- When a creditor forgives $600 or more of your debt, the IRS generally considers that canceled amount as taxable income, triggering a Form 1099-C.

- Most people who settle debts do not actually owe taxes on the forgiven amount because they qualify for the IRS “insolvency exclusion.”

- If your total liabilities exceeded the total value of your assets at the exact time the debt was settled, you are legally insolvent and can exclude the canceled debt from your income using Form 982.

The Post-Settlement Tax Panic

You fought through the collection calls, you finally scraped together a lump sum, and you successfully negotiated a $10,000 credit card balance down to $4,000. You feel a massive sense of relief. The debt is behind you. Then, late the following January, an official-looking document arrives in the mail from your former creditor. It is a Form 1099-C, and it says you received $6,000 in “Cancellation of Debt” income.

The panic usually sets in immediately. Most people assume this means they now owe the IRS taxes on $6,000 they never actually received. I spent twelve years inside the debt collection industry, and I saw this cycle of confusion happen every single tax season. Collectors rarely explain the tax implications when they are pushing you to agree to a payment. Their goal is to get the account resolved, not to act as your accountant.

The IRS does consider forgiven debt to be income. That is the rule. But there is a massive exception to this rule that applies to the vast majority of people who are forced to settle their accounts. It is called the insolvency exclusion.

The good news is that if you were dealing with a true financial hardship when you settled your debt, you likely qualify for this protection. The IRS specifically wrote this rule because it makes no sense to tax money you do not actually have. This guide will walk you through exactly how Form 1099-C works, how to calculate your insolvency, and how to prove it on paper so you can protect yourself from paying a tax bill you do not actually owe.

Why the IRS Treats Canceled Debt as Income

To understand how to avoid paying taxes on a settlement, you first have to understand the logic behind why the IRS cares about it at all. When you originally borrowed money from a bank or used a credit card to make a purchase, that money was not taxed as income. The IRS does not tax loans because you have a legal obligation to pay the money back.

However, when a creditor agrees to accept less than the full balance and completely forgives the rest, that legal obligation to repay disappears. In the eyes of the tax code, you received an economic benefit. Since you got to keep the money or the goods you bought without having to pay for them, the IRS views that forgiven balance as income you essentially “earned” that year.

If a bank forgives $600 or more of a principal balance, they are legally required to file a Form 1099-C with the IRS and send a copy to you. The form will show the exact amount canceled and the date the settlement was finalized.

“Inside the collection agencies I worked for, generating 1099-C forms was entirely automated. Once the final settlement payment cleared and the forgiven amount hit the $600 threshold, the system flagged it for the January mailing batch. No human reviewed it to see if you could afford the taxes. It is simply a compliance requirement for the creditor.”

This automated reporting happens whether you negotiated the account yourself or whether you spent months completing a debt resolution program. The creditor’s system only cares about the math. But just because the creditor reports the canceled debt to the IRS does not mean you automatically have to write a check to the government.

The Insolvency Exclusion: Why Most Clients Owe Nothing

This is the most critical concept to grasp if you have settled an account. The IRS recognizes that if you were broke enough to require a debt settlement, taxing you on the forgiven amount makes no logical sense. They provide a specific relief mechanism called the insolvency exclusion.

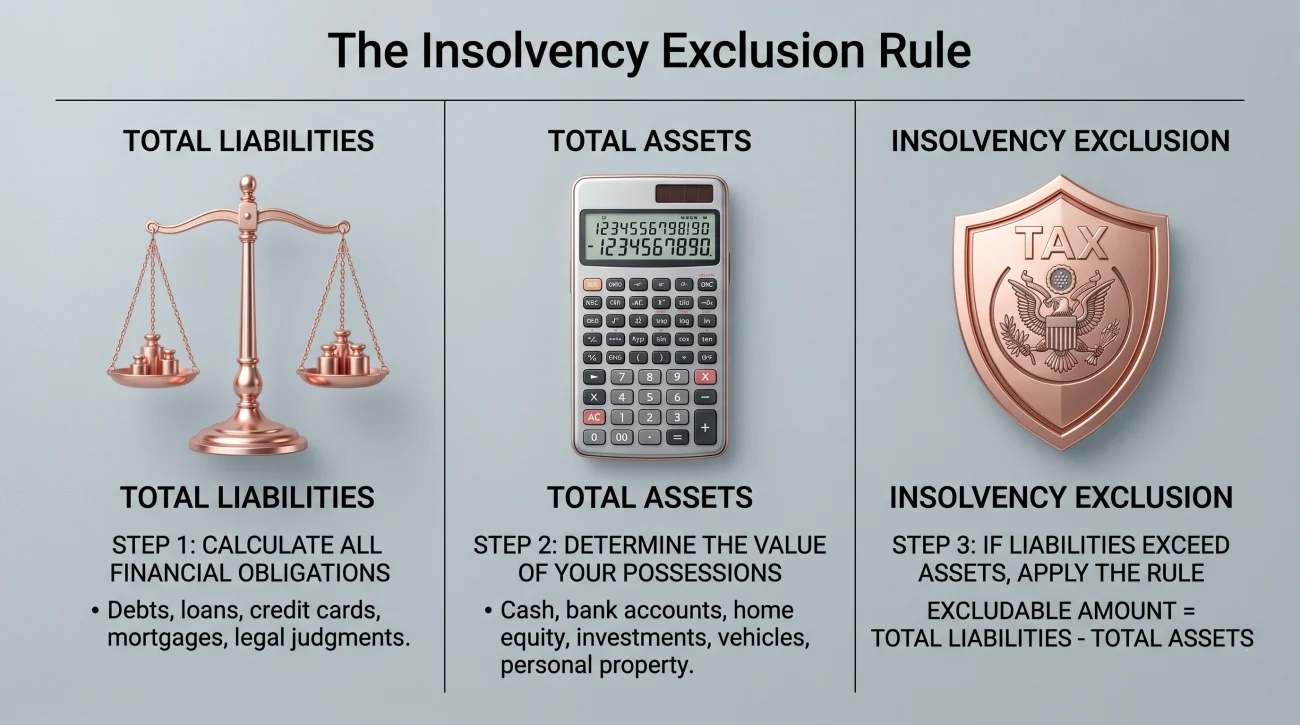

If you were legally insolvent at the exact moment the debt was canceled, you can exclude the forgiven amount from your taxable income up to the amount of your insolvency.

What does “insolvent” mean to the IRS? It is a simple math equation: your total liabilities (everything you owe to everyone) exceeded the fair market value of your total assets (everything you own) immediately before the cancellation occurred.

Let’s look at how this math works in the real world.

Imagine you settle a credit card account, and $10,000 is forgiven.

Immediately before the settlement, you take an inventory of your finances:

Total Debts (credit cards, medical bills, car loan, student loans): $50,000

Total Assets (bank balance, value of your car, personal property): $35,000

$50,000 (Liabilities) minus $35,000 (Assets) = $15,000.

You are legally insolvent by $15,000.

Because your insolvency ($15,000) is greater than the forgiven debt ($10,000), the entire $10,000 is excluded from your income. You owe zero taxes on the settlement.

Most people who are forced into a position where they cannot pay their minimums fit this profile perfectly. Their debts far outweigh what they own, which is exactly why they stopped paying in the first place. This protection is the primary reason why the fear of a massive tax bill is usually worse than the reality.

What Actually Counts in the Asset and Liability Test?

While the concept of insolvency is straightforward, the way you calculate it can trip people up. The IRS requires you to calculate the fair market value of all your assets. This does not just mean the cash in your checking account. It includes things you cannot easily liquidate.

Here is what you must include when calculating your assets for the insolvency test:

- The current market value of your vehicles (what they would sell for today, not what you paid).

- The fair market value of your home or real estate.

- Balances in all checking, savings, and investment accounts.

- The balance of your retirement accounts (401k, IRA, pension), even if you cannot access them without a penalty.

- The garage-sale value of your furniture, electronics, and personal property.

⚠️ Warning: Feeling broke on a monthly basis is not the same as being legally insolvent. If you have $45,000 in credit card debt, but you also have $60,000 sitting in a 401k that you have not touched, the IRS views your assets as greater than your liabilities. In that specific scenario, you would not be insolvent, and the canceled debt would likely be taxable.

On the liability side, you count every single debt you owe immediately before the settlement. This includes the debt that is about to be forgiven, your remaining credit cards, auto loans, mortgages, medical bills, student loans, and even unpaid taxes.

The timing is crucial. You measure your insolvency immediately before the specific debt was canceled. If you settle four different accounts across an entire year, technically, you have to run the insolvency calculation four separate times based on the date of each settlement.

How Collectors Weaponize the 1099-C in Negotiations

Because the insolvency exclusion is so powerful, you might wonder why debt collectors never mention it. During my years on the collection floor, I frequently heard collectors use the threat of a 1099-C to manipulate consumers into making larger payments instead. It is a common psychological tactic. The collector knows that you are afraid of the IRS.

The pitch usually sounds like this: “Listen, if we settle this for half, we are legally required to send you a 1099-C for the rest. You are going to end up paying the IRS anyway, so you might as well just pay us the full balance today to avoid a tax audit.”

Panicking when a collector brings up the IRS, assuming that a tax bill is unavoidable, and agreeing to a higher settlement amount just to prevent a 1099-C from being issued.

Recognizing that the collector is using the tax code as a scare tactic. Knowing that if your debts exceed your assets, the insolvency exclusion will protect you regardless of what the collector claims.

This is why handling discussions with creditors directly requires you to understand the rules better than the person on the other end of the phone. The collector does not know your total asset picture. They do not know if you are insolvent. They are simply using the word “taxes” as leverage to close a deal.

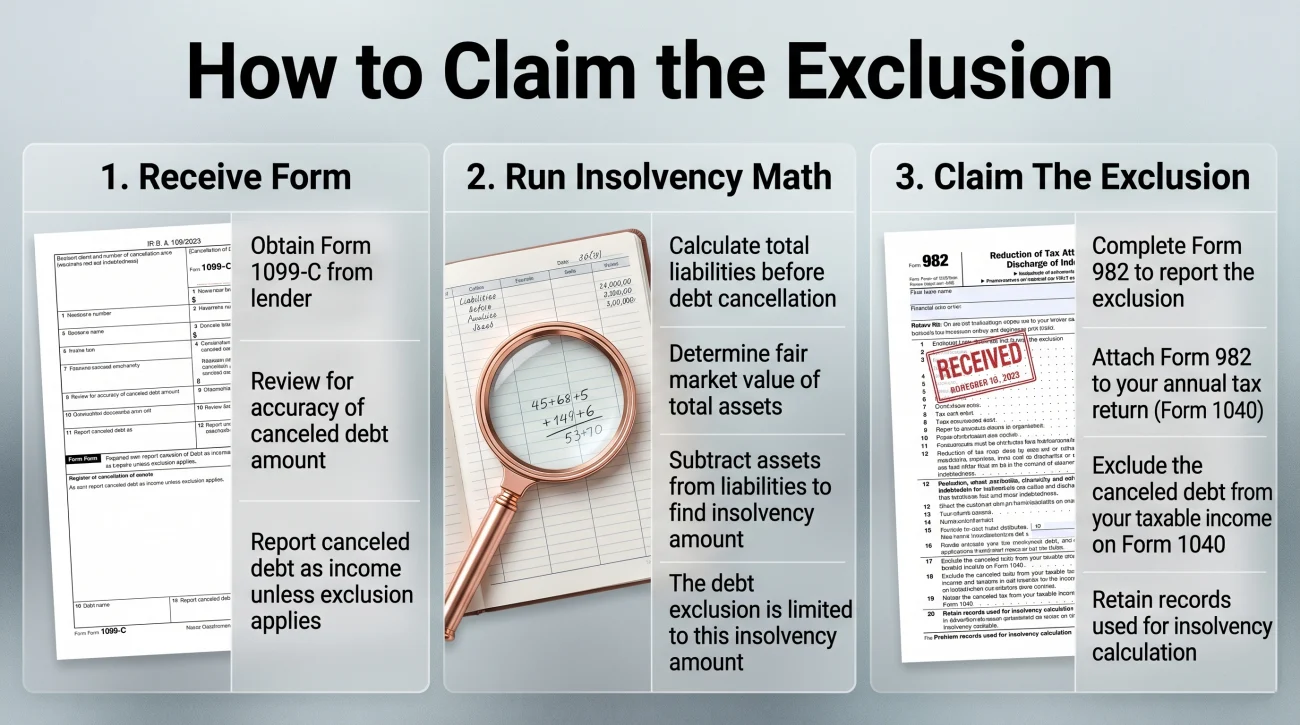

How to Claim the Exclusion Using Form 982

Once you have run the numbers and confirmed that your liabilities exceeded your assets, the next step is proving it to the government. You do not get the insolvency exclusion automatically just because you were broke. You have to claim it when you file your federal tax return for the year you received the 1099-C. This is done using IRS Form 982 (Reduction of Tax Attributes Due to Discharge of Indebtedness).

When filing, you will take the canceled debt amount from your 1099-C and include it on your tax return. Then, you use Form 982 to show the IRS that you qualify for the exclusion. You will check the box indicating a “discharge of indebtedness to the extent insolvent,” and you will list the amount of the forgiven debt that is excluded based on your calculation.

The IRS Publication 4681 provides a specific “Insolvency Worksheet” that helps you list out your assets and liabilities. While you do not have to mail this worksheet in with your tax return, you must keep it in your files. If the IRS ever questions your exclusion, that worksheet is your proof.

I always tell consumers that if their financial situation is complex, or if they own property and retirement accounts, they should have a tax professional handle Form 982. A good CPA will know exactly how to document the fair market value of your assets to ensure the exclusion is applied correctly. If you are evaluating professional negotiation firms to handle your accounts, they will often advise you that this tax form is coming, but by law, they cannot fill it out for you.

Other Exemptions Besides Insolvency

While insolvency is the most common reason a settled debt becomes tax-free, there are a few other scenarios where canceled debt is completely excluded from your taxable income.

The most absolute protection comes from bankruptcy. If your debt is discharged in a Title 11 bankruptcy proceeding (like Chapter 7 or Chapter 13), it is never taxable. There is no asset calculation required, and there is no cap on the dollar amount. The bankruptcy court order acts as an absolute shield against the IRS.

“On the collection floor, a bankruptcy filing was the ultimate stop sign. The moment a consumer provided a valid Chapter 7 case number, the account was dead to us. We knew the bankruptcy discharge was bulletproof – not just against our collection efforts, but against any future tax liability for the consumer. Unlike settlement where we still generated a 1099-C, a bankruptcy meant the IRS would not view the wiped balance as income.”

Additionally, certain types of student loan forgiveness are excluded from income, particularly if the loan is canceled in exchange for working in a specific public service profession for a set period. However, this is highly specific to federal programs and rarely applies to standard consumer debts.

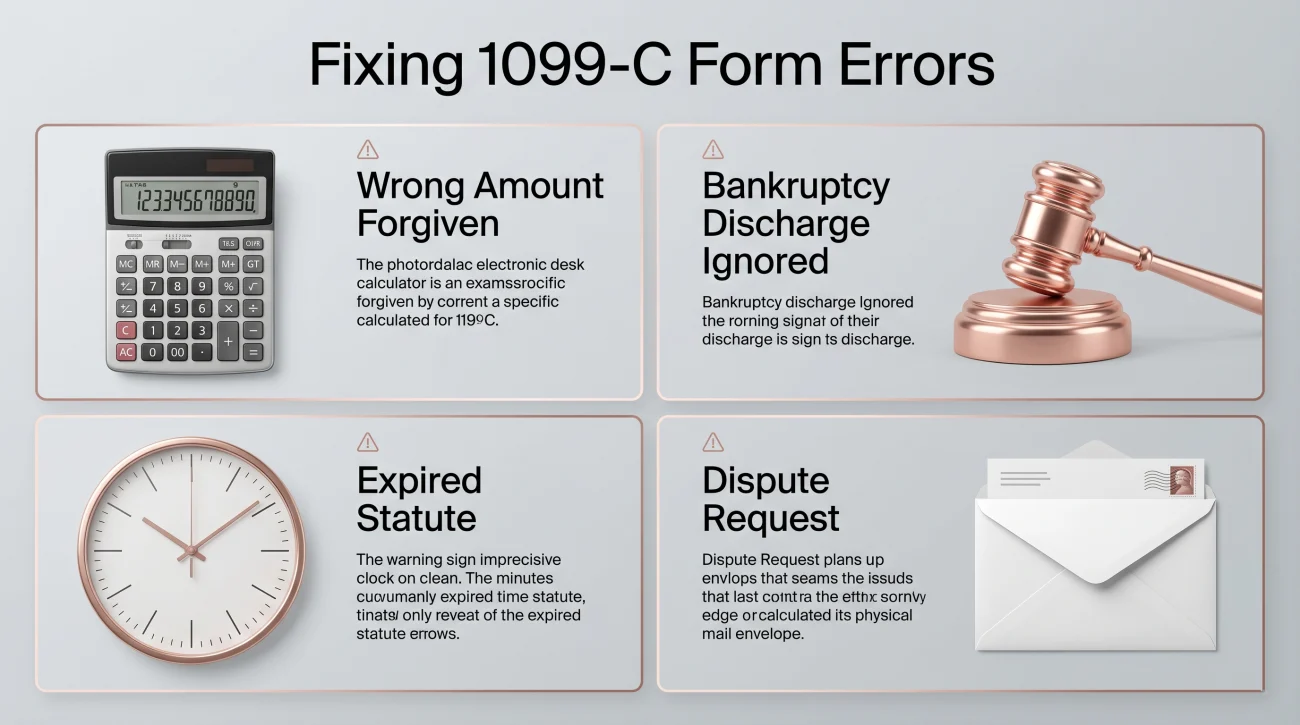

What to Do if Your 1099-C Has Errors

One of the most frustrating realities of post-settlement life is dealing with creditor paperwork errors. It is not uncommon to receive a 1099-C that is completely inaccurate.

Common errors include reporting the wrong amount forgiven, issuing a 1099-C for a debt that was actually included in a bankruptcy discharge, or sending a form for a debt where the statute of limitations expired years ago without any settlement taking place.

If you receive a 1099-C with incorrect information, you must take action. Do not simply attach it to your tax return and assume the IRS will sort it out. Contact the creditor’s tax reporting department immediately. Request that they issue a corrected 1099-C.

This highlights the golden rule of debt resolution: keep a paper trail of everything. You must save your written settlement agreement, the proof of your cleared payment, and any confirmation letters stating the account was settled. If the creditor refuses to correct a faulty 1099-C, you will need that documentation to prove to the IRS that the reported amount is wrong.

Signs You Should Stop Letting Tax Fear Delay Your Settlement

Many consumers stay trapped in a cycle of minimum payments purely because they are terrified of the tax consequences of a settlement. If you are holding off on negotiating an account, you need to evaluate if that fear is actually justified based on your real-world finances.

You are likely letting tax anxiety paralyze you unnecessarily if:

- You are avoiding settlement discussions even though your total debt load is objectively larger than everything you own.

- You are considering draining a protected retirement account to pay a collector in full, just to avoid a potential 1099-C.

- You are trying to manage multiple high-balance accounts on your own, falling further behind each month, rather than seeking a structured resolution because you fear an IRS audit.

If your liabilities outweigh your assets, the tax impact is often zero. If you are overwhelmed by multiple accounts and want to see how professionals manage both the negotiation process and the documentation, you may want to consider working with an established settlement organization to map out a comprehensive strategy.

Final Thoughts: Documentation is Your Best Defense

The fear of the IRS is a powerful deterrent, but it should not keep you trapped in a cycle of debt you cannot afford. The tax code provides the insolvency exclusion specifically so that a financial hardship does not turn into a permanent tax burden. Knowing the rules allows you to take control of your accounts without panic.

Your primary job now is proactive record-keeping. Save the settlement agreement, keep your proof of payment, and run your insolvency worksheet the day the settlement clears, rather than waiting for January. Having your asset values documented early makes tax season stress-free. If you are still weighing your next steps, take the time to continue reviewing all available pathways to eliminate your balances.

❓ FAQ

💵 Do I have to pay taxes on forgiven debt?

By default, the IRS considers forgiven debt as taxable income. However, if your total debts were greater than your total assets at the time of the settlement, you can use the insolvency exclusion to eliminate the tax liability completely.

📄 What is a 1099-C form for debt?

A 1099-C is an official IRS tax form titled “Cancellation of Debt.” Creditors are legally required to send this form to you and the IRS if they forgive $600 or more of a principal debt balance during a settlement.

⚖️ How do I prove I was insolvent?

You prove insolvency by completing the IRS Insolvency Worksheet found in Publication 4681. You calculate the fair market value of all your assets and subtract all your liabilities immediately before the debt was canceled. You keep this worksheet for your records.

😨 Does a 1099-c mean I owe money?

Not necessarily. Receiving the form just means the creditor reported the forgiven amount to the IRS. Whether you owe money depends entirely on whether you qualify for an exclusion, such as the insolvency exclusion, when you file your taxes.

🗑️ Can I ignore a 1099-c from a debt collector?

No. The IRS receives a copy of the 1099-C. If you ignore it and fail to include it on your tax return with the appropriate Form 982 exclusion, the IRS automated system may adjust your return and send you a tax bill with penalties.

❓ What happens if a debt collector doesn’t send a 1099-c?

If less than $600 was forgiven, they are not legally required to issue the form. However, if more than $600 was forgiven and the form never arrives, the IRS still considers the canceled amount as income. You do not need the physical 1099-C to claim the insolvency exclusion; you can use your final settlement letter and proof of payment to show the canceled amount and file your Form 982 accordingly.

🏢 Do I owe taxes if my debt was sold to a collection agency?

Selling a debt is not the same as forgiving it. You do not owe taxes when a debt is sold because you still owe the balance. You only face potential tax consequences if the collection agency eventually settles the debt for less than you owe.

🏦 Does credit counseling trigger a 1099-c?

No. In a nonprofit Debt Management Plan (credit counseling), you repay 100% of the principal balance at a reduced interest rate. Because no principal is forgiven, no 1099-C is issued and there are no tax consequences.

⏳ How long after settlement does the 1099-c arrive?

Creditors are required to mail the 1099-C by January 31st of the year following the year the settlement was finalized. For example, if you settled an account in August, you will receive the form in January of the next year.

📉 Will a 1099-c affect my credit score?

The 1099-C itself is a tax document and does not appear on your credit report. However, the settlement that triggered the 1099-C will be reported as “settled for less than full balance,” which does have a negative impact on your credit score.

Relief options exist alongside the collection process. These explain both sides.

- The options for resolving debt outside of continued collection

- How Long Does Debt Settlement Take: The Realistic 2-4 Year Timeline and What Affects It

- How to Pay Off Credit Card Debt: A Working Plan Based on What You Can Actually Afford

- What Debts Can Be Settled or Included in a Debt Relief Program - and What Can't

- Debt Settlement vs Credit Counseling: Two Very Different Programs for Two Very Different Situations

Some of these have deadlines attached. Start here if something is already happening.

- What collectors can legally do to you while a settlement program is running

- How to handle a lawsuit on a debt you are actively trying to settle

- What happens to a garnishment order when debt relief is in progress

- How bank levies interact with the debt you are trying to resolve

- How professional settlement programs work and what they actually cost

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.