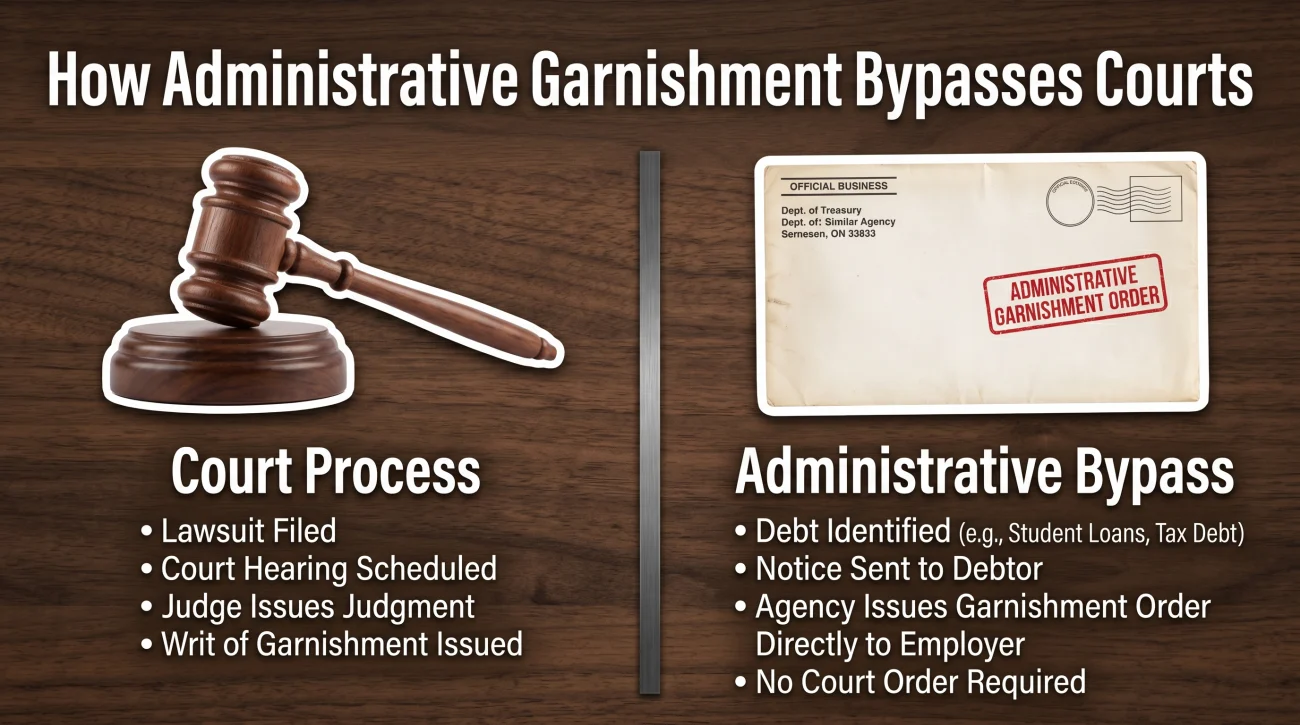

- The Department of Education does not need a court judgment to garnish your wages. They use an administrative process that bypasses the local court system entirely.

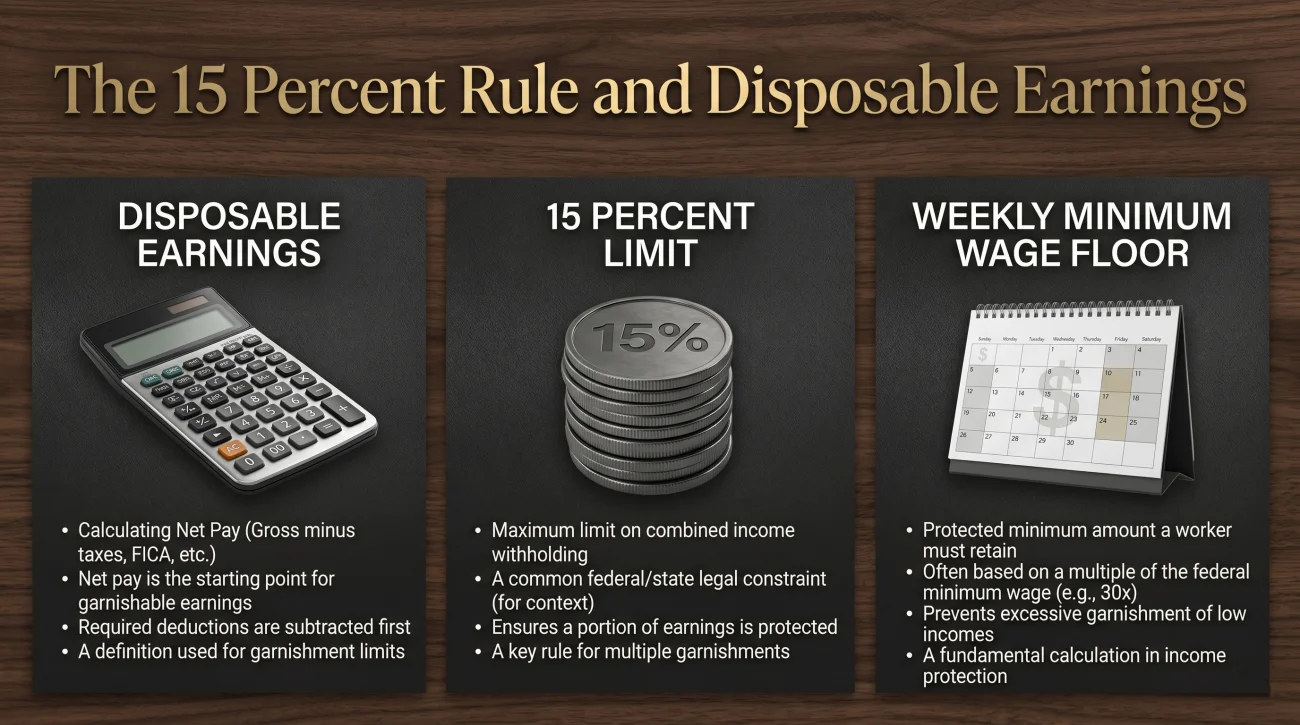

- Federal student loan garnishment is limited to 15 percent of your disposable earnings, which is lower than the standard limit for consumer debts.

- You have exactly 30 days from the date on your Notice of Intent to Garnish to establish a repayment plan or file a dispute, which halts the deduction before your employer is ever contacted.

- Collection activities on defaulted federal student loans have resumed, meaning millions of borrowers will face garnishment notices throughout 2025 and 2026.

The Shock of Administrative Wage Garnishment

Most people assume that before anyone can take money directly out of their paycheck, there has to be a lawsuit. You picture a courtroom, a judge, a summons, and an opportunity to defend yourself. For credit card debts and medical bills, that process is exactly how it works. But the federal government operates under a completely different set of rules.

Federal student loan wage garnishment is an administrative process. The Department of Education, or the guaranty agency holding your defaulted loan, does not have to sue you. They do not have to win a civil judgment. They have the statutory authority to send an order directly to your employer, legally compelling your HR department to withhold a portion of your wages. This is what catches millions of borrowers off guard.

If you have received a garnishment notice for a defaulted federal student loan, or if you know your loans have been in default during the pandemic pause, you are on a very specific timeline. The collections machine has restarted in 2025 and 2026. Understanding the mechanics of how this specific garnishment works is the only way to protect your paycheck.

How Administrative Garnishment Bypasses the Courts

When you take out a federal student loan, you agree to specific terms governed by the Higher Education Act. One of those terms grants the government extraordinary collection powers if you default. Default typically occurs after 270 days of missed payments on a federal direct loan.

Once you hit that default status, the loan can be transferred to a collection agency working on behalf of the government. Unlike a private debt collector who must file a lawsuit in your local county court to secure a judgment, the federal government uses Administrative Wage Garnishment. They bypass the judicial system entirely.

“During my years in the collection industry, we knew that government-backed debt carried the ultimate leverage. A private collector working a medical bill has to grind through the court system for months, hoping for a default judgment. The Department of Education simply mails a packet to the employer’s payroll department.”

The first time the consumer realizes it is happening is often when they look at their pay stub. This structural difference is why it is vital to know exactly what type of wage garnishment you are dealing with. If you wait for a court summons that is never coming, you will miss your chance to stop the deductions.

The 2025 and 2026 Restart Timeline

For several years, borrowers in default experienced a massive reprieve. The pandemic-era payment pause halted wage garnishments, tax refund offsets, and Social Security offsets. Furthermore, the government introduced the Fresh Start program, designed to pull millions of borrowers out of default and back into good standing.

However, that protective era has ended. Collections on defaulted federal student loans officially resumed in May 2025. The Department of Education began preparing and sending the first wave of garnishment notices to employers in late 2025 and early 2026. While there was a brief administrative pause in January 2026 due to ongoing repayment reforms and legal challenges regarding income-driven plans, the administrative collection process is fully active.

There are roughly 5.3 million borrowers currently in default. A significant portion of these borrowers defaulted after 2020 and have never experienced the reality of Administrative Wage Garnishment. If your loans remained in default after the Fresh Start deadline passed, your account is eligible for aggressive collection measures.

The 15 Percent Rule and Your Disposable Earnings

The amount the government can take for a federal student loan is strict, but it is actually lower than the maximum allowed for private consumer debts. Under federal law, the Department of Education can garnish 15 percent of your disposable pay.

The calculation is based on your disposable earnings. This term creates massive confusion because it does not mean your final take-home pay. Disposable earnings are defined as your gross pay minus legally required deductions. Legally required deductions include federal taxes, state taxes, local taxes, Social Security, and Medicare.

⚠️ Warning: Voluntary deductions do not protect your income. Your health insurance premiums, 401k contributions, union dues, and life insurance deductions are not subtracted when calculating your disposable earnings. The 15 percent is calculated on the amount before those voluntary deductions are taken out.

There is a floor designed to protect extremely low-income earners. The government cannot garnish any amount if your disposable pay is less than 30 times the federal minimum wage per week. Currently, the federal minimum wage is $7.25 per hour, making that floor $217.50 per week. If your disposable income is below $217.50 weekly, your student loan garnishment should be zero.

If you have multiple debts, the priority rules matter. If you already have a child support withholding order, or if you are facing an aggressive IRS wage levy, the total amount taken from your check across all garnishments typically cannot exceed 25 percent of your disposable earnings, though child support has higher limits.

The Notice of Intent to Garnish: Your First Warning

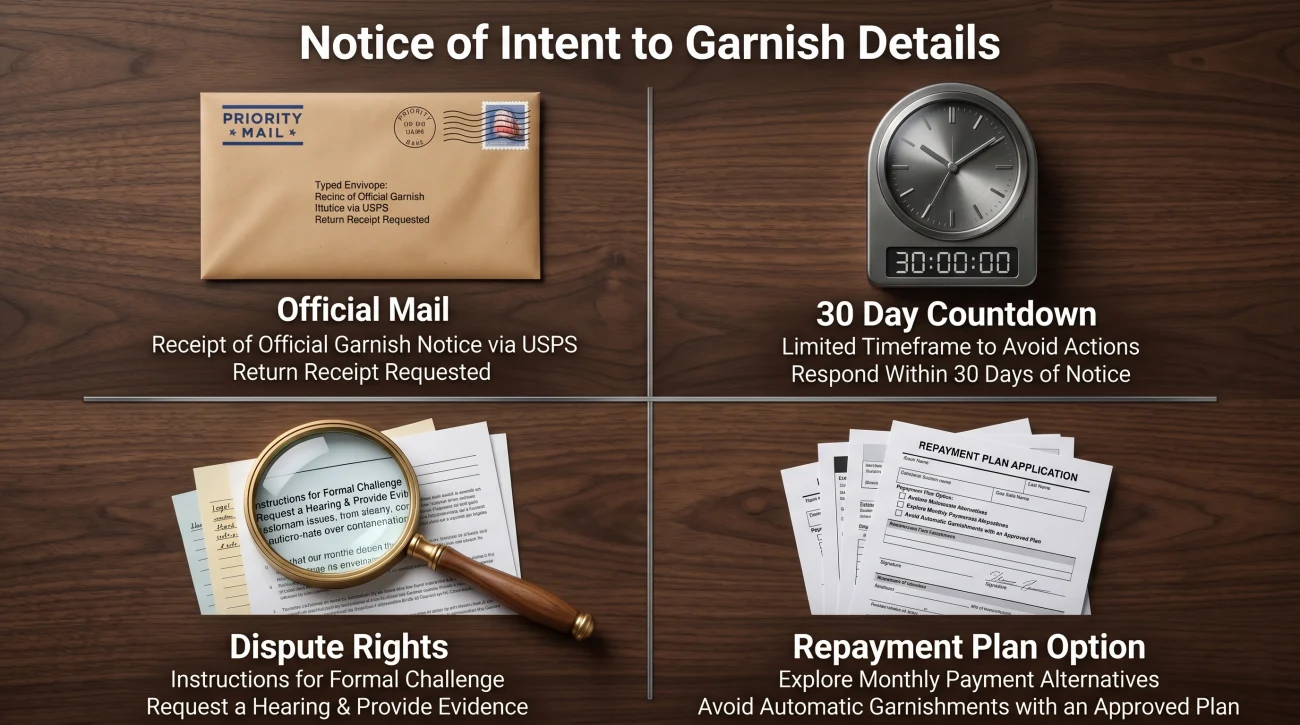

This is the single most important concept regarding student loan collection. Before the government can order your employer to withhold wages, they must send you a written warning. This document is typically titled a Notice of Intent to Garnish.

The date printed on this letter starts a strict 30-day countdown. This is your primary action opportunity. If you secure a resolution before the clock runs out, you can stop the garnishment before your employer ever sees a document.

What the Notice Packet Contains:

1. The exact amount you owe in total, including principal, interest, and fees.

2. The government’s intent to garnish 15 percent of your disposable pay.

3. Your right to inspect and copy records related to your debt.

4. Your right to request a hearing to dispute the debt or claim financial hardship.

5. Your right to enter into a written repayment agreement to avoid the garnishment entirely.

Many consumers ignore this notice. They assume it is just another standard collection letter, or they believe they cannot afford to make a payment anyway. Ignoring this letter guarantees that your employer will receive an order to deduct 15 percent of your pay.

Putting the notice in a drawer because you do not have the money to pay the balance in full. Assuming that because you are broke, they cannot take anything.

Using the notice period to proactively establish a repayment plan based on your income, which could literally set your required payment to zero dollars while protecting your paycheck from a forced 15 percent deduction.

How to Stop It Before Your Employer Is Contacted

If you are still within that initial notice period, you have highly effective options to pull your account out of the garnishment pipeline. The goal is to reach a resolution with the loan servicer or the collection agency before day 31.

Option 1: Income-Driven Repayment (IDR)

For many borrowers, the most logical step is to get the loans out of default and enroll in an Income-Driven Repayment plan. These plans calculate your monthly payment based strictly on your income and family size. If your income is low enough, your required monthly payment could be zero dollars. Even a zero dollar payment counts as an on-time payment and prevents garnishment. Do not wait for the courts to settle debates over specific plan names. Enrolling in the baseline income-driven structure currently offered by your servicer is your most reliable, immediate move to establish a compliant payment history and block the active withholding order.

Option 2: Loan Rehabilitation and Your Credit Report

Rehabilitation is a one-time opportunity to cure a default. You agree in writing to make nine affordable monthly payments over a ten-month period. Your payment amount is determined by your discretionary income. If the standard 15 percent discretionary formula is too high, you can request a calculation based on your actual monthly expenses.

The biggest advantage of rehabilitation is its impact on your credit report. Once you complete the required payments, the default status is entirely removed from your credit history. It is the only option that wipes the default slate clean.

I have seen many borrowers panic because they sign a rehabilitation agreement but still see a deduction on their next check. The reality is that there is a lag. It can take one to two payroll cycles for the official release order to reach your employer and for HR to process it. You must communicate this gap to your household budget.

Option 3: Loan Consolidation

Consolidation allows you to pay off your defaulted federal loans by taking out a new Direct Consolidation Loan. To consolidate a defaulted loan, you must agree to repay the new loan under an Income-Driven Repayment plan. Once the new loan is originated, the default is cleared, and the threat of garnishment ends.

Consolidation is much faster than the nine-month rehabilitation process. However, it does not remove the record of the default from your credit report. The new loan will show as current, but the old default damage remains visible to future lenders for up to seven years.

Changing Jobs Will Not Erase the Order

A common question I used to hear was whether quitting a job and moving to a new employer would cancel the garnishment. The short answer is no, but it does buy a very small amount of time.

The garnishment order is attached to your Social Security number, not just your current job title. When you start a new position, your new employer will eventually report your hiring to the state directory of new hires. The Department of Education actively cross-references this database. Once their automated system spots your new employer, a fresh direct withholding order is mailed out.

⚠️ Warning: Relying on job-hopping to avoid collection usually backfires. You end up with unexpected deductions at your new job just as you are trying to establish yourself, and the underlying loan balance continues to grow rapidly with added interest and collection costs.

Gig Workers and 1099 Contractors: A Different Rulebook

The standard 15 percent wage limit applies specifically to W-2 employees. If you are an independent contractor, a freelancer, or a gig worker, you do not receive a traditional paycheck with “disposable earnings.”

However, the government can still intercept your income. Instead of a standard wage garnishment, they can issue a levy directly to the companies that pay you. In my operational experience, tracking down 1099 income was a frustrating challenge for private collectors, but the federal government has far better visibility into tax records and 1099 filings. If they issue a levy to a client or a gig platform you work for, that company may be legally required to turn over 100 percent of the owed compensation, not just 15 percent, because it is classified as a business receivable rather than protected W-2 wages.

Requesting a Hearing for Hardship or Dispute

If you believe the debt is not yours, the balance is entirely wrong, or that losing 15 percent of your pay would cause extreme financial hardship, you can request a hearing. The instructions for requesting a hearing are included in the Notice of Intent to Garnish.

If you submit your hearing request in writing before the expiration date on your notice, the government cannot garnish your wages until the hearing process is completed and a decision is issued. This effectively pauses the collection action.

To win a hardship claim, you must provide detailed documentation of your finances. You will need to submit an income and expense form proving that taking 15 percent of your disposable pay would prevent you from meeting basic survival needs like housing, food, and essential medical care. When I watched these claims get denied, it was almost always because the borrower listed credit card payments, cable bills, or private school tuition as essential expenses. The hearing official will only protect absolute survival necessities.

What Happens If Your Request Is Denied?

If the hearing official rejects your hardship claim, the withholding order moves forward to your HR department. But a denial is not the end of the road. Even if the garnishment begins, you still retain the right to enter a loan rehabilitation program or consolidate the loan. Entering those programs will eventually stop the active garnishment, though you will have to endure the paycheck deductions during the setup period. If the hearing does not go your way, the withholding order lands squarely on your employer’s desk, bringing up the next major concern: your job security.

Your Job Security and Employer Obligations

A common fear is that an employer will simply fire an employee rather than deal with the administrative headache of processing a federal wage garnishment. Federal law provides specific protections regarding this exact scenario.

In my experience reviewing accounts, a garnishment order inside an HR or payroll office is treated as just another piece of mandatory compliance paperwork. They do not judge the debt, and they do not get advanced warning before you do. When the packet arrives from the government, their only legal option is to run the calculation and start withholding.

Under Title III of the Consumer Credit Protection Act, an employer is strictly prohibited from firing you, demoting you, or taking any disciplinary action against you because your wages are being garnished for any one single debt. A student loan administrative garnishment counts as one debt.

However, that protection has limits. If you have multiple garnishments for different debts, that federal protection disappears. You can learn more about how the one-debt rule functions by reviewing the rules on whether an employer can fire you for wage garnishment.

The Social Security Offset Risk

Wage garnishment targets active employment income. But the federal government also has the authority to target retirement income through a separate process called the Treasury Offset Program. If you are receiving Social Security retirement or disability benefits, the government can withhold a portion of your monthly check to pay defaulted student loans.

They can take up to 15 percent of your total benefit, provided that the offset does not leave you with less than $750 per month. Supplemental Security Income is exempt from this offset. While there have been temporary pauses on Social Security offsets for student loans, the statutory authority remains intact. Understanding how different income streams are treated is vital, especially when looking at Social Security wage garnishment rules.

Whether you are trying to protect your paycheck or your retirement benefits, identifying your exact position in the collection timeline is the next crucial step.

Signs You Still Have Time to Protect Your Paycheck

When you are dealing with federal administrative collections, the timeline is everything. Identifying exactly where you are in the process determines which options remain viable. If you recognize any of these scenarios, you need to act immediately.

- You received a Notice of Intent to Garnish recently and the response deadline has not yet passed.

- You have not received a notice, but your credit report shows a federal student loan in active default status.

- You are currently earning wages, but your income is low enough that an income-driven repayment plan would likely set your payment near zero.

- You received a notice, but you know the loan was already discharged through a closed school discharge or total and permanent disability.

If you are confused by the documentation, or if your employer has just notified you that a deduction is starting next week, you need to evaluate your legal and financial standing immediately. If you cannot decipher the notice or need help challenging an active order, consulting with a wage garnishment attorney can provide clarity on your specific defense options. For a broader view on how to halt the process across different debt types, review the complete guide on how to stop wage garnishment.

Final Thoughts on Administrative Collections

The hardest part of dealing with a federal student loan default is the feeling that a faceless bureaucracy is reaching directly into your livelihood. Because they operate outside the local court system, the process feels both invisible and inevitable.

But the reality I learned from the inside is that the government’s collection system is rigid, heavily reliant on automated timelines, and bound by strict procedural rules. That rigidity is actually your advantage. If you engage with their notices, properly format a hardship request, or initiate a structured repayment plan before the deadlines expire, you force their system to pause. The worst outcome always happens when a borrower assumes they have no power and simply ignores the letters. Engaging early is the absolute best way to protect your paycheck.

❓ FAQ

⏰ When exactly is student loan garnishment restarting in 2026?

After a temporary pause in early 2026, the Department of Education is expected to resume sending garnishment notices in the summer of 2026. The exact date you receive a notice depends on when your specific loan account is processed by the collection agency.

📞 Will a collector call me before they take my paycheck?

They might call, but a phone call is not legally required. The only legal requirement before administrative garnishment begins is that they mail a written Notice of Intent to Garnish to your last known address at least 30 days prior.

📉 Can they take more than 15 percent if I make a lot of money?

No. For federal student loans, the administrative wage garnishment cap is strictly set at 15 percent of your disposable earnings, regardless of how high your income is.

🛑 How do I stop the deduction once my employer has already started it?

Once deductions begin, you can stop them by paying the debt in full, entering into a loan rehabilitation agreement, or successfully proving extreme financial hardship through a formal hearing request.

🏦 Can the government freeze my bank account for student loans?

The Department of Education typically relies on wage garnishment and tax offsets. To freeze your personal bank account, they generally must escalate the matter to the Department of Justice, which would then file a lawsuit in federal court to obtain a judgment.

🏢 Does my HR department have to warn me before they deduct the money?

Federal law requires employers to notify you when they receive a garnishment order. However, because the employer must comply with the order immediately upon receiving it, this wage garnishment notice from your job often arrives at the exact same time your pay is reduced.

📝 Does asking for a hearing automatically pause the garnishment?

If you submit a written request for a hearing within the mandatory deadline stated on the Notice of Intent to Garnish, the garnishment cannot begin until a decision is made. If you request it after the deadline, the garnishment usually proceeds while you wait for the outcome.

💼 Can my boss fire me because of this garnishment?

Under federal law, your employer cannot fire you for a single wage garnishment order. If this is the only garnishment on your record, your job is protected from termination based solely on the garnishment.

💸 Will filing for bankruptcy stop a student loan garnishment?

Filing for bankruptcy triggers an automatic stay that pauses the student loan wage garnishment while the bankruptcy is active. However, student loans are rarely discharged in the process, meaning the debt will likely survive, and bankruptcy is a severe financial decision that carries long-term credit consequences.

👵 Can they take my Social Security retirement check instead?

Yes. The government uses the Treasury Offset Program to take up to 15 percent of Social Security retirement or disability benefits for defaulted student loans, though they must leave you with at least $750 per month.

Garnishment sits at the end of a process that starts earlier. These cover the full picture.

- How courts allow collectors to reach your paycheck and your bank

- Types of Wage Garnishment: Why the Debt Type Changes Everything About Your Options

- IRS Wage Levy: Why It's Different and How the IRS Can Take Almost Everything

- How to Claim a Wage Garnishment Exemption: The Forms, Deadlines, and What Happens Next

- Head of Household Exemption from Wage Garnishment: Florida's Strongest Wage Protection and the Waiver Trap

Garnishment is a symptom. These cover the options that address what caused it.

- The collector behavior that typically comes before the garnishment order

- How the lawsuit you may have missed is what created the garnishment

- How wage garnishment works and the options available to stop or limit it

- When a collector goes after your bank account instead of your wages

- How settling the underlying debt stops the garnishment permanently

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.