- The court papers you received are actually two separate documents stapled together: the Summons and the Complaint.

- The Summons is the court’s procedural notice. It dictates the exact deadline you have to respond. You must look here to find out how much time you have.

- The Complaint is the collector’s list of allegations. In cases involving third-party debt buyers, this document is often deliberately vague because they lack the original contract documentation.

- Ignoring the papers or refusing to accept them from a process server will not protect you; it only results in an automatic loss.

- You must verify the documents are legitimate by calling the court clerk, then file a written response before the clock runs out.

Decoding the Stack of Papers on Your Counter

If you are reading this, there is a strong chance a thick stack of legal papers just landed on your kitchen counter. Maybe a process server knocked on your door and handed them to you directly. Maybe they arrived via certified mail, or perhaps you found them taped to your front door. Your name is printed at the top, a dollar amount is listed, and panic is likely the dominant emotion you are feeling right now.

I know exactly what those packets look like, and I know exactly how they are designed to make you feel. During my 12 years working inside third-party collection agencies and for a national debt buyer, I saw thousands of these legal packets generated, printed, and sent out for service. We banked heavily on the fact that the average consumer would take one look at the dense legal jargon, feel entirely overwhelmed, and simply put the papers in a drawer hoping the problem would go away.

When people ask me what a debt collection summons is, they usually hold up the entire thick packet. But the first step to regaining control of your situation is understanding that you are not holding just one document. You are holding two completely different documents with two completely different purposes: the Summons and the Complaint.

Confusing the purpose of these two documents is the primary reason people miss their deadlines and lose their cases automatically. Let’s break down exactly what you are holding, what each page requires of you, and why the vagueness of the claims against you is actually a massive signal about the weakness of the collector’s case.

The Summons: Your Procedural Clock

The cover page (or the first couple of pages) of the packet is the Summons. It is crucial to understand that the Summons is not a letter from the debt collector. It is an official procedural notice from the court system itself. The Summons exists to formally notify you that a civil lawsuit has been filed against you and to establish the legal rules of engagement.

The Summons has one job that matters more than anything else: it tells you exactly how long you have to respond to the lawsuit.

When consumers panic, they tend to flip right past the Summons and go straight to the pages that list the dollar amount they supposedly owe. They read the allegations, get angry, feel scared, and completely miss the procedural instructions printed on the very first page. You must look at the Summons first, because it contains the timeline that dictates everything else you do.

“When I was reviewing default judgments at the debt buyer, I routinely saw cases where the consumer actually had a valid, winnable defense. But they lost simply because they read the Complaint, got mad, and spent three weeks trying to call the original creditor to argue, instead of looking at the Summons to see their 14-day court deadline.”

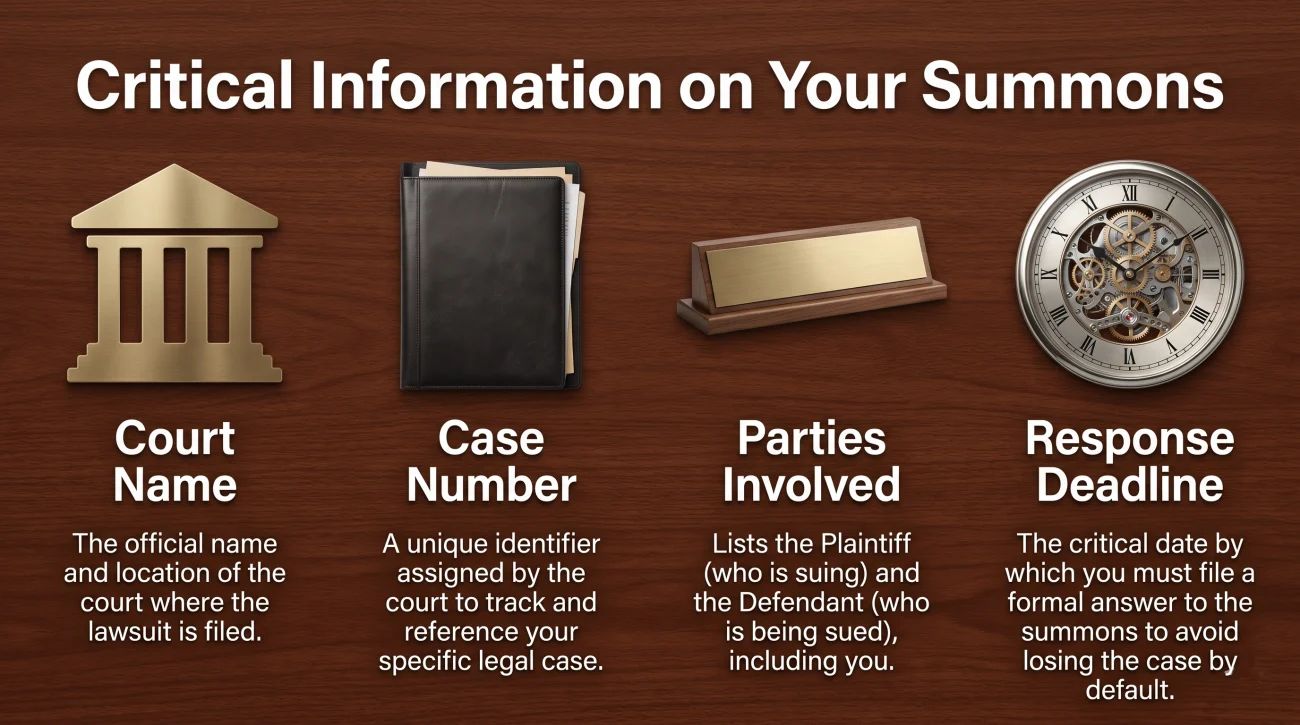

On a legitimate Summons document, you will typically find the following critical information:

- 📌 The name and physical address of the specific court where the lawsuit was filed.

- 📌 The case number (sometimes called a docket number) assigned by the court clerk.

- 📌 The names of the Plaintiff (the company suing you) and the Defendant (you).

- 📌 The exact number of days you have to file a formal written response with the court.

This deadline is absolute and non-negotiable. It does not pause because you called the collector to argue about the balance. It does not pause because you are busy gathering old bank statements. If you need help calculating exactly when your time is up based on how and when you received the papers, you must prioritize finding the exact response window on your paperwork before taking any other action.

The Complaint: The Collector’s Claims and the Strategy of Vagueness

Attached directly behind the Summons is the Complaint (in some jurisdictions, this is referred to as the Petition). While the Summons comes from the authority of the court, the Complaint is drafted entirely by the debt collector’s attorney. This document is essentially their wish list. It outlines who they are, why they believe you owe them money, their legal theory for suing you, and the exact dollar amount they want the judge to award them.

If you are being sued by a third-party debt buyer, you might be surprised by how incredibly thin the Complaint is. Readers frequently tell me they expected to receive a thick file of evidence proving the debt, but instead, they got two or three generic, repetitive paragraphs.

This vagueness is not a legal technicality or an oversight. It is a deliberate strategy based entirely on how the debt buying industry operates behind the scenes.

Example of a typical debt buyer complaint paragraph:

“Defendant entered into an agreement with Original Creditor. Defendant defaulted on the account. Plaintiff purchased the account and is now the lawful owner. Defendant owes Plaintiff $4,250.00 on an open account, plus costs.”

Why doesn’t the Complaint include your original signed credit card contract? Why doesn’t it include a line-by-line accounting of every purchase, late fee, and interest charge? Because in the vast majority of cases, the debt buyer simply does not possess those documents when they file the lawsuit.

The Debt Buyer Spreadsheet Reality

To understand why the Complaint looks the way it does, you have to understand how these companies acquire your debt. When a massive debt buyer purchases a portfolio of defaulted credit cards from a major bank, they are essentially buying a massive Excel spreadsheet. They pay just pennies on the dollar for rows of digital data containing names, social security numbers, charge-off dates, and final balances.

They do not automatically receive a physical warehouse full of your signed contracts and monthly statements. Getting those actual documents from the original bank costs them extra money and takes time.

Filing a bare-bones Complaint that meets only the absolute minimum legal standard is strategically correct for a collector who cannot yet prove the intricate details of the account. They file the vague documents because they are counting on the debt lawsuit timeline to end quickly in an automatic win. The vagueness is not a standard of proof, it is a signal that their documentation is likely weak.

Comparing the Two Documents Side by Side

To ensure you never confuse the two, here is a practical breakdown of how the Summons and the Complaint function differently in your case.

| Feature | The Summons | The Complaint (or Petition) |

|---|---|---|

| Author | Issued under the authority of the Court | Drafted by the Plaintiff’s (Collector’s) Attorney |

| Primary Purpose | To officially notify you of the lawsuit and deadlines | To state the allegations and the amount of money demanded |

| Critical Information | Your exact deadline to file a written response | The legal basis the collector claims gives them the right to sue |

| Required Action | Follow its timeline strictly | Respond to its specific numbered paragraphs in your Answer |

Always keep these documents together in a safe folder, but mentally separate their functions. The Summons tells you when to act. The Complaint tells you what you are defending against.

What “Being Served” Actually Means (And Why Avoidance Fails)

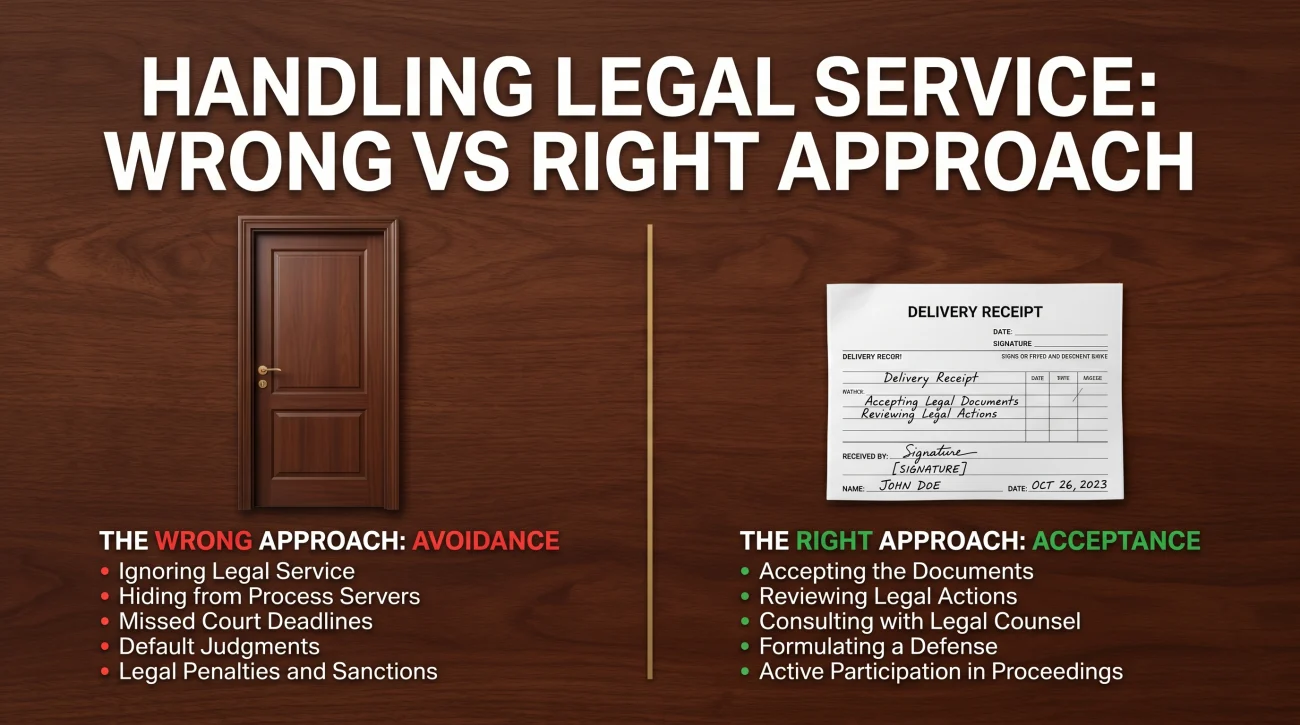

A very common misconception I hear from consumers is that if they do not physically take the papers into their own hands, or if they refuse to sign a receipt for them, they have not been officially served and the lawsuit cannot move forward. This is a dangerous myth that leads directly to lost cases.

“Being served” simply means the court is legally satisfied that you have been given proper notice of the lawsuit so that you have a fair opportunity to defend yourself.

Refusing to open the door for the process server, or telling them “I refuse to accept these” when they try to hand them to you, thinking this legally stops the clock from starting.

Accepting the papers calmly, noting the exact date and time you received them on the envelope, and immediately starting your preparation to file a written response.

At the debt buyer, some of our easiest default judgments came from people who thought they outsmarted the process server. I used to read process server notes saying things like: “Defendant refused to open door, shouted they won’t accept papers through the window.” We would log that as a refusal or substitute service, the 14-day clock would start anyway, and we would win by default because the consumer mistakenly thought they had paused the game. They didn’t.

If a process server confirms your identity at your doorstep, they can legally drop the papers at your feet, walk away, and file a sworn affidavit with the court. In many states, substitute service (handing them to another adult in your home) or service by certified mail is also perfectly legal. The bottom line you must remember is that avoidance is not a valid legal defense.

How to Verify the Papers Are Real (And Not a Scam)

Because aggressive debt collection scams are rampant, it is entirely reasonable to question whether the papers you just received are a legitimate court Summons or merely a scare tactic from a shady agency pretending to possess court authority.

When I worked in collections, we sometimes had consumers call us completely confused about papers that didn’t even come from our firm. They were from scam operations trying to intercept payments before our legitimate lawsuit ran its course. Fake summonses are specifically designed to look intimidating, but they almost always fail one simple, practical test: they cannot withstand a direct phone call to the actual civil court clerk.

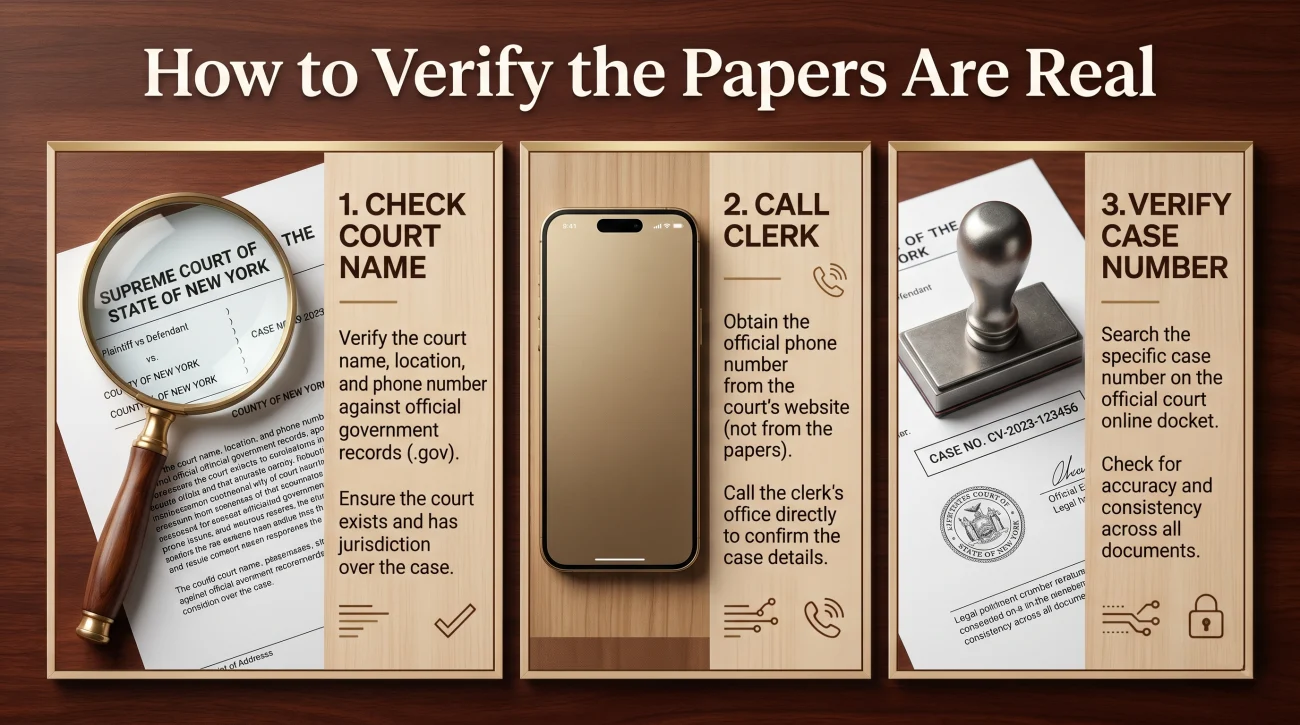

Here is the exact process to verify the documents in your hand:

- Look at the top of the Summons for the specific name of the court (for example, “Justice Court of Harris County” or “Maricopa County Superior Court”).

- Do not call any phone number printed on the Complaint or the Summons itself. Open your web browser, search for the official government website of that specific county court, and find the phone number for the civil clerk’s office.

- Call the clerk and use this script: “Hello, I received some legal papers in the mail today and I want to verify if there is an actual active case filed against me. The case number listed on the document is [Insert Number].”

💡 Pro Tip: Court clerks cannot give you legal advice, but they can absolutely confirm public facts about the court’s docket. They deal with these inquiries every single day.

If the clerk confirms the case number matches your name and the plaintiff’s name, the lawsuit is 100% real and the clock is running. If the clerk tells you that the case number does not exist in their system, you are likely dealing with a scam tactic.

Signs the Complaint Reveals a Weak Case

If you have verified that the lawsuit is real, you need to assess the strength of the collector’s claims. While receiving a lawsuit is always serious, the actual documents often reveal massive vulnerabilities in the debt buyer’s legal position. Based on how these portfolios are processed, you should look for specific red flags in the paperwork you were served.

You need to consider your defensive strategy if you notice any of the following signs in the Complaint:

- The date of your last payment or the “charge-off” date listed seems like it was many years ago. This is a major signal that the statute of limitations may have expired.

- No original credit agreement is attached to the Complaint, only a generic, recent billing statement.

- The original creditor or your original account number is not explicitly named anywhere in the document.

- The amount claimed does not match any account balance you recognize, suggesting unauthorized fees have been layered on top.

In these situations, evaluating whether your situation requires professional legal defense can completely change the trajectory of the lawsuit, as attorneys know exactly how to exploit these documentation failures.

What You Must Do Next: The Written Answer

Once you understand what the Summons and Complaint are, you have one primary objective: you must prevent a default judgment by filing a formal written response with the court, universally known as an Answer.

This sounds highly intimidating, but filing your Answer is a straightforward mechanical process. You do not need to write a complex, multi-page legal brief citing case law. A typical Answer in a consumer debt case essentially does three things:

- It responds to each numbered paragraph in the collector’s Complaint (usually by admitting, denying, or stating you don’t have enough information to know).

- It lists your “affirmative defenses” (such as the statute of limitations or mistaken identity).

- It demands that the plaintiff prove their ownership of the debt.

Calling the attorney who sued you to complain does not count as an Answer. Writing an emotional letter to the judge explaining your financial hardship does not count. You must take the specific steps for filing a formal response with the civil court.

By filing a document that states a blanket denial that forces them to prove their claims, you effectively shift the burden of proof back onto the collector. If you are unsure of how to format this document or what specific language to use, you must review what exactly to write in your defensive document so it meets the court’s basic standards without accidentally admitting fault.

What Happens After You File Your Answer

So what happens when you actually fight back? When a properly filed, contested Answer landed on my desk at the collection agency, that file was immediately pulled from the “expected automatic win” pile. We now had to make a business decision.

The moment you respond, the lawsuit becomes real litigation, and three paths typically open up:

- Settlement offers improve: Because going to trial is expensive, collectors are often much more willing to negotiate a favorable settlement once they see you aren’t going to default.

- Discovery begins: They may send you written questions, but you also gain the right to demand their original paperwork, which they often struggle to produce.

- Voluntary dismissal: If they review their file and realize they truly don’t have the chain of title or original contracts needed to beat your defenses, they may simply drop the case.

Final Thoughts: Reversing the Power Dynamic

A debt collection lawsuit is engineered to be intimidating, but it is ultimately just a business process. The company suing you is playing a numbers game, betting heavily that you will feel too overwhelmed to participate. When you understand that the Summons is just a timeline, and the Complaint is often just an unproven wish list, the paperwork loses its power to paralyze you.

Do not let a stack of generic papers dictate your financial future. Verify the case, mark the deadline on your calendar, and get your Answer filed. The moment you step into the legal arena and push back, you force them to play by the rules, and very often, that is a game they are not prepared to finish.

❓ FAQ

⏰ What happens if I ignore a debt collection summons?

If you ignore the summons and miss the deadline to respond, the debt collector will ask the court for a default judgment. The court will likely grant it automatically, which gives the collector the legal right to garnish your wages and freeze your bank accounts.

📞 Can I just call the debt collector to explain my situation instead of going to court?

Calling the collector does not stop the lawsuit or pause your deadline. You must file a written Answer with the court to protect yourself. Any phone negotiations should only happen after your formal Answer is filed.

⚖️ Do I need to hire a lawyer as soon as I get a summons?

Not always. Many people successfully file a basic Answer themselves, especially in small claims courts. However, if the balance is large, or you believe your consumer rights were violated, consulting an attorney is highly recommended.

👮 Does a court summons mean I am going to jail for unpaid debt?

No. You cannot go to jail for owing a consumer debt like a credit card or medical bill. This is a civil lawsuit, not a criminal matter. The worst outcome is a financial judgment against you.

🏠 What if the process server left the summons with my roommate?

In most states, leaving the papers with a competent adult who lives at your residence is considered valid “substitute service.” The clock on your deadline starts running, so you must treat it as officially served.

💸 Can I still settle the debt after I have been served with a summons?

Yes. Most debt collection lawsuits actually settle before going to trial. However, it is crucial that you file your written Answer first to prevent a default judgment while you are negotiating.

📅 What does a “return date” mean on my summons?

In some courts, instead of saying you have 20 days to respond, the summons will list a specific return date. This is the exact calendar date by which your written Answer must be filed, or a hearing you must attend.

🏢 Why is the company suing me a name I have never heard of?

You are likely being sued by a third-party debt buyer. These companies purchase defaulted accounts from original creditors (like your bank) for pennies on the dollar and then file lawsuits to collect the full balance.

📄 What if the amount listed in the complaint is wrong?

Debt buyers frequently add unauthorized fees and interest. You can dispute the specific amount in your written Answer, forcing them to provide an itemized accounting of how they reached that number.

🛡️ Can I stop a summons by refusing to sign for certified mail?

No. Refusing delivery does not protect you. Courts often consider the mailing attempt as sufficient legal notice, and the collector will simply proceed to get a default judgment while you remain unaware of the timeline.

What each stage of litigation requires and where your leverage sits.

- What the lawsuit process looks like from summons to judgment

- What to file, when to file it, and what happens if you do not

- The legal arguments that can defeat a debt collection lawsuit

- What a default judgment allows collectors to do and how to fight one

- How to negotiate a resolution once litigation has started

Once judgment is entered, collectors gain tools they did not have before.

- The FDCPA violations collectors commonly commit during the collection process

- How to respond to a debt lawsuit and what defenses are available to you

- How a judgment becomes a garnishment order on your paycheck

- When a collector uses a judgment to freeze your bank account instead

- How to settle before the judgment turns into something harder to stop

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.