- Being sued for a debt does not mean the collector has proven their case. Debt buyers rely on a 70 to 90 percent default rate, expecting you to ignore the paperwork so they can win automatically.

- Filing a formal Answer with the court completely changes the collector’s financial calculation. It forces them to produce original documentation and an unbroken chain of title, which many debt buyers simply do not have.

- Your response deadline is rigid and absolute. Depending on your state and the court, you typically have 14 to 30 days from the date you were served. Finding this exact date on your summons is your immediate priority.

- Once a default judgment is entered, collectors gain the legal authority to garnish your wages, freeze your bank accounts, and place liens on your property. Responding is the only way to block this automatic escalation.

Court Papers on the Counter: Understanding What Just Happened

A stack of legal documents just landed on your kitchen counter. Maybe they arrived via certified mail, or perhaps a process server handed them to you directly at your front door. Your name is clearly printed as the defendant in a civil lawsuit. If your heart rate spiked and panic set in, know that your reaction is entirely normal. You want to know what this means, how serious it really is, and exactly what you are supposed to do next.

Here is the reality of the situation. Roughly one in four Americans with debt in collections will eventually face this exact scenario. And unfortunately, the vast majority of them will do exactly the wrong thing next, simply because they do not understand how the debt collection legal machine actually operates behind closed doors.

During my 12 years working inside third-party collection agencies and one of the nation’s largest debt buyers, I sat in the rooms where these litigation decisions were made. I trained the collectors who made the calls, and I reviewed the accounts that were ultimately forwarded to law firms for suit. I am not an attorney, and this is not legal advice for your specific state. But I can tell you exactly how this process works from the inside. I know why these lawsuits are filed, how the business model depends on your confusion, and what actually makes a debt collector back down.

To understand why collectors are often vulnerable to pushback, you have to understand how they get your account. The entity suing you is almost certainly a third-party debt buyer, not your original bank. These companies purchase defaulted accounts in massive portfolios for pennies on the dollar. Because accounts are resold multiple times in bulk, the specific, individualized paperwork like your signed contract is rarely transferred seamlessly. The documents you received consist of two main parts. The summons is the court’s official procedural notice, telling you where the case was filed and how many days you have to respond. The complaint is the collector’s statement of what they claim you owe. While the paperwork looks intimidating and final, it is actually just the opening move in a process that is highly vulnerable to scrutiny.

The 70 Percent Default Reality: A Business Model, Not a Legal Outcome

There is a fundamental truth about debt collection litigation that changes how you should view the paperwork you just received. When a debt buyer files a lawsuit against you, they are not doing so because they have spent hours building an airtight, undeniable legal case supported by pristine original documents. They are filing the lawsuit because they expect you to do nothing.

Between 70 and 90 percent of all debt collection lawsuits end in a default judgment. This happens simply because the person being sued never files a response with the court. In the collections industry, a default judgment is not viewed as a hard-fought legal victory. It is the core business model. Debt buyer law firms file lawsuits in massive volumes, fully aware that most people will be too scared, too confused, or too overwhelmed to participate. The court filing fee is minimal, and the expected payout from a default judgment makes the math highly profitable.

“During my time at a national debt buyer, the ‘case files’ we sent over to our litigation attorneys were often nothing more than a single line on an Excel spreadsheet. There was no original signed contract attached, no detailed account history, and no proof of purchase. Just a name, an address, and a balance. We forwarded hundreds of these accounts for suit every week, banking entirely on the fact that 80 percent of the defendants would default and the judge would never ask us to produce the actual evidence.”

This is the insight that shifts the power back to you. The collector is counting on your silence. The moment you break that silence and force them to prove their claims, their entire business calculus is disrupted.

What a Default Judgment Actually Gives Them

Before a lawsuit is filed, a debt collector has very little actual power over you. They can call your phone, send letters to your home, and place negative marks on your credit report. These tactics are stressful and annoying, but they cannot reach into your wallet and take your money without your consent.

A lawsuit is the mechanism they use to upgrade their power. If you ignore the summons and the court awards them a default judgment, the debt transforms from a simple contract dispute into a binding court order. This is a critical escalation. With a default judgment in hand, the collector suddenly possesses all the enforcement tools they previously lacked.

Depending on your state laws, a default judgment authorizes the collector to move directly to wage garnishment, which forces your employer to withhold a percentage of your paycheck and send it directly to the debt buyer. It allows them to issue a bank account levy, freezing your funds and seizing your balances. It also permits them to place a property lien on your real estate, ensuring they get paid if you ever sell or refinance your home.

The transition from receiving annoying phone calls to having your wages seized happens entirely through the default judgment process. Preventing that judgment from being entered is the single most important action you can take right now.

Why Filing an Answer Changes Everything

The way you stop a default judgment is by filing a document called an Answer. An Answer is your formal, written response to the lawsuit, filed directly with the court and served to the collector’s attorney. Filing this document does not require you to be a legal expert, but its impact on the collector’s strategy is massive.

When you file an Answer, you are putting the court and the collector on notice that you are actively participating in the case. You are formally disputing the claims and shifting the burden of proof back where it belongs: on the plaintiff. Many people assume they cannot file an Answer if they actually owe the money. This is a misunderstanding of how civil litigation works. You are not required to do the collector’s job for them.

Calling the debt collector’s law firm right after receiving the summons to argue about the balance or explain your financial hardship, while never filing any paperwork with the court. The court does not know about your phone call, and your deadline to respond continues to tick down toward a default.

Drafting a formal, written Answer that generally denies the claims and demands proof, filing it with the court clerk, and mailing a stamped copy to the plaintiff’s attorney before the deadline expires.

In practice, the moment your Answer is processed, the case becomes real litigation. The debt buyer’s law firm now has to evaluate the cost of taking the case to trial against the likelihood that they can actually produce the required documentation. For a complete guide on how to prepare and submit this critical document, read our step-by-step breakdown on how to respond to a debt collection lawsuit.

This sounds straightforward, but in practice, it forces the debt buyer to transition from an automated filing system into actual legal work. If they only have a spreadsheet row and cannot produce your original credit agreement or a clear chain of assignment, your filed Answer exposes that weakness immediately.

The Deadline Reality: Finding Your Exact Window

Your response deadline is the most critical piece of information in the entire process. If you miss it by a single day, the court can enter a default judgment against you, regardless of how strong your defenses might be.

This timeline is strictly governed by state law and the specific type of court where the case was filed. In most jurisdictions, the deadline ranges from 14 to 30 days. However, the most common mistake consumers make is guessing when the clock started. The countdown does not begin on the date printed at the top of the complaint, nor does it begin on the day you finally open the envelope.

The clock starts on the exact day you were legally served with the papers. To find your specific deadline, you must look directly at the summons document. It will usually state something like, “You must file a written response within 20 days after this summons is served on you.” If the instructions are vague, or if you are unsure what day you were officially considered served, your safest move is to call the clerk of the court listed on the summons. Give them your case number and ask them to confirm your response date.

💡 Pro Tip: Always calculate your deadline conservatively. If you believe you have 20 days, aim to have your Answer filed and stamped by day 15. Do not leave your financial future up to mail delays or courthouse closures.

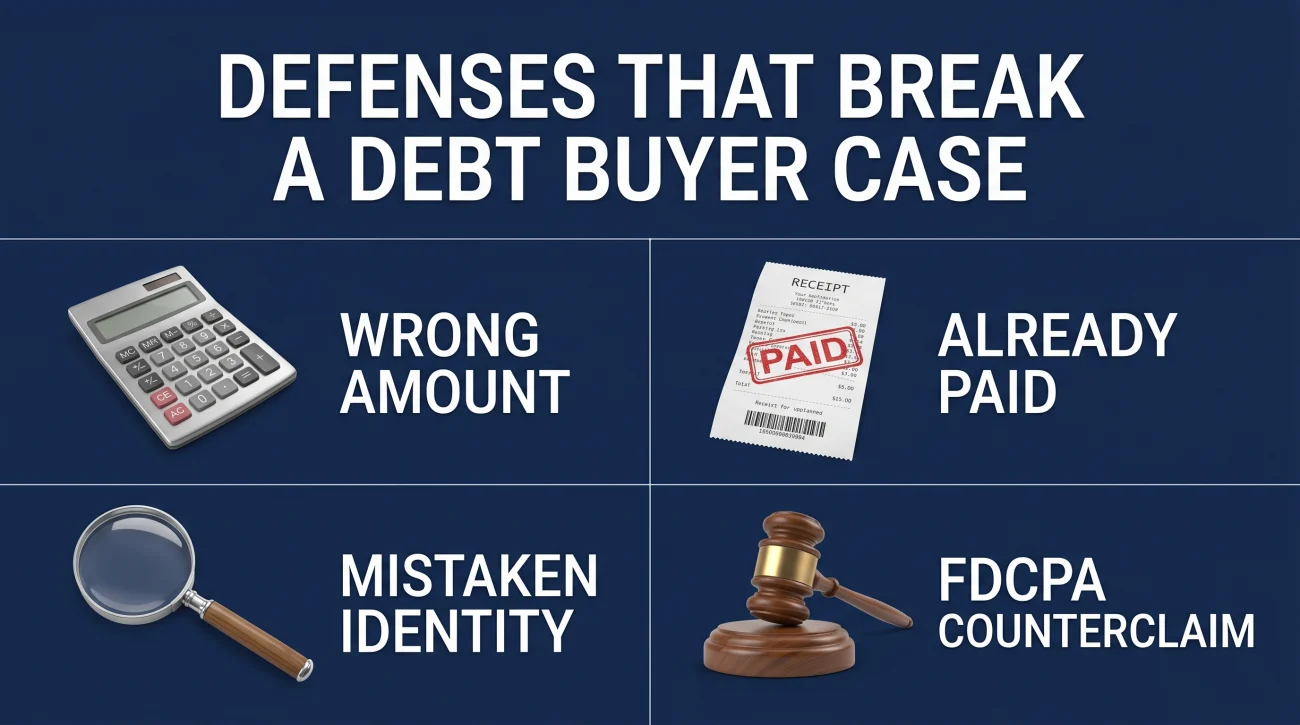

Defenses That Break a Debt Buyer’s Case

If you choose to fight the lawsuit, you will need to list your legal reasons in your Answer. These are called affirmative defenses. Because of the way the debt buying industry operates, there are specific defenses that frequently destroy their ability to win in court.

The most common and powerful defense against a third-party debt buyer is challenging their chain of title, which lawyers refer to as “lack of standing.” When an original creditor like a major bank sells a portfolio of defaulted accounts, the portfolio is often resold multiple times to different buyers over several years. To legally sue you, the current plaintiff must prove they own your specific account. They must show an unbroken chain of assignment from the original creditor through every single buyer, ending with them. Furthermore, they must produce documentation that your specific name and account number were included in each of those bulk sales.

Because these portfolios are sold as massive data files, the specific, individualized paperwork is rarely transferred seamlessly. When you force a debt buyer to prove their chain of title, they often cannot do it.

The second major defense is the statute of limitations. Every state has a legal time limit on how long a collector has to sue you for a debt, typically ranging from three to six years for credit card accounts. This clock usually starts on the date of your last payment. If a collector sues you after this window has closed, the debt is time-barred. However, the court will not automatically check this for you. You must proactively raise the statute of limitations as a defense in your Answer.

These are not the only tools available. Depending on your situation, you may have other strong grounds to challenge their claims:

- Wrong Amount: The balance is inflated with unauthorized fees not permitted by the original contract.

- Already Paid: You previously settled or paid this account in full to a prior collector.

- Mistaken Identity: You are an authorized user, or the account simply does not belong to you.

- FDCPA Counterclaim: The collector broke federal rules (like threatening arrest) during the collection process, giving you leverage to sue them back.

To understand the full range of arguments available to you, review our comprehensive guide on debt collection lawsuit defenses.

What Happens If You Already Missed the Deadline?

Many people reading this are in a state of panic because they know they have already missed their response window, or they have just discovered that a default judgment was entered against them months ago. If you are in this position, you need to know that the situation is bad, but it is not necessarily permanent.

If you missed the deadline but a judgment has not yet been officially entered by the judge, you should still attempt to file your Answer immediately. Many courts will accept a late filing if the plaintiff has not yet finalized the default process.

If the judgment is already finalized and your wages are being garnished, you may still have options. Courts have procedures to vacate, or undo, a default judgment if you can prove you had a legally valid reason for not responding. One path is proving “excusable neglect,” meaning you had a legitimate emergency, such as a sudden hospitalization, a natural disaster, or the court papers were mailed to a previous address where you no longer live.

Another common and successful ground for vacating a judgment is improper service, commonly known in the industry as “sewer service.” This occurs when the process server lies on their affidavit and claims they delivered the papers to you when they actually left them at an old address or simply threw them away.

If you can prove to the court that you were never properly served, the court lacked the jurisdiction to enter the judgment in the first place. Vacating the judgment stops the garnishments and resets the case back to the beginning, allowing you to file your Answer. For the specific steps on how this mechanism works, consult our guide on understanding and fighting a debt collection default judgment.

Settlement Before Court: The Power of Filing First

Whether you are fighting a newly filed lawsuit or trying to resolve one after successfully vacating a judgment, you might wonder if going to trial is your only option. It is a common misconception that formally contesting the case locks you into a courtroom battle. In reality, filing your Answer is often the best way to secure a highly favorable settlement.

By filing an Answer, you introduce real litigation costs into their equation. The attorney handling your case now has to manually request documents, prepare for discovery, and block out time for court appearances. Taking a case to trial requires substantial attorney hours, which is rarely justified for a small debt balance.

Because of this, the period immediately after you file your Answer is usually when you have the maximum leverage to negotiate. Collectors who were previously demanding 100 percent of the balance will often become remarkably flexible, sometimes accepting 40 to 60 percent of the claimed amount just to close the file and avoid the trial costs.

Whenever you enter settlement discussions after a lawsuit is filed, everything must be in writing. If you reach a verbal agreement on the phone to settle the debt for a lump sum, do not send a dime until the plaintiff’s attorney sends you a written agreement stating that your payment will result in the lawsuit being “dismissed with prejudice.” Without that exact phrasing in writing, they can take your money and still proceed with the lawsuit.

Keep in mind that settling a debt for less than you owe can have surprise tax consequences. The IRS often considers forgiven debt as taxable income, triggering a 1099-C form, though insolvency exemptions exist. If you are considering this route, it is vital to understand the exact sequencing and the required written protections outlined in our strategy for how to settle a debt collection lawsuit.

Warning Signs That Require Immediate Action

In the debt collection legal system, time is your most valuable asset, and it disappears quickly. If you are dealing with any of the following scenarios, the standard advice may not be enough, and attempting to navigate the procedural hurdles alone could result in permanent financial damage. These are the signs that you need to elevate your response.

- ⚠️ Your response deadline is within 10 days. Drafting and properly serving an Answer takes time. If the clock is running out, you need immediate intervention to prevent an automatic default.

- ⚠️ You have already been hit with a default judgment. If you just discovered a frozen bank account or an impending wage garnishment, the window to file a motion to vacate is narrow and procedurally strict.

- ⚠️ The collector committed severe FDCPA violations. If they threatened arrest, contacted your employer illegally, or sued on a known time-barred debt, you may have grounds for a counterclaim that shifts liability to them.

- ⚠️ The debt is not yours or the balance is heavily inflated. Whether dealing with identity theft or thousands in unauthorized fees, the required legal arguments become significantly more complex to navigate alone.

If any of these warning signs apply to your situation, you are facing a scenario where professional legal strategy is heavily advised. Do not risk a default judgment when a qualified professional can help you navigate the courts. Take the time to consider understanding your options when a collector files suit so you can protect your assets effectively.

Final Thoughts: Reclaiming Your Leverage

Being served with a debt collection lawsuit is an incredibly stressful experience, designed intentionally to make you feel powerless. But the system only works flawlessly for the debt buyer when you choose not to participate. By understanding that their business model relies on your silence, you can see the lawsuit for what it really is: a demand for proof that they often cannot provide.

Your immediate task is clear. Find the deadline on your summons. Draft your Answer. File it with the court and serve it to the plaintiff’s attorney. Do not let them win by default. By stepping into the process, you strip away their biggest advantage and force them to prove their claims. Whether you ultimately use that position to force a dismissal through lack of documentation, or use it to negotiate a highly favorable settlement, taking action is the only way to protect your financial future.

Your Next Steps: The Core Defense Guides

Navigating a debt collection lawsuit is not a single event; it is a sequence of strategic decisions. During my years inside the collection industry, I watched countless consumers lose simply because they didn’t know how to handle the specific phase of the lawsuit they were trapped in. To give you the exact tools you need to fight back, I have broken down the entire legal defense process into four comprehensive core guides. Find the one that matches your current situation and use it to build your strategy:

- 📌 Phase 1: The Immediate Reaction. If the clock is ticking and you need to file your response, start with our step-by-step breakdown on how to respond to a debt collection lawsuit. It covers exactly how to draft your Answer to prevent a default.

- 📌 Phase 2: Building Your Shield. If you are preparing your Answer or heading into the discovery phase, you need to know which legal arguments actually break a debt buyer’s case. Review the specific arguments in our guide to debt collection lawsuit defenses, focusing heavily on chain of title and the statute of limitations.

- 📌 Phase 3: The Worst-Case Scenario. If you missed the deadline, or if you just discovered your wages are being garnished from a case you never knew about, the fight might not be over. Learn the exact requirements for vacating the ruling in our guide to navigating a debt collection default judgment.

- 📌 Phase 4: The Exit Strategy. If you have filed your Answer and want to use your newly gained leverage to resolve the case without a trial, you need to understand the negotiation timeline. Our framework on how to settle a debt collection lawsuit explains when to make your offer and what must be in the written agreement before you pay a dime.

❓ FAQ

📋 What should I do when I am sued by a debt collector?

The very first thing you must do is locate the response deadline printed on the summons. You must then draft and file a formal written Answer with the court before that deadline expires, and mail a copy to the plaintiff’s attorney. Doing this prevents a default judgment.

⏰ How long do I have to answer a debt collection lawsuit?

In most states and courts, you have between 14 and 30 days from the exact date you were legally served with the papers. Do not guess this date; check your summons or call the court clerk immediately to confirm your exact deadline.

⚖️ What if I cannot afford to hire an attorney?

You do not have to have a lawyer to defend yourself. Many consumers successfully file their own Answer (acting “pro se”), particularly in small claims court or for straightforward debt buyer cases. For more complex situations involving FDCPA violations, consumer attorneys often work on contingency, meaning they only get paid if they win your case.

🚫 Can I ignore a debt collection lawsuit if the debt isn’t mine?

No. If you ignore the lawsuit, the court will assume the collector’s claims are entirely true and issue a default judgment against you. You must file an Answer denying the claims and raising the defense of mistaken identity to force them to drop the case.

🛑 What happens if I ignore court papers from a debt collector?

If you ignore the papers, the debt collector will request a default judgment from the judge. Once granted, this judgment gives them the legal authority to garnish your wages, freeze your bank accounts, and place a lien on your real estate.

📝 How do I answer a debt collection summons without a lawyer?

You can draft an Answer that includes a general denial of their claims and lists any affirmative defenses you have (like statute of limitations or lack of standing). You must file the original with the court clerk, pay any required filing fee, and mail a stamped copy to the collector’s attorney.

📅 Can a debt collector sue me after 7 years?

It depends on your state’s statute of limitations, which is usually between 3 and 6 years for credit card debt. If they sue you after this period, the debt is “time-barred.” However, the case won’t be thrown out automatically; you must raise the statute of limitations as a defense in your Answer.

🤝 Can you settle a debt after being served with papers?

Yes, most lawsuits actually end in a settlement. The best strategy is to file your Answer with the court first so you are protected from a default judgment, and then contact the plaintiff’s attorney to negotiate a settlement based on your financial hardship or documentation gaps.

💸 Will I go to jail if I lose a debt collection lawsuit?

No. You cannot go to jail simply for failing to pay a civil consumer debt. Debtors’ prisons are illegal in the United States. However, if you ignore a direct court order later in the process (like a summons for a debtor’s examination), you can be held in contempt of court.

📄 What proof does a debt collector need to win in court?

They must prove that they legally own your specific account (an unbroken chain of title), that the balance is completely accurate and authorized by the original agreement, and that they filed the suit within the statute of limitations. Debt buyers frequently fail to produce this documentation when challenged.

What each stage of litigation requires and where your leverage sits.

- What the lawsuit process looks like from summons to judgment

- What to file, when to file it, and what happens if you do not

- The legal arguments that can defeat a debt collection lawsuit

- What a default judgment allows collectors to do and how to fight one

- How to negotiate a resolution once litigation has started

Once judgment is entered, collectors gain tools they did not have before.

- The FDCPA violations collectors commonly commit during the collection process

- How to respond to a debt lawsuit and what defenses are available to you

- How a judgment becomes a garnishment order on your paycheck

- When a collector uses a judgment to freeze your bank account instead

- How to settle before the judgment turns into something harder to stop

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.