- Debt collector harassment is rarely random. It is a calculated stress test used when an account is stalled, designed to force a response before the agency spends money on legal action.

- Collectors use advanced skip tracing and data brokers to profile you before they dial. They often know exactly where you work and what leverage will apply the most pressure.

- Federal law restricts their tactics, explicitly forbidding calls before 8 a.m., repeated calls to your employer after being warned, and fake threats of arrest or immediate property seizure.

- Keeping a precise written log of the abuse is your strongest weapon. Your memory is not evidence, but a detailed log gives a professional exactly what they need to evaluate an FDCPA lawsuit against the collector.

The Reality of Escalating Collection Calls

I spent 12 years inside third-party collection agencies and a national debt buyer. I have sat on the collection floor and listened to exactly how these calls are made. I know what collectors are trained to say, where they push the boundaries, and what it actually means when a file goes from routine letters to aggressive, daily phone harassment. Understanding that internal shift is the key to protecting yourself.

The calls usually start before you have even had your morning coffee. You look at your phone and see a blocked number, or perhaps a local area code that you know is spoofed. When you do not answer, they call back two hours later. Then they call your office. Then comes the most terrifying tactic of all: a vague voicemail threatening that a “courier” has been dispatched to your property, or that “pending legal action” requires your immediate compliance.

You are not imagining the pressure, and you are not overreacting. If a debt collector is harassing you, they are doing it with a specific goal in mind. They want you scared, off-balance, and desperate enough to make a payment just to make the phone stop ringing. This level of aggressive contact leaves most people paralyzed. You know you owe a debt, so you assume you have to tolerate the abuse. You wonder if they can actually do the things they are threatening, like having you arrested or showing up at your front door.

What you are experiencing right now is a deliberate phase in the collection cycle. To stop it, you do not need to argue with the person on the other end of the line. You need to understand what the law allows, what the collector knows about you, and how to force the harassment to stop using the leverage you did not know you had.

What Collectors Know Before The Phone Rings

Many people assume that a debt collector calling their workplace or mentioning a family member is just a lucky guess. It is not. Before the predictive dialing software ever routes your file to a collector’s headset, the agency has likely run your profile through comprehensive skip tracing software and specialized data brokers.

These databases pull from public records, credit applications, utility bills, and even social media. A well-equipped agency often knows your current address, your last three employers, the names of your immediate relatives, and whether you recently applied for a new line of credit. They use this data to calculate your “propensity to pay.”

If you have a steady job, they know that calling your workplace will create maximum embarrassment and jeopardize your employment. If they see you recently moved, they might threaten to send someone to your new address. They map out your pressure points before they ever pick up the phone.

The Economics of the Call Floor

The Consumer Financial Protection Bureau (CFPB) reported over 109,000 debt collection complaints in 2023, with communication tactics and harassment remaining top issues. But inside the agency, this behavior is rarely viewed as harassment. It is viewed as “file pressure.”

Agencies run on volume, metrics, and strict file economics. When an account first lands on a collector’s desk, it has a specific expected value. A fresh charge-off might be worth aggressively pursuing, but as the account ages without a payment, it becomes a depreciating asset. At a certain point, the floor manager or the software identifies your file as stuck.

When a file is stuck, the agency has to make a choice. They can close the account and return it to the original creditor, they can prepare the file for a lawsuit, or they can turn up the pressure to see if you will break. Escalating the contact is the cheapest way to shake the tree.

“On the collection floor, we knew exactly which accounts were on the edge of being sent to the legal department. When a collector suddenly starts calling your family members or using highly aggressive language, it is rarely an accident. It is a stress test. They are trying to find out if embarrassment or fear will force you to open your wallet before the agency spends money drafting a lawsuit.”

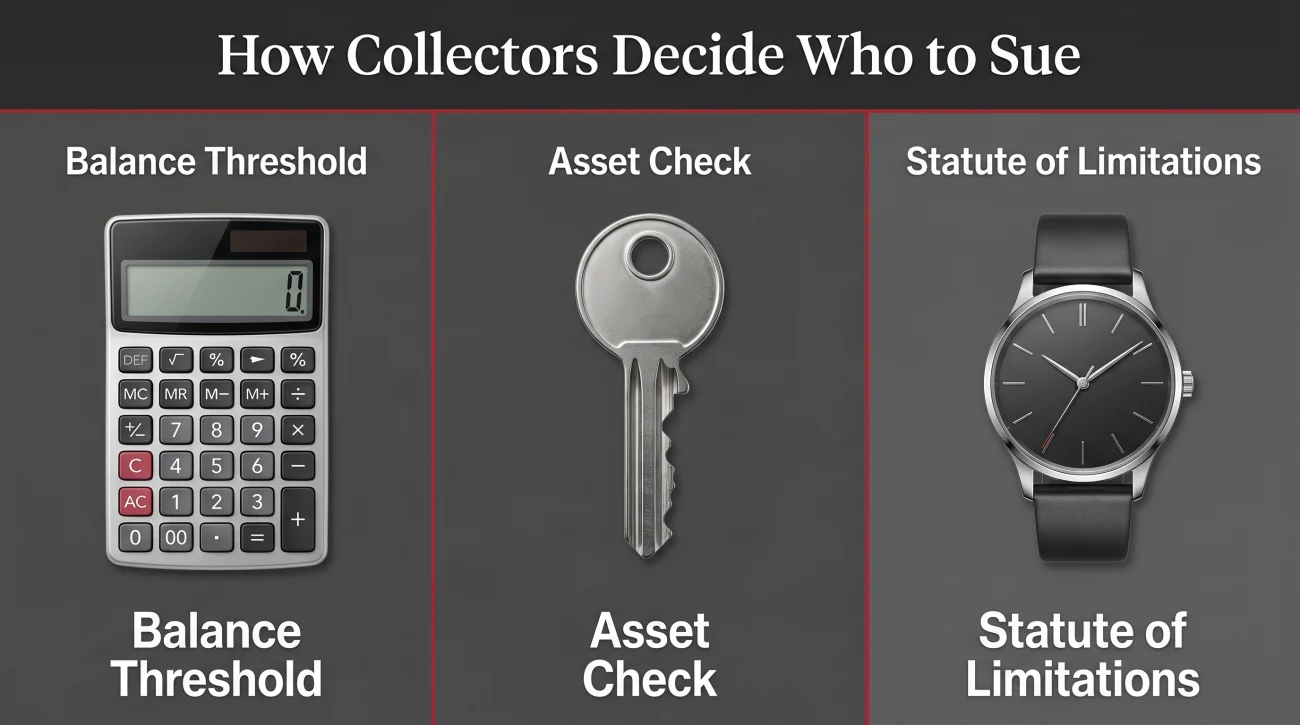

How Collectors Decide Who to Sue

Not every account subjected to phone pressure ends up in a courtroom. Litigation costs money. Before an agency pays a local attorney to draft a summons, they run a strict calculation to determine if you are a profitable target. They look at three specific factors:

- The balance threshold: Small accounts often stay in the call cycle or get bundled and sold to another debt buyer because they are not worth court fees. Large balances immediately trigger a legal review.

- A fresh asset check: If their skip tracing shows you have a steady W-2 income or own property, you are a high-value target. They know that if they win a default judgment, they can easily garnish your wages or levy your bank account.

- The statute of limitations: If the legal window to sue you is closing within a few months, the urgency spikes. A sudden, massive increase in phone harassment is often a desperate attempt to extract a payment before they are forced to file a lawsuit to beat the clock.

Where the FDCPA Draws the Line

The Fair Debt Collection Practices Act (FDCPA) is the federal law that dictates exactly what third-party debt collectors can and cannot do. Collectors are trained on exactly where these legal boundaries sit, and some are willing to step right over them if they think you will not document their behavior.

Timing and Frequency Violations

The law explicitly forbids collectors from contacting you at unusual times or places. This generally means they cannot call you before 8 a.m. or after 9 p.m. in your local time zone. Furthermore, using an auto-dialer to call you back-to-back or filling up your voicemail with the intent to annoy, abuse, or harass you is a clear violation.

Workplace Interference and Third Parties

Under federal law, a collector can call your workplace to try to reach you initially. However, if you tell them that your employer does not allow you to receive such calls while on the clock, they must stop immediately. They are also highly restricted when contacting your family members. They can generally only call a third party once to obtain your location information, and they cannot discuss your debt or reveal that they are a debt collector to anyone but you.

Deceptive Threats of Arrest or Violence

Debt is a civil matter. You cannot go to jail for an unpaid credit card or personal loan. Any debt collector threatening legal action involving the police, claiming there is a warrant for your arrest, or implying that they will seize your property today without a court judgment is using illegal deception.

Arguing with the collector on the phone, trying to convince them that you do not have the money, or begging them to stop calling your boss.

Ending the conversation quietly, documenting the exact time and nature of the threat, and using that documentation to seek professional intervention.

The Real Danger of Ignoring the Escalation

The most common mistake consumers make is assuming that if they just block the numbers and wait it out, the agency will eventually give up. What happens when the calls stop is often much worse than the harassment itself.

When an agency exhausts its phone tactics without getting a payment, the file does not just disappear. If the balance is large enough and they believe you have a job or a bank account, the file moves from the call floor to a collection attorney’s desk. This transition is silent. The harassing phone calls will abruptly stop, giving you a false sense of relief. A few weeks later, a process server shows up at your door with a lawsuit summons.

⚠️ Warning: Do not mistake silence for safety. From the collector’s perspective, the harassment was just the final warning shot before they decided to pursue a default judgment.

When the legal department takes over, the burden of proof shifts. Whether they file a lawsuit or you decide to hold the agency accountable for FDCPA violations, you need hard evidence. You must treat your situation like an active case file from this moment forward.

Documentation and The Critical Next Step

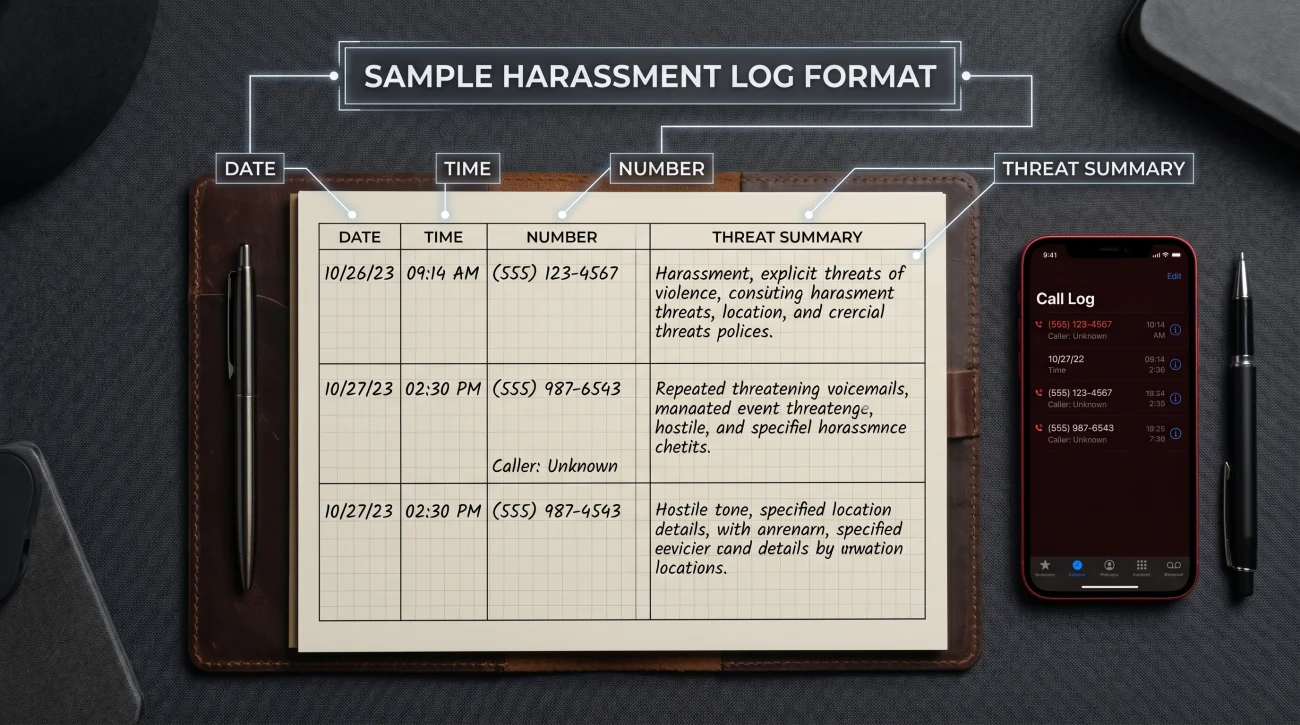

If you want to turn the tables on a rogue collection agency, you have to stop acting like a victim and start acting like a case manager. Collectors rely on the fact that you are too stressed to take notes. Your memory of feeling threatened is not evidence. A precise written log is.

Keep a manual log on paper or in your phone. Every time they call, write down the details immediately. Once you have three to five documented instances of abusive or borderline behavior, this log becomes your primary tool.

Sample Harassment Log Format:

Date: [Insert Date]

Time of Call: [Insert exact time, note if before 8am/after 9pm]

Phone Number Used: [Insert caller ID number]

Name of Agency/Collector: [If provided]

Summary of Threat: [e.g., “Claimed they were sending a process server today” or “Called my manager’s direct line after being told to stop”]

You do not mail this log to the collection agency. You hand this log to a professional. It gives a consumer protection attorney exactly what they need to evaluate the strength of your case and determine if the agency can be sued for statutory damages.

Diagnosing Your Situation

You know the harassment is happening, and you now know it might be illegal. The internet is full of templates for “cease and desist” letters, but sending one blindly without understanding your overall leverage can trigger the collector to immediately file a lawsuit since you have cut off all other forms of communication.

There are two distinct realities here, and identifying yours is critical.

In the first reality, the debt is valid, the balance is high, and you simply cannot afford to pay it. The harassment is a symptom of a larger financial crisis. Your goal here is to resolve the underlying debt before it turns into a garnished paycheck. You need a buffer between you and the collectors, someone who can step in, stop the bleeding, and negotiate the balance down through a formal debt relief program.

In the second reality, the collector has blatantly violated the FDCPA by threatening arrest or disclosing your debt to your employer. When this happens, the dynamic flips entirely. Debt collectors who commit FDCPA violations can be sued. The violation itself becomes massive leverage that a debt defense attorney can use to wipe out the debt and secure damages for you.

Making the wrong move, like admitting to the debt on a recorded line while trying to get them to stop calling, can destroy your leverage permanently. Before you make another move, you need to understand the timeline you are working against and let a professional evaluate your next step.

Final Thoughts: The Cost of Inaction

Debt collector harassment is designed to overwhelm your decision-making abilities. Doing nothing is the highest risk choice you can make, because the collector’s timeline moves forward whether you answer the phone or not.

Within 30 days of escalating harassment, the agency typically makes its internal legal determination on your file. Within 60 to 90 days, accounts selected for litigation are handed over to local attorneys to draft summonses. Every week that passes reduces your options to negotiate a favorable settlement or build a strong FDCPA counterclaim.

If the harassment is ongoing and you need a permanent solution to an overwhelming balance, exploring debt relief options puts a professional buffer between you and the agency. If you have been threatened, publicly embarrassed, or contacted at illegal hours, you need an immediate legal review of your call log.

Take your documentation, seek a professional case evaluation, and force the collection agency to answer for their tactics before the timeline runs out.

❓ FAQ

📱 Can a debt collector text me or message me on social media?

Yes, recent updates to federal rules allow debt collectors to send text messages and use social media to contact you. However, they must clearly identify themselves as debt collectors, and they are required to provide a simple, straightforward way for you to opt out of receiving electronic communications.

💵 Does paying a small amount stop the harassment?

Making a “good faith” partial payment is one of the most dangerous mistakes you can make. It rarely stops the calls permanently, and worse, it can reset the statute of limitations on the debt. This gives the collector a brand new window of several years to legally sue you for the remaining balance.

🔍 How do I know if the collection agency calling me is legitimate?

Scammers often use aggressive tactics that mimic bad debt collectors. A legitimate collector is legally required to send you a written “validation notice” within five days of their first contact. If they refuse to provide their physical address, their agency name, or written proof of the debt, you should not engage with them.

🏦 Can a collector garnish my wages without warning me first?

No. A third-party debt collector cannot garnish your wages or freeze your bank account simply because you ignored their calls. They must first file a lawsuit against you, serve you with court papers, and win a judgment in a court of law before they have the power to touch your paycheck.

📅 How long does a collection agency have to sue me?

This depends on your state’s statute of limitations for debt, which typically ranges from three to ten years. Once this legal window expires, the debt becomes “time-barred.” A collector can still ask you to pay a time-barred debt, but they cannot legally sue you or threaten to sue you for it.

Four areas of the collection process. Start wherever your situation applies.

Some situations have deadlines attached. These pages are written for those situations.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.