- A bank levy is not a mistake. It means a debt collector already sued you, won a judgment, and obtained a court order to freeze your funds.

- Federal law protects specific types of income like Social Security and VA benefits, but you must take fast legal action to prove those funds are exempt.

- You have a very short time window to challenge the freeze before the bank permanently transfers your money to the collector.

- Trying to fix this by calling the collection agency directly gives them more leverage. Your best immediate move is getting a professional case evaluation.

The Moment Your Account Stops Working

You tried to pay for groceries and the card was declined. You opened your banking app expecting to see your normal balance, but instead, the available funds show zero or a negative number. There might be a vague note about a legal hold or a pending levy. You are not dealing with a banking glitch. A debt collector just executed a bank levy against you.

This is the most aggressive collection tool in the industry playbook. It hits without warning and instantly cuts off your access to your own money. When you are suddenly unable to pay rent, buy food, or put gas in your car, panic is the natural response.

From my years working inside collection agencies, I can tell you that freezing a bank account is a highly calculated move. It is designed specifically to force your hand. Understanding what legally happened behind the scenes is the only way to figure out what to do next without making the situation worse.

What Just Happened and How It Is Legal

A debt collector cannot simply wake up one morning and decide to freeze your bank account. The law requires a specific chain of events to take place before a bank will ever restrict your funds. If your bank account is frozen due to debt, it means you have already lost a lawsuit.

Somewhere in the past, the collection agency filed a lawsuit against you. You may not have known about it. Perhaps the summons was delivered to an old address, given to a roommate who never handed it to you, or you simply ignored the paperwork because you did not know how to respond. When you fail to show up in court, the judge grants the collector a default judgment.

That judgment changes everything. It transforms an unverified debt into a court-ordered mandate. With a default judgment in hand, the collector requested a writ of execution or a bank levy order. They served that order directly to your bank. By law, your bank must comply with the court order and freeze the funds in your account up to the total amount owed.

Key Point: Your bank did not betray you. They are legally required to freeze your account when served with a valid court order. Getting angry at the bank teller will not unfreeze your money.

This legal reality dictates your next steps. You are no longer just dealing with an aggressive debt collector. You are dealing with a court order. To get your money back, you must address the legal mechanism holding it in place.

The Immediate Fallout and the Legal Timer

The immediate pain of a frozen bank account goes far beyond the frozen balance itself. When a debt collector executes a levy, the financial collateral damage starts compounding within hours.

Any automatic payments scheduled for your mortgage, car loan, or utility bills will bounce. Checks you wrote days ago will be returned for insufficient funds. Your bank will likely start hitting you with overdraft fees and non-sufficient funds penalties for every single transaction that fails. You are suddenly trapped in a situation where you cannot pay your core living expenses.

This brings us to the most critical factor you are facing right now. The money in your account has not been sent to the debt collector yet. It is frozen in place. The bank is holding it in suspense while a legal timer ticks down.

Once your account is restricted, you typically have a window of 10 to 30 days depending on your specific state laws to challenge the freeze. However, the operational reality of the legal system means you really only have about 72 hours to decide on a course of action. Court paperwork takes time to draft, review, and file. If you wait until the last minute to start looking for help, the funds will be gone.

Understanding Exempt Funds

Not all money in your bank account is legally available for a debt collector to take. Both federal and state laws protect specific types of income from being seized through a bank levy. If your frozen account contains these protected funds, you have a strong legal pathway to get the account unfrozen.

Under federal law, several common types of income are strictly exempt from debt collection levies. These typically include Social Security benefits, Supplemental Security Income, Veterans benefits, federal retirement benefits, and federal disability payments. Many states also add their own protections for unemployment benefits, worker’s compensation, and a baseline amount of wages.

Assuming the bank automatically knows your money is exempt and will release it for you without any legal paperwork.

Recognizing that the burden of proof is on you to legally demonstrate to the court that the frozen funds fall under an exemption category.

If two months of Social Security payments were directly deposited into your account, the bank is supposed to automatically protect those specific funds under a federal banking rule. However, if your account contains a mix of exempt benefits and regular wages, the situation becomes highly complicated. The collector will aggressively try to take the non-exempt portion, and the bank will simply freeze everything until the court tells them otherwise.

The Collector’s Playbook: How They Picked You

To navigate this emergency, it helps to understand what the person on the other side of the desk is trying to accomplish. A debt collector does not execute a bank levy blindly. It costs the agency time and court fees to locate your bank and serve the paperwork. We looked for specific signals before spending that money.

Inside the agency, we actively monitored accounts for red flags that indicated a high probability of a successful levy. We prioritized files where we saw consistent direct deposit patterns from a known employer, high balance thresholds reported by skip-tracing vendors, or recent credit applications that revealed active banking relationships.

“A bank levy was our highest-leverage tool. We did not use it hoping to quietly drain a few hundred dollars. We used it to force the consumer to the negotiating table immediately. We knew that cutting off your cash flow was the fastest way to make you pick up the phone.”

The collector wants you to panic. They are betting that the stress of missed rent and bounced checks will make you agree to anything just to get the freeze lifted. They hold all the leverage because they already have the court judgment.

When consumers call the agency directly in a panic, they almost always make critical mistakes. They accidentally reveal where they work, creating a target for wage garnishment. They mention other bank accounts they hold, handing over new targets if the current levy does not satisfy the total balance. Calling the agency directly to beg for your money is the single biggest tactical error you can make during a levy.

What Happens Next If You Do Nothing

Some people assume that once the account is frozen, the situation is finalized and they just have to accept the loss. This is exactly how the collection agency secures easy revenue.

If you ignore the notices and let the holding period expire, the bank lifts the freeze by issuing a cashier’s check directly to the court or the collection agency. Your money is permanently transferred. Once that transfer clears, the amount is credited against your judgment balance.

But the problem does not end there. If the money seized in the levy does not cover the full amount of your debt plus accumulated interest, the judgment remains active. The collector will simply wait a few months, monitor your credit profile to see when you have rebuilt your savings, and file another levy order to freeze the account all over again. Doing nothing guarantees a cycle of repeated financial hits.

Your Immediate Options for Resolving the Freeze

If you are wondering what to do if your bank account is frozen, you generally have three distinct paths. None of these are simple weekend projects. They involve the legal system and require precision.

Your most direct path to unfreezing the account is filing a claim of exemption. If your funds fall under the protected categories we discussed earlier, you must file a formal claim with the court. This requires submitting specific legal forms, providing bank statements as evidence, and scheduling a hearing.

“Inside the agency, we saw hundreds of exemption claims denied not because the funds weren’t legally protected, but because the consumer missed a local filing deadline by one day or formatted the paperwork wrong. The court does not give you grace points for trying. We won those cases on technicalities.”

If your funds do not qualify for an exemption, another approach involves negotiating a release directly with the judgment creditor. Since the levy is a pressure tactic, the collector is sometimes willing to lift the freeze if you agree to a lump-sum settlement or a strict payment plan. However, negotiating from a position where your money is already held hostage is incredibly difficult. Without a professional intervening to apply counter-leverage, the agency has no incentive to offer you a fair deal.

Finally, you might have grounds to attack the root of the problem by challenging the underlying judgment itself. If you were never properly served with the original lawsuit, you can file a motion to vacate the default judgment. Vacating the judgment destroys the collector’s legal authority to hold the levy. This maneuver requires proving improper service or establishing a valid defense to the original lawsuit, which completely resets the playing field.

Who Can Actually Help You With a Levy

When dealing with a bank levy, consumers often get confused about who to hire. The reality is that you actually have two separate problems occurring at the same time: the immediate emergency of the frozen funds, and the underlying debt that caused the lawsuit in the first place.

To challenge the freeze directly, file an exemption claim, or vacate a default judgment, you need a debt defense attorney. They handle the acute legal emergency and communicate with the court to protect your current assets.

However, an attorney does not make the original debt vanish. If you have significant unsecured debt spread across multiple credit cards or collection agencies, surviving one bank levy just delays the inevitable. This is where a debt settlement or debt relief program comes in. While a relief program cannot magically unfreeze an account that was levied yesterday, it is often the necessary next step to negotiate the total balance down and resolve the core problem so you never face a lawsuit again.

You need to assess both sides. Talk to a legal professional to evaluate the active freeze, and consider a free debt relief consultation to see if a settlement program can permanently clear the remaining balances off your record.

How to Get Information From Your Bank

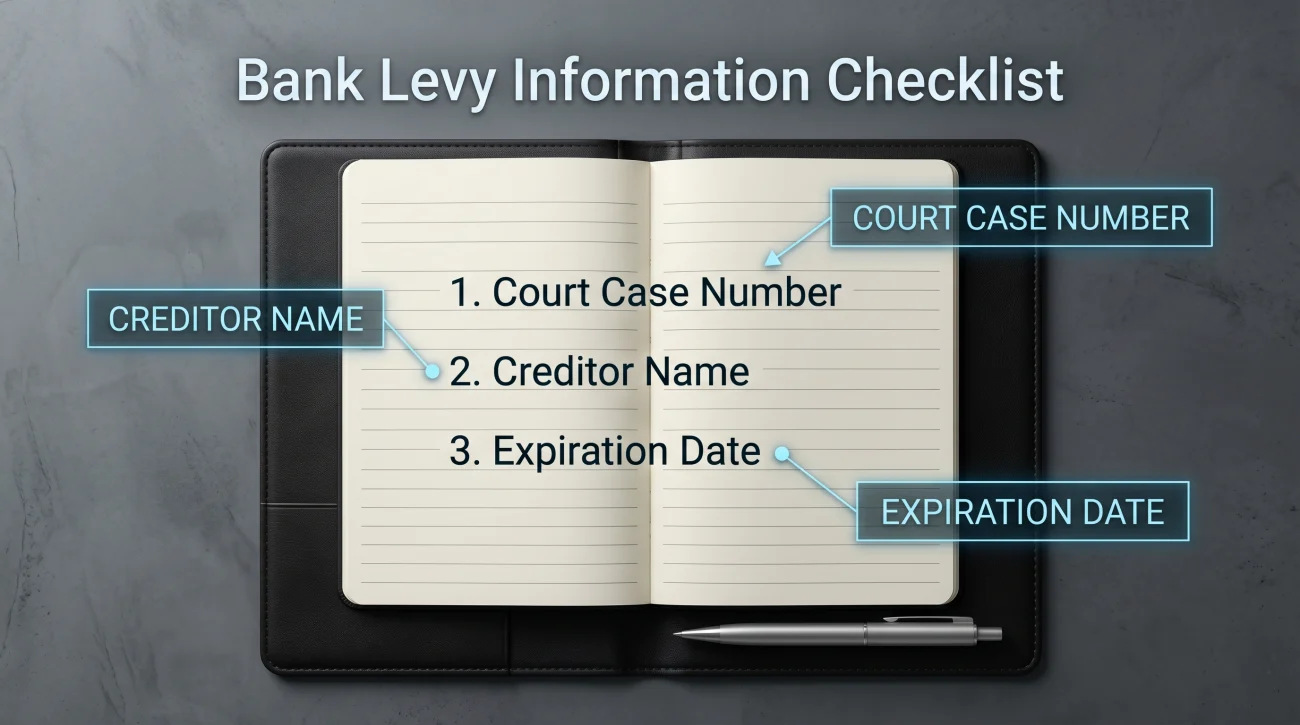

Before any professional can help you, they need to know exactly who is freezing the account and under what authority. Your bank teller cannot give you legal advice, but they are required to provide you with the documentation of the levy.

Call your bank’s main customer service line or visit a branch and ask for the legal department. You need to gather three critical facts to move forward:

- The specific court case number and jurisdiction where the judgment was filed

- The exact name of the creditor or collection agency that ordered the levy

- The specific date the holding period expires before your funds are transferred

You can use this approach when speaking to the bank representative:

“My account currently shows a legal hold or freeze. I need you to provide me with the name of the creditor who filed the levy, the court case number, the state and county where the judgment was filed, and the exact date the holding period expires before funds are transferred.”

Write this information down exactly as it is given to you. Any professional reviewing your case will need this court number immediately to look up the docket and see what the collector has filed.

Common Mistakes When Your Account is Frozen

When consumers are suddenly locked out of their cash, they often make critical errors that lock in their losses permanently. Avoiding these mistakes is just as important as taking the right actions.

- ❌ Depositing more money. The levy often applies to the account itself up to the judgment amount. If you deposit your next paycheck into the frozen account, those new funds will likely be trapped by the same levy.

- ❌ Assuming the freeze lifts on its own. The account only unfreezes when the debt is paid, the funds are forcibly transferred, or a judge orders the release. Time does not heal a bank levy.

- ❌ Trying to hide money. Attempting to rapidly transfer funds out of other accounts to hide them from the collector can sometimes be viewed as fraudulent conveyance, creating much bigger legal problems.

Final Thoughts on Surviving a Bank Levy

A frozen bank account is the peak of the debt collection cycle. It represents a total loss of financial control. The debt collector has bypassed the letters, gone through the court system, and reached directly into your pocket.

The holding period is your last line of defense. The money is frozen, but it has not been transferred yet. Every day you wait to get a professional assessment is a day closer to that money disappearing for good. Do not try to navigate complex court procedures or face a hostile judgment creditor alone while your rent money is on the line.

Your situation requires an immediate strategy. Find out if your funds qualify for an exemption, if the judgment can be challenged, and what relief options exist for the overall debt. Request a free case review today to explore both your legal options for the active levy and debt settlement solutions for your underlying balances.

❓ FAQ

🏦 Can a debt collector freeze my bank account without notice?

Yes, the actual freezing of the account happens without warning to prevent you from withdrawing the funds. However, the freeze can only happen after a lawsuit and a court judgment. You should have received a summons for the initial lawsuit, though many consumers miss or ignore it.

⚖️ How long does a debt collector freeze a bank account?

The initial freeze is temporary, usually lasting a holding period of 10 to 30 days depending on your state. After that period expires, if you have not successfully challenged the levy in court, the bank permanently transfers the frozen money to the debt collector to pay off the judgment.

🛑 How can I stop a bank account levy immediately?

The fastest ways to address a levy are filing a claim of exemption if your funds are protected by law, negotiating a settlement directly with the creditor to release the hold, or filing for bankruptcy, which triggers an automatic stay. All of these options require fast legal action.

👥 Can a debt collector freeze a joint bank account?

Yes, in most states, a debt collector can freeze a joint bank account even if only one person on the account owes the debt. The non-debtor owner must then step in and file paperwork with the court to prove which specific funds belong to them and are not subject to the judgment.

⏰ Can a debt collector freeze my account more than once?

Yes. If the money seized in the first levy does not cover the total amount of the judgment, the collector can return to court later and request another levy against the same account or a different account you own until the debt is fully satisfied.

Four areas of the collection process. Start wherever your situation applies.

Some situations have deadlines attached. These pages are written for those situations.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.