- A wage garnishment is a legally binding court order. Your employer cannot simply choose to stop withholding your money, and calling the collector to ask for mercy will not work.

- Once garnishment begins, up to 25 percent of your disposable income can be legally seized from every paycheck until the debt is paid in full.

- There are legal mechanisms to interrupt or stop a garnishment, including claiming state exemptions, negotiating a lump sum settlement, or filing for bankruptcy protection.

- Because state laws vary heavily and the clock is ticking on your next paycheck, determining which path will actually stop your garnishment requires a professional case review.

The Shock of the Missing Paycheck

You looked at your direct deposit, and the number was wrong. Not just a slight miscalculation on your hours or a tax bracket adjustment, but significantly wrong. You called your human resources department expecting them to fix a simple payroll error.

Instead, they told you something that made your stomach drop: they received a court order from a debt collector. They are legally required to withhold a portion of your income before the money ever hits your bank account.

You are not imagining the financial panic you feel right now. A wage garnishment is the most aggressive and disruptive tool in the entire debt collection playbook. It bypasses your ability to prioritize your own bills, your rent, and your family’s needs, sending your hard-earned money directly to a creditor.

If you are reading this, you do not need a theoretical lecture on how debt collection works. You are in financial emergency mode. You need to know what this order means, how the collector got the power to take your money, and most importantly, what can actually stop a wage garnishment from draining your next paycheck.

The Reality Check: How a Collector Got Access to Your Wages

A wage garnishment does not happen overnight, even if it feels like an ambush. A debt collection agency cannot simply call your employer and demand part of your salary just because you owe them money.

To get a garnishment order, the collector had to follow a specific legal process. They had to file a formal debt collection lawsuit against you. They had to serve you with a summons. And ultimately, they had to win a judgment in court.

You might be thinking: “I never went to court. I never saw a judge.”

In the vast majority of cases, you do not have to. Over 70 percent of debt collection lawsuits end in what is called a default judgment. This happens when a consumer receives a summons but fails to file a formal written response with the court. When you do not respond, the court assumes the collector’s claims are valid and grants them the judgment by default.

“From my years inside a collection agency, securing a wage garnishment was the ultimate finish line for a file. Once a judge signed that order and we sent it to the debtor’s employer, we stopped working the account. We didn’t have to make aggressive calls anymore. We just sat back and waited for the checks to arrive every payroll cycle. The pressure was entirely off us, and entirely on the consumer.”

That is the reality of your current situation. The collector is no longer trying to convince you to pay. They have weaponized the legal system to take the payment automatically. Knowing this history does not put the money back in your pocket today, but it is crucial for understanding why informal promises will no longer work.

Many people panic and call the collection agency, offering a small monthly payment plan if they will just stop the garnishment. The collector will usually refuse. They already have a guaranteed mechanism to take 25 percent of your check. They have no incentive to accept a smaller, voluntary payment.

The only way to stop a court order is with another legal action. You must use the legal system to challenge the exemption status, force a settlement, or trigger a legal freeze on collection activities.

Why Doing Nothing is the Worst Possible Option

Since calling the collector to ask for mercy is off the table, human nature often defaults to avoidance. Some consumers hope that the garnishment is a one-time penalty or that it will naturally fall off after a few weeks. It will not.

In most standard cases, a creditor is legally permitted to garnish a specific percentage of your disposable earnings, which is commonly up to 25 percent.

To put that into practical terms: if your disposable earnings (what is left after mandatory deductions like taxes) are $1,000 per week, the collector can take $250 out of every single check. That is $1,000 a month disappearing from your household budget.

📌 Note: Bank Levy vs. Wage Garnishment

Many people confuse these two aggressive collection tactics. A wage garnishment takes money from your paycheck before you ever receive it. A bank levy freezes the money already sitting in your checking or savings account. If a collector has a judgment against you, they can often deploy both methods simultaneously.

The garnishment will not stop until the total judgment balance is paid in full. Furthermore, judgments often accrue post-judgment interest. If you have a large balance, you could be losing a quarter of your income for years.

Every paycheck that is processed while you wait is money that is permanently gone. You cannot retroactively un-garnish wages that have already been disbursed to the creditor. The clock is ticking constantly toward your next payroll date.

The Paths That Can Actually Stop a Wage Garnishment

You cannot simply ask your employer to ignore the order. Your employer is legally bound to comply; if they refuse, the court can hold the employer financially responsible for your debt. The solution must come from the legal side.

There are generally four paths to interrupt or stop an active wage garnishment. None of them are simple, and all of them require moving quickly.

Path 1: Filing a Claim of Exemption

Federal and state guidelines protect certain types of income from being seized by creditors. If your income falls into these protected categories, you can file a formal claim with the court to reduce or completely stop the garnishment.

Protected funds often include Social Security benefits, disability payments, veteran’s benefits, and certain types of pension income. Additionally, many states have “head of household” exemptions that protect a larger portion of your wages if you provide the primary financial support for dependents.

The challenge here is procedural. Exemptions are not automatic. You typically must file a specific legal response with the court that issued the judgment, and there is usually a strict deadline to act after receiving the notice. If you miss the deadline or file the paperwork incorrectly, you forfeit your right to the exemption.

Path 2: Negotiating a Lump-Sum Settlement

It sounds counterintuitive: why would a collector settle the debt if they are already successfully garnishing your wages?

The answer comes down to the time value of money. If you owe $15,000, and your garnishment is pulling $150 a week, it will take the collector nearly two years to recover the full amount. Collectors want cash today.

If you have access to a lump sum of money, perhaps from a tax refund, a family member, or selling an asset, you can sometimes negotiate a deal. You offer them a guaranteed, immediate lump sum (for example, $8,000 to settle the $15,000 debt) in exchange for them voluntarily filing a release of the garnishment with the court.

This is a delicate negotiation. If you signal that you have access to funds, but your offer is too low, the collector will simply let the garnishment run. You have to know exactly how much leverage you possess.

Path 3: Challenging the Original Judgment

In some cases, the garnishment can be stopped by attacking the root cause: the default judgment itself. This usually involves initiating a legal challenge to overturn the judgment.

To succeed here, you typically must prove that you were never properly served with the original lawsuit. If the collector served the papers to an old address or handed them to someone who does not live with you, the court may agree that you never had a fair chance to defend yourself.

Challenging a judgment does not make the debt disappear. It simply hits the rewind button on the lawsuit, forcing the collector to prove their case from the beginning. However, the moment the judgment is overturned, the legal authority for the garnishment evaporates, and the deductions must stop.

Path 4: The Bankruptcy Automatic Stay

This is the nuclear option, but it is also the most immediate and absolute way to stop a garnishment. The moment you file for bankruptcy (whether Chapter 7 or Chapter 13), a federal injunction known as the “automatic stay” immediately goes into effect.

The automatic stay legally forces all collection activities, including wage garnishments, bank levies, and harassing phone calls, to halt immediately. Your employer will be notified, and the deductions will cease.

While bankruptcy offers immediate relief, it carries profound, long-term consequences for your credit score and financial life. A bankruptcy filing stays on your credit report for up to ten years, severely impacting your ability to rent an apartment, buy a car, or secure future credit. It is not a step to take lightly, and it is usually only appropriate if your overall debt burden is entirely unmanageable, not just because of a single garnishment.

Why You Need a Wage Garnishment Attorney to Navigate This

When you are losing a quarter of your paycheck, spending time trying to decipher state civil procedure codes is a luxury you cannot afford. This is not a situation where DIY legal tactics are advisable.

The rules governing garnishments, exemptions, and court filings are intensely state-specific. A strategy that perfectly stops a garnishment in Texas might be completely useless in Florida. Furthermore, making a mistake on a claim of exemption form or missing a strict filing deadline means you lose by default again.

A qualified debt defense or wage garnishment attorney evaluates the battlefield from a professional standpoint. When they look at your case, they are assessing multiple variables simultaneously:

- 📋 Do your income type and family status qualify for state-specific exemptions?

- 📋 Was the original summons served legally, or are there grounds to challenge the judgment entirely?

- 📋 Did the collection agency commit any FDCPA violations during their pursuit of the debt that could give you counter-leverage?

- 📋 Is the total balance low enough that a lump-sum settlement makes financial sense?

- 📋 Does your overall financial picture indicate that a bankruptcy filing is the most logical protective measure?

An attorney knows the exact threshold at which a collector will accept a settlement over a continuous garnishment. They know how to draft the paperwork to stop the bleeding while the negotiations take place. But before they can do that, they need to know exactly what they are dealing with.

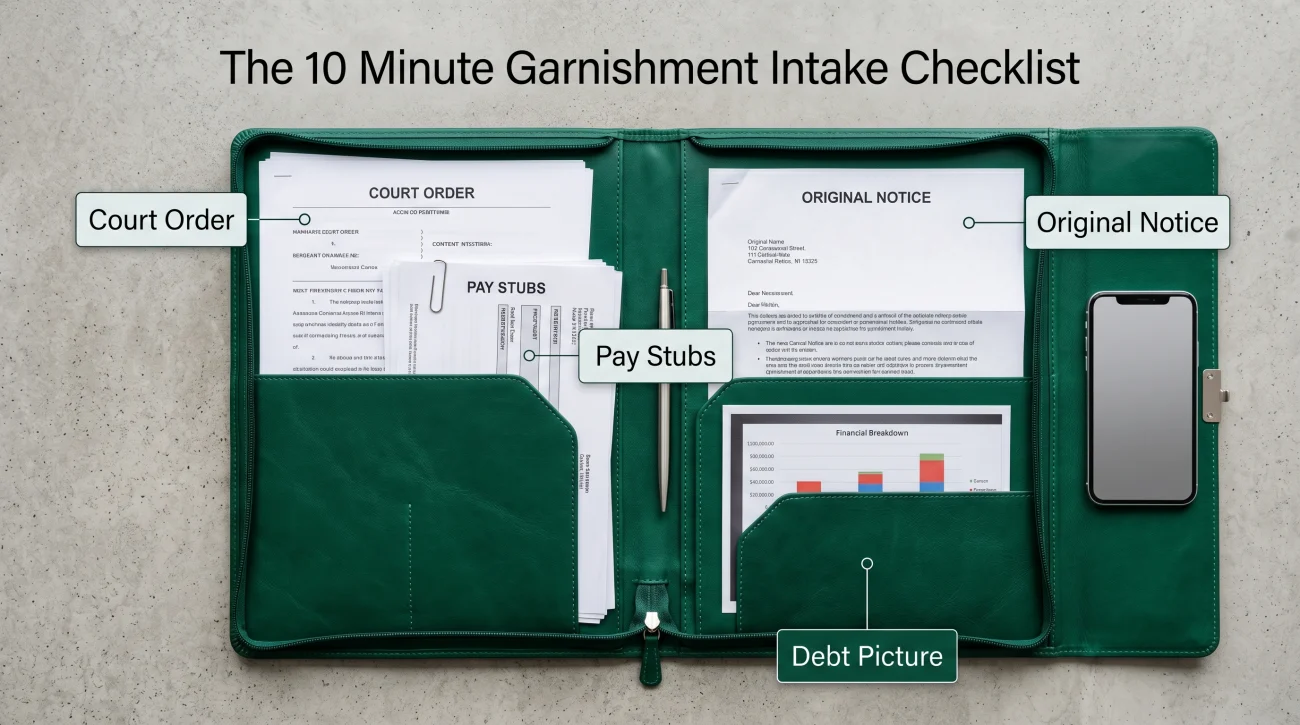

The Preparation Checklist: Don’t Make the Call Empty-Handed

If you are going to seek professional help to stop the garnishment, you need to provide the attorney with the raw data they need to assess your leverage immediately.

The 10-Minute Garnishment Intake Checklist

Before you request a case evaluation, gather the following information. Having this ready will allow a professional to tell you immediately what options are viable.

1. The Garnishment Order: Ask your HR department for a copy of the actual court order they received. This document contains the case number, the specific court jurisdiction, and the name of the law firm representing the creditor.

2. Your Pay Stubs: Have your last three pay stubs available so the exact amount of disposable income and the deduction rate can be verified.

3. The Original Notice: Did you ever receive a summons in the mail or handed to you at your door? If so, note the date.

4. Total Debt Picture: Beyond this specific garnishment, how much other unsecured debt (credit cards, medical bills, personal loans) do you currently hold?

⚠️ Warning: Do not delay your consultation just because you cannot find every single document. Time is the most critical factor. Every day you wait brings you closer to the next payroll cycle.

Final Thoughts: Reclaiming Your Paycheck

Watching your wages be diverted to a debt collector is demoralizing, but it is not a permanent state unless you allow it to be. The legal system that gave the collector the power to garnish your wages also provides the mechanisms for you to stop it.

The open question is which specific mechanism applies to your life. Your state’s exemption laws, your specific income mix, the size of the judgment, and your overall debt burden all create a unique puzzle. There is no one-size-fits-all article that can tell you definitively whether you should file a claim of exemption, attempt a settlement, or look toward bankruptcy.

That is why taking action in the next 24 hours is paramount. You need a professional to look at the math, assess the court order, and deploy the right legal strategy before your next paycheck is processed.

If your wages are actively being garnished, you need to understand your legal options immediately. Talk to a wage garnishment attorney to get a free case evaluation and find out what can actually be done to protect your income today.

❓ FAQ

🛑 How can I stop a wage garnishment immediately?

The fastest ways to stop a wage garnishment immediately are filing for bankruptcy (which triggers an automatic stay) or successfully filing a claim of exemption if your income qualifies under state law. Both require filing formal legal documents with the court.

📝 Can I stop a garnishment without hiring an attorney?

While individuals can technically represent themselves, navigating the court system, filing the correct exemption paperwork, and hitting strict state-specific deadlines is incredibly risky. A single procedural mistake usually results in the garnishment continuing.

💸 What happens to the money already taken from my paycheck?

In almost all cases, wages that have already been garnished and disbursed to the creditor cannot be recovered. This is why acting immediately to stop future deductions is so critical.

💼 Can my employer fire me because of a wage garnishment?

Generally, labor protections prevent an employer from firing you for having a single wage garnishment against you. However, those typical protections often do not apply if you have multiple garnishments from different debts.

💰 Can a debt collector take my entire paycheck?

No. For standard consumer debts like credit cards or medical bills, garnishments are generally capped at a specific percentage of your disposable earnings, which is commonly 25 percent in many standard cases.

📞 Will calling the debt collector stop the garnishment?

Generally, no. Once a collector has gone through the expense of a lawsuit to secure a court-ordered garnishment, they will rarely stop it simply because you ask or promise to make voluntary payments. They will only stop it if forced legally or if a highly favorable lump-sum settlement is reached.

⏳ How long does a wage garnishment last?

A wage garnishment lasts until the underlying judgment is fully satisfied. This means it will continue deducting money from your paychecks until the original debt amount, plus any court fees and accrued post-judgment interest, is paid down to zero.

🏦 Can debt relief stop a wage garnishment?

Debt relief programs have significantly less leverage once a judgment is entered and a garnishment is active. While an attorney or negotiator can still attempt to settle a judgment, the collector holds most of the power since they are already receiving forced payments.

Four areas of the collection process. Start wherever your situation applies.

Some situations have deadlines attached. These pages are written for those situations.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.