- A debt collector is legally permitted to call your workplace under federal law, but they must follow extremely strict rules regarding what they can say.

- Their primary goal in calling your job is rarely just to find you. It is a calculated tactic designed to use social pressure and the fear of your employer finding out to force a payment.

- They cannot legally disclose that they are a debt collector or mention that you owe a debt to anyone at your job, including your boss or a receptionist.

- You have the absolute right to stop these calls immediately. Simply telling the collector that your employer does not permit personal calls forces them to stop contacting you at work.

The Anxiety of the Workplace Collection Call

The phone rings at your desk, and your heart sinks. It is a debt collector. Suddenly, you are not just worried about your finances; you are terrified that your coworkers or your boss might find out about your situation.

During my twelve years working inside third-party collection agencies, I saw firsthand how this specific tactic was utilized. We knew a call to a home number might go to voicemail and be ignored for weeks, but a call to a workplace almost always gets an immediate, highly emotional reaction. That feeling of panic is exactly what the collector is going for.

If you just received a call at your job, you need to understand the ground rules. Yes, the law provides them with a narrow window to make these calls, but it also gives you a highly effective kill switch to shut them down. Here is what they can actually do, why they are really calling, and how you can protect your livelihood.

Why Collectors Call Workplaces: The Real Motive

To understand how to handle these calls, you first need to understand why they happen. Most consumers assume that a collector calls their job simply because they could not reach them at home. While that is sometimes the case, the reality of collection floor operations is much more strategic.

Under the Fair Debt Collection Practices Act (FDCPA), the legal justification for contacting a third party, which includes your employer, is strictly to acquire “location information.” This means they are supposedly just trying to confirm your home address, your personal phone number, or where you are currently employed. That is the legal cover.

The operational reality is different. Social pressure is the actual goal. When a collector calls your workplace, the possibility that your employer or your colleagues might overhear the conversation is significant. The pressure of maintaining a professional image while dealing with a debt collector drives people to make payments much faster than a standard collection letter ever could.

When I was training new agents on the collection floor, the rule was simple. If a consumer was ignoring our calls to their mobile phone, we looked for a verified place of employment. We knew that calling a front desk and asking for the consumer by their full legal name would make them incredibly uncomfortable. It was a pressure lever, pure and simple, completely legal as long as we stuck exactly to the script.

Regulators are well aware of this psychological dynamic. The Consumer Financial Protection Bureau (CFPB) has explicitly noted in its rulemakings that workplace calls are frequently used to embarrass and coerce consumers, not just to locate them. This is why the rules surrounding these calls are so strict.

Is It Legal for Them to Call Your Job?

This is the most common question I hear from consumers facing this situation. The short answer is yes, it is legal under federal law for a debt collector to call your workplace. However, it comes with a massive, built-in exception that works entirely in your favor.

The FDCPA allows debt collectors to contact you at your place of employment unless the collector knows, or has reason to know, that your employer prohibits you from receiving such communications. They are allowed to make the initial assumption that calling you at work is fine until that assumption is corrected.

If you work in an environment where personal calls are obviously forbidden, like a hospital floor or a busy restaurant kitchen, the collector arguably has reason to know that calling you there is inappropriate. However, proving this in hindsight is difficult. You cannot rely on them to infer your company policy. You have to tell them directly.

It is crucial to note that these federal rules apply specifically to third-party collection agencies and debt buyers. If your original creditor, like the actual bank that issued your credit card, is calling you directly, they operate under a different set of rules that are often less restrictive.

If you are dealing with collectors finding your company email address instead of calling, there are separate rules governing electronic communications. You can review how to handle that scenario in our guide on whether debt collectors can email you.

What They Are Legally Allowed to Say to Your Employer

Because the risk of exposing your debt to your boss or coworkers is so high, federal law places extreme limitations on what a collector can say when someone else answers the phone at your job. They are permitted to seek location information, and absolutely nothing else.

If a receptionist, a colleague, or your manager answers the phone, the collector must adhere to the following strict boundaries:

- 📌 They can only state their own name. They cannot state the name of their collection agency unless explicitly asked.

- 📌 They can state that they are confirming or correcting your location information.

- 📌 They absolutely cannot state that you owe a debt.

- 📌 They cannot indicate that the call is related to the collection of a debt.

- 📌 They cannot use a company name that indicates they are in the debt collection business. For example, if their company is “National Debt Recovery Professionals,” they must use an acronym or a generic name to avoid tipping off your employer.

When collectors follow the law, the conversation is incredibly brief and vague. When they break the law, they usually do it by dropping hints, hoping your employer gets suspicious and confronts you.

“Hi, this is Mike from Advanced Credit Solutions. I need to speak with John Doe regarding an urgent financial matter attached to his file. Is he available?”

“Hello, my name is Mike. I am trying to reach John Doe to confirm his current contact information. Can you connect me to him, or confirm if he still works there?”

If the collector crosses the line and actually tells your boss or a coworker that you owe money, they have committed a severe third-party disclosure violation. This is highly actionable. If this has happened to you, you need to understand what to do if they explicitly revealed your financial situation to a manager by reading our guide on when a debt collector tells your employer about your debt.

How to Stop Workplace Calls Immediately

You do not need to hire a lawyer to stop a debt collector from calling your job. You do not need to wait for a court order. The law gives you the power to stop this specific type of contact with a single sentence.

To stop the calls, you simply have to provide them with the knowledge that your employer prohibits personal calls. This applies even if your employer does not actually have a strict formal policy. Your verbal statement to the collector that you cannot receive these calls at work is legally sufficient to put them on notice. Once you say the words, they must stop dialing your workplace number.

If you are a remote worker using your personal cell phone for business, this boundary can sometimes feel blurred. However, the rule remains the same. If you state you cannot receive these calls during working hours on that line, they must respect that boundary.

💡 Pro Tip: You can give this notice verbally over the phone the next time they call your job. You do not legally have to do it in writing to make it effective, although written confirmation is always safer for your own records.

Here is exactly what to say if you answer the phone at work and realize it is a collector:

“This is my place of employment. My employer prohibits me from receiving personal calls here. You are not to contact me at this number again.”

Do not explain yourself. Do not apologize. Do not get drawn into a conversation about the debt itself. Deliver the statement, document the time you said it, and hang up. That is all it takes.

What Happens After You Tell Them to Stop

Once you establish that boundary, a line is drawn in the sand. Any legitimate, compliant collection agency will immediately update your file to flag the work phone number as “Do Not Call.” They understand the legal liability of ignoring this specific instruction.

If they call your workplace again after you have explicitly told them not to, they have committed an FDCPA violation. Each subsequent call to your job becomes a documentable offense. This is where your own record-keeping becomes your best defense.

Get into the habit of logging every interaction. Simply tell them the calls are prohibited, write down the exact date, time, and the agent’s name in a notebook, and if they call back, follow up with a formal written cease communication request.

It is crucial to understand what stopping workplace calls does not do. It only protects your workplace. It does not stop them from calling your personal cell phone, your home phone, or sending you letters. If you want to block them from reaching your personal numbers entirely, you need to execute a broader strategy, which you can learn about in our guide on how to stop debt collector calls completely.

You also need to be aware of the rules limiting their overall call volume. Even if they are calling your cell phone instead of your work phone, they cannot call you fifty times a week. To understand these limits, review how many times a debt collector can legally call you.

Common Mistakes When the Collector Calls Work

Because these calls trigger panic, consumers often make mistakes that either damage their legal position or prolong the harassment. Here are the most common errors I have seen people make when these calls hit your workplace.

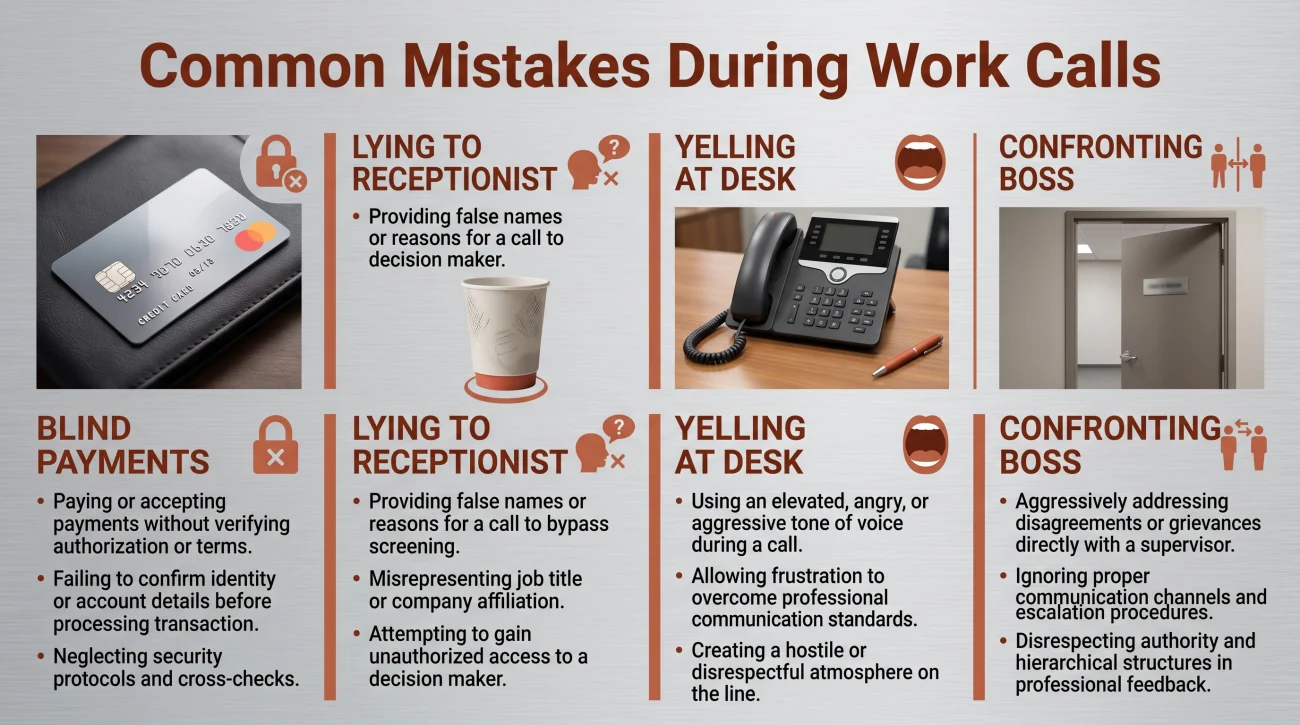

- Panicking and making a blind payment: The pressure of a coworker listening in often makes people blurt out a promise to pay or offer a credit card number just to get the collector off the phone. Never make a payment under duress. Paying without validating the debt or checking the statute of limitations can legally revive a dead debt.

- Lying to the receptionist: If a collector leaves a message, do not create elaborate lies for your receptionist about who the caller was. Keep it simple. Say it is a personal matter and you will handle it. Over-explaining often draws more suspicion.

- Engaging in a screaming match at your desk: Yelling at a debt collector from your cubicle is exactly what they want. It proves they have found a pressure point, and it guarantees your coworkers will hear about your financial troubles. Stay perfectly calm, state the prohibition policy, and disconnect.

- Confronting your employer: Some consumers get so nervous they preemptively go to their boss to explain the collection calls. Unless you are applying for a security clearance or a specific financial role, your personal debts are not your employer’s business. Handle the collector; do not overshare with management.

Signs the Workplace Call Crossed a Legal Line

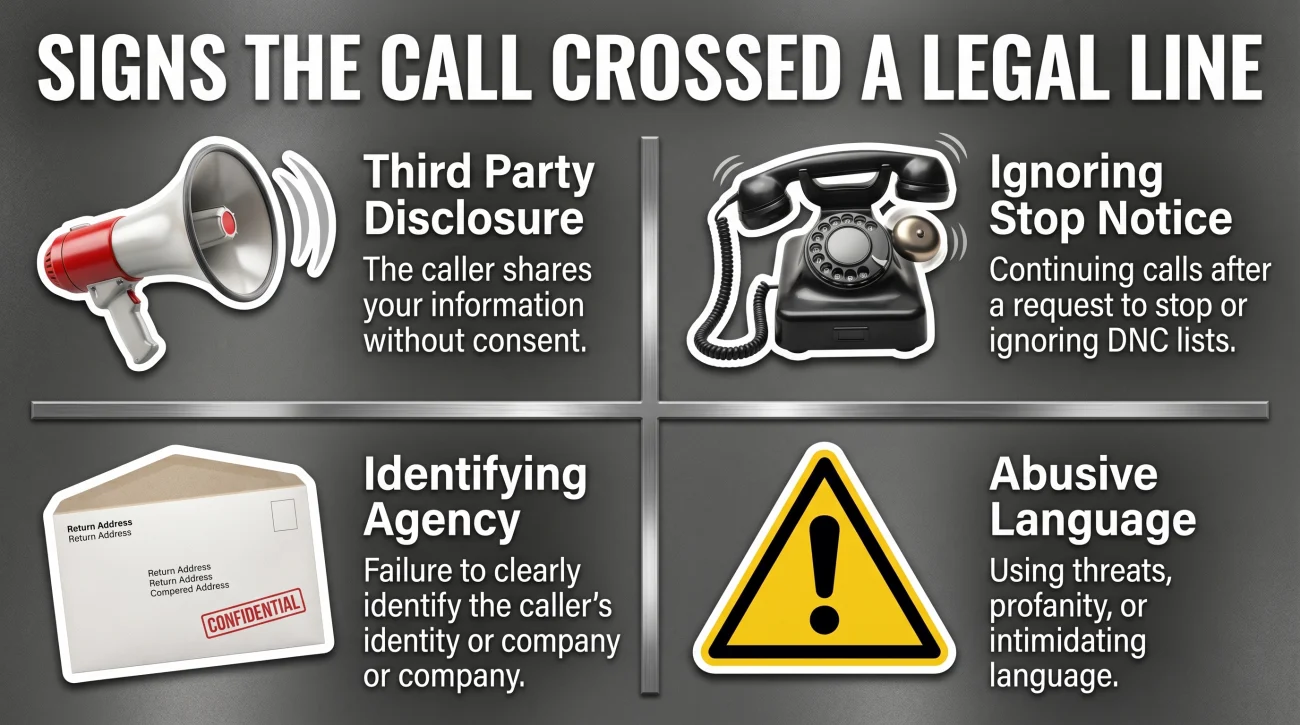

Knowing that they are allowed to call your work is one thing. Knowing when they have broken the law while doing it is another. The FDCPA provides strict protections, and collectors who rely on intimidation frequently violate them. If you are experiencing aggressive workplace contact, you need to evaluate if their actions have crossed into illegal harassment.

Here are the clear signs that the collector has violated your federal rights at your job:

- ⚠️ The collector told a coworker or your boss about the debt. If they disclosed that you owe money to anyone other than you, this is a major third-party disclosure violation.

- ⚠️ They called your workplace again after you told them to stop. Once you state that personal calls are prohibited, a second call is an immediate FDCPA violation.

- ⚠️ They identified themselves as a collection agency to a third party. Even if they did not mention the debt explicitly, leaving a message saying “Please have him call Smith Debt Recovery” is illegal.

- ⚠️ They used threatening or abusive language with the person who answered the phone. Harassing a receptionist to get to you is strictly prohibited.

If any of these scenarios apply to your situation, the collector has handed you significant legal leverage. Documenting these violations is the first step toward holding abusive agencies accountable for illegal tactics. If you believe your rights have been violated and the pressure is threatening your job, you should seriously evaluate your options with professional help. Learn more about your options by reviewing our comprehensive guide on how to handle debt collector harassment.

Final Thoughts: Protecting Your Professional Life

Stopping a workplace call solves the immediate crisis, but it does not erase the underlying account. Now that you know how to protect your professional life, your next step is to address the debt itself on your terms.

Take control of the narrative. Document the interaction, monitor your credit report, and evaluate whether the collector has provided proper validation of the balance they claim you owe. Understanding the full scope of your federal protections is your best defense against an industry that thrives on consumer confusion. You can explore those broader rights by reading our overview of debt collection laws, and you can understand how they are allowed to reach out to you elsewhere by checking the general collector contact rules.

❓ FAQ

📞 Can a collection agency call my boss directly?

Yes, they can call the main company line and end up speaking to your boss if your boss answers the phone. However, they can only ask for your location information. They are strictly prohibited from telling your boss that you owe a debt or identifying themselves as debt collectors.

🚫 Do I have to tell them in writing to stop calling my job?

No. Under the FDCPA, a verbal statement that your employer prohibits personal calls is enough to legally require them to stop calling your workplace. Written notice is always better for your own records, but verbal notice is legally sufficient to trigger the protection.

🗣️ What if the debt collector leaves a voicemail at work?

If you have a personal, direct-dial voicemail at work that only you can access, they can leave a message. However, the message cannot be deceptive. If they leave a message on a shared line or desk phone where a coworker could easily overhear it, the collector risks a third-party disclosure violation. Document exactly what the message said and who heard it.

🏢 Can I get fired because a debt collector keeps calling?

Employers can and do fire people over repeated disruptive calls, which is why stopping this fast matters. This is exactly why you need to immediately inform the collector that personal calls are prohibited, halting the disruption before it jeopardizes your job.

📱 Does stopping work calls stop them from calling my cell phone?

No. Informing a collector that they cannot call your workplace only protects that specific phone number. They are still legally permitted to call your personal cell phone or home phone unless you send a formal, written Cease and Desist letter requesting them to stop all communication.

🤐 What if my coworker found out about my debt from the caller?

If the debt collector explicitly told your coworker that you owe a debt, or identified themselves as calling from a collection agency regarding an unpaid bill, they have committed an FDCPA violation. You should document exactly what was said and when, as you may have grounds for legal action.

⚖️ Do I need a lawyer if they called my job?

If they simply called and asked for you, no. That is initially legal. However, if they called repeatedly after you told them to stop, or if they disclosed your debt to your employer, you should consult a consumer protection attorney, as these are actionable federal violations.

The full FDCPA framework and the four areas where it matters most.

- Your legal rights when collectors call, write, or threaten to sue

- When they can call, what they cannot say, and how to make it stop

- How to identify FDCPA violations and what you can do with them

- Why the age of a debt determines what a collector can legally do

- Your right to demand proof before paying or acknowledging anything

Harassment is one thing. Lawsuits, garnishments, and frozen accounts are another.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.