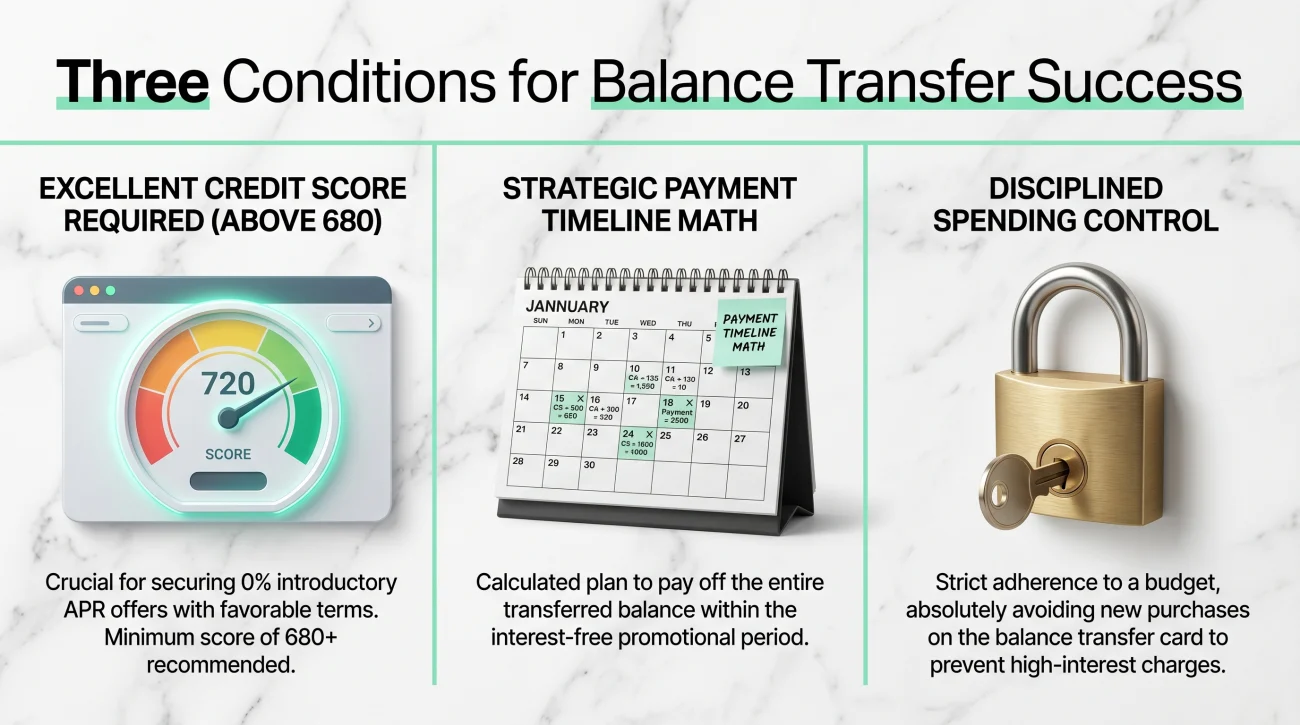

- A zero percent intro APR balance transfer is a powerful payoff tool, but it only works if you have good credit, disciplined spending habits, and the cash flow to clear the balance before the promo ends.

- Transfer fees typically consume three to five percent of your transferred balance upfront, meaning a ten thousand dollar transfer will cost you up to five hundred dollars on day one.

- When the introductory period expires, the remaining balance is immediately hit with a standard variable APR, which often ranges from twenty to twenty eight percent.

- If your credit score is below 650 or you cannot mathematically pay off the total debt within the 12 to 21 month promotional window, this strategy will likely trap you in a worse financial position.

The Zero Percent Strategy: A Precision Tool, Not a Magic Wand

During my years working inside collection agencies, I reviewed thousands of defaulted accounts to understand how the consumer got into trouble. I consistently saw one specific pattern that created some of the largest debt loads. A consumer would open a balance transfer credit card, move all their high interest debt to a zero percent introductory rate, and feel an immediate sense of relief. The pressure was off. But because they treated the transfer as a solution rather than a strict timeline, the promotional period expired before they paid off the principal. Suddenly, they were hit with a massive interest rate on the remaining balance, and they had usually started spending on their old, cleared cards again.

A zero percent intro APR balance transfer is arguably the most powerful debt payoff tool available to consumers today, allowing you to pause the brutal mathematics of compound interest. But it is a precision tool, not a magic wand. Credit card issuers market these heavily because they know the statistics. They know a massive percentage of people will fail to clear the balance before the clock runs out. If you lack the exact conditions required for success, the math will turn against you.

The Three Mandatory Conditions for Success

Most personal finance advice presents a balance transfer as a universal good. The reality on the ground is very different. For a balance transfer to actually get you out of debt, three highly specific conditions must all be true at the same time. If any single condition is missing, this approach usually fails.

First, you must have a credit score above 680. Zero percent introductory offers are reserved for consumers with good to excellent credit. If you have already missed payments, defaulted on other accounts, or have a highly elevated credit utilization ratio that has dragged your score below 650, you will likely be denied. Even if you are approved with a lower score, the bank may give you a credit limit of one thousand dollars, which is useless if you are trying to transfer ten thousand dollars of debt.

Second, you must have the mathematical ability to pay off the transferred balance before the introductory period ends. These promotional windows typically last between 12 and 21 months. This is a strict deadline. You must divide your total balance by the number of months in your promotional window to find your required monthly payment. If your budget cannot accommodate that specific monthly payment, you are planning to fail from the start.

Third, you must have the discipline to completely freeze new spending. This is where the psychological trap springs shut. Moving your debt to a new card means your old credit cards suddenly show a zero balance. The available credit looks tempting.

“In the collection industry, we categorized accounts by how they failed. The ‘double exposure’ profile was common. We loved seeing a defaulted balance transfer card alongside a maxed out original card. It told us the consumer tried to reorganize their debt but failed the spending discipline test, leaving them with twice the exposure they originally had.”

How to Evaluate and Choose the Right Offer

If you meet the three conditions, your next step is picking the right card. Do not simply click on the first zero percent offer you see. The details buried in the fine print will dictate whether the transfer is mathematically viable.

Look at the transfer fee first. A card offering 21 months at zero percent but charging a five percent transfer fee might actually cost you more upfront than a card offering 15 months with a three percent fee. Calculate the dollar amount of that fee based on your specific debt load.

Next, verify the standard APR that applies after the promotional period. If the bank is going to hit you with a 28 percent rate on day one after the promo expires, you are taking on a massive risk if your payoff plan hits a speed bump. Finally, read the terms carefully to ensure there is no deferred interest clause. True balance transfer cards do not retroactively charge you interest on the original balance if you miss the deadline, but you must confirm this in writing before applying.

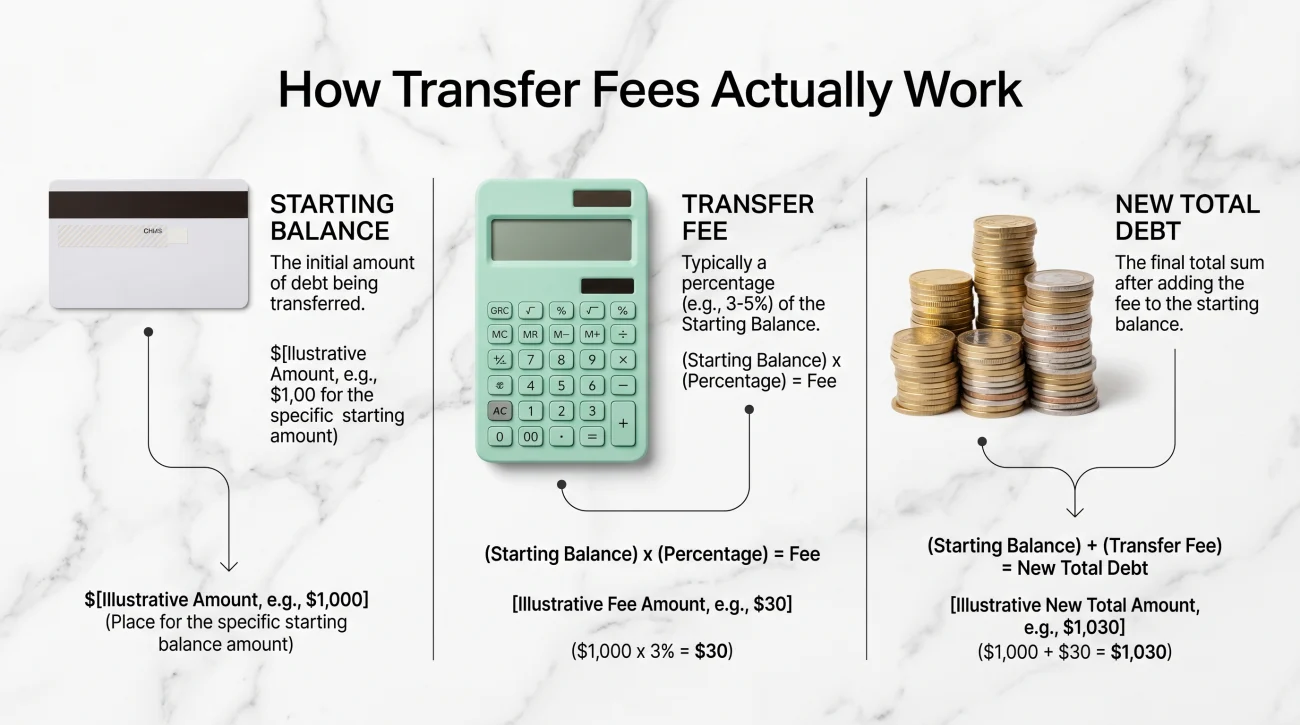

How the Transfer Mechanics and Fees Actually Work

The mechanics of transferring a balance are straightforward, but the underlying costs require close attention. Once you are approved for a new balance transfer card, you provide the issuer with the account numbers and balances of the high interest cards you want to clear. The new bank pays off your old banks directly. The debt does not disappear. It is simply moved to the new account under a new set of rules.

This service is rarely free. Almost all balance transfer cards charge an upfront balance transfer fee. This fee is added to your new principal balance immediately. Many consumers ignore this fee because they do not have to write a check for it, but it represents a real cost that you must pay back.

If you transfer $10,000 to a new card with a 5 percent balance transfer fee, the bank adds $500 to your balance on day one.

Your new starting balance is $10,500.

If your promotional period is 15 months, your required monthly payment to reach zero is exactly $700 per month ($10,500 divided by 15).

When I reviewed accounts for collection agencies, I could always tell exactly who failed to factor in the transfer fee. They would reach the end of their promotional period with exactly five hundred or six hundred dollars remaining. They paid down the original balance perfectly, but forgot the fee. That remaining balance was instantly hit with a high variable APR.

The Partial Transfer Problem: When the Limit Is Too Low

One of the most frustrating realities of this strategy is that you do not know your credit limit until after you apply and trigger the hard inquiry. It is incredibly common to apply with the intention of transferring fifteen thousand dollars of debt, only to be approved for an eight thousand dollar limit.

If you face a partial transfer scenario, you must be strategic. Transfer the debt with the highest interest rate first to maximize your savings. For example, if you have a store card at 29 percent and a standard credit card at 22 percent, move the store card balance over.

Once the transfer is complete, you now have a zero percent balance on the new card and a remaining balance on your old cards. The correct mathematical approach is to pay only the minimum required payment on the zero percent card, and redirect every extra dollar you have toward the remaining high interest balances. This is a modified version of the avalanche method, and it prevents the old cards from continuing to bleed your budget dry.

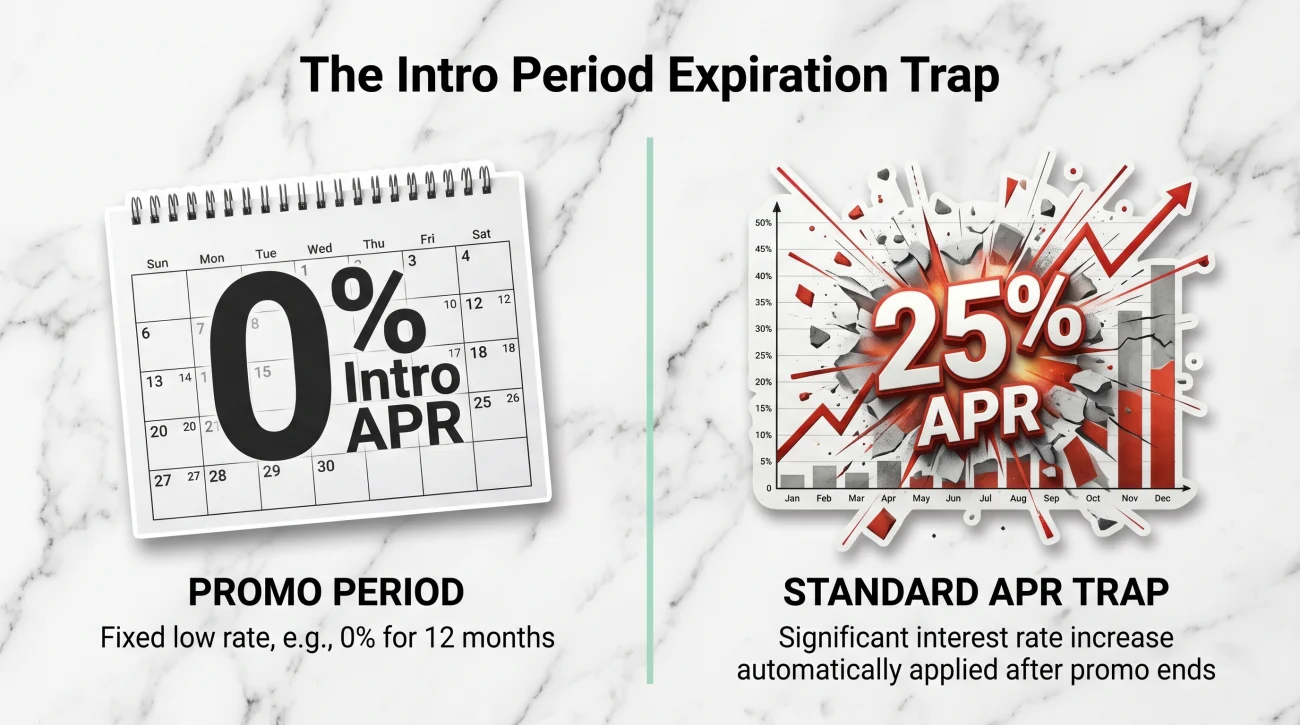

The Intro Period Expiration Trap

The business model of a balance transfer card relies on the fact that human beings are terrible at predicting their future behavior. The bank is betting against your discipline. They offer you 15 months of free financing because their data shows a massive portion of consumers will fail to clear the balance in that time. When that failure happens, the trap closes.

Imagine it is day 22 of month 16. Your 15 month promotional window has just closed. You started with ten thousand dollars, and because life got expensive, you only managed to pay it down to four thousand dollars. On day 22, the interest rate on that remaining four thousand dollars immediately rockets from zero percent to the standard variable APR, which is often between 20 and 28 percent.

You are no longer making progress. The heavy headwind of compound interest has returned, and your manageable monthly payment has suddenly transformed into a debt treadmill. The sudden shock of a 25 percent APR on a large remaining balance is often enough to derail a consumer’s financial stability.

Calculating your budget based on the minimum payment the credit card company requires during the zero percent period. This guarantees a large remaining balance when the promotion ends.

Dividing the total balance (including the transfer fee) by the number of months in the promotional window. Setting this specific amount as an automated monthly payment that cannot be skipped.

The Midpoint Rescue Plan

If you realize halfway through the promotional period that you are going to fall short, you must adjust your strategy immediately. Do not wait for the expiration date to surprise you. Hoping for a sudden windfall is not a financial strategy.

If you are at month eight of a fifteen month promotion and tracking behind, execute a rescue plan immediately. First, recalculate the exact math gap. Determine how much extra you need per month to hit the deadline. Second, decide whether you will solve the gap by cutting expenses drastically or by taking on a temporary side income specifically dedicated to that shortfall. Every dollar earned goes straight to the principal.

Third, if you run the numbers and realize the remaining balance will be mathematically impossible to clear before the rate skyrockets, you need to look at creating a more structured, long term strategy. It is better to begin researching alternatives like a Debt Management Plan while you are still at zero percent, rather than waiting until your monthly payment doubles and you start missing due dates.

The Hidden Impact on Your Credit Score

Consumers often worry that transferring balances will destroy their credit score. The reality is more nuanced. Moving debt around changes the metrics the credit bureaus use to evaluate your risk profile, and the impact usually happens in three distinct phases.

First, applying for the new card generates a hard inquiry on your credit report. This will cause a small, temporary dip in your score, usually around five to ten points. This dip is brief and recovers quickly as long as you make your payments on time.

Second, a temporary utilization spike occurs. Once the transfer goes through, your new credit card might be maxed out. For example, if you are approved for a ten thousand dollar limit and you transfer ten thousand dollars, that specific card is at 100 percent utilization. Credit scoring models view maxed out individual cards as a high risk indicator, which can suppress your score in the short term.

Third, the overall utilization benefit takes effect. As the old cards report zero balances and you begin aggressively paying down the new card, your overall credit utilization ratio across all your accounts drops. Because you now have more total available credit and you are lowering the principal balance every month, your credit score will typically see a net positive increase over the course of the promotional period. The key is that you must actually pay the debt down.

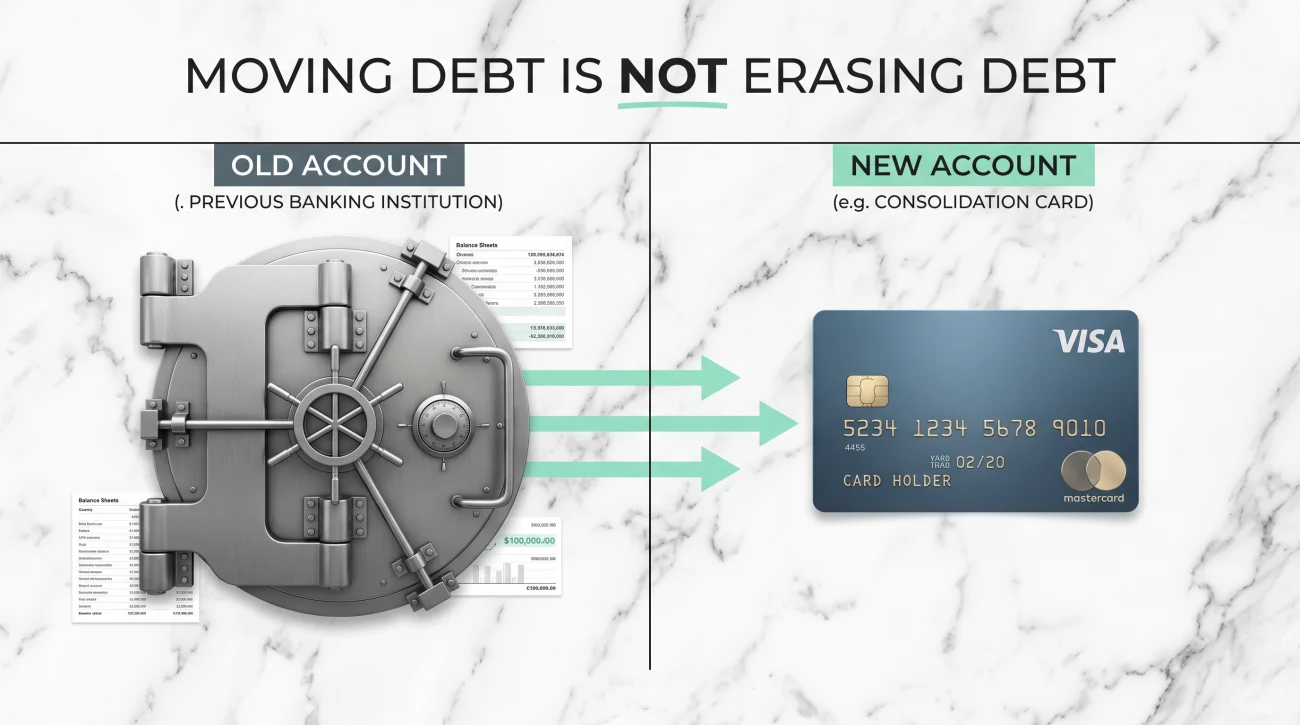

Moving Debt Is Not Erasing Debt

One of the most dangerous moments in a debt payoff journey is the day you log into your old credit card account and see a balance of zero. It feels like an accomplishment. It feels like you have erased the debt. You have not erased a single penny. You have simply moved the liability from one bank to another, and you paid a fee to do it.

If you want to succeed, you must treat the old, cleared accounts with extreme caution. Keeping the accounts open is generally good for your credit history length, but you must introduce friction to prevent yourself from using them.

- 📌 Remove the old credit cards from your physical wallet immediately. Out of sight creates a necessary physical barrier to impulse spending.

- 📌 Delete the saved card numbers from your web browser and apps. Mindless, one-click spending on Amazon or food delivery apps is what quietly rebuilds debt balances. Force yourself to type in a card number manually.

- 📌 Place a small, recurring subscription (like Netflix) on the old card. Set this single charge to autopay in full every month from your checking account. This keeps the credit card active in the eyes of the bank and the credit bureaus, without the risk of carrying a balance.

The Danger of Balance Transfer Stacking

When consumers fail to pay off the balance before the intro period expires, they often attempt to solve the problem by transferring the remaining debt to yet another zero percent card. This is known as balance transfer stacking, or serial transferring. It is a highly dangerous game of musical chairs.

Inside the agency, we called these consumers ‘jumpers.’ We would pull a credit report and see three different balance transfer accounts opened twelve months apart. It told us the consumer was just shuffling the deck chairs instead of paying the principal. Eventually, their debt to income ratio worsened, they ran out of banks willing to approve them, and the whole house of cards collapsed.

Stacking fails because the transfer fees compound. If you pay a five percent fee to move a balance, fail to pay it off, and then pay another five percent fee to move it again, you are effectively paying a ten percent penalty simply to hide the debt. Furthermore, each new card approval lowers your average account age and adds another hard inquiry. Eventually, your credit profile will look too risky, an application will be denied, and you will be trapped with the massive interest rate you were trying to outrun.

Comparing Balance Transfers to the Alternatives

A balance transfer is a DIY strategy for people with good credit and manageable debt loads. It is not the only option, and depending on your circumstances, it might be the wrong one. You must compare it against the alternatives before committing to a hard inquiry and a transfer fee.

If you have a large debt load that you cannot possibly pay off in 18 months, a balance transfer will only defer your pain. In this scenario, using a fixed rate personal loan to restructure what you owe is often a safer choice. A debt consolidation loan provides a fixed interest rate and a fixed payment schedule over three to five years. The interest rate will not be zero, but it will not suddenly explode to 25 percent at the end of a promotional period. It provides predictable, stable amortization.

If your credit score has already dropped below 650, you likely will not qualify for a balance transfer card or a low rate consolidation loan. In this case, a nonprofit Debt Management Plan (DMP) becomes a viable alternative. A credit counseling agency negotiates lower interest rates directly with your current creditors, allowing you to pay the principal off over a few years without taking out new credit.

If you are already falling behind on minimum payments and have no budget surplus to speak of, moving the debt to a new card will not solve the underlying cash flow problem. This is the point where you must consider more aggressive interventions.

Signs You Are on the Wrong Path

A balance transfer is designed to accelerate payoff, not act as a permanent hiding spot for money you cannot afford to repay. If you are struggling with your current debt, you need to evaluate whether moving it around is actually solving the root issue.

You are likely on the wrong path if your monthly interest charges across all your accounts exceed what you could realistically cut from your budget. If the math simply does not balance out, a temporary zero percent window will not create money out of thin air. You are also in the danger zone if you view a newly opened credit limit as a financial cushion rather than a strict reorganization tool.

When the math of DIY payoff breaks down, and your debt burden exceeds your ability to pay it down even at zero percent interest, it is time to stop applying for new credit. You need to look at options designed specifically for actual financial hardship. This means exploring the full spectrum of available paths out of debt. If you cannot make your minimum payments and multiple accounts are nearing default, your situation requires working with a professional program to negotiate your balances down rather than just moving them to a different bank.

Final Thoughts: The Expiration Date Is Absolute

A zero percent balance transfer strips away the excuse of high interest rates and forces you to confront the actual principal. The banks offer these promotions because they know human nature will usually fail to beat the clock. In the collection room, we saw the aftermath of those failures every day. Automate your payments, respect the expiration date, and close the gap, or you are simply paying a fee to delay the inevitable.

❓ FAQ

💳 What happens if I don’t pay off a balance transfer in time?

Once the promotional period ends, the remaining balance is subject to the card’s standard variable APR, which is often above 20 percent. This new, high interest rate is applied to whatever principal is left, making it much harder to pay off.

📉 Does a balance transfer hurt my credit score?

Initially, you will see a small dip due to the hard inquiry from the application. However, if you use the card to pay down debt without adding new purchases, your overall credit utilization ratio improves, which generally helps your score over time.

🏦 Can I transfer a balance between cards from the same bank?

No. Banks generally do not allow you to transfer debt between their own products. You must transfer the balance to a credit card issued by a completely different financial institution.

💸 Is the balance transfer fee worth it?

Yes, usually. Paying a one time fee of 3 to 5 percent is almost always cheaper than paying 20 to 25 percent in interest annually, provided you actually pay down the balance during the zero percent promotional period.

⏳ How long does it take for a balance transfer to process?

It typically takes between five and fourteen days for the new bank to send funds to your old bank. You must continue making minimum payments on your old card until you see the balance officially drop to zero to avoid late fees.

🚫 Can I use a balance transfer to pay off a personal loan?

Many credit card issuers allow you to transfer balances from personal loans, auto loans, or even use balance transfer checks to deposit cash into your checking account to pay off other debts. Check the specific terms of your offer.

🛑 Should I close my old credit card after transferring the balance?

No, it is usually better for your credit score to keep the old account open. Closing it reduces your total available credit, which spikes your utilization ratio. Keep it open but secure the card so you do not use it.

Relief options exist alongside the collection process. These explain both sides.

- The options for resolving debt outside of continued collection

- How to Negotiate Debt Yourself: Hardship Programs and Settlements

- How to Pay Off Credit Card Debt: A Working Plan Based on What You Can Actually Afford

- Debt Consolidation Loan: When It Saves Money and When It Doesn't

- Do You Owe Taxes on Settled Debt? The 1099-C, the Insolvency Exclusion, and What to Do

Some of these have deadlines attached. Start here if something is already happening.

- What collectors can legally do to you while a settlement program is running

- How to handle a lawsuit on a debt you are actively trying to settle

- What happens to a garnishment order when debt relief is in progress

- How bank levies interact with the debt you are trying to resolve

- How professional settlement programs work and what they actually cost

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.