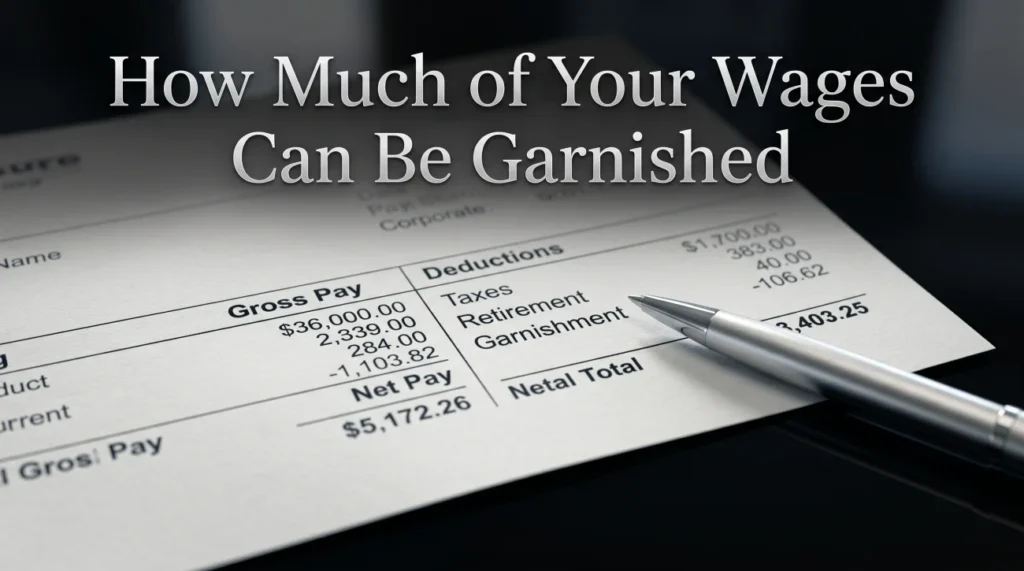

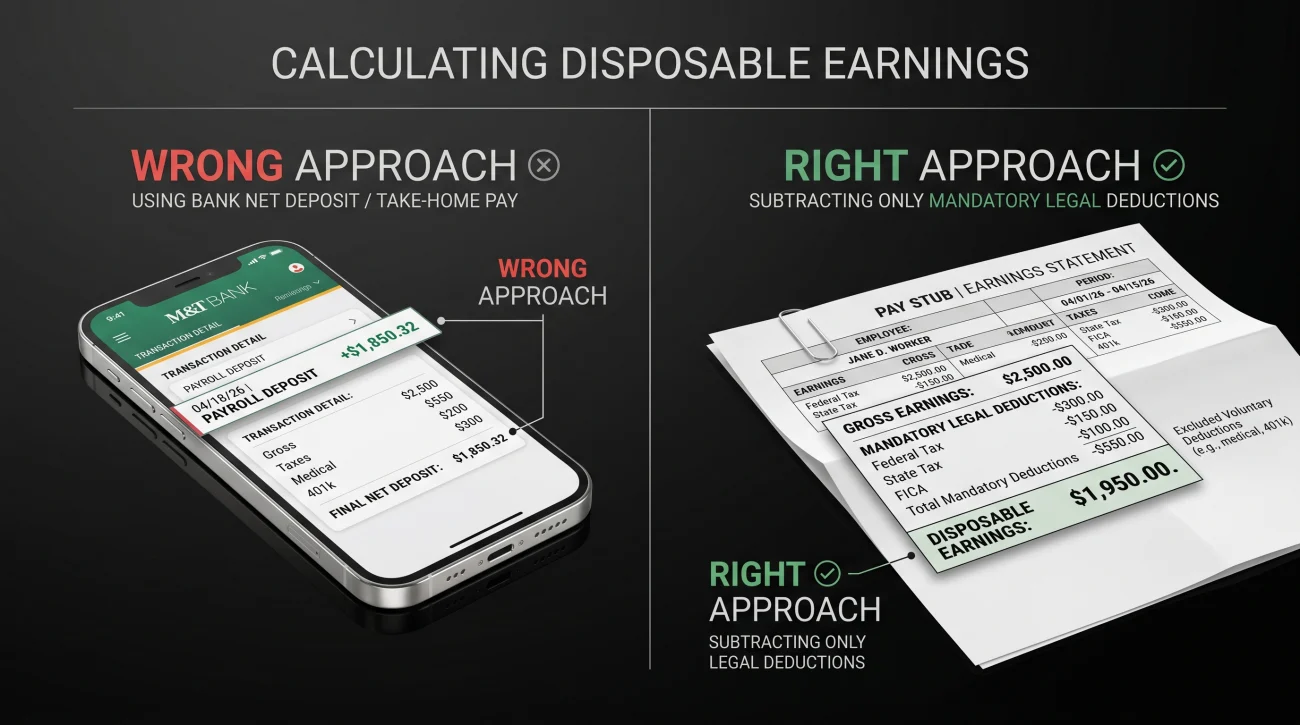

- The amount garnished is not based on your final take-home pay. It is calculated using a specific legal definition called “disposable earnings,” which only excludes legally required tax deductions.

- Voluntary deductions like health insurance premiums and 401k contributions do not protect your wages. The court considers that money available for debt collection.

- For consumer debt, federal law caps garnishment at 25% of your disposable earnings, or the amount that exceeds 30 times the federal minimum wage, whichever results in a lower deduction.

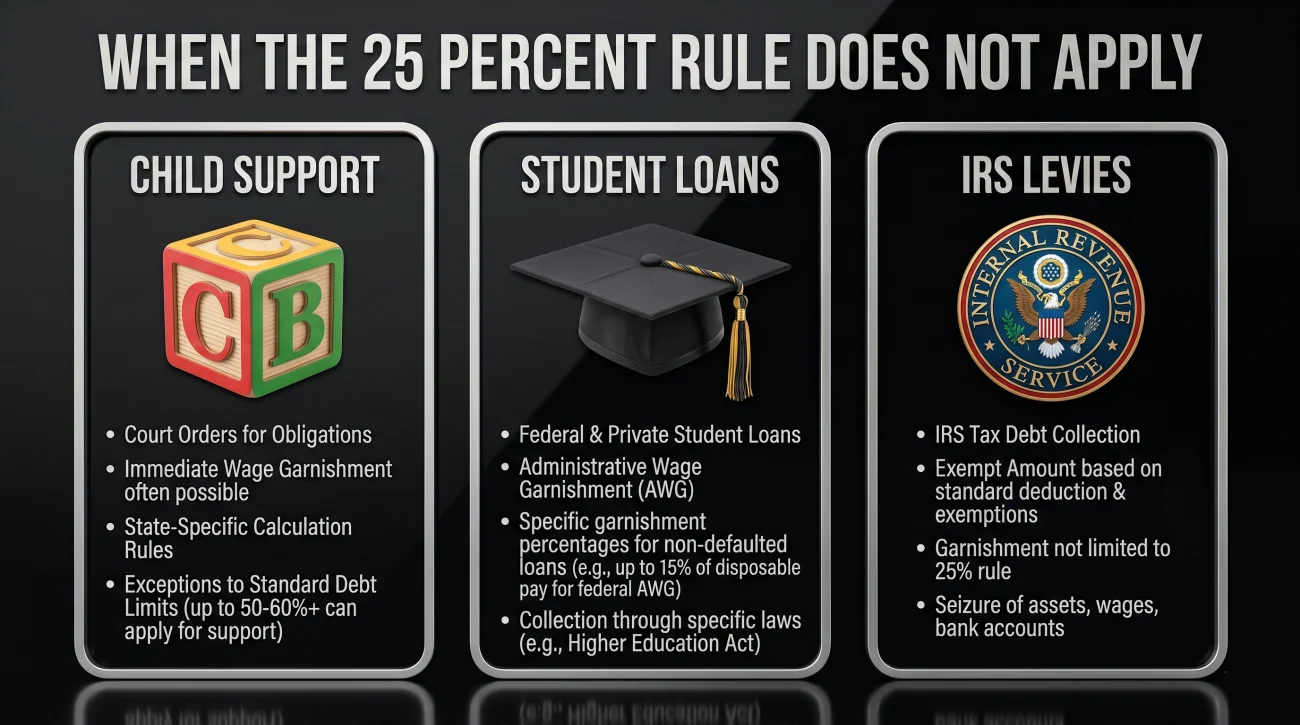

- Child support, federal student loans, and IRS tax levies follow completely different rules. Child support can take up to 65%, while the IRS has no percentage cap at all.

- If your state has stricter garnishment limits than the federal government, your employer is legally required to follow the state law to give you more protection.

The Reality of the Numbers on Your Pay Stub

In my 12 years working inside third-party collection agencies and debt buying firms, I listened to thousands of inbound calls from panicked consumers who had just received their first paycheck after a garnishment order took effect. Almost every single time, the confusion started from the exact same place. The consumer had done the math in their head, assuming the collector was going to take 25% of the money they usually brought home. When they looked at their pay stub and saw a much larger chunk of their wages missing, they immediately assumed their employer had made a mistake or the collection agency was breaking the law.

The hard truth is that wage garnishment calculations are not based on what feels fair, nor are they based on the money that actually hits your bank account. The system operates on a rigid, specific legal definition of what counts as income. Misunderstanding this formula is the primary reason people lose their leverage and fail to protect the money they are legally entitled to keep.

This guide will break down exactly how the 25% limit works in the real world. We will cover why your actual take-home pay is not the number the court uses, how the federal calculation protects low-income earners, and the specific scenarios where this rule is completely thrown out the window. Once you understand the mechanics of the math, you can accurately audit your own pay stubs and know immediately if a collector or your payroll department has crossed the line.

Disposable Earnings: The Biggest Trap in Garnishment Math

Every piece of confusion regarding federal garnishment limits stems from one legal term: disposable earnings. Most people logically assume that “disposable” means the cash they have left over after their bills are paid, or at the very least, the net pay deposited into their checking account after all employer deductions. That assumption is incorrect, and it is a costly mistake to make.

Under Title III of the Consumer Credit Protection Act (CCPA), disposable earnings represent your gross pay minus ONLY the deductions that are legally required by law. These legally required deductions are strictly limited to federal income tax, state and local income taxes, the employee’s share of Social Security taxes, Medicare taxes, and mandatory state unemployment insurance. That is it. Nothing else counts.

The law views voluntary deductions, such as health insurance premiums, 401k contributions, or union dues, as income that is still available to pay your judgment creditor.

“This is consistently where consumers lose leverage. I would review accounts where a debtor called in furious, claiming they couldn’t buy groceries because we took too much. I would look at their employer’s worksheet and see they had hundreds of dollars going into a 401k and a top-tier health plan. The collection system does not care about your retirement or your voluntary benefits. The court calculates the 25% before those voluntary deductions are ever removed.”

Let us look at a practical example of how this plays out on a real pay stub. Assume your gross pay is $1,000 per week. Your legally required taxes amount to $200. You also choose to have $150 deducted for health insurance and $50 for your retirement account. The actual net pay deposited into your bank account is $600. However, your disposable earnings for the garnishment calculation are $800 ($1,000 gross minus $200 in required taxes). The creditor is allowed to take 25% of that $800 figure, not 25% of your $600 net pay.

Looking at the final net deposit in your bank account (after taxes, health insurance, and retirement are taken out) and calculating 25% of that final number to estimate your garnishment.

Starting with your gross pay, subtracting only mandatory state and federal taxes, and then applying the 25% garnishment limit to that specific subtotal.

The Two-Test Formula for Consumer Debt

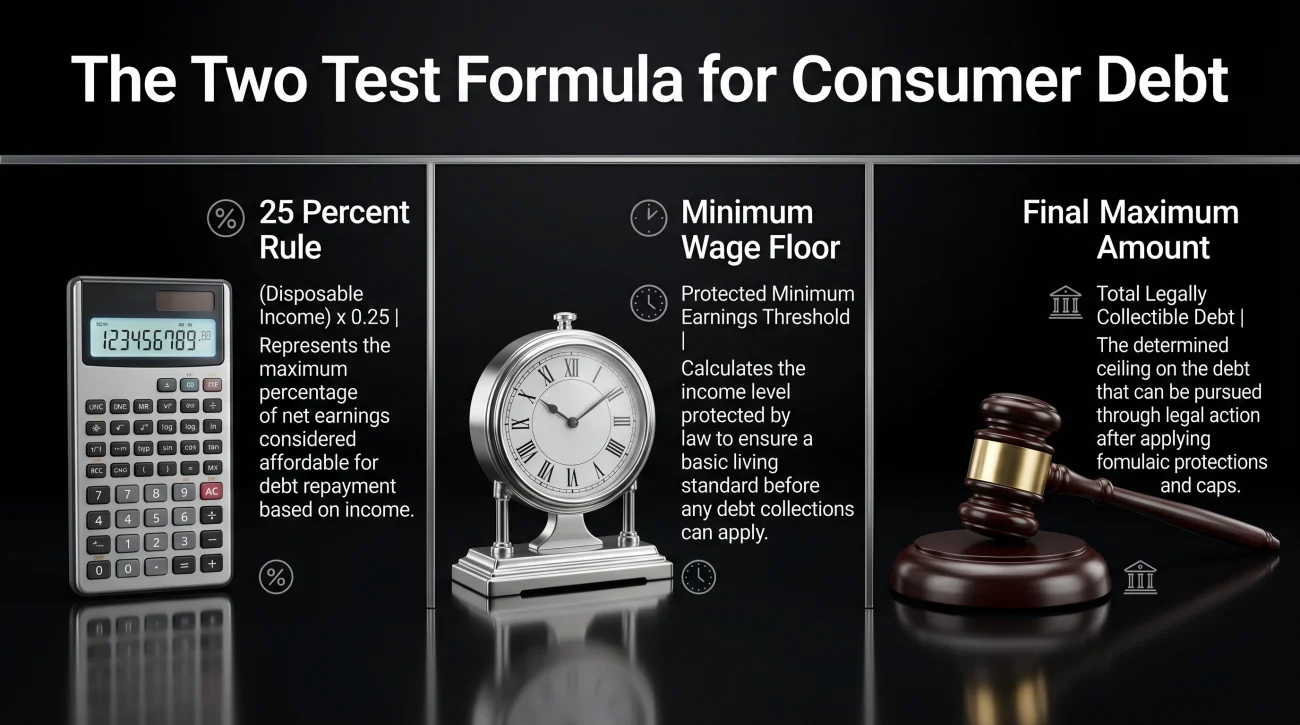

For standard consumer debts, which include credit card defaults, medical bills, personal loans, and private student loans, federal law relies on a two-test system to determine the absolute maximum that can be legally taken from your paycheck. Your employer’s payroll department is legally obligated to run both of these calculations. They must then apply whichever test results in the lower deduction amount.

The first test is straightforward: 25% of your disposable earnings. The second test acts as a protective floor: it calculates the amount by which your weekly disposable earnings exceed 30 times the federal minimum wage.

Currently, the federal minimum wage sits at $7.25 per hour. When you multiply that by 30, you get $217.50. This creates a hard baseline. If your weekly disposable earnings are $217.50 or less, nothing can be garnished for a consumer debt, regardless of how much you owe the creditor or how aggressively they want to collect.

What If You Are Paid Bi-Weekly or Semi-Monthly?

The $217.50 floor is based on a weekly pay schedule, but most Americans do not get paid every week. If your payroll runs on a different schedule, the federal floor scales up accordingly. For a bi-weekly payroll (every two weeks), the floor is exactly double: $435.00 per paycheck. If you are paid semi-monthly (twice a month), the floor is $471.25. If your disposable earnings fall below these specific numbers for your pay period, your paycheck is completely protected from consumer debt garnishment.

How Your Employer Runs the Calculation

To demystify what happens in the HR office, we need to walk through the exact mathematical steps a payroll administrator takes when they receive a writ of garnishment. Let us use an example of a worker who has $500 a week in disposable earnings.

Step 2 (Test 1): Calculate 25% of disposable earnings ($500 x 0.25) = $125.

Step 3 (Test 2): Subtract the federal floor from disposable earnings ($500 minus $217.50) = $282.50.

Step 4: Compare the results of Test 1 and Test 2. The law requires the employer to use the lesser amount.

Result: Because $125 is less than $282.50, the maximum wage garnishment for this pay period is capped at $125.

The reason this 30x minimum wage floor exists is to prevent extreme poverty. It ensures that workers earning at or near the minimum wage retain enough of their income to cover basic survival expenses like rent and food. For instance, if an employee has disposable earnings of just $250 a week, Test 1 (25%) would allow a $62.50 deduction. But Test 2 ($250 minus $217.50) results in only $32.50. Because the employer must choose the lower number, the worker is protected and only loses $32.50.

If you suspect your employer is miscalculating this formula, you need to request the documentation they are using. Many payroll software systems automate this, but human error in categorizing what is and is not a required deduction happens frequently.

Your Verification Checklist: Request the calculation worksheet from HR, verify the deduction categories yourself, and compare the math against the federal floor to ensure no errors were made.

Here is a simple, non-confrontational script you can use to request this information from your employer. You want to frame it as a personal record-keeping request rather than an accusation of wage theft.

Subject: Request for garnishment calculation worksheet

Hello [HR Contact Name],

I noticed a court-ordered deduction on my most recent pay stub. For my own personal financial records and budget planning, could you please provide me with a copy of the worksheet or the specific calculation formula the payroll system used to determine my disposable earnings for this period?

I just want to make sure I understand how my voluntary benefits are being handled alongside the federal 25% limit.

Thank you for your help,

[Your Name]

All of these calculations provide a predictable safety net for credit card and medical debt. But if the debt you owe involves the government or domestic support, that safety net disappears entirely.

When the 25% Rule Does Not Apply: Government and Support Debts

Everything we have discussed so far applies exclusively to consumer debt judgments. If your debt is owed to the government, or if it involves domestic support obligations, the consumer protection rules are completely discarded. You can learn more about how the origin of your debt dictates the collection rules in our breakdown of the different types of wage garnishment.

Child Support and Alimony

When it comes to Income Withholding Orders for child support or spousal support, the limits are pushed higher than any other category of debt. Under federal law, up to 50% of your disposable earnings can be garnished if you are currently supporting a second family (a spouse or child not covered by the support order). If you are not supporting another family, that limit increases to 60%. Furthermore, if you are more than 12 weeks behind on your support payments, the agency can add another 5% penalty, bringing the absolute legal maximum to a staggering 65% of your disposable earnings.

Federal Student Loans

The Department of Education does not need to sue you to take your wages. They use a process called Administrative Wage Garnishment (AWG). For defaulted federal student loans, the limit is capped at 15% of your disposable earnings. While 15% is lower than the consumer debt cap, the fact that it can be implemented without a court judgment or a judge’s oversight is what usually catches borrowers completely off guard.

IRS Tax Levies

The Internal Revenue Service does not play by percentage rules at all. There is no maximum cap for an IRS wage levy. Instead, the IRS relies on a specific exempt amount table, known as IRS Publication 1494. This table dictates a very modest flat amount of money you are allowed to keep based on your tax filing status and your dependents.

For example, under recent Publication 1494 guidelines, a single taxpayer with no dependents paid on a weekly basis might only be allowed to keep roughly $290 of their paycheck. Every single dollar earned above that fixed protected amount is legally seized by the IRS. In practical terms, this can result in the vast majority of a paycheck being seized, regardless of how much the person earns.

Multiple Garnishments: The Priority Ladder

A frequent and highly stressful scenario occurs when an employee has multiple garnishment orders hitting their employer at the same time. The law dictates exactly who gets paid first through a strict priority ladder, and the total amount taken is still bound by the legal caps.

Child support and alimony always sit at the top of the priority ladder. IRS tax levies generally come next, followed by federal student loans. Consumer debts like credit cards and medical bills are at the absolute bottom of the priority list. If two consumer creditors send orders, the first one received by the employer takes priority.

“I regularly saw consumer debt accounts where we successfully served a garnishment order, only to receive a notice back from the employer that the debtor was already paying 30% of their income to child support. Because child support takes absolute priority and the total consumer cap is 25%, our collection agency would get zero dollars. We just had to sit in line, sometimes for years, until the child support obligation changed or the debtor’s income drastically increased.”

The federal cap applies to the total aggregate amount garnished from your paycheck. If a higher-priority obligation is already eating up the available legal capacity, a lower-priority consumer creditor cannot legally stack another deduction on top. They have no choice but to wait in line until the priority debt is satisfied.

State Laws That Provide Stronger Shields

The federal 25% rule acts as a baseline of protection across the entire United States. However, states have the authority to pass their own laws that provide even more protection for debtors. The golden rule of wage garnishment is this: if state law offers more take-home pay to the employee than federal law, the employer is legally obligated to use the state law.

There are four states that provide the ultimate shield against consumer debt collection: Texas, Pennsylvania, North Carolina, and South Carolina. If you live and work in one of these jurisdictions, your wages are entirely off-limits for standard consumer judgments like credit cards and medical bills. Creditors in these states have to rely on different tactics, which you can read about in our guide to states that prohibit wage garnishment entirely.

Other states do not ban the practice, but they do enforce stricter math. For example, Illinois and Massachusetts limit consumer garnishments to 15% of gross wages or disposable earnings, depending on specific state formulas. New York caps it at 10% of gross wages or 25% of disposable earnings, whichever is less. Florida offers a complete exemption for individuals who can prove they provide more than half the financial support for a dependent, provided their income falls under certain thresholds. Checking the wage garnishment limits by state is a critical step in verifying your employer is playing by the right rulebook.

⚠️ Warning: If you work for a large national corporation that handles its payroll out of a different state, they will sometimes mistakenly apply the federal 25% limit instead of your specific state’s stricter protections. It is your responsibility to catch this jurisdictional error, as the payroll software may simply default to the federal standard.

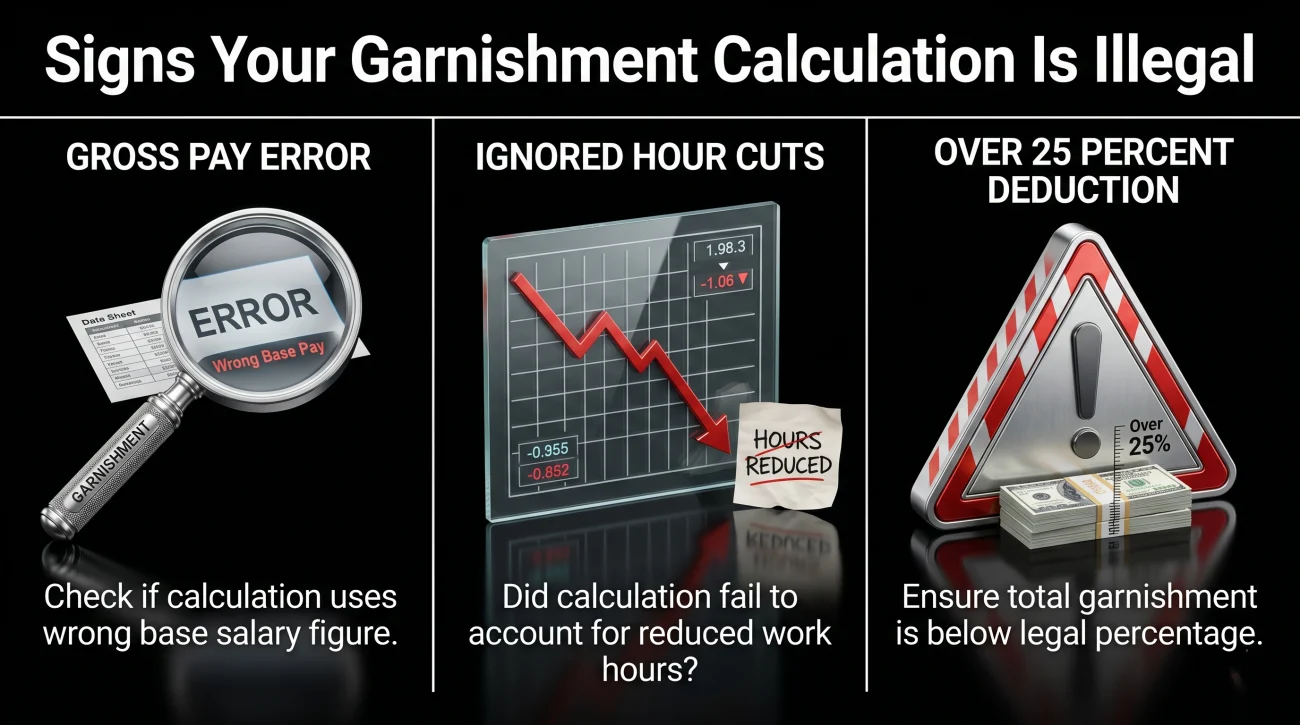

Signs Your Garnishment Calculation Is Illegal

When you are already stressed about making ends meet, it is natural to just accept the paperwork your company hands you. But payroll departments make mistakes, and automated systems frequently miscategorize income. If you are experiencing any of the following scenarios, you are likely having your wages taken illegally.

The most obvious red flag is if the amount deducted for a consumer debt is visibly higher than 25% of your post-tax income. Another massive warning sign is if your HR department calculates the 25% deduction based on your gross pay rather than your disposable earnings. For example, if your gross pay is $1,000 and your disposable earnings are $800, taking 25% of the gross takes $250 out of your pocket, while the legally correct calculation only takes $200. This is a common error in smaller companies without automated payroll software, and it artificially inflates the amount the creditor receives at your expense.

You should also be vigilant during weeks where your hours are cut. If your paycheck drops significantly, your disposable earnings might fall below the 30 times minimum wage floor. If your employer continues to take a flat 25% from a meager paycheck, this is a failure to apply the mandatory floor protection. Failing to run this secondary test means they are illegally leaving you with less than the law requires.

If any of these signs sound familiar, do not waste time arguing with your HR representative. They will not change a court order based on a verbal complaint. Your best move is to have your situation evaluated by a wage garnishment attorney. A legal professional can quickly audit your pay stub, identify the calculation violation, and file an immediate motion with the court to enforce the legal limits. Alternatively, if the math is correct but you still cannot survive, you need to explore the broader strategies on how to legally stop the garnishment process entirely.

Final Thoughts: Take Control of the Math

Understanding the disposable earnings calculation transforms you from a passive participant into an active defender of your paycheck. Do not rely on your employer’s payroll software to seamlessly navigate federal floors and state-specific exemptions. Their primary goal is compliance with the court order, not maximizing your take-home pay.

Create a dedicated folder for all your pay stubs and garnishment notices. Build a habit of reviewing your pay stub the exact day it is issued, especially if your hours fluctuate week to week. By auditing the math yourself, you ensure that the collection agency gets exactly what the law allows, and absolutely nothing more.

❓ FAQ

📞 Can my employer take more than 25% for a credit card debt?

No. Under federal law, consumer debts like credit cards are strictly capped at 25% of your disposable earnings, or the amount exceeding 30 times the minimum wage. If your state has a lower limit, the state limit applies.

🏥 Does paying for health insurance protect my paycheck?

No. Health insurance premiums, 401k contributions, and union dues are considered voluntary deductions. They do not reduce your disposable earnings, meaning the 25% is calculated before those expenses are paid.

💼 What happens if I have two garnishments at once?

The federal cap still applies to the total. If you have two consumer debt garnishments, they cannot combine to exceed 25% of your disposable earnings. The first one received usually takes priority until paid off.

🏦 Is bank garnishment calculated the same way?

No. Once the money is deposited into your bank account, the 25% wage protection no longer applies. A creditor with a bank levy can freeze the entire account balance, subject to different state bank exemptions.

📝 How do I know if my employer did the math right?

You must ask your HR or payroll department for the specific garnishment calculation worksheet. Compare their definition of your disposable earnings against your gross pay minus mandatory taxes.

📉 Can I ask the judge to lower the 25%?

In many states, yes. You can file a Claim of Exemption based on financial hardship, providing an income and expense breakdown to show the court that 25% prevents you from affording basic necessities.

👶 Why is my child support garnishment taking half my check?

Child support is exempt from the 25% consumer limit. Federal law allows up to 50% or 60% of your disposable earnings to be taken for support, plus an extra 5% if you are in arrears.

🏛️ Does the IRS have a maximum percentage they can take?

No. The IRS does not use a percentage cap. They use a table (Publication 1494) that leaves you with a fixed, small amount for living expenses and legally levies everything else you earn above that amount.

💵 What is the absolute minimum I am allowed to keep?

For consumer debt, federal law protects 30 times the federal minimum wage per week (currently $217.50). If your disposable earnings are at or below this floor, your wages cannot be garnished at all.

🛑 How fast can I stop a wrong calculation?

If the math is legally incorrect, an attorney can file an emergency motion with the court to correct the order. If the math is correct but you need it stopped, filing for bankruptcy triggers an automatic stay immediately.

Garnishment sits at the end of a process that starts earlier. These cover the full picture.

- How courts allow collectors to reach your paycheck and your bank

- Types of Wage Garnishment: Why the Debt Type Changes Everything About Your Options

- Can Your Employer Fire You for Wage Garnishment? The One-Debt Rule

- Can Social Security Be Garnished? What's Protected, and the Bank Account Trap That Isn't

- Federal Student Loan Wage Garnishment: How Administrative Garnishment Works and Why 2025-2026 Changes Everything

Garnishment is a symptom. These cover the options that address what caused it.

- The collector behavior that typically comes before the garnishment order

- How the lawsuit you may have missed is what created the garnishment

- How wage garnishment works and the options available to stop or limit it

- When a collector goes after your bank account instead of your wages

- How settling the underlying debt stops the garnishment permanently

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.