- Your ability to successfully negotiate debt depends entirely on two factors: how many days delinquent the account is, and whether the original creditor or a debt buyer owns it.

- If you are current on your payments, do not ask for a settlement. You must ask for a hardship program, which typically involves temporary rate reductions or fee waivers to help you catch up.

- If your account is in default, debt buyers generally have much more flexibility than original creditors. Because they purchase debt for pennies on the dollar, they can often accept thirty to fifty percent of the balance and still make a profit.

- Never negotiate based on emotion. Collectors respond to facts, specifically the availability of immediate lump sum funds.

- Do not pay a single dollar toward a negotiated settlement until you have the complete agreement terms in writing. Verbal promises from collectors are non binding and routinely broken.

The Reality of DIY Debt Negotiation

During my years working inside collection agencies and for a national debt buyer, I listened to thousands of consumers try to negotiate their balances down over the phone. The consumers who failed almost always made the same fundamental mistake. They negotiated based on emotion, focusing on their personal hardship, job loss, or medical emergencies. They assumed the collector was making a moral judgment about whether they deserved a break.

The consumers who succeeded negotiated based on the collector’s internal math. They understood that the person on the other end of the line was looking at a computer screen that displayed a specific “settlement authority floor”, which is the absolute lowest number they were allowed to accept without a manager’s override. If you know how the system works, you can negotiate your own debt successfully without hiring a third party company.

Debt negotiation is a mechanical process. The exact strategy you use, and the percentage you can expect to save, depends entirely on where your account sits in the delinquency timeline. An original bank will treat you very differently on day 30 of a missed payment than a third party debt buyer will treat you on day 400. Before you pick up the phone, you must diagnose exactly where your leverage lies.

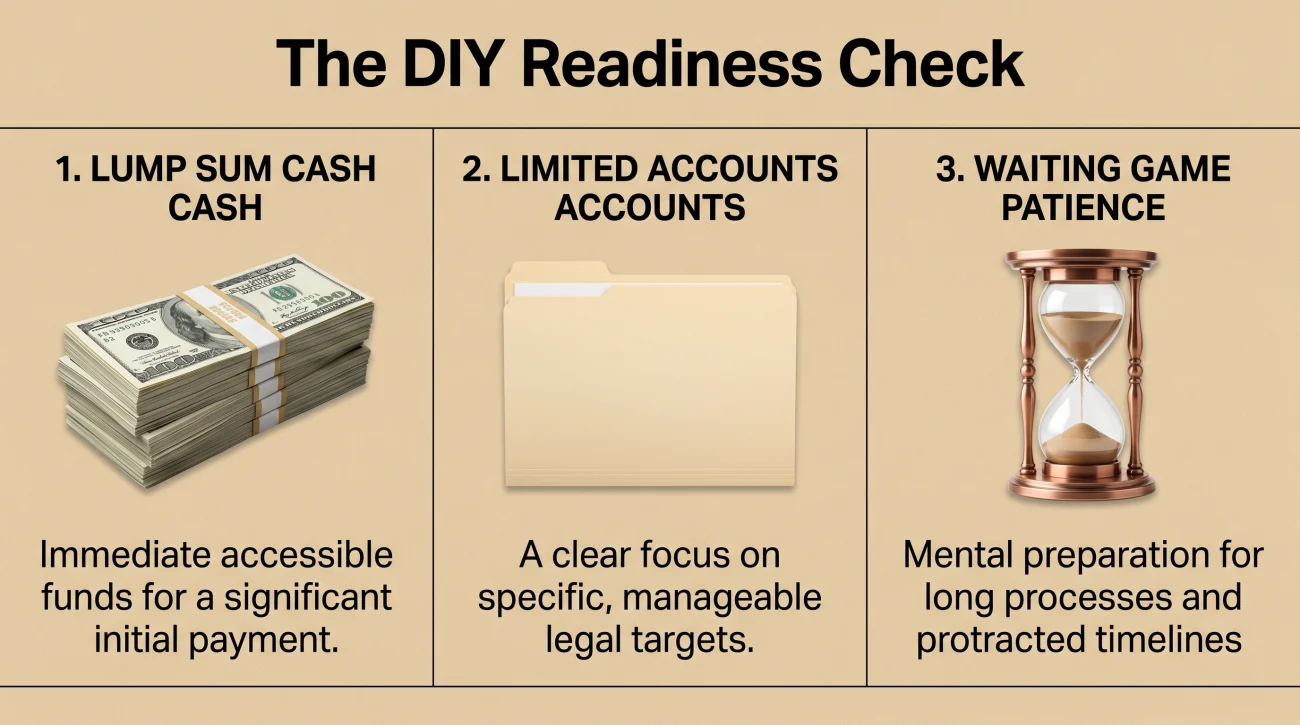

The DIY Readiness Check: Are You in the Right Position?

Negotiating your own debt is completely legal, but it is not the right path for everyone. It requires specific financial resources and a high tolerance for confrontation. Before you commit to the DIY route, you need to verify that your situation actually supports this strategy. Ask yourself these three core questions.

First, do you have access to a lump sum of cash right now? Professional negotiation relies heavily on the leverage of immediate funds. Without capital to offer upfront, your options are significantly limited.

Second, are you dealing with fewer than four accounts? Managing a single negotiation is straightforward. Juggling six different creditors, each at a different stage of delinquency, while fielding dozens of collection calls daily, quickly becomes a full time job. The complexity multiplies with every account you add.

Third, are you emotionally prepared to play a waiting game? Successful negotiation often requires letting an account sit in default until the creditor realizes you truly cannot pay the full amount. This means watching your credit score drop and enduring aggressive collection tactics. If the idea of this stress is overwhelming, or if you lack the cash to make lump sum offers, you need to explore the broader spectrum of available debt relief programs designed to handle the heavy lifting for you.

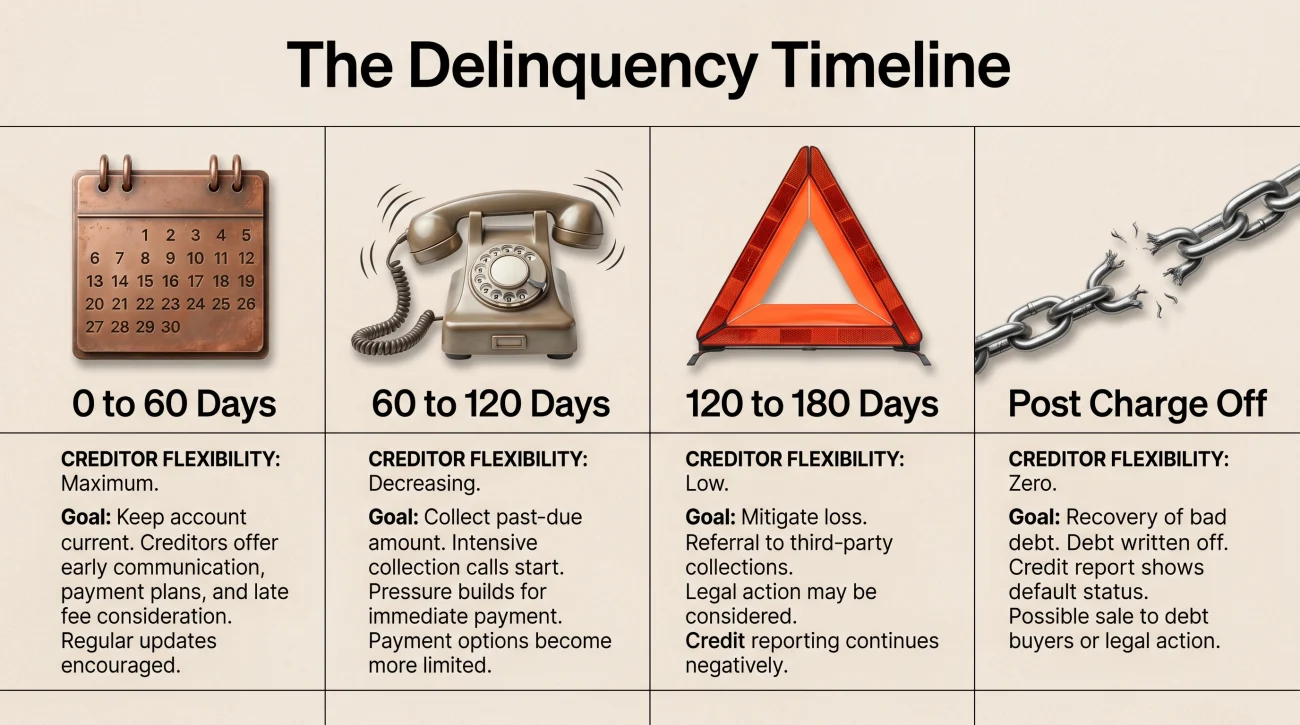

The Delinquency Timeline: Your Guide to Creditor Flexibility

The single biggest misconception about debt settlement is that every creditor operates by the same rules. They do not. A creditor’s willingness to accept less than what is owed is directly tied to the age of the debt and the internal accounting rules they must follow. The longer the debt goes unpaid, the more their leverage decreases and your leverage increases.

| Delinquency Stage | Account Owner | Expected Negotiation Target |

|---|---|---|

| 0 to 60 Days Late | Original Creditor | Hardship programs only (rate reductions, waivers). No principal reduction. |

| 60 to 120 Days Late | Original Creditor | Lump sum settlement becomes possible. Expect 50 to 70 percent of the balance. |

| 120 to 180 Days Late | Original Creditor | Maximum motivation before charge off. Often willing to accept 40 to 60 percent. |

| Post Charge Off | Debt Buyer / Collector | Highest flexibility. Often accept 25 to 50 percent, as they purchased the debt at a deep discount. |

You cannot call your credit card company when you are perfectly current on your payments and ask them to cut your balance in half. They have zero mathematical incentive to do so. If you are current, you must pursue the hardship path. If you are already deeply behind, you pursue the settlement path.

The Hardship Program Path: For Current Accounts

If you have not yet missed a payment but know you are about to fall off a financial cliff, you need to utilize internal hardship programs. Every major bank has a department dedicated to loss mitigation. Their entire job is to prevent accounts from defaulting.

To access these programs, call the customer service number on the back of your card. Do not speak to the frontline representative. Clearly state that you are experiencing financial hardship and request a transfer to the “hardship department” or “executive resolution team”.

“I am struggling to keep up with my payments. Can we settle this balance for half of what I owe so I can clear it out?” (Original creditors will not settle an account that is currently paying on time.)

“I have experienced a sudden financial hardship and I want to avoid defaulting on this account. I need to know what short term hardship programs, rate reductions, or payment deferrals you currently offer so I can maintain my good standing.”

If the representative asks for proof, be prepared to submit an unemployment letter or medical bill. If they claim no programs exist, politely ask to escalate to a supervisor. These programs are internal policies, so persistence and reaching the right department are mandatory. You are typically looking for a temporary reduction of your interest rate to zero percent for six to twelve months, a waiver of late fees, or a short term payment deferral.

⚠️ Warning: Enrolling in a bank’s internal hardship program usually results in the immediate closure or suspension of that credit card. You will not be able to make new purchases. The arrangement will be noted on your credit report, but this is vastly preferable to the severe credit damage caused by multiple missed payments.

However, if you are already past the hardship window and your account has fallen into default, the conversation changes entirely.

The Lump Sum Settlement Path: For Defaulted Accounts

If your account is already more than 90 days past due, the original creditor has begun reserving capital against your potential default, and they are deciding whether to sue you, sell your account to a debt buyer, or settle. If the account has already been sold to a debt buyer, they are operating on pure profit margin, as they likely bought your debt for less than ten cents on the dollar.

This is where lump sum settlement becomes your primary weapon. The strategy is built on the anchor principle. You must calculate the absolute maximum you can afford to pay in a single transaction. Once you have that number, you never open the negotiation with it. You must start significantly lower to give the collector room to counteroffer.

Field Note: “When I was on the floor, we loved when a consumer called in and immediately said, ‘I have two thousand dollars to settle this five thousand dollar debt.’ They showed their entire hand in the first ten seconds. My job was to say, ‘I can’t do two thousand, but my manager approved twenty five hundred.’ The consumer would then scramble to find the extra five hundred. If they had started by offering twelve hundred, we would have happily settled at their actual two thousand dollar target.”

If your target settlement is 40 percent of the total balance, your opening offer should be around 20 to 25 percent. Expect the collector to reject this immediately and counter with an offer of 70 percent. This is theater. Stay calm, reiterate that your funds are strictly limited, and slowly inch your offer up in small increments until you meet in the middle.

The Insider Secret: End of Month Timing

When I was managing collection floors, the energy in the room completely shifted during the last five days of the month. Collectors are driven by monthly commission quotas. A collector who is stubbornly holding out for a seventy percent settlement on the tenth of the month might eagerly accept a forty percent settlement on the twenty eighth just to hit their bonus tier.

Use this structural pressure to your advantage. Make your initial contact in the middle of the month to establish your low opening offer. When they reject it, tell them you will see if you can borrow a slightly higher amount and call back. Call them back between the twenty fifth and the thirtieth. Their flexibility will be at its absolute peak. Furthermore, the end of the calendar year (November and December) is historically the most favorable time to settle. Agencies are aggressively trying to clear their books, meet year-end bonus targets, and reset their bad-debt budgets before January. If you have cash in hand during the second week of December, your leverage is at its absolute maximum.

What to Say: The Negotiation Simulation

You do not need a word for word monologue, but you do need to know how to counter standard collection tactics. When I trained new collectors, we spent hours drilling specific rebuttals designed to break a consumer’s resolve. Your tone should remain flat, professional, and entirely detached from emotion. Here is how a standard back and forth should sound when you refuse to play their game.

You: “I am calling to resolve this account today. I have secured a one time lump sum of $1,500 borrowed from family. I am offering this to settle the $5,000 balance in full.”

Collector: “We cannot accept $1,500. The lowest my system allows is $3,500. If you can’t pay that, we can set up a payment plan.” (The standard first rejection)

You: “A payment plan is not an option for my budget. The $1,500 is what I have available today. If we cannot reach an agreement, I will have to allocate these funds to a different creditor.”

Collector: “Let me put you on hold and speak to my manager.” (Wait two minutes). “My manager authorized a one time drop to $2,800, but that offer expires at the end of the day.” (The false urgency tactic)

You: “I appreciate you checking. I cannot do $2,800. The absolute maximum I can pull together is $2,000, and I can authorize that payment as soon as I receive the settlement letter.”

Collector: (Silence for 10 seconds. The silence tactic designed to make you nervous).

You: (Remain completely silent. Do not fill the dead air).

Collector: “Okay, I will send the letter for $2,000.”

This exchange works because it neutralizes their primary weapons. You establish that your funds are strictly limited, and you take control of the urgency by threatening to pay a different creditor instead.

💡 Pro Tip: Debt Buyer vs. Original Creditor: The simulation above is typical for a third party debt buyer who cares strictly about the cash amount. If you are negotiating with an original creditor like your bank, they will often require you to answer questions about your income, employment status, and expenses before they will even entertain a settlement offer. Keep your answers brief and focused strictly on your financial hardship.

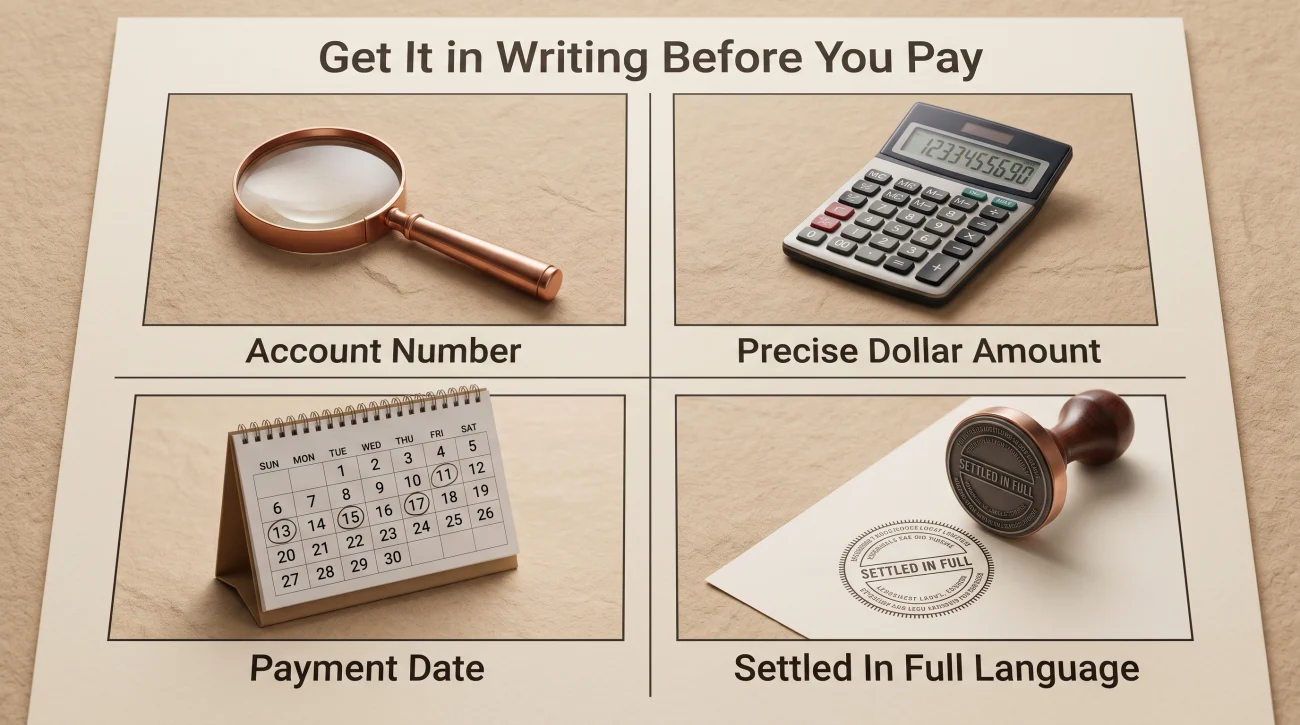

The Golden Rule: Get It in Writing Before You Pay

This is the most critical rule in the entire debt settlement process. If a collector agrees to settle your ten thousand dollar balance for four thousand dollars over the phone, that verbal agreement is completely worthless. In the agency, I saw countless accounts where a consumer paid a verbal settlement, only for the floor manager to pocket the money as a partial payment and immediately assign the remaining balance to a new collector desk. You must demand a formal settlement letter emailed or mailed to you.

Before you pay, confirm the letter explicitly contains:

1. Your exact account number and the name of the agency.

2. The precise dollar amount of the agreed settlement.

3. The exact date the payment must be received by.

4. Clear language stating that upon receipt of this payment, the account will be considered “settled in full” or “satisfied in full,” and no further collection attempts will be made.

If the collector claims they cannot send a letter until after you make a “good faith” payment, hang up the phone. It is a standard industry lie designed to extract funds without committing to the discount. Legitimate agencies generate settlement letters in seconds.

What to Do After the Settlement is Paid

Your responsibility does not end the moment the funds leave your account. The debt collection ecosystem is notoriously messy, and paid accounts are frequently sold to new buyers by mistake. To protect yourself, you must treat the settlement letter and the proof of payment (like a cleared bank statement) as permanent financial records. Never throw them away.

Wait forty five days after your payment clears, then pull your credit reports from all three bureaus. Verify that the account status has been officially updated to “Settled in full” or “Paid for less than the full balance,” and that the remaining balance shows as zero. If a new collection agency suddenly contacts you about the same debt a year later, do not panic and do not argue. Simply mail them a copy of the settlement letter and the cleared payment record, stating the debt was legally satisfied. That legally forces them to close the file.

The Hidden Cost: 1099-C Tax Consequences

When you successfully negotiate a debt down, the money you saved does not simply vanish. The IRS views forgiven debt as a form of income. If a creditor cancels $600 or more of your principal balance, they are legally required to report that forgiveness to the IRS and send you a Form 1099-C at the end of the tax year.

Many DIY negotiators are completely blindsided by this. They settle a massive credit card bill, celebrate the win, and then receive a tax bill the following spring. Fortunately, the IRS recognizes that consumers who negotiate debt are usually doing so because they are in deep financial distress, and they provide a specific exemption for this exact scenario.

There is a specific IRS rule called the insolvency exclusion. If your total debts exceeded the total fair market value of your assets at the exact moment the debt was forgiven, you can legally exclude the canceled amount from your taxable income. Because this exclusion saves consumers thousands of dollars, understanding how the 1099-C tax process actually works is a mandatory step before you finalize any large settlement.

Signs DIY Negotiation Is the Wrong Path for Your Situation

There is a distinct breaking point where managing your own debt transition moves from being a money saving strategy to a dangerous liability. Knowing when to stop trying to DIY and when to bring in structural help is the difference between resolving your debt and ending up in court.

If your situation matches any of the following diagnostics, the DIY path is likely failing you:

- Sign 1: You are facing active litigation. If you have been served with a court summons, the window for casual phone negotiation has closed. You are now dealing with the creditor’s legal department. This requires an immediate formal response, and you must shift your strategy toward defending a debt collection lawsuit before a default judgment is entered against you.

- Sign 2: You lack the capital for lump sum offers. If your plan is to ask a collector to accept 50 percent of the balance, but you need to pay that 50 percent over three years, you will be rejected. Settlement relies on the leverage of immediate cash. Without it, your offers have no weight.

- Sign 3: You have five or more delinquent accounts. The administrative burden of tracking settlement timelines, managing collection calls from multiple agencies, and timing your payments perfectly is massive. One missed deadline can void a settlement agreement entirely.

- Sign 4: Your original creditors refuse to negotiate. Some major banks have strict internal policies against settling with consumers directly, but maintain established back channel agreements with professional settlement companies.

- Sign 5: The psychological toll is paralyzing. If the constant ringing of the phone is affecting your employment, your health, or your family, the stress is costing you more than the fee a professional would charge.

When the complexity of your debt exceeds your ability to manage it manually, continuing to attempt DIY negotiation usually results in escalating balances and eventual lawsuits. If you lack the cash reserves or the emotional bandwidth to fight collectors on multiple fronts, your most logical next step is to evaluate what reputable debt settlement programs actually offer and transition the burden to a professional team. You can start by reviewing the highest rated debt settlement companies to understand their minimum requirements and fee structures.

Final Thoughts: Leverage Requires Patience

Negotiating your own debt is entirely an exercise in leverage. During my last year on the collection floor, I watched a consumer systematically negotiate a twenty thousand dollar balance down to six thousand simply by calling on the twenty ninth of the month, sticking strictly to their planned numbers, and refusing to speak over the awkward silence. They treated it like a cold business transaction, and the agency eventually folded.

Patience is your greatest asset. Collectors are paid on commission and face intense monthly quotas. If you remove emotion, treat the debt strictly as a math problem, and hold the line until you have a legally binding letter in your hand, you can successfully resolve your accounts for a fraction of what you owe.

❓ FAQ

🗣️ How do I start a negotiation with a debt collector?

Start by clearly stating you are experiencing extreme financial hardship and have a small, limited lump sum available to resolve the account today. Ask them what their lowest acceptable settlement figure is to close the file completely.

📉 What percentage should I offer to settle credit card debt?

If dealing with the original bank, an opening offer of 30 percent gives you room to settle between 50 and 60 percent. If dealing with a third party debt buyer, opening at 15 to 20 percent allows you to safely target a 30 to 40 percent final settlement.

🛑 Can a debt collector refuse to negotiate?

Yes. Creditors and collectors are under no legal obligation to accept less than the full balance owed. If they believe you have significant income or assets, they may refuse a settlement and choose to pursue a lawsuit instead.

📞 Should I talk to debt collectors on the phone?

If your goal is to negotiate a settlement, you generally must speak with them on the phone to execute the back and forth offers. However, keep the conversations strictly factual, record the date and time of the call, and demand all final agreements in writing.

⏱️ How long should I wait before offering a settlement?

The optimal window for original creditors is usually between 90 and 150 days past due, right before the debt is charged off. For debt buyers, wait until you have the cash in hand to make an immediate lump sum payment.

📝 What is a pay for delete agreement?

This is a negotiation tactic where you offer to pay the debt only if the collector agrees to completely remove the negative account from your credit report. While highly desirable, major banks and reputable collection agencies rarely agree to this practice anymore. If a collector does agree to a pay for delete, you absolutely must get that specific promise written into the formal settlement letter before you pay, as verbal promises to delete credit reporting are almost never honored.

🏦 Will a hardship program hurt my credit score?

Hardship programs are designed for accounts that are still current. While the bank will likely close the card to new purchases, preventing you from adding debt, the arrangement does far less damage to your score than simply missing payments and going into default.

📧 Is an email settlement letter legally binding?

Yes. An emailed settlement letter directly from the collection agency detailing the exact terms, your account number, and the required payment date is considered legally valid. Save a backup copy of the PDF immediately.

💳 Can I settle debt by making monthly payments?

Yes, but you will pay a steep premium. Collectors are highly resistant to term settlements because default rates are high. If you need 12 months to pay, they may only agree to drop the balance by 10 or 20 percent, compared to 50 percent for a lump sum.

⚖️ What happens if a collector breaks a settlement agreement?

If you have the agreement in writing and proof that the payment cleared your bank on time, the debt is legally satisfied. If they attempt to collect the remainder or sell it to another buyer, you have concrete proof of a Fair Debt Collection Practices Act violation.

Relief options exist alongside the collection process. These explain both sides.

- The options for resolving debt outside of continued collection

- Do You Owe Taxes on Settled Debt? The 1099-C, the Insolvency Exclusion, and What to Do

- Medical Debt Relief: How to Negotiate Hospital Bills, What the 2025 Rules Changed, and What Actually Gets Forgiven

- How Long Does Debt Settlement Take: The Realistic 2-4 Year Timeline and What Affects It

- How to Choose a Debt Settlement Company: What NDR, FDR, and ADR Actually Offer and the Red Flags to Avoid

Some of these have deadlines attached. Start here if something is already happening.

- What collectors can legally do to you while a settlement program is running

- How to handle a lawsuit on a debt you are actively trying to settle

- What happens to a garnishment order when debt relief is in progress

- How bank levies interact with the debt you are trying to resolve

- How professional settlement programs work and what they actually cost

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.