- Debt settlement and credit counseling are not interchangeable; they are designed for two entirely different levels of financial hardship.

- Credit counseling (Debt Management Plans) requires you to pay the full principal balance, but at a significantly reduced interest rate negotiated by a nonprofit agency.

- Debt settlement involves stopping your payments entirely so a for-profit company can negotiate a discounted lump-sum payoff.

- If you can still afford a reduced monthly payment without defaulting, a DMP is usually the safer route. If making any payment at all is mathematically impossible, debt settlement may be necessary.

- Debt settlement carries a high risk of severe credit damage and collection lawsuits, whereas credit counseling leaves a minimal mark on your credit report.

The Danger of Confusing Two Very Different Paths

When you are overwhelmed by unsecured debt, the terminology starts to blend together. You see advertisements promising to “reduce your debt” or “help you manage your payments,” and it is easy to assume that debt settlement and credit counseling are just two versions of the same service. They are not. They operate on fundamentally different models, are designed for completely different financial situations, and produce drastically different outcomes for your credit and your wallet.

In my years working inside third-party collection agencies, I saw the fallout of consumers choosing the wrong path. I reviewed accounts where consumers who could have easily completed a quiet, manageable credit counseling program instead chose a settlement program that tanked their credit and resulted in lawsuits. I also saw the reverse: people barely scraping by who enrolled in credit counseling, inevitably missed their payments, and ended up in collections anyway because they never actually had the cash flow to support the plan.

Choosing the wrong program does not just waste time; it can cost you years of financial progress and thousands of dollars in fees or judgments. To make the right decision, you have to strip away the marketing language and look at the brutal math of your specific hardship level. Your budget, not a sales pitch, dictates which of these paths is actually viable for you.

The Ground-Up Difference: How Each Program Operates

To understand which program fits your life, you have to understand exactly what happens to your money and your accounts once you sign the enrollment paperwork. The difference comes down to whether you are paying the full principal you borrowed, or trying to force the creditor to accept less.

How Nonprofit Credit Counseling (DMP) Works

Credit counseling is almost always administered through a Debt Management Plan (DMP) managed by a nonprofit agency. When you enroll in a DMP, you are agreeing to pay back 100% of the principal balance you owe. You do not get a discount on the actual debt.

What you do get is a massive reduction in interest rates. Nonprofit agencies have pre-existing concession agreements with major credit card issuers. If you are paying 24% to 29% in interest right now, the agency can often negotiate that rate down to anywhere from 0% to 8%. You make one single monthly payment to the nonprofit agency, and they disburse that money to your creditors based on the negotiated schedule. Because the crippling interest rates are neutralized, your monthly payment actually goes toward reducing the principal, allowing you to become debt-free in typically three to five years.

How For-Profit Debt Settlement Works

Debt settlement is entirely different. It is typically managed by for-profit companies, and the goal is to pay less than the full balance owed. To get a creditor to accept a reduced lump sum, the creditor has to believe that you are incapable of paying the full amount. Therefore, when you enroll in a debt settlement program, the very first step is usually to stop paying your creditors entirely.

Instead of paying your credit card companies, you make a monthly deposit into an FDIC-insured escrow account in your name. As months pass, your accounts fall deeper into default, late fees pile up, and your credit score plummets. Once enough money has accumulated in your escrow account, and your accounts are severely delinquent (usually 6 to 18 months in), the settlement company approaches your creditors and offers a lump sum from your accumulated funds to settle the account for good.

“From the collector’s side, we always knew when an account was in a settlement program. The payments would stop abruptly, and months later, a third-party authorization would hit our desk. We rarely settled early on. We waited until the account was deeply delinquent because that is when our internal guidelines allowed for the biggest discounts. That waiting period is the hardest part for the consumer to endure.”

The Eligibility Filter: Which Path Matches Your Hardship?

Most comparison pages present these two options as a matter of preference. In reality, it is a matter of financial capability. You do not pick the one you like better; you pick the one your budget allows. The defining filter is your level of hardship.

Who Fits the Debt Management Plan?

A DMP is designed for consumers who are experiencing hardship but still have a steady income and a workable budget surplus. You might be falling behind on minimum payments, but if you look at your budget, you could afford to dedicate a consistent $200 to $600 a month strictly toward your debt.

If you can afford to make a reduced, consolidated monthly payment without fail, a DMP is almost always the better option. It protects you from severe credit damage and keeps the aggressive collection tactics at bay. However, if your budget is already negative and you cannot commit to a steady monthly payment for the next four years, a DMP will fail. Missing a payment in a DMP often causes the creditors to revoke the low interest rates and boot you from the program.

Who Fits Debt Settlement?

Debt settlement is for consumers whose financial situation has broken down to the point where making any meaningful payment to creditors is impossible. If the minimum payments on your credit cards exceed your ability to pay, and you are already defaulting or on the verge of defaulting, settlement is the emergency brake.

This path is appropriate when the alternative is likely bankruptcy. It is for readers who have significant unsecured debt (usually over $10,000) and cannot realistically foresee a way to pay off the principal, let alone the interest.

Enrolling in a settlement program because the sales rep quoted a $250 per month escrow deposit versus a $450 per month DMP payment. If you actually have $500 in monthly surplus, taking the settlement path needlessly destroys your credit for a discount you did not strictly need.

Running a brutal audit of your living expenses. If your true monthly surplus is $50, you cannot survive a DMP. Settlement becomes the mathematically necessary choice, regardless of the credit damage it causes.

The Mixed Debt Scenario

Reality is rarely this clean-cut. Many consumers have a mix of debt, such as a personal loan they can keep current, but high-balance credit cards they cannot. You do not have to put every single account you own into one program. A common real-world strategy is hybrid: you maintain direct payments on the accounts you must keep or can afford, and only enroll the unmanageable unsecured debts into a program. If you find your credit is still above 650 during this audit, you might even bypass these programs entirely and explore debt consolidation loans or balance transfers.

Fee Comparison: What You Actually Pay

Neither path is free, but the way you are charged could not be more different. As a former collector, I often saw consumers shocked by the final settlement math – the company’s fee had never been part of their mental calculation.

The Cost of a Debt Management Plan

Because DMPs are administered by nonprofit credit counseling agencies, the fees are strictly regulated and generally very low. You will typically pay a one-time setup fee ranging from $0 to $50. After that, you pay a monthly maintenance fee, which usually ranges from $25 to $75. In many states, these fees are capped by law.

If you are in a 48-month program paying $50 a month in fees, the total cost for the agency’s service is roughly $2,400. However, because they are dropping your interest rates from 25% down to perhaps 5%, the thousands of dollars in interest savings over those four years easily justify the administrative cost.

The Cost of Debt Settlement

Debt settlement is a for-profit industry, and the fees are substantial. Settlement companies typically charge between 15% and 25% of the total enrolled debt. Under federal law, they cannot charge you this fee upfront. The fee is only earned after a specific debt is successfully negotiated and you make a payment toward that settlement.

Consider a scenario where you enroll $20,000 in credit card debt. If the company charges a 20% fee, their cut will be $4,000. If they successfully settle your $20,000 debt for $10,000, you will pay the $10,000 to the creditors, plus the $4,000 to the settlement company, bringing your total out-of-pocket cost to $14,000. You still save $6,000 compared to the original principal, but the fee is a heavy piece of the pie.

The Credit Impact and the Hidden Lawsuit Risk

The financial cost is only one side of the ledger. The other side is the collateral damage to your credit profile and your legal exposure during the process. This is where the divergence between the two programs becomes extreme.

Credit Counseling: Minimal Damage, Zero Lawsuits

When you enter a DMP, your creditors will typically require you to close the enrolled credit card accounts. This causes an immediate, moderate drop in your credit score due to the sudden shift in your available credit utilization. However, because you continue making on-time payments every month, your payment history remains intact. Over the life of the program, most consumers actually see their credit scores steadily improve as the balances decrease. Furthermore, because you are honoring the modified agreement, the risk of a creditor suing you is virtually zero.

Debt Settlement: Severe Damage and High Legal Exposure

The damage from debt settlement is immediate and long-lasting. Your report will show strings of missed payments, charge-offs, and accounts turned over to collections. When a settlement is finally reached, the account will be marked as “Settled for less than the full balance,” a negative mark that remains on your report for seven years.

More importantly, stopping payments exposes you to the single biggest risk in the debt relief world: litigation. While you are sitting in phase one of a settlement program accumulating funds in your escrow account, your original creditors are watching you default.

“A hard truth from inside the agency: not every creditor settles gracefully. If you owed a large balance to a particularly aggressive bank, and you stopped paying to fund an escrow account, our system flagged you for litigation. We didn’t always wait for your settlement offer; we filed a lawsuit. Consumers were often blindsided because they assumed their program provided a legal shield.”

This pressure cooker of collection calls and lawsuit threats is exactly why the drop-out rate for debt settlement programs is notoriously high. If you panic and abandon the program halfway through, you are left with destroyed credit, accumulated late fees, and no settlements. If a lawsuit does escalate, understanding your options becomes critical, which is why we extensively cover how to handle collection litigation in our other guides.

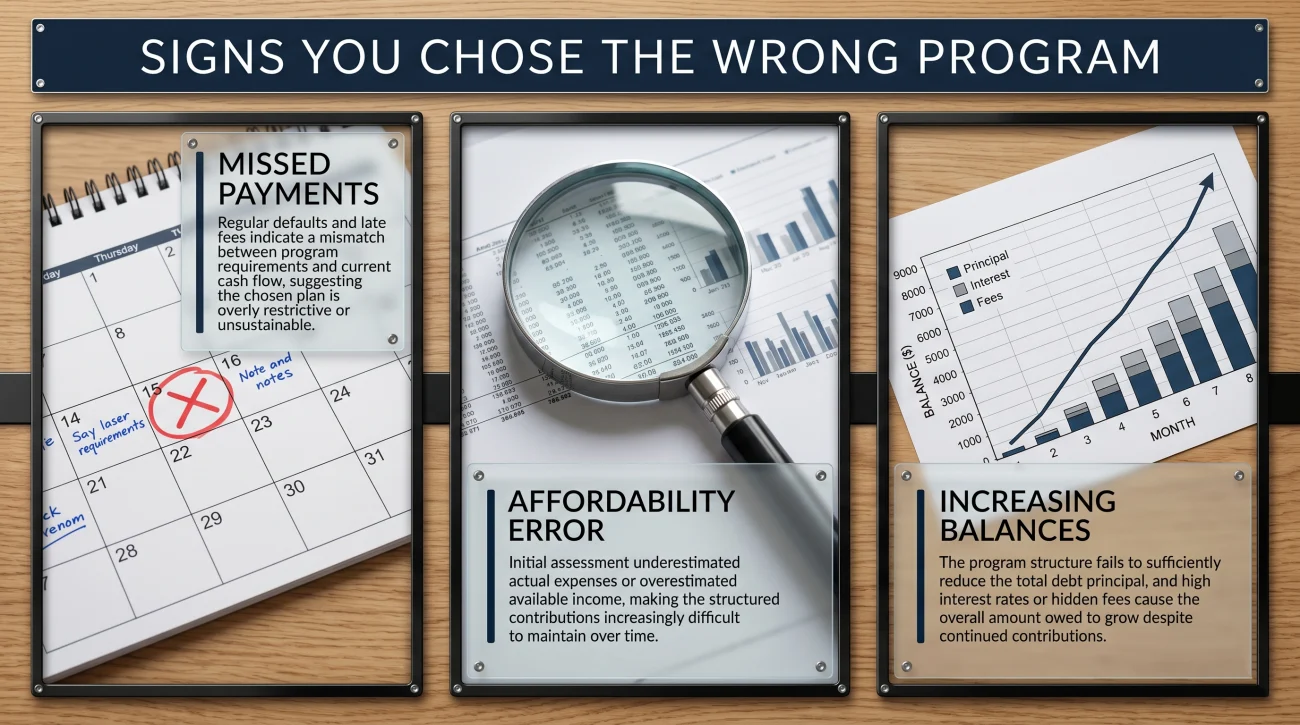

Signs You Chose the Wrong Program for Your Situation

It is unfortunately common for consumers to enroll in a program only to realize months later that the mechanics do not match their reality. If you are currently in a program, or about to sign paperwork, evaluate your situation against these red flags.

- ❌ You are in a DMP, but missing payments: If your budget is too tight to manage the monthly DMP payment, the program will fail. Your creditors will revoke the low interest rates, and you will be back where you started. This is the clearest sign that you need to evaluate settlement options.

- ❌ You are in debt settlement, but you could have afforded a DMP: If you enrolled in settlement just to get a “discount” but actually had the income to support a DMP payment, you made a critical error. You traded a temporary financial struggle for long-term credit destruction and lawsuit risks you could have avoided.

- ⚠️ Your debt balances are increasing during settlement: During the first year of settlement, while you are not paying, creditors continue to add late fees and penalty interest. This is mathematically normal for the process, but if you do not understand why it is happening, the anxiety often causes premature dropouts, leaving you with destroyed credit and no resolved debts.

How to Vet the Right Partner

Once you know which path aligns with your hardship level, you have to find a legitimate organization to facilitate the process. This is where you must act defensively.

Vetting a Credit Counselor

If the DMP path fits your budget, your search should start and end with nonprofit agencies found through the National Foundation for Credit Counseling (NFCC) directory. The initial consultation should be completely free.

💡 Pro Tip: Before committing, ask the counselor explicitly: “Can you confirm that all of my major credit card issuers have concession agreements with your agency?” Most do, but you must ensure your largest debts will actually receive the interest rate reduction.

Vetting a Debt Settlement Company

If settlement is your only viable path, avoiding scams becomes your primary job. The baseline rule is the FTC’s Telemarketing Sales Rule: a debt settlement company cannot legally charge you any fees until they have successfully settled a debt and you have agreed to it. If they ask for an “upfront fee” or “retainer,” hang up.

But verifying they are legitimate is just the baseline. You need to know if they are competent. From watching these negotiations from the creditor side, I can tell you that the questions separating experienced companies from inexperienced ones are purely tactical. When interviewing a settlement company, ask these three specific questions:

- “What is your historical completion rate?” (A legitimate company will be honest about the reality of program dropouts).

- “How do you handle aggressive creditors who are known to sue rather than settle?”

- “Are there any specific creditors in my portfolio that you historically struggle to negotiate with?”

Look for accreditation from the American Association for Debt Resolution (AADR, formerly AFCC) and ensure they are transparent about the lawsuit risks. Taking the time to understand vetting debt settlement providers will protect your escrow funds.

Final Thoughts: The Threshold Before Bankruptcy

Both credit counseling and debt settlement are essentially tools designed to keep you out of bankruptcy court. But they are not magic. They require specific financial conditions to work.

If you cannot afford a DMP payment, and your debt is so massive that you could never fund a settlement escrow account fast enough to outrun the inevitable lawsuits, you have crossed a critical threshold. At that point, Chapter 7 bankruptcy might actually be the most responsible, clean-slate financial decision you can make. Do not let the stigma of bankruptcy push you into a settlement program that is mathematically doomed from day one. Run your budget, look at the reality of your cash flow, and choose the path that actually solves the problem.

❓ FAQ

📉 Does credit counseling ruin my credit score?

No. While your score may take a small initial dip because your credit cards are closed (affecting your credit utilization), continuing to make on-time payments through the DMP usually results in your credit score improving over the 3 to 5 years of the program.

⚖️ Can I be sued while in a debt settlement program?

Yes. Because debt settlement requires you to stop paying your creditors, your accounts will go into default. Aggressive original creditors or debt buyers may choose to file a lawsuit against you to secure a judgment before a settlement is ever reached.

💳 Can I keep one credit card open if I enroll in a DMP?

Usually, no. Creditors agree to drastically lower your interest rates under the strict condition that you close your existing accounts and do not take on new debt while you are in the repayment program.

💰 Do I have to pay taxes on forgiven debt in a settlement?

You might. The IRS considers forgiven debt over $600 as taxable income. However, if you can prove you were “insolvent” (your total debts exceeded your total assets) at the time the debt was settled, you can often exclude that amount from your taxes using IRS Form 982.

⏱️ Which program gets me out of debt faster?

Debt settlement is often slightly faster, typically taking 24 to 48 months, depending on how quickly you can fund your escrow account. A Debt Management Plan (DMP) generally takes 36 to 60 months to fully pay off the principal.

🛑 Can a debt settlement company stop collectors from calling?

Not entirely. While you can direct third-party debt collectors to speak with your settlement company, original creditors (like the bank that issued your card) are not bound by the same communication rules and may continue to contact you while you are in default.

🏠 Can I include my car loan or mortgage in these programs?

No. Both credit counseling and debt settlement are designed almost exclusively for unsecured debt, such as credit cards, medical bills, and personal loans. Secured debts tied to collateral cannot be included.

🤝 If I have a co-signer, will debt settlement affect them?

Yes, severely. If you enroll a co-signed account into a debt settlement program and stop making payments, the co-signer’s credit will be equally damaged by the defaults. Collectors will aggressively pursue them for the full balance. Never include a co-signed debt in a settlement without their explicit consent.

💸 What are the upfront fees for debt settlement?

There should be absolutely zero upfront fees. Under the FTC’s Telemarketing Sales Rule, it is illegal for a debt settlement company to charge you any fees until they have successfully negotiated a settlement and you have agreed to the terms.

🏦 Do creditors have to accept a debt management plan?

No, participation is voluntary for creditors. However, almost all major credit card issuers have established, pre-negotiated concession agreements with accredited nonprofit credit counseling agencies and will accept the plan if you qualify.

Relief options exist alongside the collection process. These explain both sides.

- The options for resolving debt outside of continued collection

- How to Negotiate Debt Yourself: Hardship Programs and Settlements

- Balance Transfer Cards for Debt: The 0% APR Strategy

- How Long Does Debt Settlement Take: The Realistic 2-4 Year Timeline and What Affects It

- How Debt Settlement Actually Works: What Happens from Enrollment to Final Settlement

Some of these have deadlines attached. Start here if something is already happening.

- What collectors can legally do to you while a settlement program is running

- How to handle a lawsuit on a debt you are actively trying to settle

- What happens to a garnishment order when debt relief is in progress

- How bank levies interact with the debt you are trying to resolve

- How professional settlement programs work and what they actually cost

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.