- Wage garnishment rules depend entirely on who you owe. Private creditors must sue you and win a court judgment first. Government agencies (IRS, Department of Education, child support) can garnish your paycheck administratively without a court order.

- For consumer debt like credit cards or medical bills, federal law caps garnishment at a standard percentage of your disposable earnings. However, child support can take a significantly higher portion, and the IRS has no standard percentage cap at all.

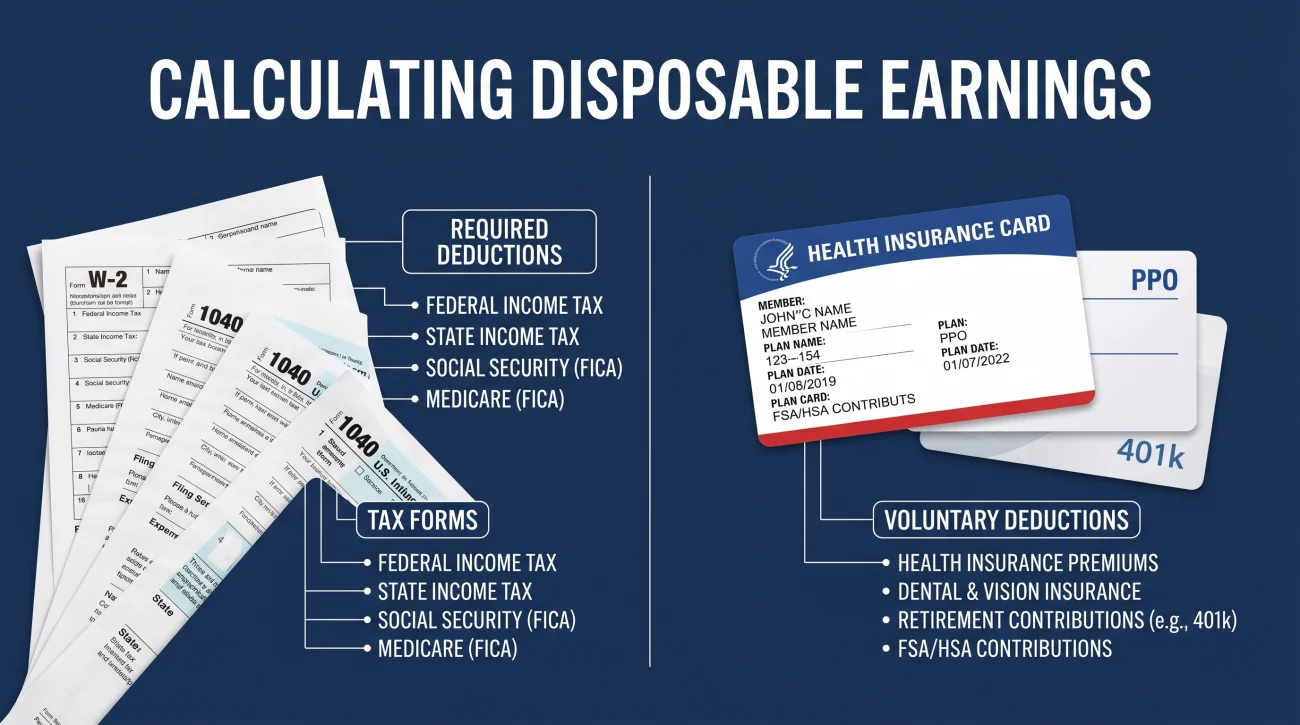

- When calculating what can be taken, voluntary deductions like health insurance and 401k contributions do not protect your income. Only legally required taxes reduce your “disposable earnings” in the eyes of the law.

- Four states completely prohibit wage garnishment for consumer debt (Texas, Pennsylvania, North Carolina, and South Carolina), but even there, residents are not immune to federal student loan or IRS levies.

- Your employer cannot legally fire you for having your wages garnished for a single debt. If you receive a second garnishment for a separate debt, that federal protection disappears.

The Reality of Losing Your Paycheck Before You Even See It

During my 12 years working inside third-party collection agencies, I reviewed thousands of accounts where wage garnishment was the final devastating blow to a consumer’s paycheck. I know exactly what the consumer is facing because I was the one initiating those orders. Wage garnishment is the most powerful debt collection tool available. It bypasses your bank account, bypasses your budget, and takes the money directly from your payroll department before the check is even cut.

If you have just learned that your wages are going to be garnished, or if you are already seeing the deductions on your pay stub, you are likely feeling a mix of panic and frustration. Most people assume the worst. They think the collector is going to take their entire paycheck, leaving them unable to pay rent or feed their family.

The truth is highly specific. The rules governing wage garnishment are completely different depending on who is garnishing you and why. Understanding which type of garnishment you are facing changes every option you have available. A credit card judgment has limits. A child support order has priority. An IRS tax levy plays by its own set of rules.

I am not an attorney, and nothing in this guide is legal advice. What I am giving you is the operational reality. I am going to walk you through how the garnishment system actually functions, how the math is calculated by your employer, and the legitimate, practical steps you can take to stop or reduce the financial bleeding.

The Court Order Divide: Who Can Take Your Money

The single most important distinction in wage garnishment is whether the creditor needs a court order to touch your paycheck. This is a concept most general legal articles gloss over, but it is the first thing we looked at on the agency floor. This distinction dictates how much warning you get and what legal levers you can pull to stop the process.

Private Creditors Require a Lawsuit

Private creditors include credit card companies, medical providers, personal loan lenders, and third-party debt buyers. If you owe a private entity, they cannot simply call your employer and demand part of your check. The law strictly forbids this.

Before a private creditor can garnish a single dime, they must file a lawsuit against you in a civil court, serve you with a summons, and win a judgment. Only after a judge signs off on a default judgment or a trial verdict can the creditor request a writ of garnishment to send to your employer. This means if you are facing a consumer debt garnishment, you had a legal window to fight the debt in court before the garnishment began.

“In collections, we knew that 90 percent of consumers would simply ignore the lawsuit summons. By not responding, they handed us a default judgment. Once we had that judgment, getting the wage garnishment order was just a matter of filing the right administrative paperwork with the court clerk.”

Government Agencies Do Not Need a Court Order

If you owe the government, or if you owe court-ordered support, the rules change entirely. Government agencies have statutory authority to issue an administrative wage garnishment directly to your employer. They do not need to sue you. They do not need a trial. They simply send official notice and begin the process.

This category includes the Internal Revenue Service (IRS) for unpaid taxes, the Department of Education for defaulted federal student loans, and state enforcement agencies for unpaid child support or alimony. Because no court judgment is required for the garnishment step itself, many consumers are caught completely off guard when the HR department notifies them of the deduction.

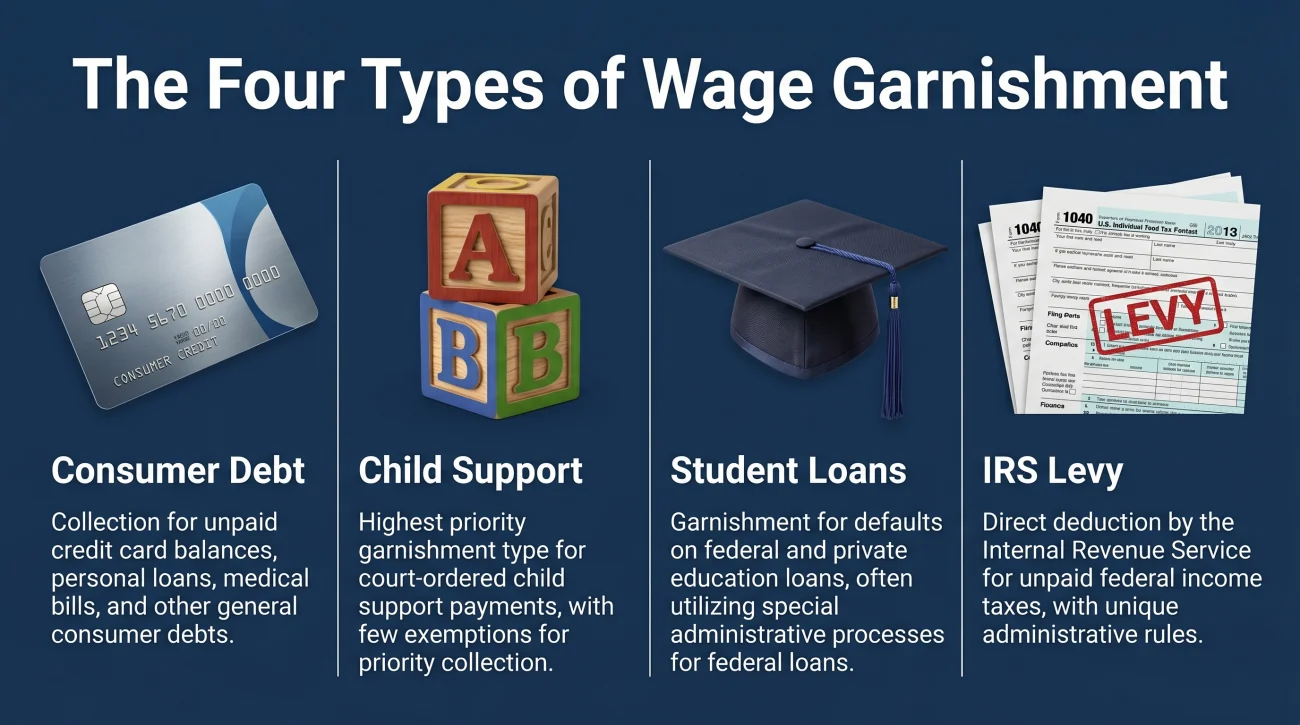

The Four Types of Wage Garnishment

Because the rules vary so wildly, you must first identify exactly which type of debt is driving the order. We categorize these into four distinct types, each carrying its own limits, employer requirements, and stopping mechanisms.

Type 1: Consumer Debt (The Standard Cap)

This is the most common type of garnishment I dealt with in the agency. It covers unpaid credit cards, broken apartment leases, defaulted auto loans, and medical debt. As mentioned, it requires a civil court judgment.

Under federal law, a private creditor is severely limited in what they can take. They are generally capped at a standard fraction of your disposable earnings. Federal law also sets a floor to protect the lowest earners – if your weekly disposable income falls below a certain threshold tied to the minimum wage, a private creditor cannot take anything. Because consumer debt requires a court judgment, it is often the easiest type of garnishment to challenge. If you were never properly notified of the lawsuit, you might be able to have the judgment vacated, which stops the garnishment dead in its tracks.

Type 2: Child Support and Alimony (The Priority Order)

Child support and spousal support operate on an entirely different level of severity. Under federal law, virtually all new child support orders automatically include an Income Withholding Order. There is no separate lawsuit required to start the paycheck deductions.

The limits here are massive. Federal guidelines allow a significant portion of your disposable earnings to be garnished depending on whether you are currently supporting a second family (spouse or child not covered by the order). If you are significantly behind in arrears, they can tack on an additional penalty, bringing the total to the highest tier the law allows.

Furthermore, child support takes absolute priority over consumer debt. If a credit card company is currently garnishing you, and a child support order hits your employer’s desk, the credit card company gets pushed to the side until the child support is satisfied.

Type 3: Federal Student Loans (The Administrative Cap)

If you default on federal student loans, the Department of Education or its contracted guaranty agency can issue an Administrative Wage Garnishment. As an administrative action, this bypasses the courts.

The federal cap for student loan garnishment is set at a lower percentage than standard consumer debt. You will receive an advance notice, which is your crucial window to act – usually by setting up a rehabilitation agreement or an income-driven repayment plan to stop the order before your employer ever sees it.

Type 4: The IRS Tax Levy (No Percentage Cap)

When you owe back taxes, the IRS uses a process called a wage levy. Like student loans, this bypasses the court system. Unlike every other type of garnishment, the IRS is not bound by a standard percentage cap.

Instead of taking a set portion, the IRS uses a fixed exempt-amount table provided by the government. This table dictates exactly how much money you are allowed to keep based on your standard deduction and dependents. Every single dollar you earn above that specific threshold goes to the IRS. For high earners or single individuals with no dependents, an IRS levy can effectively wipe out a massive majority of a paycheck. The IRS will send a final notice giving you a brief window to request a hearing and pause the action.

How the Math Actually Works: Understanding Disposable Earnings

When consumers try to calculate the garnishment in their heads, they almost always do it wrong. They look at their final take-home pay, divide it by a standard fraction, and assume that is the maximum the collector can take. This misunderstanding leads to massive shock when the first garnished paycheck arrives.

Garnishment is calculated based on “disposable earnings.” The legal definition of disposable earnings is your gross pay minus legally required deductions. That is it. If the law does not mandate the deduction, it does not protect your income from the collector.

Required Deductions vs. Voluntary Deductions

Legally required deductions include federal income tax, state and local taxes, the employee share of Social Security and Medicare taxes, and mandatory state retirement systems. These come out first.

Voluntary deductions do not reduce your disposable earnings. This is where people get hurt. Voluntary deductions include health insurance premiums, 401k contributions, union dues, life insurance, and charitable giving. Even though you never see this money in your bank account, the federal government considers it available for garnishment.

The Disposable Earnings Calculation Scenario

Let us say you earn $1,000 a week in gross pay.

– Mandatory taxes (Federal, State, FICA): $200

– Health Insurance Premium: $150

– 401k Contribution: $50

Your actual take-home pay is $600.

However, the collector does not care about the health insurance or the 401k. For garnishment purposes, your “disposable earnings” are $800 ($1,000 gross minus $200 mandatory taxes).

A standard consumer debt order might take $200 (a quarter of that $800).

Your actual take-home check is now just $400 ($600 normal take-home minus $200 garnishment). That is a devastating blow.

Key Point: Your employer’s payroll software is programmed to follow the strict legal definition. You cannot call HR and ask them to use your final net pay for the calculation. They are legally bound to include your voluntary health and retirement deductions in the garnishable pool.

The Minimum Wage Floor

For consumer debt, federal law provides a floor to ensure very low-income earners retain enough to survive. If your weekly disposable earnings fall below a specific baseline tied to the federal minimum wage, a private creditor cannot garnish anything at all. Once your earnings cross that safety threshold, a sliding scale applies until you hit the standard maximum.

State Protections That Override Federal Law

Federal rules set the floor for consumer protection, but states are allowed to pass stricter laws. If your state offers more protection than the federal government, your employer must apply the state rule. They must use whichever calculation leaves more money in your pocket.

The Four Prohibition States

There are four states that completely prohibit wage garnishment for standard consumer debt like credit cards and medical bills. If you live and work in these states, a debt buyer cannot touch your paycheck for a civil judgment.

- 📌 Texas: Consumer debt garnishment is banned by the state constitution.

- 📌 Pennsylvania: Prohibits consumer debt garnishment, though allows it for back rent and student loans.

- 📌 North Carolina: Complete ban on private consumer debt garnishment.

- 📌 South Carolina: Complete ban on private consumer debt garnishment.

However, there is a massive caveat here. This protection only applies to consumer debt. The IRS, the Department of Education, and child support enforcement can still garnish wages in all four of these states. Federal supremacy overrides state protections.

The Out-of-State Employer Loophole

There is an operational reality that many state residents do not know about until it hits them. If you live in a protective state, but work for a national corporation headquartered elsewhere, a creditor might sue your employer in that foreign state. Creditors sometimes exploit this jurisdictional loophole to enforce garnishment orders despite where you physically live. If you receive an order under these circumstances, you must have a local attorney review it immediately to see if it can be blocked.

States with Stricter Limits

Many states do not ban garnishment entirely but offer better math than the federal maximum rule. For example, some states cap the deduction at a much lower percentage of your gross wages, or they use a higher minimum-wage multiplier to protect more of your income. Other states offer powerful exemptions for anyone qualifying as a “Head of Household,” protecting their income specifically to support dependents.

If you want to know exactly how your state compares, you need to check your state’s specific Department of Labor guidelines. Do not let an out-of-state collection agency apply the federal maximum if your local state law provides a stronger shield.

The Employer’s Position: Bystanders to the Legal Process

One of the most common reactions I heard from consumers was anger at their employer. “Why did my HR department agree to this?” You need to understand that your employer is a legal bystander. They have absolutely no choice.

When a writ of garnishment arrives at payroll, it is a court order. The employer cannot evaluate whether the debt is valid. They cannot listen to your explanation that the credit card belonged to your ex-spouse. If they refuse to process the garnishment, the creditor can hold the employer legally and financially liable for the full amount of your debt. They will comply immediately.

Can You Be Fired for a Garnishment?

Federal law provides a very specific shield here. An employer cannot fire you, demote you, or take disciplinary action against you because your wages are being garnished for any one debt.

Notice the exact phrasing: one debt. It does not matter if the creditor sends ten different levy attempts over two years for that single credit card judgment; your job is safe. However, the moment your employer receives a garnishment order for a second, separate debt (for example, a medical bill judgment arriving six months after a child support order), the federal protection vanishes. In most states, an employer can legally terminate an employee who has multiple garnishments from separate debts due to the administrative burden it places on payroll.

⚠️ Warning: If you are juggling multiple delinquent accounts, keeping them out of the garnishment phase is critical to protecting your employment status.

Signs You Must Take Action Immediately

If you are reading this, you are likely feeling cornered. Garnishment removes your agency. It takes your money before you can pay your mortgage, buy groceries, or keep the lights on. The system is designed to create immense pressure to force a resolution.

However, the system also has strict procedural rules. If you are experiencing any of the following scenarios, you have active leverage and need to evaluate your legal options immediately before the next payroll cycle hits:

- You support dependents but have not filed a head of household exemption claim with the court.

- Your employer calculated the deduction based on your post-tax take-home pay, failing to subtract voluntary deductions correctly, resulting in an abnormally high hit.

- You received an IRS or Student Loan notice of intent to levy, and you are still within the response window to request a hearing or set up a payment plan.

- You live in Texas, Pennsylvania, South Carolina, or North Carolina, and a consumer debt collector is illegally attempting to attach your wages.

- You were never served with lawsuit paperwork, and the first time you heard about the debt was when HR handed you a garnishment notice.

If any of these apply to you, you cannot wait. You need to transition from panic to procedure.

💡 Pro Tip: If your situation involves an underlying lawsuit that you were never properly notified about, you need to look into exploring options to challenge the underlying lawsuit. Vacating a default judgment stops the garnishment.

What You Can Actually Do to Stop or Reduce Garnishment

You have a limited window to act from the time you receive notice. Doing nothing guarantees maximum paycheck loss. Here are the practical steps for fighting back.

1. File a Claim of Exemption

This is your first line of defense against consumer debt. Every state has a process for claiming exemptions, but it is never automatic. You must affirmatively file paperwork with the court that issued the order.

Common exemptions include the Head of Household status (proving you provide more than half the support for a dependent) or demonstrating extreme financial hardship. If taking the standard amount of your check means you will be evicted or cannot buy food, many judges have the discretion to lower the deduction significantly, or stop it entirely.

- Identify the specific court that issued the order.

- File the proper Exemption Form within your state’s tight deadline.

- Attend the hearing to prove your hardship.

Keep in mind that filing the exemption form does not stop the deductions immediately. Your employer will continue to withhold money until the judge issues a new order telling them to stop.

2. Negotiate a Voluntary Payment Plan

From the collection agency side, I can tell you that administering a wage garnishment is tedious. It requires tracking payments, communicating with employers, and dealing with payroll delays. If a consumer contacted us offering a voluntary payment plan that bypassed the employer, we were often willing to listen, especially if they could offer a lump sum settlement.

If you owe $5,000 and the garnishment is pulling $100 a week, you might contact the creditor’s attorney and offer to settle the entire debt for $3,000 cash today, provided they immediately release the writ of garnishment. If you do not have a lump sum, offering a direct monthly ACH withdrawal that is slightly less than the garnishment amount might get them to drop the employer order.

“Collectors want guaranteed money. A garnishment is guaranteed, but it is slow. If you can offer a faster, cleaner path to payment, you have leverage to negotiate the release of the wage order.”

3. Challenge the Underlying Judgment

If the garnishment is for a consumer debt, it is built on a foundation of a civil judgment. If that foundation is cracked, the whole house falls down. The most common crack is improper service of process. If the process server lied and said they handed you the summons, but you lived in a different state at the time, the court lacked jurisdiction. Filing a Motion to Vacate the Default Judgment forces the creditor back to square one. If the judge grants the motion, the garnishment is killed immediately because the legal basis for it no longer exists.

If you suspect the garnishment calculation is legally wrong or the judgment is flawed, you should consider having an experienced professional review the garnishment order for errors to protect your income.

4. The Nuclear Option: Bankruptcy

If you are drowning in multiple debts and facing garnishments from several creditors, bankruptcy is the definitive stop switch. When you file a Chapter 7 or Chapter 13 bankruptcy petition, the federal court immediately issues an “Automatic Stay.”

This is not a suggestion; it is a federal injunction. The moment your case is filed and a docket number is generated, almost all collection activity must cease instantly. Your attorney will send the case number directly to your HR department, and the payroll deductions for consumer debt will stop before the next check. However, remember the golden rule of exceptions: bankruptcy does not stop child support garnishment. While it temporarily pauses IRS levies, tax debts generally survive the bankruptcy process and will still need to be paid in full.

Taking any of these steps requires moving quickly before the next payroll cycle locks in. Once you know your options, the final step is execution.

Final Thoughts: Move Fast and Document Everything

Wage garnishment relies on your paralysis. The system is built on the assumption that you will simply accept the deduction because fighting it feels too complex and overwhelming. Do not fall into that trap.

Start by identifying exactly who is garnishing you. Calculate your own disposable earnings to ensure HR did not include your health insurance in the garnishable pool. If you qualify for a state exemption, get the form from the county clerk and file it within the response window. If you are facing government administrative garnishment, use the advance notice period to set up a repayment plan before the order reaches your boss. You have options, but they all carry strict expiration dates.

Your Next Steps: The Specific Garnishment Playbooks

General knowledge only gets you so far. When your paycheck is actively under threat, you need the exact procedural steps for your specific situation. Whether you are dealing with an aggressive child support order, an unyielding IRS levy, or a credit card judgment that slipped under the radar, the rules of engagement change entirely. I have mapped out the precise mechanics, legal limits, and counter-strategies for every major garnishment scenario below. Find your specific situation and get the exact playbook you need to protect your income.

| Wage Garnishment Topic | What You Will Learn |

|---|---|

| How Wage Garnishment Works | The exact step-by-step mechanical process from the court judgment to your HR department’s payroll deduction. |

| Types of Wage Garnishment | The critical divide between court-ordered consumer debt and administrative government levies. |

| How Much Wages Can Be Garnished? | Deep dive into the standard calculations, the minimum wage floor, and disposable earnings facts. |

| States That Prohibit Wage Garnishment | How TX, PA, NC, and SC protect paychecks, and the out-of-state employer loophole that bypasses it. |

| Wage Garnishment Limits by State | A conceptual look at how states like FL, MA, and IL offer stronger protections than federal law. |

| Child Support Wage Garnishment | Why income withholding orders are automatic and how they can legally take the largest cut of your pay. |

| Federal Student Loan Garnishment | How the Department of Education uses the administrative rule and the crucial action window to stop it. |

| IRS Wage Levy | Why the IRS ignores percentage caps entirely and uses a government table to take almost everything. |

| Can Employer Fire For Wage Garnishment? | Understanding the federal one-debt rule and when your job is genuinely at risk. |

| Multiple Wage Garnishments | Priority rules: what happens when child support and a credit card judgment hit your employer at the same time. |

| Head of Household Exemption | How family breadwinners can protect 100% of their wages, and the hidden waiver trap. |

| How to Claim a Garnishment Exemption | The required procedural steps, forms, and deadlines to stop deductions due to financial hardship. |

| Social Security Wage Garnishment | Protecting benefits at the source versus the bank level, and the automatic lookback rule. |

| Received a Wage Garnishment Notice | Your immediate action plan when the letter arrives from HR or the court. |

| Bankruptcy to Stop Wage Garnishment | How the automatic stay halts payroll deductions instantly upon filing, and what debts survive. |

❓ FAQ

💸 How much of my paycheck can a debt collector take?

For consumer debt like credit cards or medical bills, federal law caps the deduction at a specific fraction of your disposable earnings. However, if the debt is for child support, the law allows them to take a significantly larger portion of your pay.

🏥 Do health insurance premiums protect my wages from garnishment?

No. Health insurance, 401k contributions, and union dues are considered voluntary deductions. They do not reduce your “disposable earnings” calculation, meaning collectors can legally base their cut on money you never actually bring home.

⚖️ Can someone garnish my wages without taking me to court first?

A private creditor (like a credit card company) cannot. They must sue you and win a judgment first. However, government agencies like the IRS or the Department of Education can issue administrative garnishments without ever filing a lawsuit.

🚫 How do I stop a wage garnishment immediately?

The fastest ways to stop it are filing a Claim of Exemption with the court (if you qualify as head of household or face extreme hardship), negotiating a lump sum settlement directly with the creditor, or filing for bankruptcy to trigger the automatic stay.

👔 Can my job fire me if they receive a garnishment order?

Under federal law, your employer cannot fire or demote you for a single debt garnishment. However, if they receive a second garnishment order for a completely separate debt, that federal protection ends, and termination becomes legally possible.

🎓 How much can they take for defaulted student loans?

Administrative Wage Garnishment for federal student loans is capped at a lower rate than standard consumer debt. The government is required to send you an advance notice before deductions begin, giving you a brief window to enter a rehabilitation or repayment plan to stop it.

🏦 What happens if I live in Texas where garnishment is illegal?

Texas prohibits wage garnishment for consumer debt, but not for child support, IRS taxes, or federal student loans. Additionally, if you work for an out-of-state corporation, creditors sometimes exploit a loophole to enforce foreign judgments against your employer’s headquarters.

👨👩👧 Does having kids lower my garnishment amount?

It can, depending on your state. Some states offer a complete exemption if you provide more than half the financial support for a dependent. In other states, you can file a financial hardship exemption showing that the garnishment prevents you from feeding your children.

⏱️ How long does a wage garnishment last?

A garnishment remains active until the entire debt, including accumulated interest and court fees, is paid in full. It does not expire on a set timeline unless you actively challenge it, settle it, or file for bankruptcy.

📬 Will my employer tell me before the garnishment starts?

Your employer is legally required to notify you, but they must also begin withholding money immediately upon receiving the court order. In many cases, the notice from HR arrives at the exact same time as your first reduced paycheck.

How garnishment works and the options available to fight it.

- How courts allow collectors to reach your paycheck and your bank

- States That Don't Allow Wage Garnishment for Consumer Debt

- Can Your Employer Fire You for Wage Garnishment? The One-Debt Rule

- Received a Wage Garnishment Notice: What It Means and What You Must Do Before the Window Closes

- Child Support Wage Garnishment: Why the Rules Are Different - and What You Can Actually Do

Garnishment is a symptom. These cover the options that address what caused it.

- The collector behavior that typically comes before the garnishment order

- How the lawsuit you may have missed is what created the garnishment

- How wage garnishment works and the options available to stop or limit it

- When a collector goes after your bank account instead of your wages

- How settling the underlying debt stops the garnishment permanently

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.