- The type of debt you owe is the single most important factor in a wage garnishment, dictating how much warning you get and what percentage of your check is taken.

- Private creditors must sue you and win a court judgment before they can touch your paycheck, but government agencies can garnish your wages administratively without ever taking you to court.

- Federal limits vary wildly depending on the debt: consumer debt is capped at 25 percent, child support can take up to 65 percent, student loans take 15 percent, and the IRS has no percentage cap at all.

The Shock of the Missing Paycheck

During my years in the debt collection industry, the most frantic calls I took were from people who had just looked at their pay stub and realized a massive chunk of their money was missing. They were almost always in a state of shock. They wanted to know how someone could legally take their earnings, and more importantly, how to make it stop immediately.

The first question I always asked them was simple, but it usually caused confusion. I asked them exactly who was taking the money. Most people assume that all wage garnishments follow the exact same set of rules. They think there is one universal law that protects a certain percentage of their income and gives them a specific set of rights to fight back.

That is not how this system works. The type of debt being collected is the single most important variable in the entire wage garnishment process. It determines whether a judge had to sign off on the order, how much of your disposable income can be legally seized, and what legitimate options you have left to protect your livelihood.

If you treat an IRS wage levy like a credit card garnishment, you are going to lose leverage and waste valuable time. Understanding the exact type of garnishment you are facing is the mandatory first step before you make a single phone call or file a single piece of paperwork.

Signs You Need to Identify Your Garnishment Type Immediately

The worst mistake you can make right now is guessing. If you have multiple old accounts in collections, you might assume the garnishment is for a medical bill when it is actually an old apartment lease deficiency. If you assume wrong, you will send your dispute or exemption claim to the wrong place, and the deductions will continue.

You need to pause and identify exactly what you are dealing with if you experience any of these symptoms:

- You are looking at a payroll deduction but have received zero paperwork explaining where it is going.

- You received an official notice, but it does not list a county court or a civil case number anywhere on the document.

- You have multiple deductions hitting your paycheck at the exact same time, and your human resources department cannot tell you which one takes legal priority.

- You know for a fact that you were never served with a lawsuit summons, yet your wages are being garnished by a private debt collector.

If you are unsure what kind of garnishment you are facing, you need professional eyes on your paperwork. Do not wait for the next pay period. Consider reaching out to a wage garnishment attorney who can review the order, identify the underlying debt, and tell you exactly what legal mechanisms are available to stop it.

If you need to ask your employer for the details, use a simple, direct written request so you have a paper trail.

Sample Request to Employer Payroll/HR

Subject: Request for copy of garnishment order

Hello [HR Contact Name],

I recently noticed a wage garnishment deduction on my pay stub. Could you please provide me with a full copy of the underlying garnishment order or writ that the company received? I need to review the court case number, the issuing agency, and the creditor information so I can address this issue directly with the source.

Thank you for your help.

[Your Name]

Once you have the actual order in your hands, you eliminate the guesswork and can determine which side of the legal divide your debt falls on.

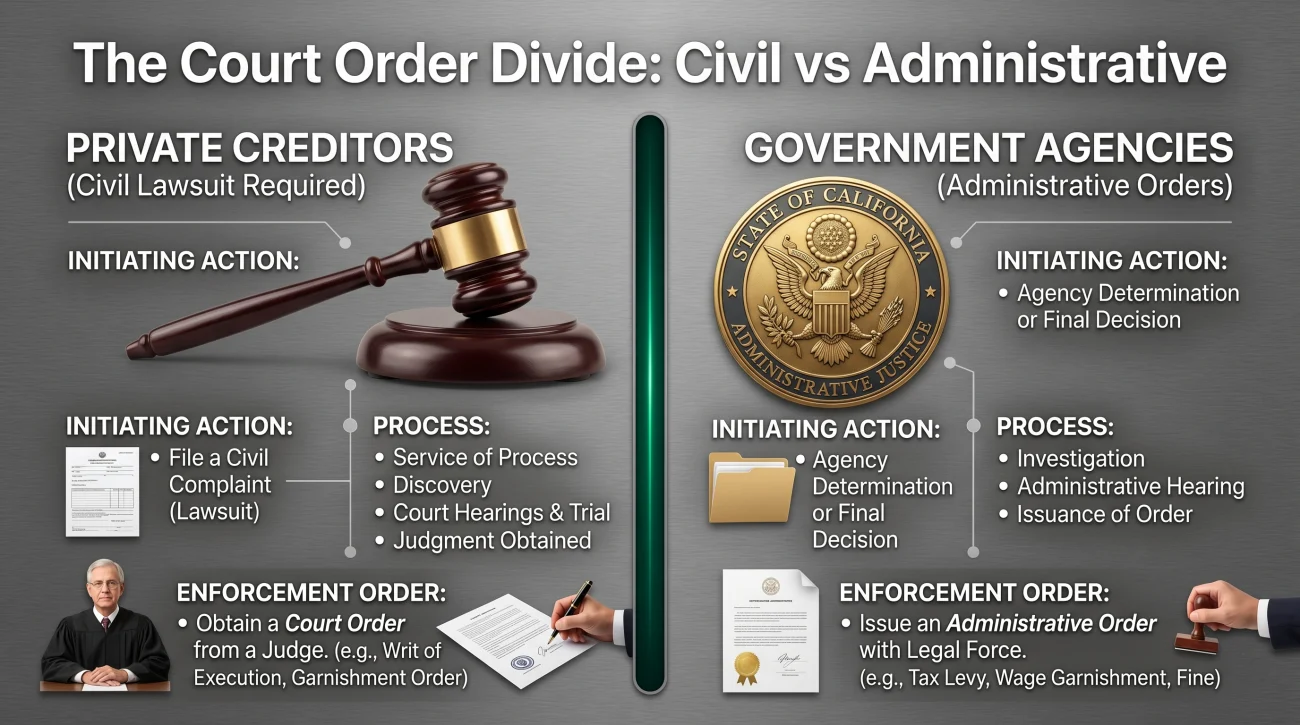

The Court Order Divide: Who Has to Sue You First?

The biggest point of confusion I saw on the collection floor revolved around the concept of a lawsuit. Consumers would call in, furiously reading from a notice they got from their human resources department, screaming that the garnishment was illegal because they were never served with lawsuit papers.

I took hundreds of calls from consumers threatening to sue us because we garnished their wages without a court date. I had to calmly explain that we were collecting for a federal agency. We did not need to sue them. The law gave us the authority to go straight to their employer. That realization is a heavy blow for a consumer to take.

This is the fundamental divide in wage garnishment. You must determine which side of this line your debt falls on.

On one side, you have private creditors. These include credit card companies, medical billing offices, personal loan lenders, and auto finance companies collecting on a deficiency balance. Under the law, these entities are completely powerless to garnish your wages on their own. They must file a formal lawsuit in civil court, serve you with a summons, and win a judgment against you. Only after a judge signs that order can they send a writ of garnishment to your employer. This means you had an opportunity to defend yourself in court before the garnishment ever started.

On the other side of the divide, you have government entities. This includes the Internal Revenue Service, the Department of Education, state tax authorities, and child support enforcement agencies. These agencies possess administrative garnishment authority. They do not need to file a lawsuit. They do not need to see you in court. After sending you the legally required warning letters, they can issue an order directly to your employer, forcing them to withhold your pay.

If you were never sued, your garnishment is almost certainly administrative. If you were sued, it is a civil judgment. Knowing this distinction maps out the specific rules your creditor must follow.

Type 1: Consumer Debt Garnishment

This is the most common type of garnishment I dealt with when working for third-party debt buyers. A consumer stops paying a credit card, the account charges off, a debt buyer purchases the account, files a lawsuit, wins by default because the consumer did not show up, and eventually files for a wage garnishment order.

Because consumer debt requires a court judgment, it is highly regulated by Title III of the Consumer Credit Protection Act. Federal law places a strict cap on how much a private creditor can take. They are limited to 25 percent of your disposable earnings, or the amount by which your weekly disposable earnings exceed 30 times the federal minimum wage, whichever is lower.

Disposable earnings are not simply your take-home pay. The legal calculation uses your gross pay minus only the legally required deductions, such as taxes and Social Security. Voluntary deductions, like your health insurance premiums or retirement contributions, are not subtracted when the 25 percent cap is calculated. For a deeper breakdown of this math, you need to understand exactly how the wage garnishment process works from the employer’s side.

⚠️ Warning: Do not assume your employer is calculating the 25 percent correctly. Payroll software sometimes mistakenly includes voluntary deductions as exempt, which results in the creditor taking more of your money than the law allows.

Certain types of income are also completely protected from consumer debt collection. If your only income is Social Security, SSDI, or VA benefits, private creditors cannot directly garnish those benefit payments. Consumer debt also faces heavy state-level restrictions. Four states completely prohibit wage garnishment for consumer debts: Texas, Pennsylvania, North Carolina, and South Carolina. If you live in one of these states and work for a local company, a credit card company cannot touch your paycheck, no matter how large the judgment is.

Type 2: Child Support and Alimony

Child support and alimony garnishments operate in a completely different legal universe. If you are dealing with this type of deduction, you are not dealing with a traditional debt collector. You are dealing with an Income Withholding Order.

Under federal law, nearly every child support order issued in the United States automatically includes an income withholding provision. There is no separate lawsuit required to activate it. When the support order is finalized, the state enforcement agency simply sends the directive to your employer.

The percentage limits here shock people who are used to the 25 percent consumer debt rule. Federal law allows child support to take up to 50 percent of your disposable earnings if you are currently supporting a second family. If you are not supporting another spouse or child, that number jumps to 60 percent. If you are more than twelve weeks behind on your payments, the agency can add an extra 5 percent, bringing the legal maximum to an astonishing 65 percent of your disposable income.

Child support also takes priority over almost everything else. If you have an active child support wage garnishment, and a credit card company sends a judgment order to your HR department, the credit card company gets nothing until the child support obligation is fully satisfied or drops below the 25 percent cap. Your employer holds the second order in a priority queue.

Type 3: Federal Student Loan Garnishment

When you default on a federal student loan, the Department of Education does not need to hire a local attorney to sue you. They utilize Administrative Wage Garnishment. This allows them, or their contracted guaranty agencies, to bypass the court system entirely.

The limit for federal student loans is capped at 15 percent of your disposable earnings. While this is lower than the consumer debt cap, it still represents a significant financial hit. The most critical element of a student loan garnishment is the timeline and the mandatory advance warning.

Before the Department of Education can issue the order to your employer, they are legally required to send you a written notice of intent to garnish at least 30 days in advance. This 30-day window is your lifeline. If you act within this window, you can stop the garnishment from ever reaching your payroll department.

Ignoring the 30-day notice of intent from the Department of Education because you cannot afford your normal monthly payment, assuming you can just explain your hardship to your HR manager later.

Using the 30-day window to apply for an Income-Driven Repayment plan or a loan rehabilitation program, which legally halts the administrative garnishment process before your employer is ever notified.

It is important to note that collections on defaulted student loans resumed recently after a long pandemic pause. Millions of borrowers who have never experienced an administrative garnishment are now receiving these notices. Understanding federal student loan wage garnishment rules is no longer a theoretical exercise. If you fall into this group, treating an administrative notice like a standard collection letter is a mistake that will guarantee a 15 percent pay cut.

Type 4: The IRS Wage Levy

The Internal Revenue Service plays by rules that no one else is allowed to use. When enforcing collection on back taxes, the agency issues a wage levy. Because this is another form of administrative collection, you will not see a courtroom. But unlike every other type of garnishment, the IRS has no set percentage cap.

The federal 25 percent limit simply does not apply to the IRS. Instead of a percentage, the IRS calculates what they are going to take based on a fixed exempt-income table found in IRS Publication 1494. This table specifies a precise dollar amount of your paycheck that is protected based on your filing status and the number of dependents you claim.

Everything above that protected amount belongs to the IRS.

If you are a single filer with no dependents making a decent salary, the exempt amount is alarmingly low. It is entirely possible for an IRS wage levy to consume 70 to 80 percent of a worker’s paycheck. The IRS will send a Final Notice of Intent to Levy, giving you a 30-day window to request a Collection Due Process hearing. Just like with student loans, missing this window means the levy activates, and you lose your primary opportunity to halt the deductions.

Comparing the Four Major Garnishment Types

To see how drastically your situation changes based on the debt type, review this operational breakdown. This is exactly how collection professionals view your account based on the paper in front of them.

| Garnishment Type | Court Order Required? | Maximum Federal Limit | Primary Way to Stop It Before It Starts |

|---|---|---|---|

| Consumer Debt (Credit cards, medical, personal loans) | Yes (Civil Judgment) | 25% of disposable earnings | Respond to the initial lawsuit summons, negotiate a settlement, or file bankruptcy. |

| Child Support & Alimony | No (Automatic IWO) | 50% to 65% of disposable earnings | File for a formal modification through the family court system. |

| Federal Student Loans | No (Administrative) | 15% of disposable earnings | Enter an Income-Driven Repayment plan or rehabilitation during the 30-day notice window. |

| IRS Wage Levy | No (Administrative) | No percentage cap (uses Publication 1494 table) | Request a hearing, set up an installment agreement, or apply for Currently Not Collectible status within 30 days. |

How the Debt Type Changes Your Options

Understanding these differences is not just an academic exercise. It directly dictates your playbook when you sit down to figure out how to stop the financial bleeding. Your strategy must align with the type of debt. A tactic that works perfectly against a credit card company will be completely ignored by the IRS.

If you are dealing with a consumer debt judgment, your options are relatively broad. Since this stems from a civil lawsuit, you can investigate whether the judgment was obtained legally. Many default judgments are entered because the consumer was never properly served with the lawsuit papers. If you can prove bad service, a judge can vacate the judgment, which instantly kills the garnishment order. You can also file a claim of exemption if you qualify under your state’s laws, or you can negotiate a lump-sum payoff directly with the collection attorney. Furthermore, filing for bankruptcy creates an automatic stay that halts consumer garnishments the moment your petition is filed.

If you are facing a child support garnishment, your options are incredibly narrow. You cannot negotiate with your employer. You cannot negotiate with a debt collector. Even filing for Chapter 7 bankruptcy does not stop a child support income withholding order. The only legitimate path to reducing the deduction is to return to the court that issued the original order and prove a substantial change in your financial circumstances to get the support amount modified.

For administrative garnishments like federal student loans and IRS levies, your power lies in the administrative procedures of those specific agencies. With student loans, combining your defaulted loans into a Direct Consolidation Loan can lift the garnishment quickly. With the IRS, proving that the levy prevents you from meeting basic living expenses can get you placed in Currently Not Collectible status, which suspends the levy entirely while your finances recover.

Key Point: Your employer is a bystander in all of these scenarios. They cannot advocate for you, and they cannot refuse a valid legal order just because you explain your hardship to them. You must deal with the source of the order, not your payroll department.

How and When Does a Garnishment End?

A common question I heard from consumers was a simple one: “How long is this going to last?” The answer, again, depends entirely on the type of debt.

For consumer debt judgments, the garnishment typically continues until the total judgment balance, plus any legally allowed post-judgment interest and court fees, is paid in full. Once the balance hits zero, the creditor must file a satisfaction of judgment with the court, which officially releases the employer from the withholding order. If you negotiate a lump-sum settlement, the release happens as soon as the settlement funds clear.

Child support income withholding orders continue until the child reaches the age of majority or graduates high school, depending on the terms of your support order. However, if you have arrears or past-due balances, the garnishment will continue until that back-owed amount is entirely satisfied, even if the child is already an adult.

Administrative garnishments stop when you resolve the underlying issue. A student loan garnishment ends when the loan is paid off, consolidated, or successfully rehabilitated through a payment program. An IRS wage levy is released when the tax debt is paid, the statute of limitations on collection expires, or you successfully negotiate an alternative resolution like an Offer in Compromise or an approved installment agreement. Knowing exactly what it takes to release these orders helps you see the finish line, but handling the immediate impact on your paycheck requires a clear strategy.

Final Thoughts on Garnishment Types

Navigating a wage garnishment is stressful because it feels like you have lost control of your own income. In my experience reviewing accounts on the collection floor, the most profitable files were always the ones where the consumer simply did not know they had the right to challenge the order. They accepted the deduction and tried to survive on whatever was left.

By identifying whether you are dealing with a civil judgment, a child support order, or an administrative levy, you take the first step toward regaining control. You shift from reacting to the missing money to actively challenging the mechanism that took it. Read the notices carefully, track the deadlines, and remember that federal and state laws provide specific pathways to relief, but only if you use the right tool for the right type of debt. To fully protect yourself, you should review the comprehensive guide on wage garnishment rules and limits so you know exactly where you stand.

❓ FAQ

🏛️ Can a credit card company garnish my wages without suing me first?

No. Private creditors, including credit card companies and medical providers, must file a lawsuit, serve you with papers, and win a court judgment before they have any legal authority to garnish your wages.

📞 Who tells my employer what kind of garnishment it is?

The entity taking the money sends a formal legal order to your employer. If it is a private debt, it will be a court-issued writ. If it is a government debt, it will be an administrative order from the specific agency.

⏰ How much warning do I get before they take my check?

It depends heavily on the debt type. The IRS and Department of Education must send 30-day advance notices. For consumer judgments, your employer may begin withholding as soon as they receive the court order, sometimes before you even get the notice in the mail.

💼 Does my employer know what the debt is for?

Yes. The garnishment order sent to your HR or payroll department will clearly list the creditor, the issuing court or agency, and the total balance owed. Your employer needs this information to know where to send the withheld funds.

💸 What happens if I have child support and a credit card garnishment at the same time?

Child support takes legal priority. If the child support order takes up your legally allowable garnishment limit (often 50 percent or more), the credit card garnishment must wait in line, receiving nothing until the support obligation is met.

🛑 Can I just tell my HR department to stop the deduction?

No. Your employer is legally mandated to comply with the garnishment order. They cannot stop the deduction based on your request or financial hardship. You must get a release from the court or the issuing agency.

📉 Why is the IRS taking so much more than 25 percent?

The federal 25 percent cap applies to consumer debts, not tax levies. The IRS uses a specific table that protects a flat dollar amount for your basic living expenses and seizes everything else, which often results in much higher deductions.

📝 Can bankruptcy stop every type of wage garnishment?

No. While the automatic stay in bankruptcy will instantly stop consumer debt garnishments and pause IRS levies, it does not stop child support or alimony income withholding orders.

🎓 Are student loan garnishments really starting again?

Yes. After a multi-year pause, the Department of Education has resumed the administrative wage garnishment process for defaulted federal student loans. Borrowers receive a 30-day notice before deductions begin.

✉️ What should I look for on the notice to figure out who is taking my money?

Look specifically for a court case number. If you see a county or circuit court listed with a case number, it is a civil judgment. If you see letterhead from a government agency and no court details, it is an administrative garnishment.

Garnishment sits at the end of a process that starts earlier. These cover the full picture.

- How courts allow collectors to reach your paycheck and your bank

- Head of Household Exemption from Wage Garnishment: Florida's Strongest Wage Protection and the Waiver Trap

- How Much of Your Wages Can Be Garnished? The 25% Rule and When It Doesn't Apply

- Multiple Wage Garnishments at the Same Time: Priority Rules and What Happens to Your Paycheck

- Received a Wage Garnishment Notice: What It Means and What You Must Do Before the Window Closes

Garnishment is a symptom. These cover the options that address what caused it.

- The collector behavior that typically comes before the garnishment order

- How the lawsuit you may have missed is what created the garnishment

- How wage garnishment works and the options available to stop or limit it

- When a collector goes after your bank account instead of your wages

- How settling the underlying debt stops the garnishment permanently

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.