- Wage garnishment is not a single event; it is a rigid legal process that starts long before the money leaves your paycheck.

- For consumer debts, a collector must win a lawsuit first. For government debts, they bypass the courts entirely.

- Your employer receives the legal order before you do. They have no legal choice but to comply and cannot evaluate whether the debt is fair or valid.

- The amount taken is based on “disposable earnings,” which excludes taxes but does not exclude voluntary deductions like health insurance or 401k contributions.

- Filing a claim of exemption or negotiating directly are the primary ways to interrupt the cycle once it begins.

The Silent Paperwork That Targets Your Paycheck

When people realize their wages are about to be garnished, the reaction is almost always a mix of panic and confusion. The most common question I hear is: “How did they just reach into my paycheck without asking me?”

The truth is, they did not just reach in. A long, methodical legal process took place behind the scenes. In my twelve years working inside the debt collection industry, I watched this process execute thousands of times. I have trained collectors on how to locate employment information, and I know exactly how the paperwork flows from a creditor’s desk to your employer’s payroll department.

Most consumers believe they will get a phone call asking for permission, or at least a final warning before the deductions start. That is not how wage garnishment works. Once the legal machinery is turned on, it runs largely without your involvement. The collector does not ask your employer to withhold the money; they serve a legal order that forces them to do it.

Understanding the exact mechanics of this process is not just about satisfying your curiosity. It is about survival. If you know how the order is created, how your employer calculates the deduction, and when the money actually moves, you can identify the specific points where you still have leverage to fight back.

Step 1: The Legal Green Light (The Order is Created)

A debt collector cannot simply wake up one morning and decide to garnish your wages. They need legal authority. How they get that authority depends entirely on the type of debt you owe.

This is the most critical dividing line in the entire collection industry. For private consumer debts such as credit cards, medical bills, personal loans, or auto deficiencies, the creditor must take you to court. They have to file a lawsuit, serve you with a summons, and win a judgment against you. Only after a judge signs that judgment can the creditor request a writ of garnishment.

If you have a consumer debt being garnished, it means you were sued, and you lost. In many cases, consumers lose by default because they never responded to the lawsuit paperwork.

Government debts operate in a completely different reality. Agencies collecting federal student loans, back taxes (IRS), and child support do not need to sue you. They possess administrative authority. They can issue a garnishment order directly, bypassing the court system entirely. This distinction changes your timeline, your rights, and your options. Understanding which category of wage garnishment you are facing is the first step in formulating a response.

💡 Action Step: If a consumer debt is being garnished but you never received a lawsuit summons, your first move is to pull your court records. A default judgment based on improper service can often be challenged and vacated.

Step 2: Finding and Serving Your Employer

Once the creditor has the court order or administrative authority, they must deliver it to your employer. This step often feels like a violation of privacy to the consumer, but to a collector, it is just data processing.

Collectors use sophisticated skip-tracing databases like The Work Number, LexisNexis, and credit bureau employment history to locate your current job. Sometimes, they simply call the front desk of a suspected employer and ask to verify employment. Once they confirm where you work, they serve the writ of garnishment.

“On the collection floor, locating a verified employer was the ultimate prize. Once we found out where someone worked, we stopped trying to negotiate over the phone. We just fed the employer’s address into the legal pipeline and let the court order do the heavy lifting.”

This document is sent to your employer’s registered agent, HR department, or payroll processor. It is an official legal mandate. It commands the employer to begin withholding a specific portion of your earnings to satisfy the debt.

Your employer has no choice but to accept this document. They cannot reject it because they think you are a good employee. They cannot reject it because they know you are struggling financially. Failure to comply with a valid garnishment order can make the employer legally liable for your entire debt. Consequently, payroll departments process these orders with absolute, mechanical efficiency.

Step 3: You Receive the Notice

This is the part of the process that causes the most frustration. In many states, the first time you realize your wages are being garnished is when you open your pay stub and see a massive deduction.

Federal and state laws dictate how and when you must be notified. However, the sequence of events is counter-intuitive. The creditor serves your employer first. Your employer is then required to provide you with a copy of the garnishment order and a notice of your rights.

Because payroll cycles move quickly, your employer may receive the order on a Tuesday, process it into the payroll system on Wednesday, and hand you the notice on Thursday on the exact same day your paycheck is reduced. You are deliberately the last person in the chain to know, preventing you from quitting or hiding assets before the trap snaps shut.

When you do receive this paperwork, it triggers a tight legal countdown. You typically have a brief 20-day window to review the details of the garnishment notice and file a formal claim if you qualify for an exemption. Ignoring this document means accepting the maximum deduction by default.

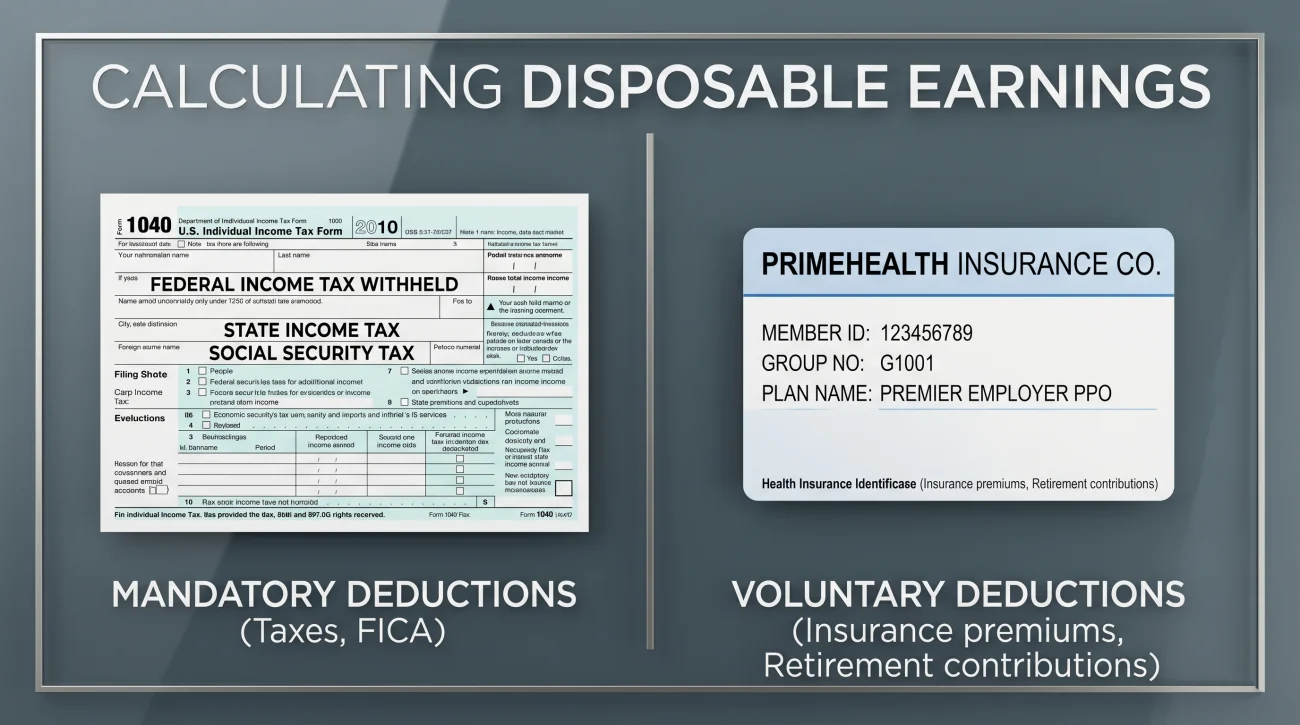

Step 4: The Calculation (Disposable Earnings)

Once your employer has the order, their payroll software must calculate exactly how much money to extract from your check. They do not just take 25% of your gross salary, nor do they take 25% of your final take-home pay. They use a specific legal formula based on your “disposable earnings.”

This definition trips up almost everyone outside of the legal and payroll professions.

Disposable earnings are your gross pay minus only legally required deductions. What counts as legally required?

- 📌 Federal income tax

- 📌 State and local taxes

- 📌 Social Security (FICA)

- 📌 Medicare

- 📌 State unemployment insurance

Here is where the math hurts. Voluntary deductions do not reduce your disposable earnings. If you pay for health insurance premiums, contribute to a 401(k), pay union dues, or have life insurance deducted from your check, the creditor gets to calculate their percentage before those voluntary items are paid.

“I bring home $600 a week after taxes, health insurance, and my 401k. The collector can only take 25% of that $600.”

“Your gross pay is $1000. Minus taxes ($200), your legal disposable earnings are $800. The collector takes 25% of $800 ($200). Your health insurance and 401k are then deducted from whatever is left. Your actual take-home pay will plummet.”

I regularly saw accounts where the debtor’s payroll department messed up the disposable earnings math. They would just take 25% of the gross check, completely ignoring the formula. The creditor will never complain about receiving too much money. It is entirely on you to catch this.

For consumer debts, the federal limit is generally 25% of these disposable earnings, or the amount by which your weekly disposable earnings exceed 30 times the federal minimum wage, whichever is lower. Knowing exactly how the garnishment calculation limits work is vital, because payroll software occasionally makes errors, and you are the only one who will suffer for it.

Step 5: Deduction and Remittance

With the calculation complete, the money is physically withheld from your paycheck. But it does not go immediately into the collector’s pocket. Bi-weekly, semi-monthly, or weekly, whenever you get paid, the calculation runs, the money is separated, and the check is sent out.

Your employer holds the funds in their accounting system and then remits them according to the instructions on the writ. Usually, the money is sent to the local court that issued the judgment or mailed directly to the law firm representing the creditor.

The Remittance Lag: There is almost always a delay between the day the money leaves your paycheck and the day it is credited to your actual debt balance. Your employer might remit funds in a batch once a month, and the attorney’s office takes time to process the check. Do not panic if your balance does not drop immediately, but you should request a written payment history from the creditor every 90 days to ensure every garnished dollar is being applied correctly.

When Multiple Garnishments Collide: What happens if you have two creditors trying to garnish you at the same time? Priority rules take over. Child support and IRS tax levies always win. If you already have an active child support order taking 50% of your check, a consumer debt collector gets nothing, even with a valid judgment. They just have to wait in line. If two consumer creditors have judgments, the first one to serve the employer gets paid first while the second order is queued.

📌 Note: Do not assume that your debt balance is going down perfectly dollar-for-dollar. In many states, post-judgment interest continues to accrue on your balance even while you are being garnished. A $5,000 judgment can take much longer to pay off than you think if 9% interest is constantly being added to the principal.

Step 6: How the Process Finally Stops

A wage garnishment order does not have a natural expiration date in most jurisdictions. It is an open-ended directive that remains active until one of specific events occurs.

First, the debt is paid in full. Once the principal, interest, and court costs are satisfied, the creditor must file a satisfaction of judgment with the court and send a release to your employer.

Second, you successfully file a Claim of Exemption. If you prove to the court that you are the head of household (in certain states), or that the garnishment prevents you from buying food and paying rent, the judge can order the garnishment reduced or stopped.

Third, you negotiate a settlement. A creditor may agree to release the garnishment if you can provide a lump-sum payment or enter into a voluntary payment plan that they prefer over the slow drip of payroll deductions.

Fourth, you successfully vacate the judgment. If you can prove you were never properly served with the original lawsuit, the court can throw out the judgment, which instantly kills the garnishment order.

Fifth, you file for bankruptcy. The moment a Chapter 7 or Chapter 13 bankruptcy petition is filed, an “automatic stay” goes into effect. This is a federal injunction that forces all collection activity, including wage garnishments, to halt immediately.

The system is designed to run indefinitely. The deductions will not stop on their own, which means you must evaluate your situation and choose which strategy to stop the garnishment is actually viable for you.

The Employer’s Perspective: HR is Not Your Lawyer

This is a reality check that many consumers struggle to accept: your employer is a bystander in this fight.

When an employee sees a garnishment hit their check, their first instinct is often to storm into the human resources office and demand that the deduction be stopped. They will explain that the debt is too old, that the collector is lying, or that they were never sued.

HR cannot help you. They cannot evaluate the validity of the debt. If they receive an order that looks legally valid on its face, they must comply. Asking your payroll manager to ignore a court order is asking them to break the law and put the company’s money at risk.

💡 Pro Tip: Keep your communications with HR strictly professional and procedural. Ask them for a complete copy of the garnishment order and the exact formula they used to calculate your disposable earnings. That is data you can use. Venting about the unfairness of the debt achieves nothing.

If you need to request the paperwork from your employer, keep it brief and documented.

Subject: Request for garnishment documentation

Hello [HR Contact Name],

I noticed a garnishment deduction on my recent pay stub. Could you please provide me with a full copy of the garnishment order, the writ, and any instructions or worksheets used to calculate the disposable earnings and deduction amount?

I need these documents to review with legal counsel. Thank you for your help.

Best regards,

[Your Name]

There is one piece of good news regarding your employer. Under the federal Consumer Credit Protection Act (CCPA), an employer cannot fire you simply because your wages have been garnished for a single debt. However, this protection is fragile. If a second, separate debt results in a garnishment, that federal job protection evaporates.

When the Process Breaks Down (And How to Audit It)

The garnishment system is designed for volume, not accuracy. Mistakes happen frequently. Because your employer is just following instructions and the creditor just wants money, you are the only person who will catch a procedural error.

Before you accept the deduction or call an attorney, you need to run a self-audit on your own pay stub. Do not assume the math is correct.

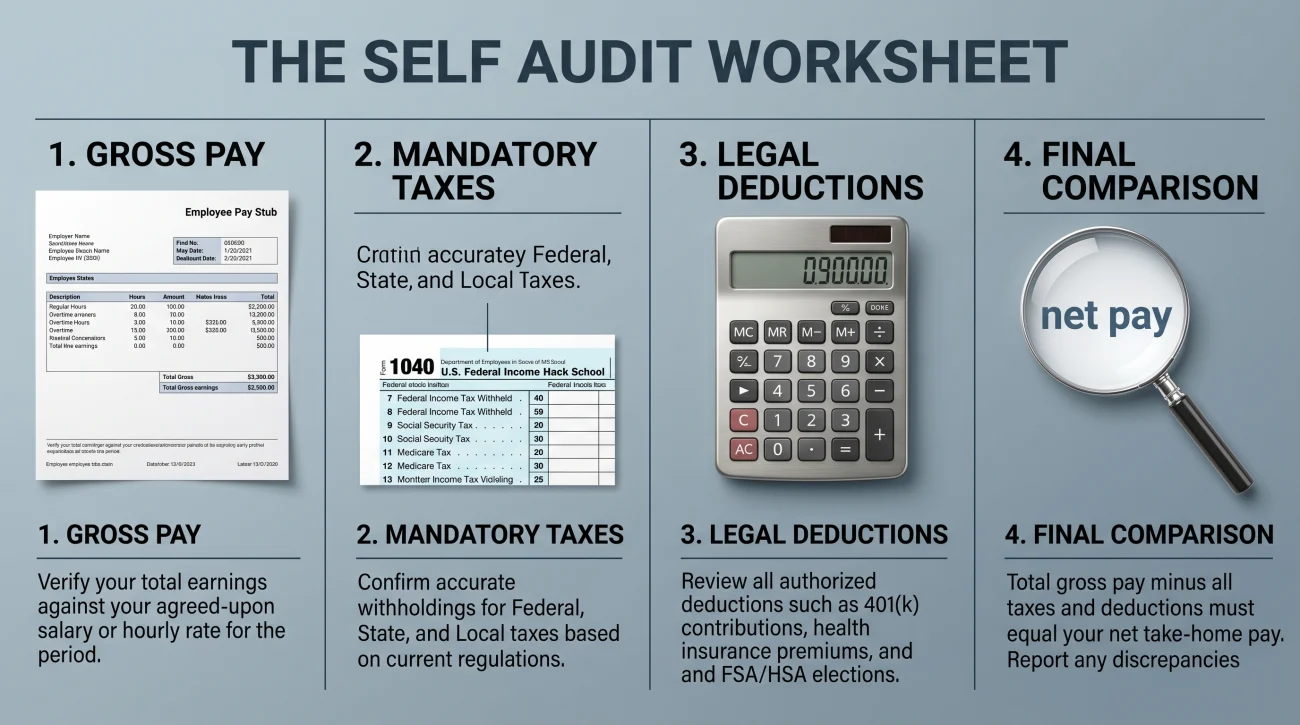

The Self-Audit Worksheet:

1. Look at your Gross Pay.

2. Subtract ONLY mandatory taxes (Federal, State, Social Security, Medicare). Do not subtract your health insurance or 401k. The resulting number is your Disposable Earnings.

3. Multiply your Disposable Earnings by 0.25 (25%). This is the maximum legal deduction for consumer debt.

4. Compare that figure to the actual garnishment line item on your pay stub.

If your deduction is higher than the number you calculated, or if you never received any official notice from the court, the machinery is broken. Do not attempt to explain legal nuances to your payroll department. When the math is wrong, or the procedure has been violated, your most effective move is having a consumer defense attorney intervene to force compliance or demand the return of improperly seized funds.

Final Thoughts: Taking Back Control

Wage garnishment is an aggressive, automated process that strips away your financial control. It works so well because the collection industry relies on the fact that most consumers do not understand the mechanics of how an order moves from the courthouse to a payroll department.

Now that you know the exact steps, you can stop reacting to the shock of the missing money and start looking for procedural weak points. Ask yourself if you qualify for a head-of-household exemption or if the original lawsuit was filed improperly. The collector expects you to just quietly adjust your life to a smaller paycheck. Documenting the process, verifying their math, and asserting your legal exemptions is how you take that control back.

❓ FAQ

⚙️ How long does it take for wage garnishment to start after a judgment?

It can happen in a matter of weeks. Once the judgment is entered, the creditor must locate your employer and file the writ. If they already know where you work, the paperwork can reach your employer’s payroll department within 14 to 30 days of the judgment being finalized.

📝 Does my employer have to tell me before they start garnishing my wages?

They are required to provide you with notice, but they do not have to wait for your permission to start. In many cases, employers process the court order immediately to remain legally compliant, meaning you might receive the notification on the exact same day your first paycheck is reduced.

💵 If I pay the debt collector directly now, will my employer immediately stop the deductions?

No. Your employer must continue withholding until they receive an official, court-issued release order. If you pay the collector directly without coordinating a formal release of the garnishment, you risk double-paying while your employer waits for the legal paperwork.

🏢 Can my employer be penalized for garnishing the wrong amount?

Generally, if an employer miscalculates and garnishes too much, the creditor is the one holding your funds illegally. You would petition the court for a return of funds. However, if an employer ignores the order entirely, the creditor can sue the employer for the full amount of your debt.

🏦 Where does the garnished money actually go?

Your employer does not keep the money. They are legally required to forward the withheld funds according to the instructions on the writ, where it is eventually credited toward your outstanding judgment balance.

📉 Do they calculate the garnishment before or after my 401k deduction?

Before. The law allows them to garnish based on your “disposable earnings,” which only excludes legally required taxes. Voluntary deductions like 401k contributions and health insurance premiums are completely ignored during the garnishment calculation.

🔄 What happens if I change jobs while my wages are being garnished?

The specific garnishment order tied to your old employer stops. However, the judgment against you remains active. The collector will eventually run a new skip-trace, find your new employer, and file a brand new writ of garnishment to start the process over again.

✉️ Can a debt collector mail a garnishment order directly to me?

A collector must serve the legal writ of garnishment to your employer. They may send you a copy of the judgment or a notice of intent depending on state law, but the actual order that forces the payroll deduction is served directly to the company you work for.

Garnishment sits at the end of a process that starts earlier. These cover the full picture.

- How courts allow collectors to reach your paycheck and your bank

- Types of Wage Garnishment: Why the Debt Type Changes Everything About Your Options

- Multiple Wage Garnishments at the Same Time: Priority Rules and What Happens to Your Paycheck

- Bankruptcy and Wage Garnishment: How the Automatic Stay Works

- How to Claim a Wage Garnishment Exemption: The Forms, Deadlines, and What Happens Next

Garnishment is a symptom. These cover the options that address what caused it.

- The collector behavior that typically comes before the garnishment order

- How the lawsuit you may have missed is what created the garnishment

- How wage garnishment works and the options available to stop or limit it

- When a collector goes after your bank account instead of your wages

- How settling the underlying debt stops the garnishment permanently

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.