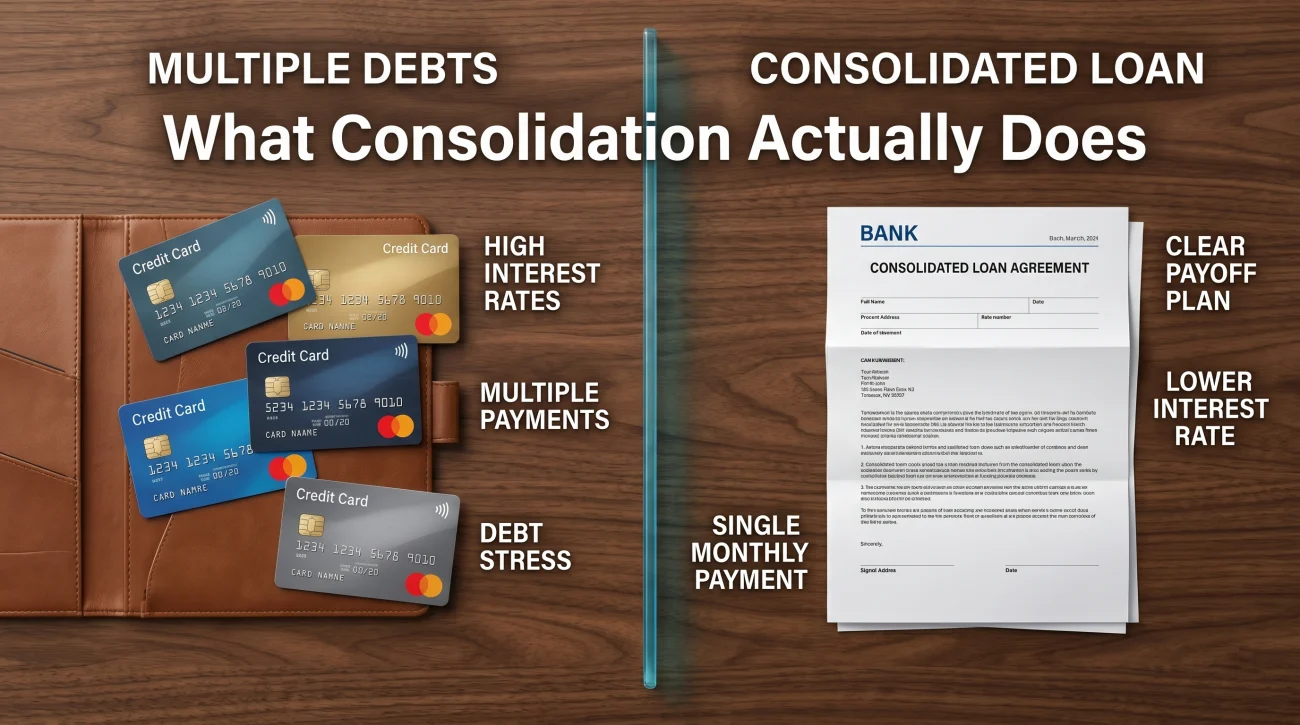

- A debt consolidation loan is a personal loan used to pay off multiple smaller debts, leaving you with one fixed monthly payment.

- It only saves you money if the new interest rate is mathematically lower than the weighted average of your current interest rates.

- Approval and interest rates are heavily dependent on your credit score. If your score is below 650, you will likely not qualify for a rate that actually helps you.

- The biggest risk is behavioral. Many consumers pay off their credit cards with a loan, keep the cards open, and run the balances back up, effectively doubling their debt.

The Reality of Moving Debt Instead of Erasing It

A debt consolidation loan is often marketed as the ultimate financial reset button. The pitch is always the same: bundle all your messy, high-interest credit card bills into one simple, low-interest monthly payment. It sounds like a perfect solution, and for a specific type of borrower, it absolutely is.

But taking out a loan to pay off debt requires a brutal level of honesty about your financial habits and your credit profile. A consolidation loan works only if the new interest rate is lower than what you are currently paying. That sounds incredibly obvious, but many people sign loan agreements without doing the math, ultimately locking themselves into terms that cost them more money in the long run.

During my years reviewing accounts inside third-party collection agencies, I saw a very specific and tragic pattern. We would receive a file for a defaulted personal loan from a major online lender. When I pulled the consumer’s credit report to assess their ability to pay, I would see five maxed-out credit cards alongside the defaulted loan. The consumer had taken the loan to consolidate the cards, felt a false sense of financial freedom, and immediately started swiping the cards again. We called it the “double debt trap.”

Understanding when a consolidation loan makes mathematical sense, and when it is simply a temporary band-aid, is the single most important step before you apply for new credit.

What a Debt Consolidation Loan Actually Is

Before analyzing the numbers, it is critical to define the financial instrument itself. A debt consolidation loan is simply an unsecured personal loan. You are borrowing a lump sum of money from a bank, credit union, or online lender for the express purpose of paying off your existing creditors.

When the loan is funded, you (or the lender directly) disburse the money to Visa, Mastercard, or your medical providers, bringing those balances to zero. You are left with a single loan, a fixed interest rate, a fixed monthly payment, and a fixed payoff date.

The fundamental truth about this process is that consolidation does not reduce what you owe. If you have $20,000 in credit card debt and you take out a $20,000 personal loan to pay it off, you still owe exactly $20,000. You have not erased a single dollar of principal. You have merely moved the debt from several institutions to one institution.

From an operational standpoint inside the collections industry, a consolidation loan is simply a balance transfer executed via cash. We often preferred dealing with consumers who had defaulted on a single large personal loan rather than tracking down five different credit card charge-offs. The paperwork was cleaner. The banks know this as well. When they approve a consolidation loan, they are intentionally buying out your smaller creditors to own the entirety of your debt. Because the principal remains identical, the entire value of this move hinges on the interest rate.

The Interest Rate Math Test

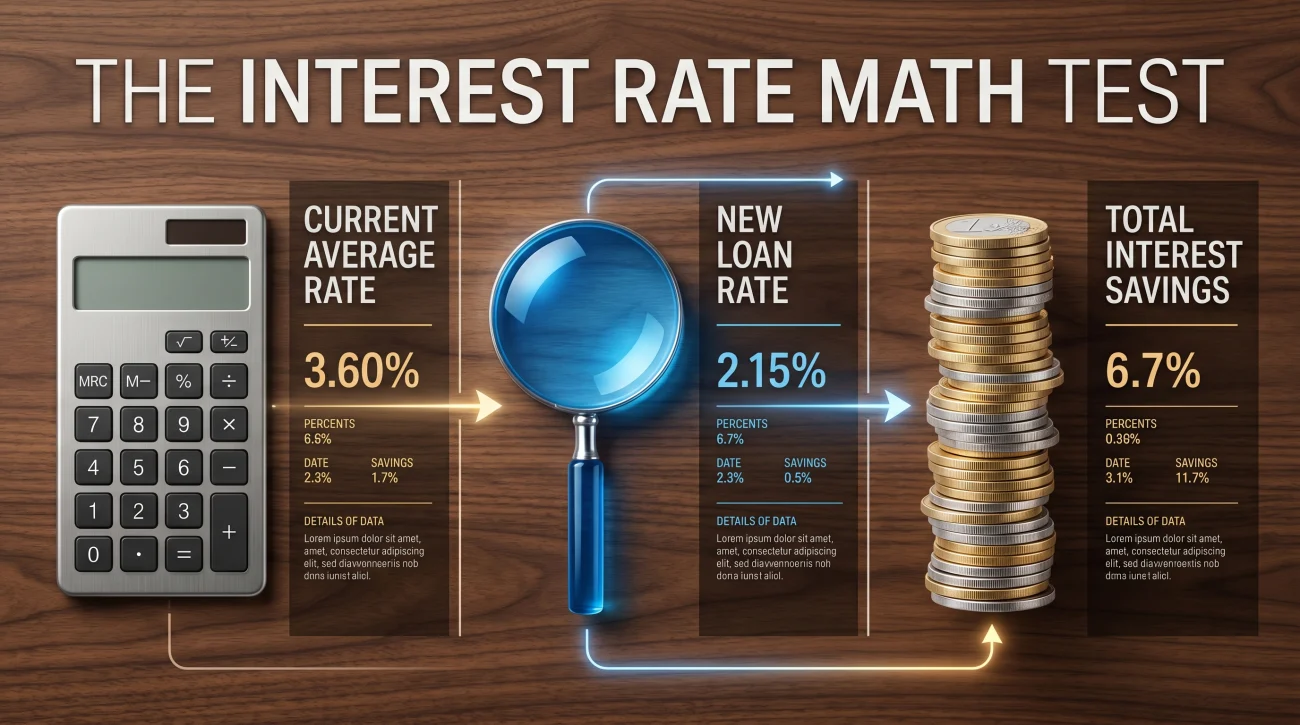

The only way to know if a consolidation loan is a good idea is to calculate your current weighted average interest rate and compare it to the rate you are being offered. You cannot just guess. You have to do the math.

First, you must add up your current monthly interest charges across all the debts you want to consolidate. Then, look at the Annual Percentage Rate (APR) offered by the personal loan. If the new loan offers a meaningfully lower rate, consolidation saves you money. If the rate is the same or higher, consolidation only simplifies your payment schedule, but it does not save you a dime.

The Mathematical Reality Check

Imagine you have $20,000 spread across three credit cards, and your average interest rate is 22%. You plan to pay this off over three years (36 months).

Scenario A (The Math Works): You qualify for a 3-year consolidation loan with a fixed 12% APR. Your monthly payment is roughly $664. Over three years, your total interest paid will be about $3,900. Without the loan, keeping that same $20,000 at 22% on a 3-year payoff track would cost you over $7,500 in interest. The consolidation saves you roughly $3,600, and your payment attacks the principal much faster.

Scenario B (The Math Fails): Your credit score is poor, so the best consolidation loan you can qualify for carries a 24% APR. Your new monthly payment rises to over $780, and your total interest paid jumps to over $8,200. Moving 22% debt into a 24% loan is stepping backward. You are paying thousands of dollars more simply for the convenience of a single payment.

Many online lenders bury high interest rates behind the promise of “one low monthly payment.” They achieve that low payment by stretching the loan term out to five or seven years. You might feel relief because your monthly cash flow improves, but you will ultimately pay vastly more in total interest. Always look at the total cost of the loan, not just the monthly payment.

The Origination Fee and Your Break-Even Point

Interest rates do not tell the whole story. Most personal lenders charge an origination fee to process the loan. This fee typically ranges from 1% to 8% of the total loan amount, depending on your credit score. The lender either adds this fee to your loan balance or deducts it from the cash they disburse to you.

If you take out a $20,000 loan with a 5% origination fee, you are paying $1,000 upfront just to borrow the money. To determine if the loan is actually worth it, you have to calculate your break-even point. If the loan saves you $3,600 in interest over three years (like in the example above), the $1,000 fee is easily justified by the $2,600 in net savings. However, if the interest rate difference is very small and only saves you $800 over the life of the loan, paying a $1,000 origination fee means you are actually losing money.

How to Shop for Rates Without Damaging Your Credit

Many consumers damage their own credit scores during the application process because they do not understand the difference between a soft pull and a hard pull.

When you formally apply for credit, the lender performs a “hard inquiry” on your credit report. This temporarily drops your score. Applying to five different lenders in one afternoon hoping to find the best rate can drag your score down just when you need it to be highest.

Instead, you must use pre-qualification tools. Most online lenders and major banks now offer pre-qualification forms that use a “soft pull.” This checks your credit background to give you an estimated interest rate without impacting your score at all. You should rate-shop extensively using only soft pulls, compare the estimated offers, and then submit a formal application (the hard pull) only to the single lender offering the best verifiable terms.

When deciding where to apply, do not overlook local credit unions. While online lenders are fast and convenient, non-profit credit unions operate differently. By federal regulation, federal credit unions are generally subject to rate caps on personal loans, which can make them more competitive than online lenders for borrowers with fair credit. They will frequently offer a better rate and lower origination fees than a heavily marketed online lender.

The Credit Score Gatekeeper

The single biggest barrier to successful debt consolidation is your credit profile. The personal loan market prices risk very strictly. Because there is no collateral backing an unsecured personal loan, lenders rely heavily on your FICO score and your Debt-to-Income (DTI) ratio to determine your interest rate.

Borrowers are often shocked by the rates they are offered when they finally check.

- Scores above 720: These borrowers typically see the best rates, often ranging from 7% to 12%. For them, consolidating high-interest credit cards is highly effective.

- Scores between 650 and 720: Borrowers in this mid-tier usually see rates between 12% and 20%. The math requires careful review here. If your cards are at 18% and the loan is at 16% with a high origination fee, the savings might be negligible.

- Scores below 650: This is the danger zone. Rates in this tier often exceed 20%, or applications are denied entirely. If your credit is already damaged because your cards are maxed out or you have missed payments, you will likely not qualify for a rate that beats your existing debt.

This creates a frustrating paradox: the people who need debt consolidation the most are usually the ones who cannot qualify for a loan that actually helps them.

What Types of Debt Can You Consolidate?

Personal loans can be used to pay off almost any type of unsecured consumer debt. The most common targets are revolving credit card balances, store charge cards, existing high-rate personal loans, and accumulated medical bills.

However, you must be very careful about mixing different categories of debt. Understanding exactly what debts can be settled or consolidated is crucial. For instance, you should generally never use an unsecured personal loan to pay off secured debt, like an auto loan, because auto loan rates are almost always lower than personal loan rates.

Furthermore, you should never consolidate federal student loans with a private personal loan. Federal student loans come with built-in consumer protections, such as income-driven repayment plans, deferment options, and potential forgiveness programs. If you pay off a federal student loan with a private consolidation loan, you strip away every single one of those government protections permanently.

But even if you have the right mix of eligible unsecured debt, the mechanics of paying them off introduce a massive behavioral risk.

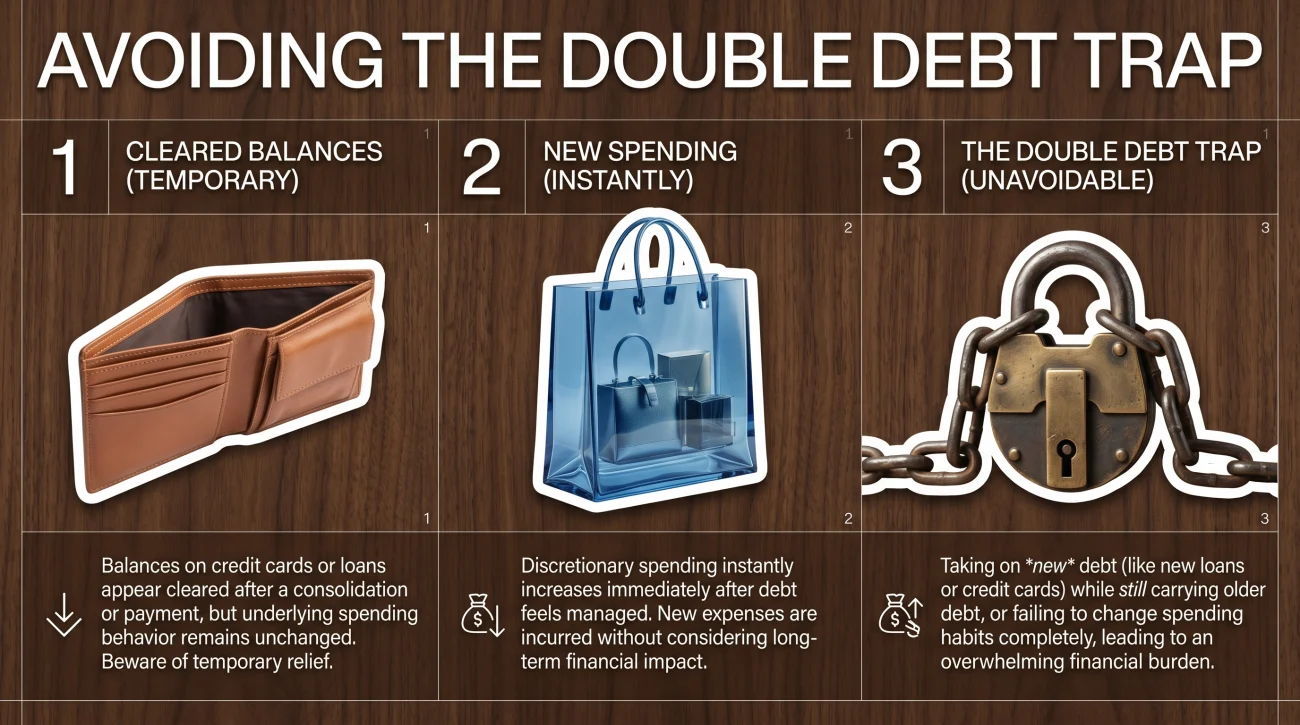

The Double Debt Trap

The mathematical failure of a high interest rate is bad, but the behavioral failure of a consolidation loan is catastrophic. This is the scenario I witnessed constantly in the collections industry.

When you use loan funds to pay off five credit cards, you suddenly have five open credit cards with zero balances. For someone who has spent years staring at maxed-out limits, seeing thousands of dollars in available credit feels like a windfall.

An unexpected car repair comes up. A medical emergency happens. A holiday rolls around. The consumer justifies using just one of the cleared cards, intending to pay it right back. Six months later, they are carrying a balance on the cards again. Now, they are trapped paying the hefty monthly installment for the consolidation loan, plus new minimum payments on the freshly charged credit cards.

Paying off your credit cards with a loan and keeping all the cards in your wallet “just in case of an emergency,” relying solely on willpower.

Paying off the cards, physically destroying the plastic, and removing the card numbers from all digital wallets and online retail accounts to introduce extreme friction against new spending.

Financial advisors debate whether you should actually close the credit card accounts after consolidating. Closing accounts can temporarily lower your credit score by reducing your average age of accounts and shrinking your total available credit. However, if you know you lack the discipline to leave a zero-balance card alone, the temporary credit score dip is infinitely better than falling into the double debt trap.

Comparing Consolidation to the Alternatives

A consolidation loan is just one tool in a much broader toolkit. To understand all your debt relief options, you must compare the loan against other structured paths.

Consolidation Loan vs. Balance Transfer

If your credit score is above 680 and your total debt is relatively small (under $10,000), a 0% introductory balance transfer credit card is mathematically superior to a personal loan. You pay a small upfront transfer fee (usually 3% to 5%), but you pay exactly 0% interest for 12 to 21 months. However, a balance transfer only works if you have the discipline to pay off the entire balance before the introductory period expires and the high standard rate kicks in.

Consolidation Loan vs. Debt Management Plan (DMP)

If your credit score has already dropped below 650, you will likely not qualify for a good consolidation loan. In this scenario, a nonprofit credit counseling agency is often the better path. In a debt management plan, the agency negotiates your interest rates down (often to single digits) without requiring a hard credit check or issuing a new loan. You still make one monthly payment, but you are required to close the accounts, which protects you from the double debt trap.

Consolidation Loan vs. Debt Settlement

If you cannot afford the monthly payment of a consolidation loan or a DMP, you are dealing with a severe hardship. In this case, neither strategy will work. Your focus shifts toward evaluating debt settlement, where you negotiate to pay less than the full principal balance, accepting severe credit damage in exchange for financial survival.

What to Do If Your Application Is Denied

If you receive a rejection notice, do not panic and do not immediately apply to five more lenders. Each formal application creates a hard inquiry that lowers your score further. A rejection is a clear signal from the financial system that your debt-to-income ratio or credit history does not support a new loan. Take 30 to 60 days to review the denial letter, stabilize your budget, and pivot your strategy toward the alternative programs mentioned above that do not require credit approval.

Signs a Consolidation Loan Is Not Your Best Option

It is vital to recognize when borrowing more money is the wrong move. A consolidation loan is a strategy for people who have a stable budget surplus but are simply bogged down by inefficient interest rates. It is not a lifeline for people who are fundamentally broke.

You need to pivot away from a loan application if any of these indicators apply to your situation:

- You are only receiving high-rate offers. If you have already been denied by multiple lenders or only quoted rates higher than your current credit cards, borrowing more money is the wrong strategy. Moving debt at a higher cost makes no sense.

- You cannot identify a monthly budget surplus. If you take out a loan and the new monthly payment still consumes 100 percent of your disposable income, one minor emergency will force you to use credit cards again.

- You have consolidated before and failed. If you previously took out a loan to clear your cards, and those cards are now carrying balances again, your problem is spending behavior, not interest rates. Another loan will only deepen the hole.

- You are trying to consolidate interest-free bills. Converting medical debts that carry zero interest into a personal loan that charges you a monthly percentage will instantly increase your total cost.

If your credit is damaged, your budget is underwater, and you are already falling behind on minimum payments, searching for a new loan is the wrong strategy. You need a structural intervention to reduce the balances, not just shuffle them around. In these severe hardship cases, you should learn how to safely evaluate programs that help you negotiate your balances for less than you owe.

Final Thoughts: The Execution Matters Most

A debt consolidation loan is a highly effective financial tool when executed with precision. The math does not care about your intentions. If the new rate is lower, the term is reasonable, and you commit to the monthly payment, you will save money and accelerate your path out of debt.

But the execution is where most consumers fail. Taking the loan is the easy part. The day the funds hit your account and your credit card balances drop to zero is actually the most dangerous moment in the entire process. It feels like you have finished the race, but you have only changed the track.

Your mindset must shift immediately from “I paid off my cards” to “I am now locked into a strict repayment contract.” Treat the loan funding date as a point of no return. Lock the cards, delete the saved numbers, and force yourself to live exclusively on the cash you actually have in the bank. If you cannot make that behavioral commitment, the consolidation loan will simply become the largest debt on your future collection file.

❓ FAQ

🏦 Does a debt consolidation loan hurt my credit score?

Applying causes a small, temporary dip due to the hard inquiry. However, using the loan to pay down maxed-out credit cards drastically improves your credit utilization ratio, which often leads to a significant score increase within a few months.

📉 What credit score is needed for a good consolidation loan?

To secure an interest rate that is actually lower than typical credit card rates, you generally need a FICO score of 680 or higher. The best rates are reserved for scores above 720.

✂️ Will taking a consolidation loan reduce the total amount I owe?

No. A consolidation loan pays off the principal balance of your old debts by creating a new loan for the exact same principal amount. It only reduces the interest you pay over time, not the core debt itself.

🏥 Can I include medical bills in a consolidation loan?

Yes, you can use the funds to pay medical providers. However, since medical bills often do not accrue interest, moving them into a personal loan that charges interest is usually a bad financial decision.

💳 Should I close my credit cards after consolidating them?

Closing them prevents you from racking up new debt, which is the safest behavioral choice. However, closing old accounts can slightly lower your credit score. If you have strict discipline, keep your oldest card open but hide it; if you lack discipline, close them all.

⏱️ How long does it take to get approved and funded?

Many online lenders offer approval decisions within minutes and can fund the loan directly to your bank account or to your creditors within 1 to 3 business days.

💵 Are there fees associated with consolidation loans?

Yes, most personal lenders charge an upfront origination fee. As detailed in the break-even section above, you must subtract this fee from your projected interest savings to determine if the loan is truly worth taking.

🚫 Can I consolidate an auto loan with a personal loan?

While technically possible if the lender allows it, it is almost never advisable. Auto loans are secured by the vehicle and carry much lower interest rates than unsecured personal loans.

Relief options exist alongside the collection process. These explain both sides.

- The options for resolving debt outside of continued collection

- Debt Relief Scams: How to Spot Them Before You Pay and What the FTC Says About Legitimate Companies

- How to Negotiate Debt Yourself: Hardship Programs and Settlements

- Balance Transfer Cards for Debt: The 0% APR Strategy

- Debt Settlement vs Credit Counseling: Two Very Different Programs for Two Very Different Situations

Some of these have deadlines attached. Start here if something is already happening.

- What collectors can legally do to you while a settlement program is running

- How to handle a lawsuit on a debt you are actively trying to settle

- What happens to a garnishment order when debt relief is in progress

- How bank levies interact with the debt you are trying to resolve

- How professional settlement programs work and what they actually cost

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.