- Federal law prohibits legitimate debt relief organizations from charging fees before they actually secure a settlement.

- Your monthly deposits must go into a dedicated, FDIC-insured account that you control entirely.

- Industry accreditation from the ACDR or IAPDA is a non-negotiable filter when evaluating your options.

- Choosing between major firms like National Debt Relief or Freedom Debt Relief should depend on your specific financial situation and your state of residence.

- A company that guarantees a specific debt reduction percentage or tells you to ignore lawsuit summonses is exhibiting major red flags.

Navigating the Noise in the Debt Relief Industry

Figuring out how to choose a debt settlement company can feel like walking through a minefield. When you are overwhelmed by financial stress, the last thing you want is to hand over your recovery to an organization that might leave you in a worse position. I spent twelve years inside third-party collection agencies and a national debt buying firm. From that vantage point, I knew exactly which settlement operations actually negotiated effectively on behalf of their clients, and which ones were fly-by-night setups just collecting processing fees.

There is an overwhelming amount of marketing in this industry. However, the difference between a legitimate partner and a predatory scam usually comes down to transparency regarding your money and honest expectations about the damage to your credit score.

Making the right choice requires understanding how these programs operate mechanically, what the fee structures actually look like under federal law, and what red flags to watch for in the fine print. In this guide, I will walk you through exactly what to look for, how to evaluate the major players in the space based on your specific debt profile, and the questions you must ask before signing any contract.

The Reality of the First 90 Days

Before you can evaluate a firm, you need to understand the mechanics of the service they provide. A debt settlement program is a structured negotiation process designed for consumers who can no longer afford their minimum monthly payments. It requires you to stop paying your enrolled creditors directly and instead make a single monthly deposit into an independent funding account in your name.

Many companies gloss over what happens next. In my experience reviewing accounts, the first 90 days of any settlement program are the hardest part of the entire process. Because you stop paying your creditors, your accounts will go delinquent. This is an intentional, and often highly stressful, part of the strategy. Creditors are generally only willing to accept less than the full balance when they realize that getting the full amount is no longer a realistic possibility.

When I was managing a collection floor, our strategy shifted the moment an account was flagged as being represented by a vetted settlement firm. We knew a lump sum offer was eventually coming once their funding balance built up, so we would pause the aggressive daily calls. Conversely, if the consumer claimed they were with a known scam agency, we kept the pressure on, knowing the promised funds likely didn’t exist.

During these early months, collection calls will spike. A legitimate settlement firm will prepare you for this pressure cooker and explain exactly how to log the calls. A scammer will promise you that a magical cease and desist letter will stop all communication instantly, which is rarely true for original creditors who still own your account.

Once enough funds have accumulated, the company will contact your creditors to negotiate a lump-sum payoff. You must approve every single settlement before a dime is transferred. If you want a deeper look into this exact timeline, understanding how the debt settlement process unfolds is a critical next step before you commit.

The Federal Rules Guarding Your Fees

The cost of this service is the area where consumers experience the most confusion. Legitimate operations work on a contingency basis, meaning they only get paid if they succeed in settling your debt. The industry standard fee ranges from 15 to 25 percent of the enrolled debt balance.

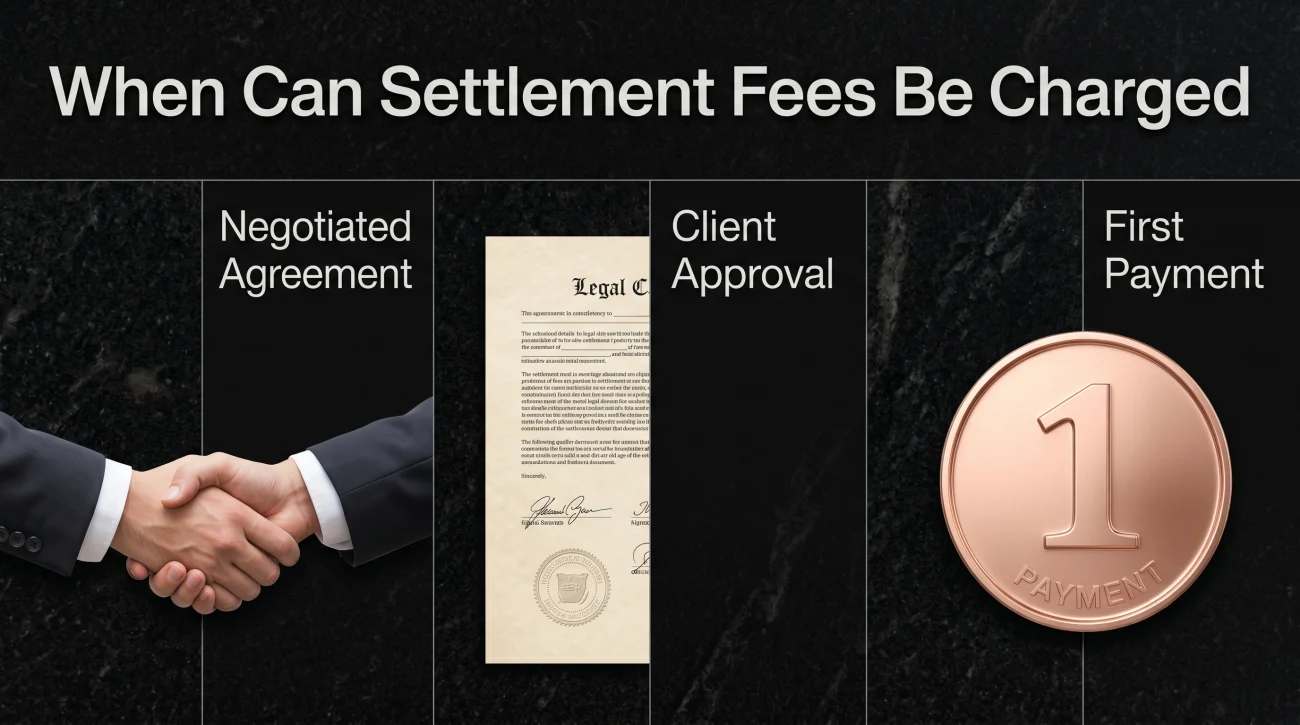

The timing of these fees is strictly governed by the Federal Trade Commission. Under the Telemarketing Sales Rule, debt relief companies that sell their services over the phone are legally prohibited from collecting a fee until three specific conditions have been met:

- The company has successfully negotiated a settlement agreement with a specific creditor.

- You have explicitly approved that specific settlement agreement.

- You have made at least one payment toward that settled debt from your funding account.

This rule is the strongest piece of consumer protection you have against fraud.

Paying a $500 enrollment fee to a company on day one, before they have contacted a single creditor on your behalf. This is illegal and a classic sign of a predatory operation.

Depositing funds strictly into an FDIC-insured account that you control, with the settlement company’s fee only being deducted after a successful, approved settlement is finalized.

It is also important to note that fees are usually calculated based on the total enrolled debt at the time you sign up, not the final settled amount. If you enroll a $10,000 credit card balance and the company’s fee is 20 percent, you will owe them $2,000 for that account upon a successful settlement, regardless of whether they settle the actual debt for $4,000 or $6,000.

Who Regulates and Accredits the Industry

Because the debt relief industry has historically attracted bad actors, voluntary accreditation has become a vital way for legitimate companies to separate themselves from the scams. Looking for specific industry credentials should be your very first filter.

The primary organization to look for is the Association for Consumer Debt Relief (ACDR). Members of the ACDR must adhere to a strict code of conduct and undergo regular audits to ensure compliance with federal billing rules. When I was working collection accounts, if a consumer told us they were represented by a firm, the very first thing we did was check the ACDR directory. If the company was not listed, we treated the account exactly the same as if the consumer had no representation at all, because we knew from experience that an unaccredited operation rarely followed through on its promises.

While ACDR membership vets the firm at the corporate level, you also want assurance about the individuals working your case. That is where another credential comes in: certification through the International Association of Professional Debt Arbitrators (IAPDA). This organization focuses on training and certifying the individual debt consultants who answer your calls and negotiate your accounts. IAPDA certification ensures that the representatives handling your financial future actually understand the laws governing collection practices.

💡 Pro Tip: Do not just take a company’s word for it if they display an accreditation logo on their website. Verify their membership directly on the ACDR or IAPDA directories. Fraudulent operations frequently steal these logos to appear legitimate.

Evaluating the Major Players by Debt Profile

A verified accreditation badge tells you a firm is operating legally, but it does not tell you if they are the right fit for your specific accounts. You have likely seen advertisements for large national providers like National Debt Relief (NDR), Freedom Debt Relief (FDR), and Accredited Debt Relief (ADR). While all three are established ACDR members, your choice should be based on your unique financial situation and your state of residence.

| Company | Minimum Enrolled Debt | Typical Fee Range | Profile Fit |

|---|---|---|---|

| National Debt Relief | $7,500 in unsecured debt | 15% to 25% | Best for straightforward credit card and personal loan balances. |

| Freedom Debt Relief | $7,500 in unsecured debt | 15% to 25% + minor account fee | Strong history navigating complex or litigious original creditors. |

| Accredited Debt Relief | $10,000 in unsecured debt | Average of 25% | Appeals to consumers needing high-touch customer service. |

When looking at National Debt Relief vs Freedom Debt Relief, the decision often comes down to the types of accounts you hold and your geographic location. Neither company operates in every US state due to varying state-level regulations. Furthermore, if your debt portfolio includes aggressive original creditors known for filing early lawsuits, a firm with a massive historical database of creditor behaviors like Freedom Debt Relief might offer a strategic advantage.

An Accredited Debt Relief review will often highlight their proactive communication during the difficult early months, though they require a slightly higher minimum debt threshold to qualify. Always match the firm’s strengths to the specific accounts you are struggling to pay. For example, if your debt includes accounts from banks known for filing lawsuits quickly, prioritize a firm with a deep history of litigation defense tactics over one that specializes primarily in basic retail credit cards.

The Questions You Must Ask Before Enrolling

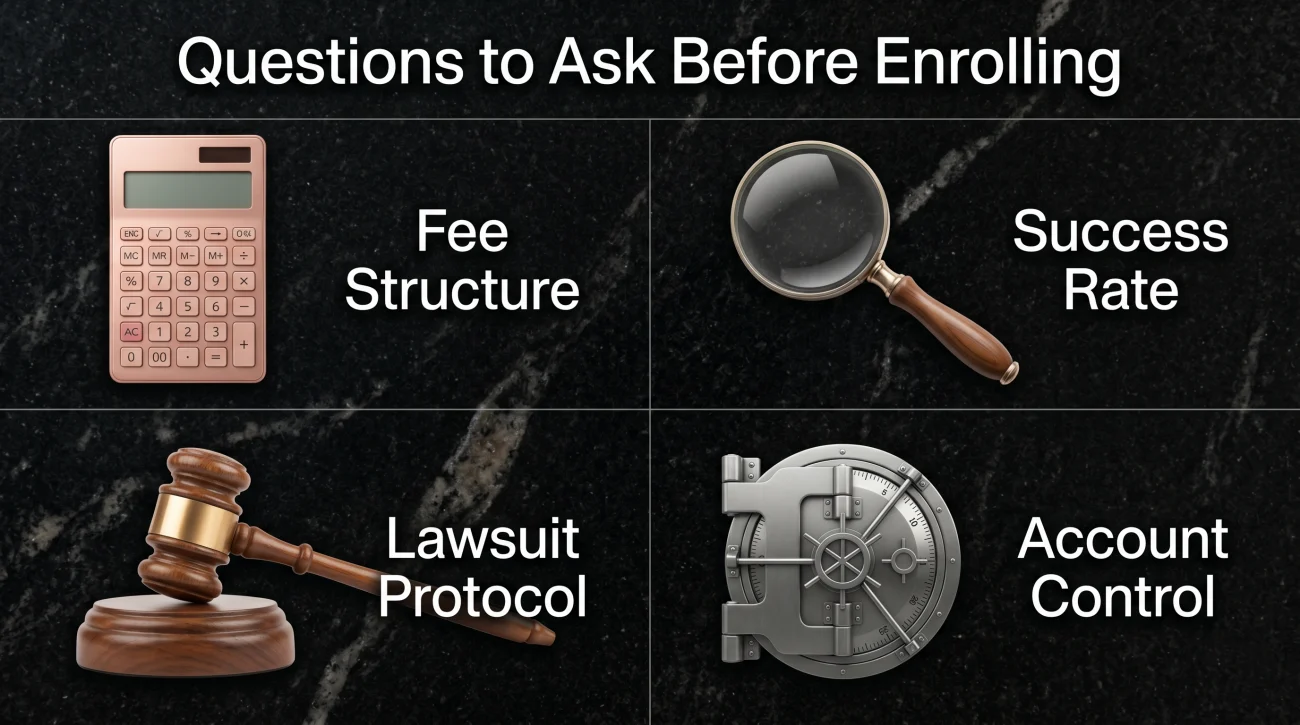

A legitimate company will welcome detailed questions about their internal processes. A predatory company will try to rush you off the phone and push for a signature. When you get a representative on the line, here are the specific questions you must ask:

- 📌 What is your exact fee structure? Force them to state clearly whether the fee is based on the enrolled amount or the settled amount, and confirm the exact percentage.

- 📌 What percentage of your clients actually complete the program? Debt settlement is difficult, and drop-out rates can be high. A firm that claims a perfect success rate is lying to you.

- 📌 What happens if an original creditor decides to sue me? This is a major fear point. Because you are withholding payments, creditors retain the right to sue. A transparent firm will explain whether they will prioritize settling that specific account to avoid a judgment, or if they partner with legal defense networks to help you respond.

- 📌 Who controls the holding account? Ensure they state clearly that the account is in your name at a third-party banking institution.

The reality is that these programs require immense patience. Before you commit, you need to look hard at how long debt settlement actually takes. Understanding that timeline upfront is the only way to know if you have the stamina for a process that typically runs 24 to 48 months.

What to Watch For in the Contract

Verbal promises from a sales representative mean absolutely nothing in this industry. If a promise is not explicitly stated in the written contract, it does not exist. Before you sign, you must review the agreement for a few critical items.

First, verify the cancellation terms. Life happens, and you might face a medical emergency midway through a 36-month program. A legitimate contract will state that you can cancel at any time without penalty, and that all unearned funds currently sitting in your account will be returned directly to you.

“The Client may terminate this Agreement at any time by providing written notice. Upon termination, any funds held in the Client’s dedicated account, less any fees already earned by the Company for settlements previously completed and approved by the Client, shall be returned to the Client within 5 business days.”

Second, ensure there is a clear disclosure regarding tax consequences. When a creditor forgives a portion of your balance, the IRS may consider that forgiven amount as taxable income. While most settlement clients qualify for an insolvency exclusion, a trustworthy company will proactively warn you about the potential of receiving a 1099-C tax form rather than hiding this reality.

Finally, ensure you are actually signing up for the correct service. If you are unsure if you can handle the severe credit damage involved, comparing the differences between debt settlement and credit counseling is a necessary step before putting your signature on any binding document.

Signs You Are Dealing With a Scam

The anxiety of dealing with aggressive debt collectors makes consumers vulnerable to anyone offering a quick fix. Scammers know this, and they use high-pressure tactics to exploit that fear. If you are currently speaking with an agency and experiencing any of the following, you need to hit the brakes.

If a representative guarantees a specific settlement outcome or timeframe, walk away. No third-party company can force a creditor to accept a 40 percent reduction. Settlement offers depend entirely on the creditor’s internal policies, the age of the debt, and who currently owns the account. Legitimate contracts will clearly state that results vary and creditors are not obligated to settle.

Another massive warning sign is a company that instructs you to ignore all mail, including certified letters or lawsuit summonses. Legitimate companies will often advise selective communication and will notify your creditors that you are represented. However, telling you to ignore a court summons is incredibly dangerous. Ignoring a lawsuit will result in a default judgment against you, which quickly leads to frozen bank accounts or wage garnishment.

📌 Note: If an agency claims they have a special government program to eliminate your credit card debt, hang up. There is no federal government program designed to forgive private unsecured debt.

If you suspect you have engaged with a fraudulent operation, your first step is to stop any automatic bank withdrawals. From there, identifying the specific warning signs of debt relief scams can help you safely report them to your state attorney general. For those who are ready to move forward safely, reviewing vetted and established debt settlement companies is the best way to ensure your financial recovery is in capable hands.

Choosing Based on Facts Not Pressure

Deciding to enter a settlement program is a major financial commitment. It requires discipline, patience, and a willingness to endure temporary credit damage in exchange for long-term relief. In my years on the operational side, the consumers who successfully navigated the process were the ones who understood exactly what they were signing up for on day one.

Do not let a high-pressure sales pitch dictate your timeline. Take a breath, review the fee structure, verify their industry credentials, and ensure the funding account operates under your control. Legitimate firms provide a highly valuable service for those who truly need it, but the burden of verifying their operational ethics rests firmly on your shoulders. Read the contract, ask the hard questions about litigation risks, and only proceed when you are fully comfortable with the terms.

If you are still weighing whether this path makes sense for your broader financial picture, exploring the full spectrum of options for dealing with debt will ensure you aren’t overlooking a simpler solution tailored to your specific hardship level.

❓ FAQ

🤔 Are debt settlement companies worth it?

They can be worth it if you are unable to make your minimum payments and have significant unsecured debt. While their fees take a portion of your savings, they handle the stress of negotiation and have established relationships with creditors. If you can afford to pay your debts in full over time, they are not the right choice.

🛠️ Can I do debt settlement myself?

Yes. You can contact your creditors or debt collectors directly to negotiate a lump-sum payoff. Doing it yourself saves you the 15 to 25 percent fee charged by settlement agencies, but it requires significant time, patience, and the ability to negotiate firmly with experienced collection floors.

📉 Will debt settlement ruin my credit?

It will cause severe damage to your credit score in the short term. Because you must stop paying your creditors for the accounts to become delinquent enough to settle, those missed payments will be heavily reported. Additionally, accounts are noted as “settled for less than the full balance.”

🏢 Does National Debt Relief hurt your credit?

Yes, enrolling with National Debt Relief or any similar firm will hurt your credit initially. The credit damage comes from the missed payments required to facilitate the negotiation process, not from the specific company you choose to hire.

💰 How much should I pay a debt settlement company?

You should expect to pay between 15 and 25 percent of the total enrolled debt balance. The fee is only due after a specific debt has been successfully negotiated and you have approved the final agreement.

🚪 What happens if I quit a debt settlement program?

If you cancel your contract, any unearned funds remaining in your dedicated account will be returned to you. However, any accounts that have not yet been settled will remain delinquent, and you will still be responsible for negotiating them or facing potential collection actions.

⚖️ Can I be sued while in debt settlement?

Yes. Because you are withholding payments from your creditors during the program, original creditors or debt buyers maintain the legal right to file a lawsuit to recover the balance. Legitimate firms will disclose this litigation risk in their contracts.

🔍 How do I know if a debt relief company is legit?

A legitimate operation will comply with federal billing laws, will use a third-party banking institution for your funds, and will hold active membership with the Association for Consumer Debt Relief (ACDR). They will also never guarantee a specific settlement amount.

✅ Is Freedom Debt Relief a legitimate company?

Yes, Freedom Debt Relief is an established firm. They are a founding member of the ACDR and have resolved billions of dollars in debt since their founding in 2002. They operate within the bounds of federal telemarketing rules regarding fee collection.

🏦 Do debt settlement companies actually pay your debt?

They facilitate the payment, but the money ultimately comes from you. You fund a dedicated account with monthly deposits. Once a settlement is reached, the firm transfers those funds directly to the creditor to satisfy the agreed-upon amount.

Relief options exist alongside the collection process. These explain both sides.

- The options for resolving debt outside of continued collection

- Do You Owe Taxes on Settled Debt? The 1099-C, the Insolvency Exclusion, and What to Do

- How Does a Debt Management Plan Work: How Nonprofit Credit Counseling Actually Helps You Pay Off Debt

- Debt Relief Scams: How to Spot Them Before You Pay and What the FTC Says About Legitimate Companies

- Debt Snowball vs Debt Avalanche: Which Pays Off Debt Faster - and Which One You'll Actually Finish

Some of these have deadlines attached. Start here if something is already happening.

- What collectors can legally do to you while a settlement program is running

- How to handle a lawsuit on a debt you are actively trying to settle

- What happens to a garnishment order when debt relief is in progress

- How bank levies interact with the debt you are trying to resolve

- How professional settlement programs work and what they actually cost

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.