- Child support wage garnishment does not require a court lawsuit or a trial to begin; an Income Withholding Order is issued automatically by state agencies.

- Federal law allows child support to take up to 65 percent of your disposable earnings, which is drastically higher than the 25 percent limit for standard consumer debts.

- Filing for bankruptcy will not stop or discharge a child support garnishment.

- If the deduction is based on an incorrect arrears calculation or an outdated income level, your only viable path is petitioning the family court for a formal modification.

The Shock of the 65 Percent Paycheck Deduction

Nothing prepares a worker for the moment they open their paystub and realize more than half of their take-home pay is gone. When someone is hit with a standard consumer debt garnishment, they lose a quarter of their disposable income. That is painful, but it is usually survivable. Child support wage garnishment operates in an entirely different universe. It is faster, it is automatic, and it can legally consume up to 65 percent of the money you earned that week.

During my years working inside third-party collection agencies, child support was the ultimate apex predator of the debt world. We would spend months tracking down a consumer, filing a lawsuit, and securing a default judgment. Then we would send our garnishment order to the employer, only to receive a notice back stating that an active child support order was already eating 50 percent of the consumer’s paycheck. When that happened, our collection efforts hit a brick wall. We got nothing until the child support was fully satisfied.

The rules for domestic support are deliberately aggressive. The government has designed this system to bypass the standard legal hurdles that slow down credit card companies and medical billers. If you are currently looking at a paycheck that has been cut in half by an Income Withholding Order, you cannot use the standard consumer defense playbook to fight it.

You need to understand exactly why you were never sued, how the staggering percentage limits are calculated, and what narrow legal avenues actually exist to lower the financial pressure on your household.

Why You Were Not Sued First

The most common confusion I hear regarding domestic support garnishment is about due process. People assume that before money can be forcibly removed from their paycheck, they must be served with a lawsuit, taken to trial, and handed a judgment by a civil court judge. That is how it works for credit cards. That is not how it works for your children.

Under a piece of federal legislation called the Personal Responsibility and Work Opportunity Reconciliation Act passed in 1996, every child support order issued or modified in the United States must include an automatic provision for wage withholding. This is known as an Income Withholding Order.

When a family court finalizes a support amount, the state child support enforcement agency automatically generates an Income Withholding Order and mails it directly to your employer. There is no separate lawsuit required to activate the garnishment. The original support order is the only legal justification the agency needs.

“Inside the agency, we fielded calls from furious consumers demanding to know why they weren’t given a chance to fight a child support garnishment in court like they did with our credit card debts. I had to explain that the family court hearing years ago was their trial. The state enforcement agency doesn’t need to sue you; they just press a button and send the federal form to your HR department.”

Because the process is administrative, it moves with terrifying speed. By the time your employer notifies you that an Income Withholding Order has arrived, they are already legally obligated to process the deduction on your very next paycheck. To truly understand how this fits into the broader landscape of paycheck seizure, it helps to review the different types of wage garnishment and how administrative power differs from standard civil judgments.

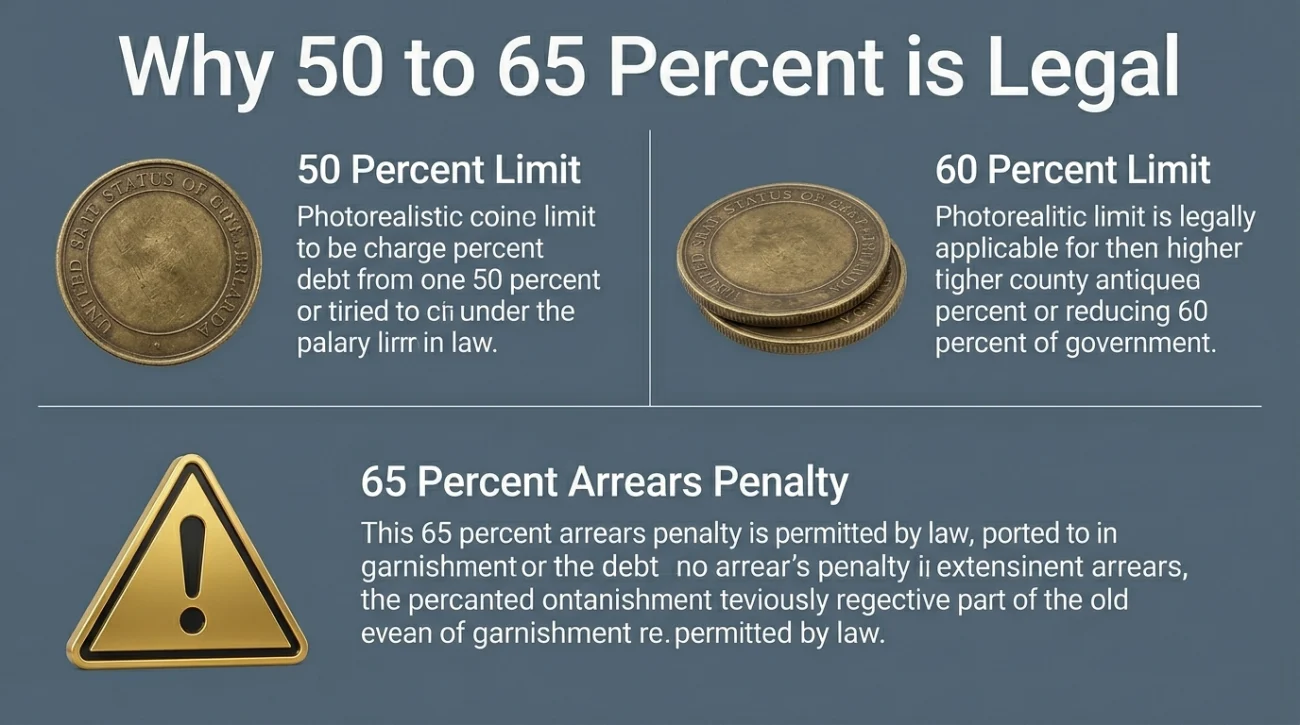

The Math: Why 50 to 65 Percent is Legal

The Consumer Credit Protection Act creates strict boundaries for how much of a worker’s paycheck can be seized. For private creditors, Title III of that act caps the extraction at 25 percent. However, lawmakers wrote specific exceptions into Title III for the support of dependents. Those exceptions allow the state to take a massive portion of your income based on three distinct tiers.

Tier One: The 50 Percent Limit

If you are currently supporting a second family, meaning you are providing living expenses for a current spouse or another dependent child who is not covered by the garnishment order in question, the federal cap is set at 50 percent of your disposable earnings.

Tier Two: The 60 Percent Limit

If you are not currently supporting another spouse or dependent child, the government assumes you have fewer immediate financial obligations. In this scenario, the limit increases. The state is legally allowed to garnish up to 60 percent of your disposable earnings.

The Arrears Penalty: An Additional 5 Percent

This is where the math becomes devastating. If you are 12 weeks or more behind on your child support payments, the law allows the enforcement agency to add an additional 5 percent penalty to the maximum limit. This means the 50 percent cap becomes 55 percent, and the 60 percent cap reaches the absolute federal maximum of 65 percent.

It is critical to understand that these percentages are calculated against your disposable earnings, not your gross pay and not your final take-home pay. Disposable earnings are your gross wages minus only legally required deductions like federal income tax, state tax, Medicare, and Social Security.

Assuming your health insurance premiums, union dues, and 401k contributions will lower the amount the state can take.

Knowing that voluntary deductions are ignored during the calculation. The 65 percent is taken from the pool of money before your health insurance is even considered, which often leaves workers with near-zero paychecks.

Priority Rules and Your Employer

If you have financial trouble, you likely have more than one debt. When multiple garnishment orders hit an employer’s desk, child support is the undisputed king of the priority ladder. It defeats credit cards, medical bills, personal loans, and even federal student loans.

If a debt collector has been taking 25 percent of your check for six months, and an Income Withholding Order for child support suddenly arrives demanding 50 percent, your employer must immediately implement the child support order. Because the total deductions cannot exceed the federal limits for the respective debts, the consumer debt collector gets bumped out. They will receive zero dollars until your child support obligation is entirely fulfilled. Dealing with overlapping orders is complex, so if you are facing this, you must understand how multiple wage garnishments and priority rules dictate your payroll.

Many workers fear that bringing an aggressive 60 percent garnishment to their employer will result in immediate termination. Federal law strictly prohibits your employer from firing you because your wages are being garnished for any single indebtedness, and child support falls under this protection.

Furthermore, because child support collection is a high priority for the government, many states back up federal protections with their own severe civil penalties for employers who retaliate. If your employer takes disciplinary action against you specifically because of an Income Withholding Order, they are likely violating both federal and state regulations. For a broader look at job security, review the federal guidelines on whether an employer can fire you for wage garnishment.

The Dead Ends: What Will Not Work

When consumers are desperate to protect their paycheck, they often waste time on strategies that work for standard debt but fail completely against family court orders.

First, bankruptcy is not an escape hatch. While filing for Chapter 7 or Chapter 13 triggers an automatic stay that immediately halts credit card lawsuits and standard garnishments, federal bankruptcy law specifically excludes domestic support obligations from that protection. The family court order survives the bankruptcy filing, and your employer will continue to deduct the money uninterrupted.

Second, your HR department cannot help you. Your payroll manager cannot negotiate the percentage down because they feel bad for your situation. If the Income Withholding Order dictates 60 percent, and your employer only takes 30 percent, the employer becomes legally liable for the difference. They will not risk their corporate compliance for you.

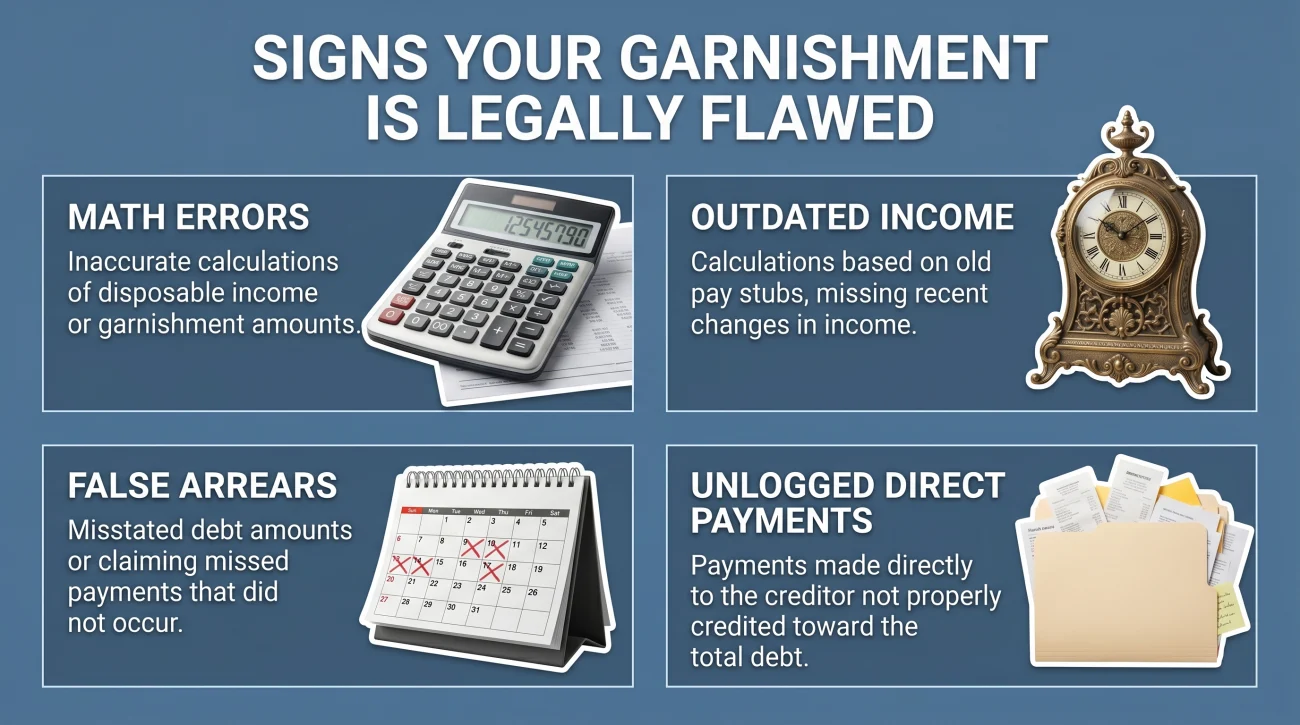

Signs Your Garnishment is Legally Flawed

While the laws heavily favor the enforcement agency, mistakes in the system are incredibly common. Automated accounting systems fail to register manual payments, and state agencies often operate on outdated information regarding your family status. You must scrutinize the deduction immediately.

You have grounds to fight back if you are experiencing any of the following:

- The deduction exceeds 65 percent of your disposable earnings under any circumstance.

- You are currently providing financial support for a new spouse or another child, but the agency is still taking 60 or 65 percent instead of the 50 percent tier.

- The 5 percent arrears penalty is being applied, but your records show you are not 12 weeks behind on payments.

- You made informal cash payments directly to the custodial parent that the state system never accounted for, resulting in a false arrears balance.

- The original support order was based on a job you lost months ago, and your current income is drastically lower.

If you are being suffocated by a calculation error, a missed payment log, or an outdated income assumption, waiting will not fix the problem. The state will continue taking the maximum allowed until you force them to stop. When the math is wrong or your circumstances have changed severely, you need to step out of the automated system and seek professional intervention to force a legal review of your wage garnishment limits.

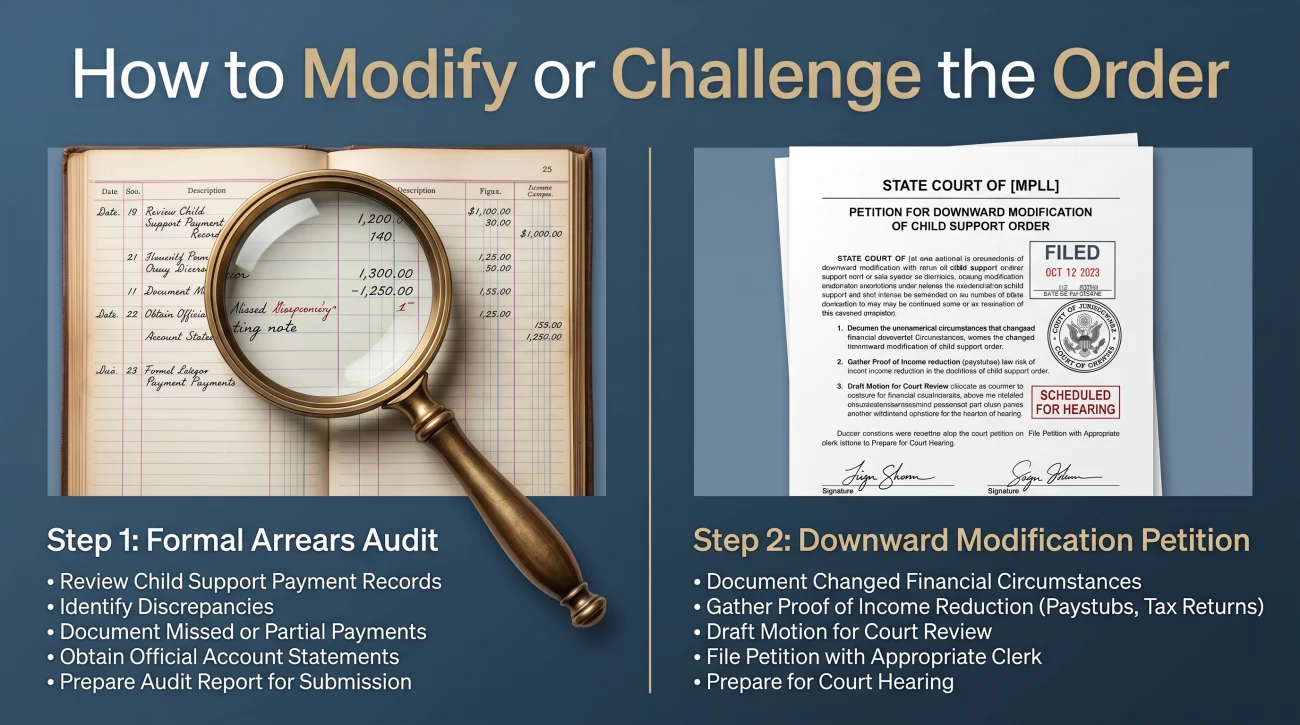

How to Actually Modify or Challenge the Order

Once you identify that your paycheck deduction is based on flawed math or outdated information, the next step is taking formal action. To reduce the crushing weight of a child support garnishment, you have to attack the root of the problem. You cannot attack the garnishment itself; you must attack the underlying support order or the accounting record.

Request a Formal Arrears Audit

If the state is taking 65 percent because their system claims you are deeply in arrears, but you know you have been making payments, you must demand a formal accounting. The informal payment trap catches thousands of parents every year. If you handed your ex-spouse cash for rent or groceries instead of routing it through the state disbursement unit, the state considers that a gift, not a child support payment. Your arrears balance grows, triggering the 5 percent penalty.

You must contact your state child support enforcement caseworker and request a full payment ledger. You have the right to contest the arrears balance in front of an administrative hearing officer.

Your request must clearly state your intention: demand an official audit, provide your proof of all informal or direct payments, and formally request the removal of the 5 percent arrears penalty.

Formal Request for Payment Audit and Ledger Review

To the Department of Child Support Services:

I am requesting a complete and formal accounting ledger for case number [Your Case Number]. My current employer is withholding wages based on an arrears calculation that I dispute.

My records indicate that the current past-due balance is incorrect, and the additional arrears penalty should not be applied to my Income Withholding Order. Please provide the official payment history on file and schedule an administrative review of my account balance so I may present my payment receipts.

Sincerely,

[Your Name]

File for a Downward Modification

If the math is correct but you simply cannot survive on the remaining 35 percent of your paycheck, your only legal path is a formal modification. You must file a petition with the family court that issued the original order, demonstrating a “substantial change in circumstances.”

A substantial change usually means an involuntary job loss, a severe medical disability, or a massive drop in your earning capacity that is outside your control. You cannot just quit your job to lower your income; the court will impute income to you based on what you are capable of earning. If you prove a legitimate, involuntary drop in income, the judge can lower your monthly support obligation, which automatically generates a new, lower Income Withholding Order for your employer.

📌 Note: A court modification is not retroactive in most states. It only lowers your payments moving forward from the date you filed the petition. The longer you wait to file for modification after losing a job, the deeper your legally binding arrears will become.

Final Thoughts on Domestic Support

Child support garnishment is meant to be highly effective and deeply disruptive to the debtor. The federal government prioritized the financial stability of the child over your ability to pay your own rent or consumer debts. The 65 percent maximum limit is brutal, and the automatic nature of the Income Withholding Order leaves no room for hesitation.

When you are facing this level of financial extraction, every day matters. You cannot passively wait for the enforcement agency to realize you are struggling. You must treat this as a legal battle, not a payroll mistake. Document your income, organize your payment history, and aggressively pursue a formal modification if your life circumstances demand it. If you are also dealing with other types of debt extraction simultaneously, make sure you understand the comprehensive strategies available to evaluate and stop different types of wage garnishment before your next payday.

❓ FAQ

💸 How much of my paycheck can be taken for child support?

Federal law allows up to 50 percent of your disposable earnings if you support another family, 60 percent if you do not, and an additional 5 percent if you are more than 12 weeks behind on payments.

⚖️ Why didn’t I get a court date before they garnished my wages?

Child support garnishment does not require a new lawsuit. Under federal law, every child support order automatically includes an Income Withholding Order that the state agency sends directly to your employer.

🛑 Will filing for bankruptcy stop my child support garnishment?

No. Domestic support obligations are completely exempt from the automatic stay in bankruptcy. Your employer will continue to deduct child support even after you file Chapter 7 or Chapter 13.

📉 Are my health insurance premiums protected from the calculation?

Usually not. The percentage limit is calculated against your disposable earnings, which subtracts mandatory taxes but ignores voluntary deductions like health insurance, 401k contributions, and union dues.

🏢 Can my boss fire me because my child support garnishment is so high?

No. Federal law prohibits an employer from firing you for any single garnishment order, and state laws explicitly protect workers from retaliation or termination based on child support withholding.

🔄 What happens if I have a credit card garnishment and a child support garnishment?

Child support takes absolute priority. If child support takes 50 percent of your disposable earnings, it leaves no room under the federal caps for the credit card garnishment, meaning the consumer debt collector gets nothing.

👨👩👧 Does having a new baby reduce my child support garnishment?

It can lower the maximum cap. If you are providing for a new spouse or dependent child, the maximum baseline the state can take drops from 60 percent to 50 percent of your disposable earnings.

📝 How do I fix an incorrect arrears balance on my garnishment?

You must contact your state child support enforcement agency immediately and request a formal payment audit. You have the right to an administrative review to prove you made payments that were not logged.

☎️ Can I just ask HR to take less money out of my check?

No. Your HR department is legally bound by the Income Withholding Order. If they take less than the order demands, the company becomes legally liable for the missing money.

🚫 Will quitting my job cancel the child support debt?

No. Quitting stops the immediate garnishment, but the debt continues to grow, arrears penalties attach, and the enforcement agency will simply send a new Income Withholding Order to your next employer.

Garnishment sits at the end of a process that starts earlier. These cover the full picture.

- How courts allow collectors to reach your paycheck and your bank

- Can Social Security Be Garnished? What's Protected, and the Bank Account Trap That Isn't

- Federal Student Loan Wage Garnishment: How Administrative Garnishment Works and Why 2025-2026 Changes Everything

- Types of Wage Garnishment: Why the Debt Type Changes Everything About Your Options

- States That Don't Allow Wage Garnishment for Consumer Debt

Garnishment is a symptom. These cover the options that address what caused it.

- The collector behavior that typically comes before the garnishment order

- How the lawsuit you may have missed is what created the garnishment

- How wage garnishment works and the options available to stop or limit it

- When a collector goes after your bank account instead of your wages

- How settling the underlying debt stops the garnishment permanently

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.