactics come into play. The rule applies per debt, not per consumer. If a debt buyer owns three different medical bills of yours, they can legally call you 21 times a week. Many agencies also rotate caller ID numbers deliberately to increase the chances that you will pick up. To fully understand these boundaries and how to force the calls to stop, you must review the complete collector contact rules.

The Mandatory Disclosure Requirement

The mandatory disclosure, often called the Mini-Miranda, is your first filter. By law, a collector must tell you they are attempting to collect a debt and that any information obtained will be used for that purpose. If a caller is demanding money but actively avoids identifying themselves as a debt collector, you are likely dealing with a scam or a rogue agency violating federal law.

Workplace Calls and Social Pressure

Collectors are permitted to call you at work. However, the moment you tell them, “My employer does not allow me to receive personal calls,” they must legally stop contacting you at your job. They do not need this in writing; a verbal notice is enough.

Why do they call your job in the first place? It is not just to verify your employment. It is about social pressure. Knowing that your boss or coworkers might overhear a conversation about debt creates intense embarrassment, which collectors use as leverage to force a payment.

Crossing the Line: Harassment, Abuse, and Public Shame

There is a difference between a collector being annoying and a collector breaking the law. The FDCPA explicitly bans conduct that is designed to harass, oppress, or abuse any person in connection with the collection of a debt.

This includes:

- ⚠️ Using obscene or profane language.

- ⚠️ Threatening violence or physical harm to you, your property, or your reputation.

- ⚠️ Publishing your name on a “bad debt” list (except to credit reporting agencies).

- ⚠️ Calling repeatedly in rapid succession just to annoy you.

One of the most insidious forms of abuse is third-party disclosure. A collector is allowed to contact your family, neighbors, or employer exactly once, and solely for the purpose of obtaining your location information (your address, phone number, or where you work). They are absolutely forbidden from identifying themselves as debt collectors or mentioning that you owe a debt.

If a collector tells your sister, your boss, or your neighbor about your financial situation, they have committed a severe violation. The public shame associated with debt is a weapon, and federal law strips that weapon away from collection agencies.

Deceptive Tactics: The Lies Collectors Use to Create Panic

Collectors cannot lie to you. This sounds straightforward, but in practice, deception is one of the most common complaints filed by consumers. The law prohibits collectors from using any false, deceptive, or misleading representation.

Collectors use carefully crafted scripts designed to walk right up to the legal line. For example, instead of illegally threatening to garnish your wages without a judgment, an agent might say, “We are reviewing your file for voluntary or involuntary asset recovery.” It is specifically designed to make you panic about your paycheck without technically crossing the legal threshold for a false threat. When they do step over that line, it becomes actionable.

The Threat of Arrest

In the United States, you cannot be arrested or sent to jail for failing to pay a civil consumer debt like a credit card or a medical bill. Debtors’ prisons were abolished over a century ago.

Despite this, threats of law enforcement involvement remain common. A collector might say, “We are dispatching police to your home,” or “This is considered theft of services, and a warrant will be issued.” This is a calculated exploit. Most people do not understand that the civil court system and the criminal justice system are entirely separate. The fear of jail causes immediate panic, which leads to immediate payments. Any threat of arrest for a consumer debt is an automatic, severe FDCPA violation.

Misrepresenting the Amount Owed

Collectors are not allowed to inflate your balance or add unauthorized fees. If your original contract did not allow for specific “collection fees,” the debt buyer cannot suddenly tack on $500 in handling charges. Claiming you owe more than you legally do, even accidentally, can trigger legal liability for the agency. If you have experienced threats or deception, understanding exactly what constitutes actionable FDCPA violations is your first step toward fighting back.

Impersonating Attorneys or Government Officials

A collector cannot claim to be an attorney if they are not one, nor can they use letterhead that looks like it came from a courthouse or a government agency. While legitimate collection law firms do exist, a standard collection agency cannot imply that legal action has been taken simply to scare you.

Your Strongest Weapon: Forcing Them to Prove the Debt

This is arguably the most powerful tool the FDCPA gives you. You do not have to simply take a collector’s word that you owe them money. You have the right to force them to prove it.

Within five days of their first communication with you, a collector must send you a written “validation notice.” This notice must outline the amount of the debt, the name of the current creditor, and a statement explaining your right to dispute the debt.

Once you receive this notice, a 30-day window opens. If you send a written dispute or a request for validation within those 30 days, the collector must legally pause all collection activities. They cannot call you, they cannot write to you, and they cannot report the debt to the credit bureaus until they provide you with verifiable proof that the debt is yours and the amount is accurate.

Key Point: Nearly half of all complaints filed with the Consumer Financial Protection Bureau (CFPB) involve consumers stating they are being pursued for debt they do not owe. Validation is how you stop this.

From an operational standpoint, debt buyers hate validation letters. They buy debts for pennies on the dollar, often receiving nothing more than an Excel file with names and balances. They frequently lack the original signed contracts or itemized payment histories. If you demand a complete chain of title and they cannot produce it, they often abandon the account entirely. To use this tool effectively, you must understand the complete debt validation process.

“I am requesting validation of this debt. I dispute this debt in its entirety. Please provide the original signed agreement, a complete itemized billing history, and the complete chain of title showing your legal right to collect this specific account.”

The Time Dimension: Statute of Limitations

Most people focus entirely on what collectors can do today—how many times they can call or what they can say. But there is another layer that determines whether they have any legal power at all: time.

There is a separate legal framework that operates alongside the FDCPA, and confusing the two is a common consumer trap. This is the statute of limitations.

The statute of limitations is a state law that sets a hard deadline on how long a collector has to file a lawsuit against you to force payment. Depending on your state and the type of debt (credit card, medical, personal loan), this window is typically between three and ten years.

If a debt is past the statute of limitations, it is considered “time-barred.” A collector can still politely ask you to pay it, but they can no longer successfully sue you for it. Furthermore, under the FDCPA, a collector cannot threaten to sue you for a debt they know is time-barred. Doing so is illegal.

The Danger of the Partial Payment

⚠️ Warning: Making even a $10 “good faith” payment on an old debt can be disastrous.

In most states, making a partial payment, or even verbally acknowledging that the debt is yours, completely restarts the statute of limitations clock from day zero. Collectors handling older accounts are trained to push for tiny payments specifically to revive their ability to sue you. Before you agree to pay anything on an old account, you must evaluate the statute of limitations on debt to ensure you do not accidentally resurrect a dead liability.

The Discipline of Documentation

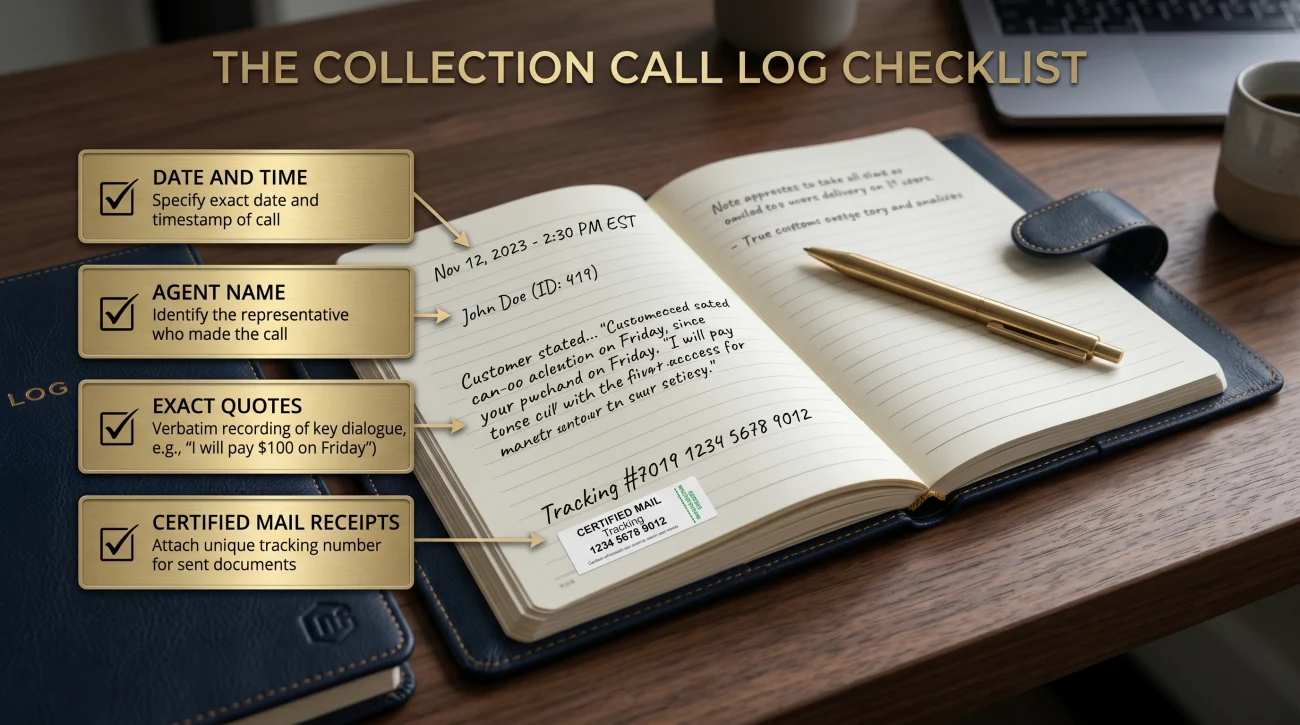

Understanding the law is useless if you cannot prove a collector violated it. In the collections industry, if it is not documented, it did not happen. You must treat every interaction with a debt collector as building a potential legal case.

Keep a physical log of every call. Do not rely on your phone’s recent calls list, as that data eventually overwrites. Request everything in writing, and keep every piece of mail they send you, including the envelopes with the postmarks.

The formula for protecting yourself is simple but requires discipline: for every call, write down the date, time, the agent’s name, and their exact quotes. Save all written notices, keep the envelopes they came in, and always send your own letters via Certified Mail.

This is exactly where consumers lose leverage. A collector threatens arrest on a Tuesday. By Friday, the consumer has forgotten the agent’s name and the exact time of the call. When it comes time to file a complaint or consult an attorney, a vague memory is not enough. A detailed logbook is undeniable proof.

Common Mistakes to Avoid

- Disputing over the phone: The FDCPA’s strongest protections only trigger when you submit disputes and requests in writing. Verbal disputes mean very little legally. In every agency I worked for, verbal disputes were almost universally ignored. The agent simply logs the call as “consumer refused to pay” rather than “consumer disputed.” If you do not put it in writing, from a compliance standpoint, it never happened.

- Arguing on the phone: You will never win a debate with a debt collector. Their goal is to keep you talking until you say something they can use. State your position briefly and hang up.

- Ignoring a court summons: Even if the debt is entirely fake, or past the statute of limitations, ignoring a formal lawsuit summons will result in a default judgment against you. This leads to frozen bank accounts and wage garnishment.

Signs You May Be Dealing With FDCPA Violations

If you are reading this, you are likely feeling overwhelmed by the sheer volume of contact or the aggressive tone of a collector. It is easy to feel powerless when someone is demanding money you may not have. But recognizing when a line has been crossed is how you regain control.

You need to assess whether the behavior you are experiencing has crossed from aggressive collection into illegal harassment. Look for these specific indicators:

- A collector called you before 8:00 AM or after 9:00 PM your time.

- They explicitly stated or implied that you could face criminal charges, jail time, or police action for not paying.

- They continued calling your cell phone after you sent a written cease and desist letter.

- They discussed your debt with a family member, a neighbor, or your boss.

- They called your workplace after you clearly told them personal calls were not permitted.

- They refused to provide written validation of the debt after their initial contact.

- They are trying to collect an amount that includes fees and interest you know were not in your original contract.

Evaluating Your Next Steps

Knowing that the FDCPA exists is only the first step. The real question is how you apply it to your specific situation. If a collector violates federal law, they can be held liable for potential statutory damages, plus your actual damages and attorney’s fees.

Because the law requires collectors to pay your legal fees if you win, many consumer protection attorneys take these cases on contingency, meaning you pay nothing out of pocket. If you recognize the warning signs above, you do not have to handle this alone. Understanding whether the contact you have been receiving crosses the line requires looking closely at your call logs and letters with professional guidance.

Final Thoughts: Controlling the Narrative

Debt collectors operate in a volume business. They push boundaries because, historically, the majority of consumers simply submit to the pressure out of fear or embarrassment. The FDCPA levels the playing field, but it requires you to actively enforce your rights.

Do not let a collector dictate the terms of your financial reality. Demand written proof. Keep meticulous records. Refuse to be intimidated by threats that have no legal backing. The moment you start citing your rights, requesting validation, and keeping logs, you transition from an easy target to a difficult account. In the collections industry, difficult accounts are the ones that get closed or returned.

Your Next Steps: The Four Core Areas of Debt Collection Defense

Understanding the broad rules of the FDCPA is only the foundation. As a former collector, I can tell you that reading the law is not enough: you need to know exactly how to deploy it against the specific tactics being used on you right now.

To help you navigate your exact phase of the collection process, I have broken down the legal framework into four primary defense areas. Depending on what you are experiencing today, select the guide below to see the insider mechanics of what the collector is doing and the precise steps you need to take to stop them.

| Core Defense Area | What You Will Learn Inside |

|---|---|

| Debt Collector Contact Rules | The comprehensive guide to when, where, and how collectors are allowed to call you, including the exact mechanics of how to shut down workplace calls, family contact, and phone harassment. |

| FDCPA Violations | How to recognize illegal tactics like arrest threats, third-party disclosure, or lying about the amount owed, and how to use those violations to create legal leverage. |

| Statute of Limitations on Debt | The master guide to time-barred debt, state lawsuit deadlines, and the dangerous partial payment traps collectors use to secretly restart your legal liability. |

| Debt Validation | The step-by-step process for forcing debt buyers to prove you actually owe the money, exposing their documentation gaps, and making unverified debts disappear. |

❓ FAQ

👔 Can a debt collector call my boss about my debt?

No. Under the FDCPA, a collector is never allowed to disclose to your employer that you owe a debt. They can call your workplace once to ask for your location information, but if you tell them personal calls are not allowed at work, they must stop calling entirely.

🚓 Can I go to jail for not paying a debt?

No. You cannot be arrested or jailed for failing to pay a civil consumer debt like a credit card, medical bill, or personal loan. If a collector threatens you with arrest or police action, they are committing a severe federal violation.

🙈 What happens if I just ignore debt collectors?

Ignoring them does not make the debt go away. It will likely damage your credit report for up to seven years. More importantly, if they file a lawsuit and you ignore the summons, the court will issue a default judgment against you, which allows them to garnish your wages or freeze your bank account.

🛑 How do I make the collection calls stop completely?

You can send a written “cease and desist” letter via certified mail. Once the collector receives it, they are legally required to stop contacting you, except to confirm they are stopping or to notify you of a specific legal action like a lawsuit.

📱 Can debt collectors text me or message my Facebook?

Yes, recent rules allow collectors to contact you via text message, email, or private social media direct messages. However, they must provide a clear way for you to opt out of those digital communications, and they cannot post publicly about your debt.

⏳ Do I still have to pay if the debt is seven years old?

It depends on the statute of limitations in your state, which dictates how long they have to sue you (often 3 to 6 years). Even if the debt is too old for a lawsuit (time-barred) and falls off your credit report after 7 years, you technically still owe it, and they can ask for it, but they cannot force payment through the courts.

📞 Why do they keep calling from different local numbers?

Collectors rotate phone numbers and use local area codes (spoofing) because people are more likely to answer local numbers than toll-free ones. While annoying, this tactic is generally legal as long as they truthfully identify themselves once you answer.

🗣️ What should I say when a collector calls me?

Say as little as possible. Do not admit the debt is yours, do not argue, and do not make a “good faith” payment, as that can restart the legal clock. Simply ask them to send you a written validation notice and then end the call.

💸 Can they garnish my wages without a warning?

No. A third-party debt collector cannot garnish your wages or touch your bank account without first suing you in court and winning a judgment. The exception is federal debt, like federal student loans or taxes, which have different rules.

🚩 Is it a scam if they refuse to send me anything in the mail?

It is a massive red flag. Legitimate debt collectors are required by federal law to send you a written validation notice within five days of first contacting you. If someone demands immediate payment over the phone and refuses to provide written documentation, it is highly likely a scam.

The full FDCPA framework and the four areas where it matters most.

- Your legal rights when collectors call, write, or threaten to sue

- When they can call, what they cannot say, and how to make it stop

- How to identify FDCPA violations and what you can do with them

- Why the age of a debt determines what a collector can legally do

- Your right to demand proof before paying or acknowledging anything

Harassment is one thing. Lawsuits, garnishments, and frozen accounts are another.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.