- Yes, debt collectors are permitted to email you. Industry regulations were updated in late 2021 to explicitly allow this communication channel.

- Collectors generally avoid sending emails to a work email address if they know it belongs to your employer, as it crosses a major compliance line.

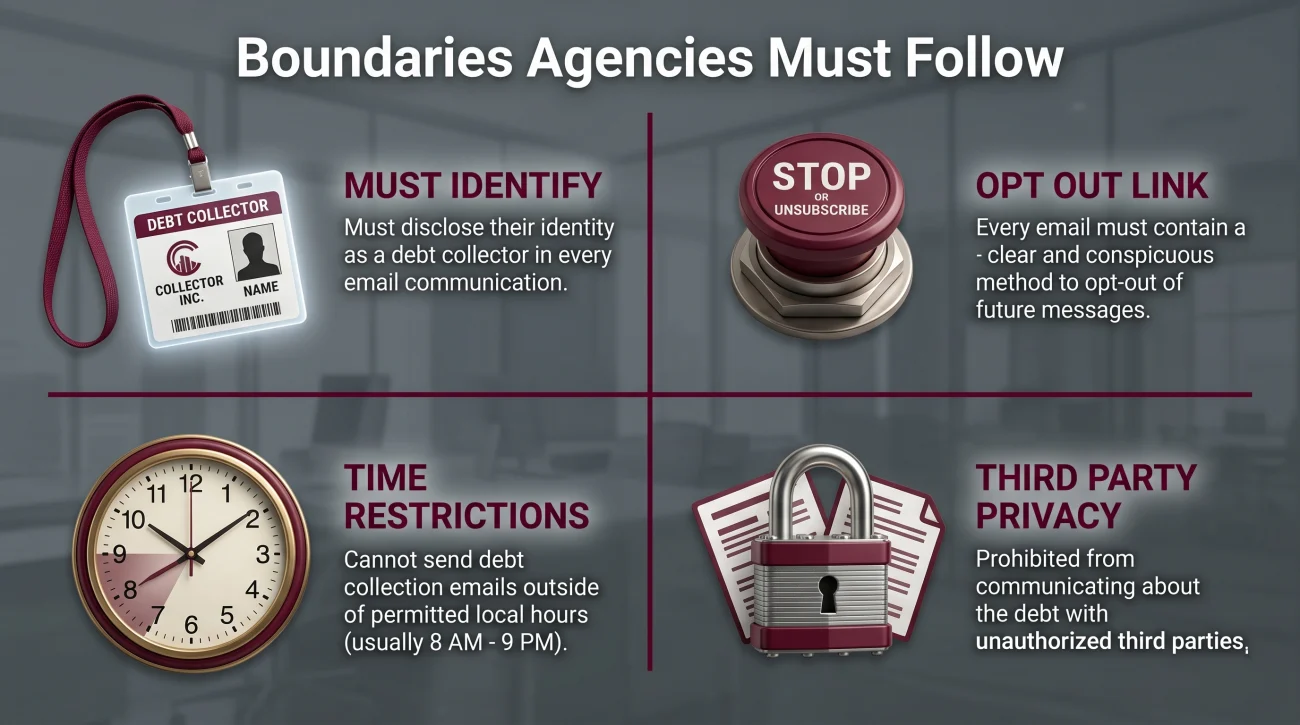

- Every legitimate debt collection email must include a clear, simple method for you to opt out of future messages.

- Phishing scams are incredibly common in this space. Never click a payment link in an unexpected email without verifying the debt independently first.

An Email in Your Spam Folder: Phishing Scam or Real Collection Attempt?

When you see an email claiming you owe a debt, your first instinct is probably to look for the grammatical errors that give away a phishing scam. For years, we were trained to assume that any unexpected email demanding money was a fraud, and that real collection agencies only used physical letters and phone calls.

But the rules of the game have changed. The short answer to whether debt collectors can email you is a definitive yes.

I spent 12 years working inside third-party collection agencies and a national debt buyer. For the majority of my career, sending an email to a consumer was something we strictly avoided. The compliance risks were simply too high. If an email bounced, or was read by a spouse, or landed on a corporate server, the agency could face massive fines. We relied almost entirely on predictive dialers and physical mail. However, that entire landscape shifted dramatically in late 2021.

Today, email is a primary tool in a debt collector’s outreach strategy. If you are receiving these messages, you need to know exactly how to distinguish a real collection attempt from a dangerous phishing scam. You also need to understand the operational boundaries collectors are expected to follow, particularly when it comes to your workplace, and the exact steps you can take to shut down the digital notifications.

The 2021 Shift: Why Collectors Are Now in Your Inbox

To understand why your inbox is suddenly a target, you have to look at the rules that govern collector contact. Historically, the regulations were written long before electronic communication existed, creating a massive gray area. Agencies wanted to use email because it is virtually free compared to physical postage, but they were terrified of crossing invisible legal lines.

That ambiguity cleared up in late 2021 when federal regulators updated the rulebook to explicitly allow electronic communications. Overnight, the industry adapted. Agencies that had never sent an email began integrating massive digital campaigns alongside their traditional phone banks. Just like debt collection text messages, reaching you on your smartphone screen proved highly effective.

Inside the agency, the transition to email was celebrated for two reasons. First, the cost per contact dropped to fractions of a penny. Second, and more importantly, email software uses tracking pixels. When we mailed a physical letter, we had no idea if you opened it. When we sent an email, the system notified the collector the exact second you opened the message. That open receipt would automatically bump your account to the top of the call queue, because we knew you were looking at your phone right then.

💡 Pro Tip: You can neutralize the tracking pixel tactic easily. Go into your email provider’s settings (Gmail, Outlook, Apple Mail) and turn off “automatically load images.” Tracking pixels are essentially tiny, invisible images. If your email client doesn’t load them, the collector’s system will never know you opened the message.

This new permission slip, however, is not unlimited. Agencies must navigate a rigid set of boundaries, and when they cut corners, they hand you leverage.

The Boundaries Agencies Are Expected to Follow

While the delivery method is modern, the fundamental consumer protections have not changed. Collectors emailing you must still adhere to basic fairness rules, plus a few email-specific mandates.

They Must Clearly Identify Themselves

A legitimate debt collector cannot send a vague email that simply says, “Urgent matter regarding your account, please call us.” Every initial communication must clearly state that the sender is a debt collector attempting to collect a debt. If an email lacks these standard disclosures, it is a significant compliance failure.

The Mandatory Opt-Out Link

This is the most critical protection for your inbox. Every single email sent by an agency must include a clear, simple method for you to opt out of future messages. Usually, this takes the form of an “Unsubscribe” link at the bottom. Sending an email without providing a way to turn off that specific channel is a line agencies know they cannot cross safely.

Time Restrictions and Electronic Delivery

Collectors are generally restricted from contacting you outside of normal waking hours. Applying this to email is practically tricky because emails are passive; you might read them at any time. However, operationally, legitimate agencies will not intentionally schedule automated emails to hit your inbox at 2:00 a.m. Doing so invites harassment complaints and unnecessary regulatory scrutiny that compliance officers work hard to avoid.

The Risk of Third-Party Disclosure

Collectors are forbidden from revealing your debt to anyone else. With physical mail, they use blank envelopes. With email, the risk is that a spouse or family member might share an email account with you, or might see the notification pop up on a shared tablet. If an agency sends an email that reveals your debt and someone else reads it, they are stepping into very dangerous territory.

The Work Email Shield: Protecting Your Corporate Inbox

One of the most stressful experiences a consumer can have is discovering a collection notice sitting in their corporate email inbox. The immediate fear is that the IT department, a manager, or human resources might monitor the server and see the message. Collectors are fully aware of this fear.

Just as calling your workplace is used as a tactic to generate social pressure, emailing a work address serves the exact same psychological purpose. It forces you to act quickly to prevent professional exposure.

Because the potential for embarrassment is so high, there are specific guardrails. Generally speaking, a debt collector is prohibited from sending emails to an address they know, or should reasonably know, is provided by your employer. Unless you specifically gave them that corporate address, used it to contact them first, or provided it to the original creditor, agencies know that blasting collection notices to a company domain is a massive compliance risk.

If an agency is doing this anyway, they are recklessly risking a third-party disclosure to your employer. From an industry perspective, agencies know this is territory they cannot safely operate in.

How to Tell if a Debt Collection Email is Real or Phishing

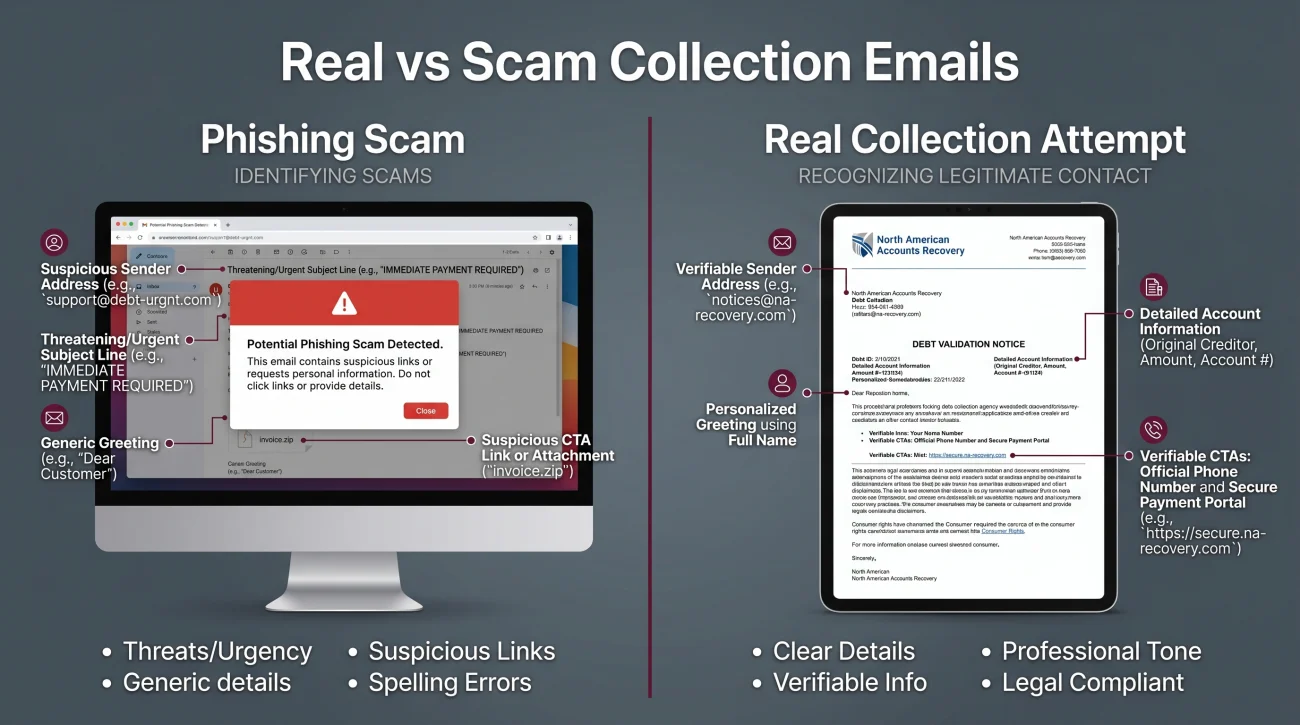

This is the most critical evaluation you must make. The inbox is a dangerous place. Because legitimate collectors are now using email, international scammers use the exact same format to impersonate them. The scammers do not want you to pay a debt; they want you to click a malicious link to steal your banking credentials or download malware.

In my operational experience, legitimate collection agencies write incredibly dry, boring, and highly formalized emails. They run every template through teams of compliance officers. Scammers, on the other hand, write emails designed to trigger blind panic. You can often spot the difference before you even open the message just by looking at the subject line.

Subject: URGENT: Arrest Warrant Issued / Legal Action Pending

“A lawsuit has been processed under your Social Security Number. You will be served at your workplace tomorrow morning. To cancel this legal action, you must immediately pay your past due balance using this secure portal: [Suspicious Link]”

Subject: Account Notification from [Agency Name]

“This email is from [Agency Name], a debt collector. This is an attempt to collect a debt. Our records indicate an outstanding balance originating from [Original Creditor]. Please contact our office at 1-800-555-0199 or visit our website to view your options. To stop receiving emails from us, click Unsubscribe.”

Here are the definitive red flags that indicate an email is a phishing scam rather than a real collection attempt:

- ⚠️ Strange Sender Addresses: Legitimate agencies use official corporate domains (e.g., [email protected]). Scammers often use free email services or domains with slight misspellings of real banks. Always check the actual sender address, not just the display name.

- ⚠️ Demands for Untraceable Payment: If the email asks you to pay a debt using gift cards, cryptocurrency, or a wire transfer, it is a scam. Real agencies process standard credit card, debit card, or ACH check payments.

- ⚠️ Threats of Imprisonment: You cannot go to jail for unpaid consumer debt in the United States. Any email threatening police action is fraudulent.

- ⚠️ Generic Greetings: Legitimate collectors know your name because they bought your file. Scammers blasting lists often use generic greetings like “Dear Customer” or “Dear Debtor.”

⚠️ Warning: Never click a link or open a PDF attachment in a collection email if you are even slightly unsure of its origin. Malicious attachments can compromise your computer immediately.

💡 Pro Tip: If you receive an email that looks legitimate but you are still hesitant, do not use the links or phone numbers provided in the message. Instead, pull your own credit report. Find the collection agency listed there, look up their official website independently, and call their main customer service line.

How to Stop Debt Collector Emails (And What to Expect Next)

If you have verified that the email is from a real agency, but you simply do not want them communicating with you digitally, you have the right to shut the channel down. The process is straightforward, but it is important to understand what happens after you do it.

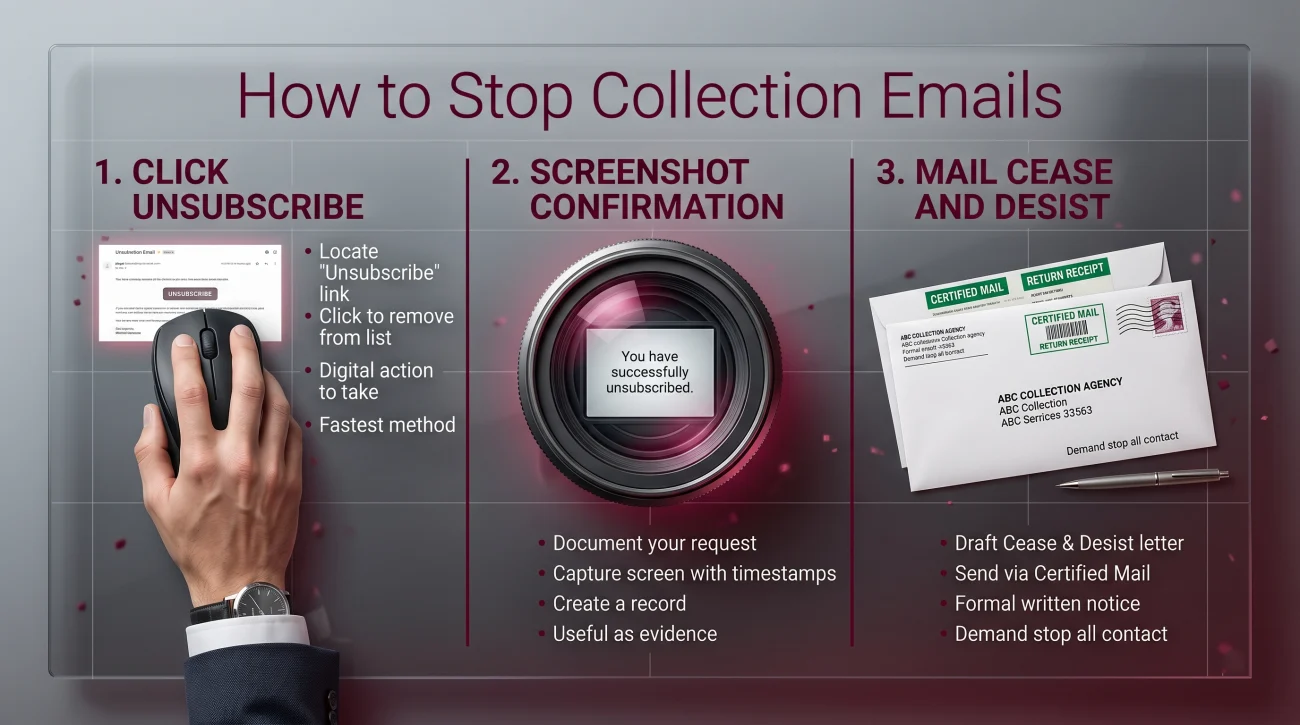

The easiest method is to use the opt-out mechanism they provided. Scroll to the bottom of the email and click the “Unsubscribe” link. Following their exact process is the fastest way to get your email address removed from their automated mailing software.

Action: Click the opt-out link + Save a screenshot of the confirmation page + Monitor your inbox

If there is no link, or if you do not trust clicking it, you can reply directly to the email stating: “I do not consent to receiving emails from your agency. Remove this email address from your file.”

Key Point: Opting out of emails only revokes their permission to use your email address. It does not erase the debt, and it does not stop their collection efforts.

Once you cut off their email access, agencies will almost always pivot their strategy. You can expect an increase in phone calls or a sudden influx of physical letters, as they shift their efforts to the channels they still have permission to use. If you want to stop all forms of contact across the board, an email unsubscribe is not sufficient. You will need to send a formal, written request to force the debt collector to stop all communication.

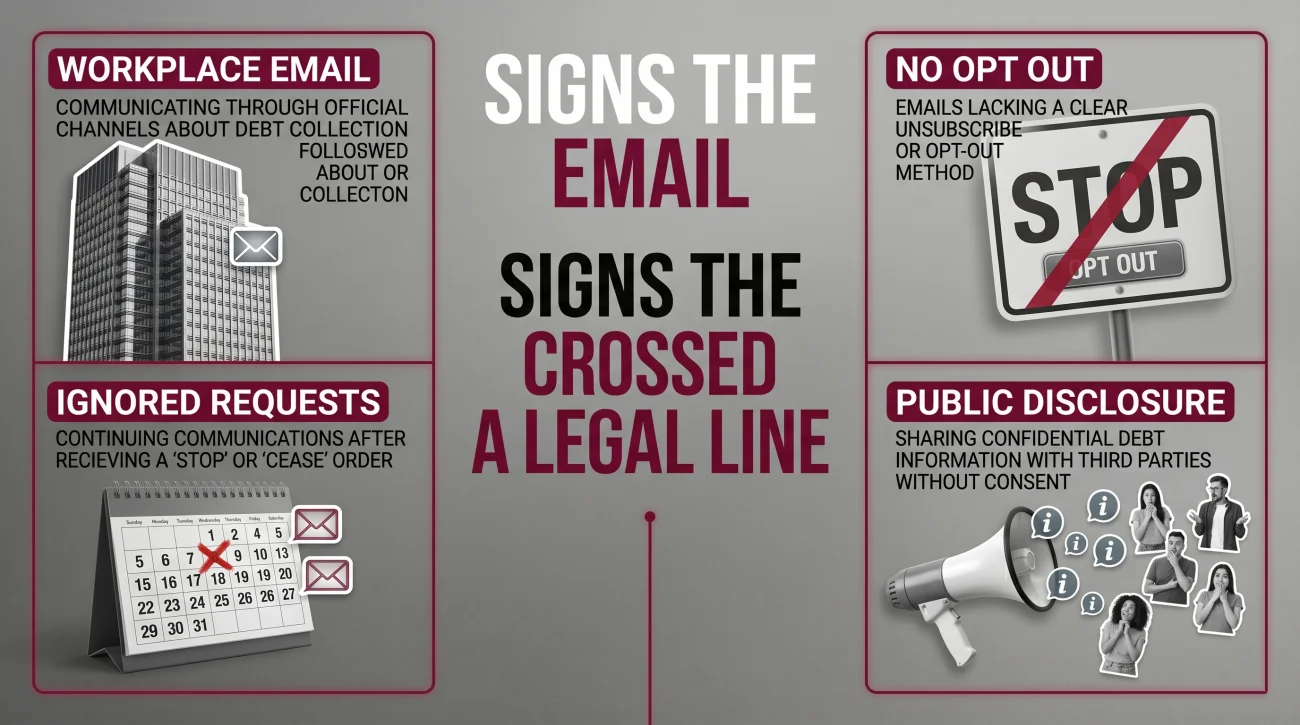

Signs the Email Contact Has Crossed the Line

Knowing that collectors are allowed to email you is only half the battle. The other half is recognizing when they execute their campaigns aggressively, creating documentable compliance failures.

You need to document your situation and preserve the evidence if you are experiencing any of the following:

- The collector sent the email to your workplace address without your prior consent.

- The email did not contain any clear way to opt out or unsubscribe.

- You clicked the opt-out link or replied asking them to stop, but the emails continued arriving days later.

- The email included threatening language or implied you had committed a crime.

- The email did not include the required disclosure stating that it was from a debt collector.

If an agency ignores your opt-out request or emails your corporate server, they are banking on the fact that you do not know your rights. Do not just delete the emails in frustration. Print them to PDF, capture the headers, and save the timestamps.

If the contact you are receiving is crossing these specific boundaries, you need to evaluate what to do if you are dealing with debt collector harassment to understand how those documented missteps can give you the upper hand.

Final Thoughts: Why Email Can Actually Work in Your Favor

Most consumers hate getting collection emails, but from an insider perspective, email is a double-edged sword for the agency. Unlike a phone call where what was said can become a “he said, she said” debate, an email creates a permanent, undeniable paper trail.

If you are trying to negotiate a settlement or dispute a balance, communicating via email forces the collector to put their offers, promises, and claims in writing. Use the opt-out tools to protect your digital privacy if you want them gone, but if you intend to resolve the account, remember that every email they send you is documented proof of exactly what they agreed to. Use that trail to your advantage.

❓ FAQ

📧 Is it actually legal for debt collectors to email me?

Yes. Recent updates to industry regulations explicitly permit debt collectors to use email as a communication channel, provided they follow strict identification and opt-out rules.

💼 Can a debt collector send emails to my work email address?

Generally, no. A collector should not send messages to an email address they know belongs to your employer, unless you specifically gave them permission to use it or used it to contact them first.

🛑 How do I stop a debt collector from emailing me?

You can stop the emails by clicking the opt-out or unsubscribe link that must be included in every message. You can also reply directly stating that you revoke consent for email communication.

🎣 How can I tell if a debt collection email is a phishing scam?

Scams often use panic-inducing subject lines, threaten immediate arrest, demand payment via gift cards or crypto, and are sent from suspicious domains. Legitimate emails identify the agency and original creditor clearly.

🔗 Should I click the link in a debt collection email?

Never click a payment link or open an attachment if you are unsure if the email is legitimate. It is always safer to look up the collection agency independently online and access their payment portal directly.

📞 If I unsubscribe from emails, will they stop calling me too?

No. Unsubscribing from emails only shuts down that specific digital channel. If you want to stop phone calls and physical mail as well, you must send a formal, written cease and desist letter by mail.

👀 Can a debt collector see if I opened their email?

Yes, if your email client automatically loads images. Agencies use tracking pixels to notify their system when a message is opened. You can defeat this by turning off “automatically load images” in your email settings.

⚖️ What happens if a collector ignores my request to stop emailing?

If an agency continues to email you after you have clearly opted out, they are crossing a major compliance line. Save the emails as evidence, as this documented pattern can give you significant leverage.

✉️ Do email notices count as my official debt validation notice?

They can. The rules allow collectors to provide your initial validation notice electronically. However, it must still contain all the required information, including an explanation of your right to dispute the debt within the timeframe specified in the notice.

💬 Can I dispute a debt by replying to the email?

While you can reply to an email, it is highly recommended to send your official debt dispute via certified physical mail. Certified mail provides undeniable proof of delivery that a simple email reply lacks.

The full FDCPA framework and the four areas where it matters most.

- Your legal rights when collectors call, write, or threaten to sue

- When they can call, what they cannot say, and how to make it stop

- How to identify FDCPA violations and what you can do with them

- Why the age of a debt determines what a collector can legally do

- Your right to demand proof before paying or acknowledging anything

Harassment is one thing. Lawsuits, garnishments, and frozen accounts are another.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.