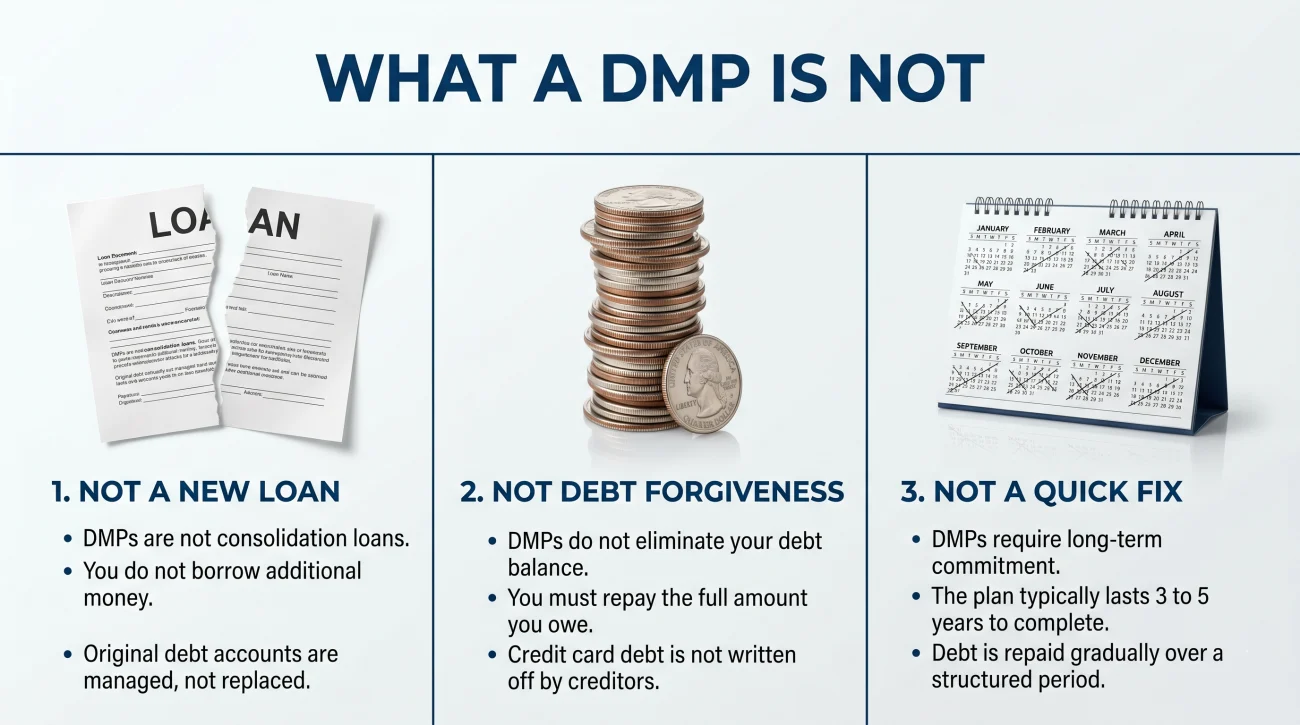

- A Debt Management Plan (DMP) is not a new loan and it does not settle your debt for less than you owe. You pay back 100 percent of the principal.

- The core benefit is a drastically reduced interest rate. Nonprofit agencies typically negotiate credit card rates from 20 to 30 percent down to 0 to 8 percent.

- You make one single monthly payment to the credit counseling agency, and they disburse the funds to your creditors on a set 3 to 5 year schedule.

- To qualify, you must have a consistent income. If you miss a DMP payment, your creditors can instantly revoke the lower interest rates.

The Mechanics of Paying Full Principal at a Lower Rate

There is a massive amount of confusion about what a debt management plan actually is. When people realize they are drowning in minimum payments, they start searching for relief. They hear terms like “consolidation,” “settlement,” and “management plan” thrown around as if they are the exact same thing.

They are not. A debt management plan, commonly called a DMP, is fundamentally different from taking out a loan or hiring a company to settle your accounts. It is not free money. It is a highly structured, rigid repayment agreement administered by a nonprofit credit counseling agency.

During my years working inside third-party collection agencies, I saw thousands of accounts cycle through the system. We always knew when a consumer had entered a legitimate DMP. The account would be flagged, the collection calls from our floor would stop, and we would wait for the agency’s disbursement check each month. From the inside, a DMP is one of the most reliable ways to stop the bleeding of compound interest, provided the consumer actually finishes the program.

The core mechanism of a DMP is simple: it slashes your interest rate so your monthly payment finally attacks the principal. This sounds straightforward, but transitioning from paying multiple credit cards to paying a single nonprofit agency requires a complete shift in how you handle your finances.

What a DMP Is (And What It Is Not)

To understand the mechanics, we have to strip away the marketing jargon. When you enroll in a DMP, you are hiring an intermediary. You are partnering with a nonprofit agency, typically a member of the National Foundation for Credit Counseling (NFCC), to negotiate with your original creditors on your behalf.

To understand how the program operates, we first need to clear up what you are actually signing up for.

- It is not a new loan. You are not borrowing money to pay off your old debts. Your debts stay exactly where they are, with the original creditors.

- It is not debt forgiveness. Unlike settlement programs, you are agreeing to pay back 100 percent of the principal balance you owe.

- It is not a quick fix. A standard DMP is designed to take between 36 and 60 months to complete.

What changes is the mathematical environment around the debt. The nonprofit agency contacts your creditors and asks them to place your accounts into a specific hardship tier. In exchange for you closing the credit cards and committing to a fixed payment schedule, the creditors agree to slash the interest rates and stop charging late fees.

“From a collector’s perspective, an account enrolled in a legitimate DMP was considered safe. Original creditors and debt buyers like these plans because they guarantee a steady, predictable recovery of the principal balance without the legal costs of filing a lawsuit.”

The Interest Rate Math That Makes It Work

The single biggest reason people stay stuck in credit card debt is the interest rate. If you are paying 24 percent APR on a large balance, a minimum payment barely covers the monthly finance charge. You are essentially paying rent on your own debt without ever owning it outright.

The reason a DMP is effective is that it changes this math drastically. NFCC member agencies have pre-existing concession agreements with all the major credit card issuers like Chase, Capital One, Discover, and Citibank. They do not have to negotiate your interest rate from scratch. The banks already have set policies that say, if a consumer enrolls through a certified nonprofit, we will drop their rate to a specific number.

Usually, that number drops from the mid-twenties down to anywhere between 0 and 8 percent.

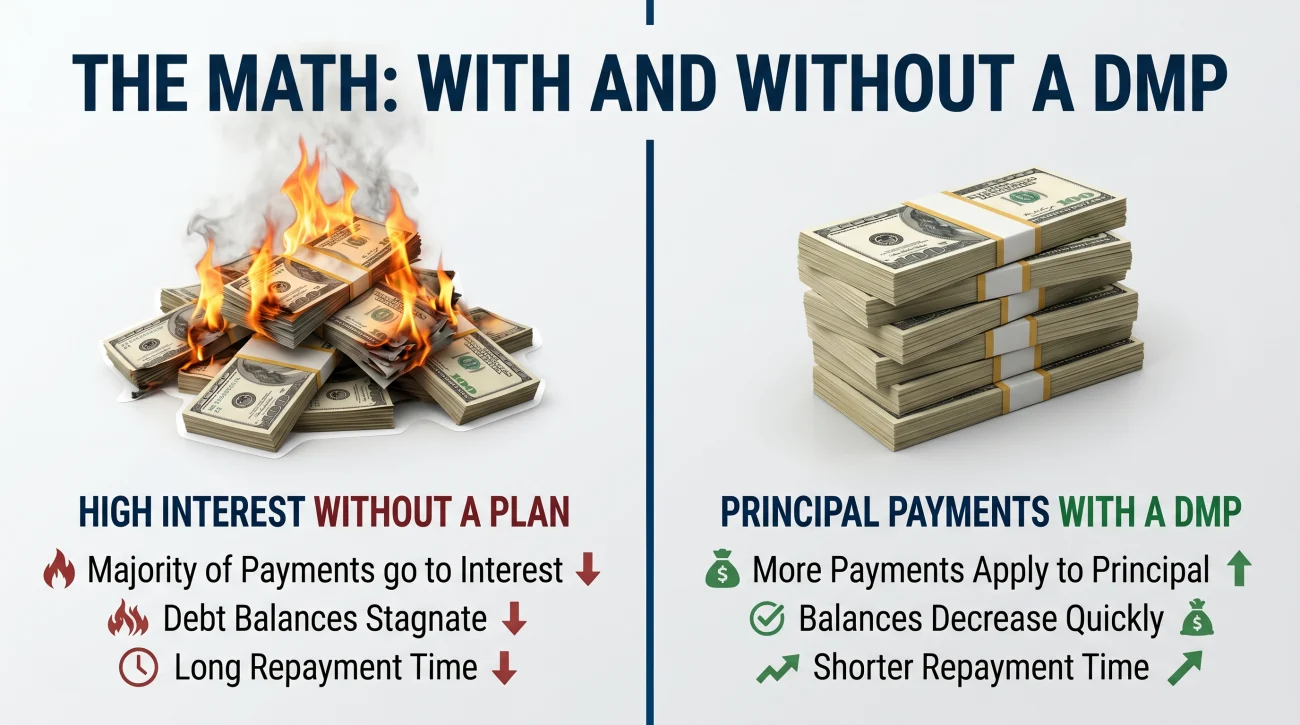

The Mathematics of Rate Reduction

Imagine you have $15,000 in credit card debt spread across three cards, averaging a 24% APR. You can realistically afford to pay $350 a month.

Without a DMP: Paying $350 a month at 24% APR, it will take you roughly 86 months (over 7 years) to pay off the balance. You will pay over $15,000 in interest alone. Your total cost will be over $30,000.

With a DMP: The agency negotiates your average rate down to 6%. You still pay exactly $350 a month. At this new rate, you will be entirely out of debt in roughly 48 months (4 years). You will pay only about $1,900 in total interest.

The payment amount did not change. The budget did not change. The only thing that changed was how much of that $350 went to the bank’s profits versus how much went to killing the principal balance. This is the entire leverage point of credit counseling.

How to Spot a Fake “Nonprofit” Credit Counselor

Because the term “debt relief” is used so broadly, many predatory companies disguise themselves as nonprofit credit counselors. They use similar language but offer completely different, often harmful, services.

Legitimate DMP providers are almost always accredited members of the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA). Their fees are transparent and strictly capped by state laws.

Legitimate agencies are transparent about their fees from the first call. If an agency asks for large upfront payments before any settlement is reached, that is a red flag you are not talking to a credit counselor. Furthermore, if they advise you to stop paying your creditors entirely to “negotiate a lower balance” instead of reducing your interest rate, you are likely dealing with a debt settlement operation, not a DMP.

Step-by-Step: How the Enrollment Process Works

Moving your accounts into a management plan is a highly formalized process. It requires full transparency about your income and living expenses. Here is exactly what happens when you pick up the phone to start.

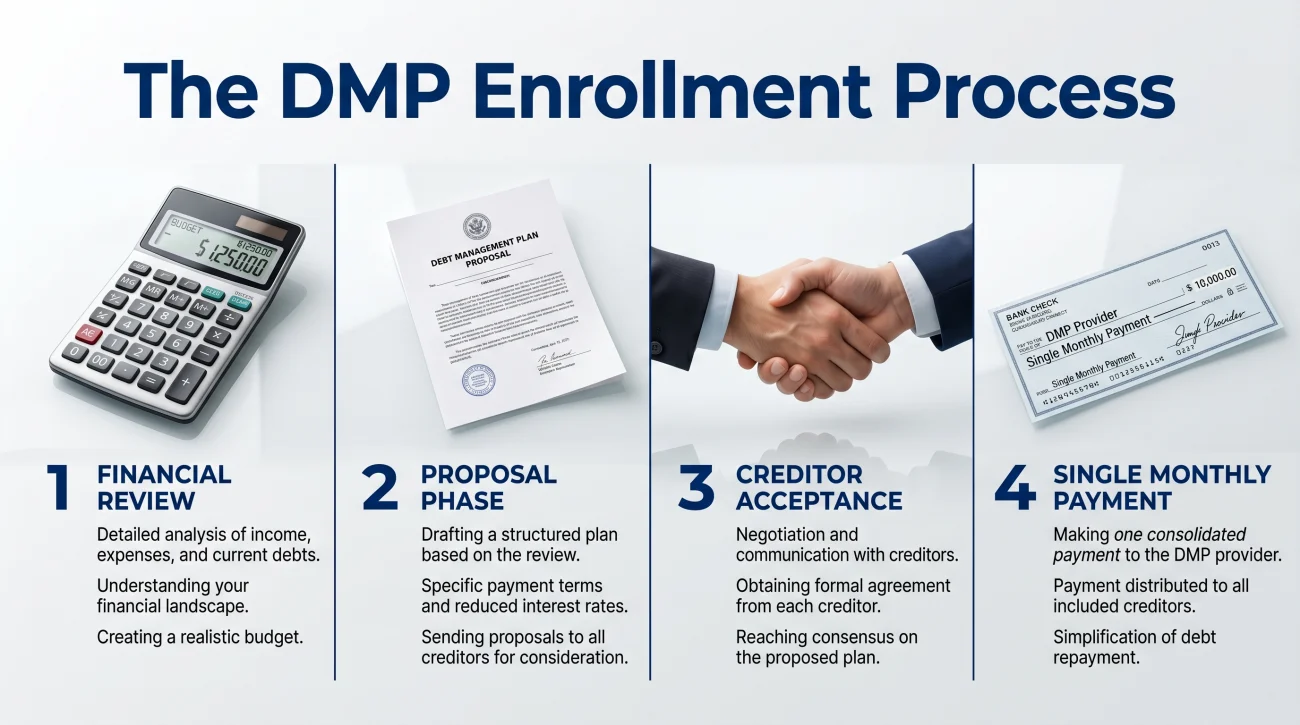

1. The Initial Financial Review

Your first interaction will be a free session with a certified credit counselor. This takes about an hour. They will pull your credit report (usually a soft pull that does not hurt your score) and ask you to detail your monthly take-home pay and your living expenses. They do this to calculate your exact monthly surplus. If you do not have enough surplus to afford the negotiated DMP payment, they will not enroll you. They will not set you up for a plan you will mathematically fail.

2. The Proposal Phase

If the counselor determines you can afford the plan, they draft a proposal. They send an electronic notification to each of your creditors stating your intent to enter a DMP. They propose a specific monthly payment to each creditor based on your balance and the pre-negotiated concession rates.

3. Creditor Acceptance and Account Closure

It takes a few weeks for creditors to respond. Usually, they accept. The moment they accept the proposal, your credit cards are closed to new purchases. You cannot keep using them. The banks are granting you a massive interest rate reduction, and in return, they are cutting off your ability to dig a deeper hole.

4. The Single Monthly Payment

You no longer pay the banks directly. Instead, you set up an automatic withdrawal from your checking account to the nonprofit agency. If your total agreed payment is $400, the agency takes $400 once a month. They then slice that money up and disburse it to Visa, Mastercard, and Discover on your behalf.

What Kind of Debt Actually Qualifies

A major point of confusion is what these agencies can actually manage. The rule of thumb is that a DMP is built for unsecured consumer debt. Unsecured means there is no collateral attached to the loan.

Credit cards are the primary target for these plans. Many agencies can also include unsecured personal loans and certain types of medical bills. If you are unsure how your specific mix of accounts will be treated, understanding exactly what debts can be settled or managed is a critical first step.

You cannot include secured debt in a DMP. Your auto loan is secured by your car. Your mortgage is secured by your house. If you stop paying those, the bank simply takes the asset back. Therefore, they have no incentive to participate in a credit counseling rate reduction program. Federal student loans are also excluded, as they have their own specific government-mandated income-driven repayment options.

A frequent complication arises with joint accounts or authorized users. If you have a joint credit card with a spouse, enrolling that card in a DMP affects both of you. The account will be closed, and the “managed by credit counseling” notation will appear on both credit reports. You cannot selectively enroll a joint account without impacting the co-signer.

Attempting to hide one credit card with a zero balance from the counselor so you can keep it open “just in case of emergencies.”

Disclosing all accounts. Creditors actively monitor your credit report during a DMP. If they see you keeping open lines of unsecured credit or opening new ones, they can revoke your concession rates and drop you from the plan.

Fees, Rules, and The Trap of Inconsistency

Nonprofit does not mean free. These agencies have staff, overhead, and processing systems to maintain. However, their fees are strictly regulated, often capped by state law.

Typically, you will pay a one-time setup fee ranging from zero to $50. After that, you will pay a monthly maintenance fee that ranges from $25 to $75. This fee is rolled into your single monthly payment. If your total payment to the agency is $400, perhaps $365 goes to your creditors and $35 goes to the agency. Compared to the hundreds of dollars you save in interest every month, the fee is generally negligible.

But the true cost of a DMP is the demand for absolute consistency. This is where many consumers lose their leverage.

⚠️ Warning: The concession rates granted by the banks are conditional. They are agreeing to 6 percent interest on the strict condition that you pay exactly on time, every single month, through the agency.

If your car breaks down and you miss your DMP payment, the agency cannot disburse funds to the banks. The banks will immediately notice the missed payment. In many cases, their automated systems will instantly revoke the concession agreement. Your interest rate will shoot right back up to the default 24 or 28 percent, late fees will be applied, and you will have to petition the agency to beg the creditors to let you back into the program.

In collections, we saw this constantly. A consumer would be on a DMP for two years, miss one payment due to a job loss, and the account would drop out of the program and end up right back on our collection floor.

How It Impacts Your Credit Score

The impact on your credit is a nuanced topic. There is a short-term hit and a long-term benefit.

When you enroll, your credit cards are closed. This negatively impacts your score in two ways. First, it lowers your total available credit, which drives your credit utilization ratio up. Second, over time, it impacts the average age of your open accounts. Additionally, the creditors will place a remark on your credit report stating that the account is being “managed by a credit counseling service.” This remark itself does not lower your FICO score, but future lenders will see it.

However, the long-term effect is overwhelmingly positive if you stick to the plan. In my experience reviewing credit files, consumers who make their DMP payments on time usually see their scores begin to stabilize and steadily recover around the 12 to 18 month mark. As the principal balances shrink due to the low interest rates, the lower credit utilization ratio eventually outweighs the penalty of the closed accounts.

DMP vs. Consolidation Loans

A very common question is whether a person should use credit counseling or just get a loan to pay everything off. The answer depends heavily on your credit score and your personal discipline.

To qualify for a debt consolidation loan at an interest rate low enough to actually save you money, you typically need a credit score above 680. If your score has already dropped because your balances are maxed out, any personal loan you qualify for will likely have an interest rate just as high as your credit cards. Moving 24 percent credit card debt into a 24 percent personal loan accomplishes nothing.

Furthermore, consolidation loans contain a trap. When you pay off your credit cards with a loan, the cards remain open with zero balances. Many consumers fall into the trap of using those cards again, ending up with the new consolidation loan plus a new pile of credit card debt. A DMP forces you to close the accounts, completely removing the temptation.

A management plan does not require a good credit score to qualify. Because the agency is not lending you money, there is no credit risk to them. As long as you have the income to support the monthly payment, you can access the lower negotiated interest rates regardless of how damaged your FICO score is.

Signs a DMP Is Not The Right Path For You

A management plan is a powerful tool, but it requires a very specific financial situation to succeed. It requires you to have a reliable, predictable budget surplus every month. You must be able to afford the negotiated payment. It is vital to understand all your debt relief options before locking into a five-year commitment.

You may need to explore different avenues if any of these situations apply to you:

- You have no budget surplus. If paying rent, utilities, and groceries leaves you with exactly zero dollars, you cannot afford a DMP. The agency will not accept you because the math simply does not work.

- Your income is highly unpredictable. If you work on commission or have wildly fluctuating gig income, the rigid, inflexible monthly payment of a DMP is a massive risk. One bad month can break the agreements.

- You are already months behind on payments. If your accounts have already charged off and been sold to collection agencies, a DMP is often less effective. You may be better served by looking at how to compare debt settlement vs credit counseling to see which strategy fits a delinquent profile.

If you cannot mathematically afford a management plan, but you still need intervention to stop aggressive collections, your focus should shift toward exploring programs that allow you to resolve your accounts for less than you owe. Doing nothing while the interest compounds is the only truly wrong choice.

Final Thoughts: Graduating from the Program

A debt management plan is a marathon. It requires you to live on a strict cash basis for years while your peers might still be swiping credit cards to fund their lifestyles. I have seen many consumers quit in month six because the lifestyle adjustment was simply too hard.

But I have also seen what happens in month 48. When you graduate from a DMP, you are completely free of the enrolled debt. Your credit score has typically stabilized and often improved. At that point, your focus shifts to rebuilding. You start with a clean slate, perhaps opening a single secured card to re-establish a normal credit history. For consumers who have steady income but just need the banks to stop the aggressive compound interest, this structured path is one of the most reliable ways out.

❓ FAQ

💰 How much does a debt management plan cost to start?

Nonprofit agencies typically charge a one-time setup fee of up to $50, followed by a monthly maintenance fee of $25 to $75. These fees are often capped by the state where you live.

💳 Do I have to include all my credit cards in the plan?

In most cases, yes. Creditors generally require you to close all open lines of unsecured credit to qualify for the hardship interest rates. Attempting to keep a card open can result in creditors rejecting your proposal.

📞 Will debt collectors stop calling me if I enroll?

Yes. Once your creditors accept the agency’s proposal and your payments begin, standard collection calls regarding those enrolled accounts will stop, as you are now in a recognized repayment program.

⚠️ What happens if I miss a payment to the counseling agency?

Your creditors can instantly revoke the concession agreements, raise your interest rates back to the default penalty levels, and apply late fees.

📉 Does entering a DMP ruin my credit score?

There is a short-term drop because your accounts are closed, which affects your credit utilization. However, consistent on-time payments over the life of the plan usually result in a stronger credit score by the time you graduate.

⚖️ Is a debt management plan the same thing as bankruptcy?

No. Bankruptcy is a legal court process that discharges debt. A DMP is a voluntary repayment plan where you pay back 100 percent of the principal you owe, just at a lower interest rate.

🏢 Will my employer find out I am using a credit counselor?

No. Your enrollment in a DMP is a private financial matter between you, the nonprofit agency, and your creditors. It is not public record and your employer is not notified.

🏠 Can I still buy a house while on a management plan?

It is difficult but possible. Most mortgage lenders require you to be on the plan for at least 12 consecutive months with a perfect payment history, and you usually need written permission from the credit counseling agency to take on new debt.

Relief options exist alongside the collection process. These explain both sides.

- The options for resolving debt outside of continued collection

- How Debt Settlement Actually Works: What Happens from Enrollment to Final Settlement

- Debt Settlement vs Credit Counseling: Two Very Different Programs for Two Very Different Situations

- Do You Owe Taxes on Settled Debt? The 1099-C, the Insolvency Exclusion, and What to Do

- How to Choose a Debt Settlement Company: What NDR, FDR, and ADR Actually Offer and the Red Flags to Avoid

Some of these have deadlines attached. Start here if something is already happening.

- What collectors can legally do to you while a settlement program is running

- How to handle a lawsuit on a debt you are actively trying to settle

- What happens to a garnishment order when debt relief is in progress

- How bank levies interact with the debt you are trying to resolve

- How professional settlement programs work and what they actually cost

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.