- The Fair Debt Collection Practices Act does not explicitly ban collectors from visiting your home, but it is extremely rare for unsecured consumer debt.

- When a collector says they are sending someone to your house, it is almost always a psychological bluff designed to create panic and force an immediate payment.

- If someone actually shows up, it is likely a process server delivering a lawsuit summons, not a collector asking for cash. Dodging a process server is a critical mistake.

- Threatening to send someone to your home when they have no actual intention of doing so is a violation of federal law.

The Reality Behind the Doorstep Threat

I am going to send a field agent to your home or place of employment to secure these funds. If you have ever heard a variation of that sentence over the phone, your heart rate probably spiked immediately. Debt collectors know exactly how terrifying the idea of a stranger showing up at your front door can be. It invades your safe space, it threatens to expose your financial struggles to your neighbors or family, and it forces a physical confrontation.

During my twelve years working inside third-party collection agencies and a national debt buyer, I saw agents use this specific threat frequently. They use it because it works. The fear of a physical visit drives people to pull out their credit cards and agree to payments they cannot afford just to keep the imaginary agent away.

But there is a massive gap between what a collector implies on the phone and what the agency is actually willing to do in the real world. You need to understand how the collection industry operates behind closed doors. Once you see the financial and legal realities of sending someone to your house, the threat loses its power. This guide will walk you through what the law actually says, why the threat is almost always a bluff, and exactly what to do if someone does knock on your door.

Is It Legal for a Debt Collector to Come to Your House?

Most people assume that physical visits from debt collectors must be illegal. The truth is more nuanced. The Fair Debt Collection Practices Act (FDCPA) is the federal law that governs third-party debt collectors. Surprisingly, the FDCPA does not contain a specific clause that outright bans a debt collector from knocking on your front door.

Technically speaking, in-person contact is permitted. However, the exact same strict rules that apply to a phone call apply to a physical visit. If a collector were to show up at your home, they would be bound by severe restrictions regarding time, privacy, and harassment.

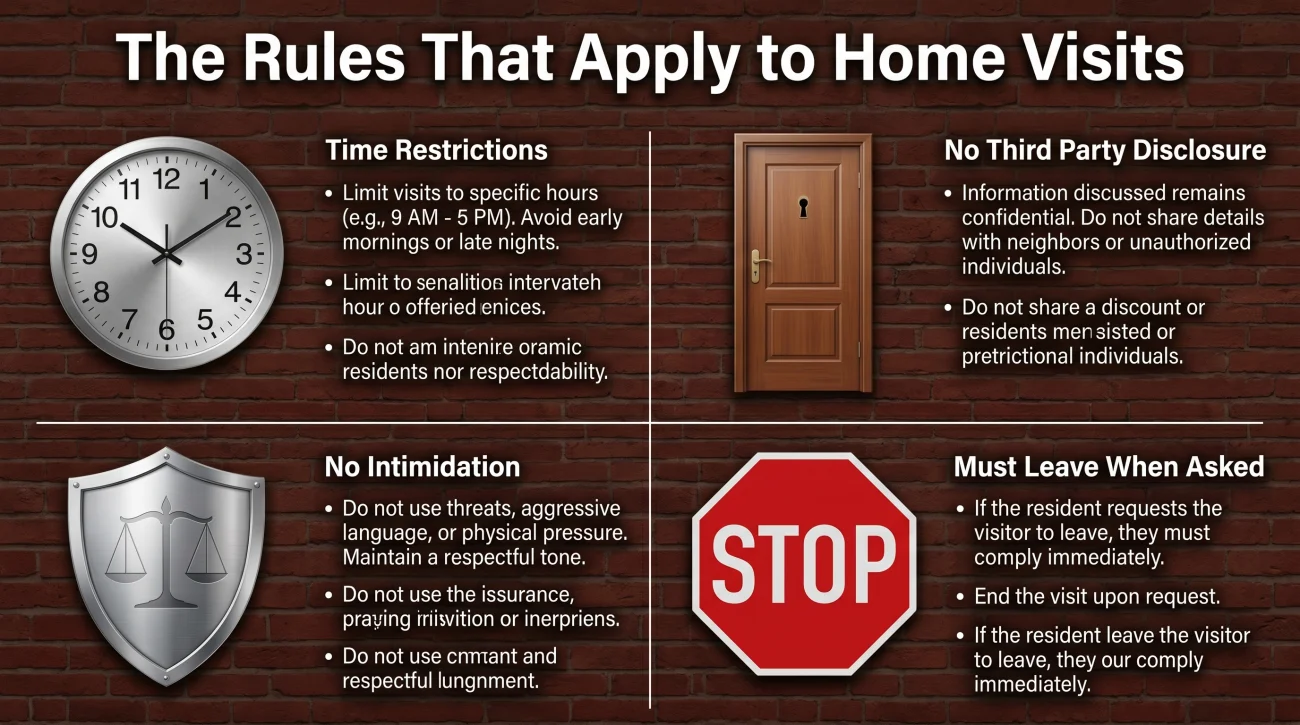

The Rules That Apply to Home Visits

If an agency actually decided to send a representative to your property, that representative must follow the strict boundaries of federal law. Understanding these rules is crucial if you want to know understanding federal debt collection laws effectively.

- They cannot visit before 8:00 AM or after 9:00 PM in your local time zone.

- They cannot discuss your debt with anyone else who answers the door, such as a roommate, child, or visiting family member. Doing so would be an illegal third-party disclosure.

- They cannot use physical force, intimidation, or abusive language while on your property.

- They must leave immediately if you ask them to leave. Refusing to leave your property constitutes trespassing.

So, while the law does not strictly forbid the visit itself, it places a minefield of legal liability around the interaction. This liability is the first clue as to why physical visits for standard consumer debts are incredibly rare.

Why the Doorstep Threat is Almost Always a Bluff

If the law allows it, why do I say it almost never happens? The answer comes down to simple economics and risk management. Third-party debt collection is a volume business. It operates on incredibly tight margins.

When a collection agency buys a portfolio of old credit card or medical debt, they might pay just pennies for every dollar owed. Their business model relies on a single collection agent making hundreds of phone calls per day using automated dialing software. The agent sits in a cubicle with a headset. They are judged on their calls per hour and their total daily revenue.

In the call centers I managed, pulling an agent off the phones, paying for their gas, insuring them for field work, and sending them driving across town for an hour to knock on one door to ask for a $600 medical bill was financially absurd. The return on investment does not exist.

The Compliance Nightmare

Beyond the cost of travel, physical visits are a compliance nightmare for collection agencies. On a phone call, the agency records everything. If a consumer claims the agent threatened them, the agency can pull the audio file to verify exactly what was said. This protects the agency from frivolous lawsuits.

At a front door, there is no verified recording. If a field agent shows up, gets frustrated, and yells something abusive, or accidentally mentions the debt to your neighbor who is walking by, the agency is completely exposed. One wrong sentence at your doorstep can result in an FDCPA lawsuit that costs the agency far more than the debt is even worth. Agencies have compliance departments, and compliance departments absolutely hate unrecorded field visits.

Because the cost is high and the legal risk is enormous, agencies rely entirely on phone calls, letters, and occasionally digital communication. To see how these other methods are regulated, you should review the the complete rules for collector contact.

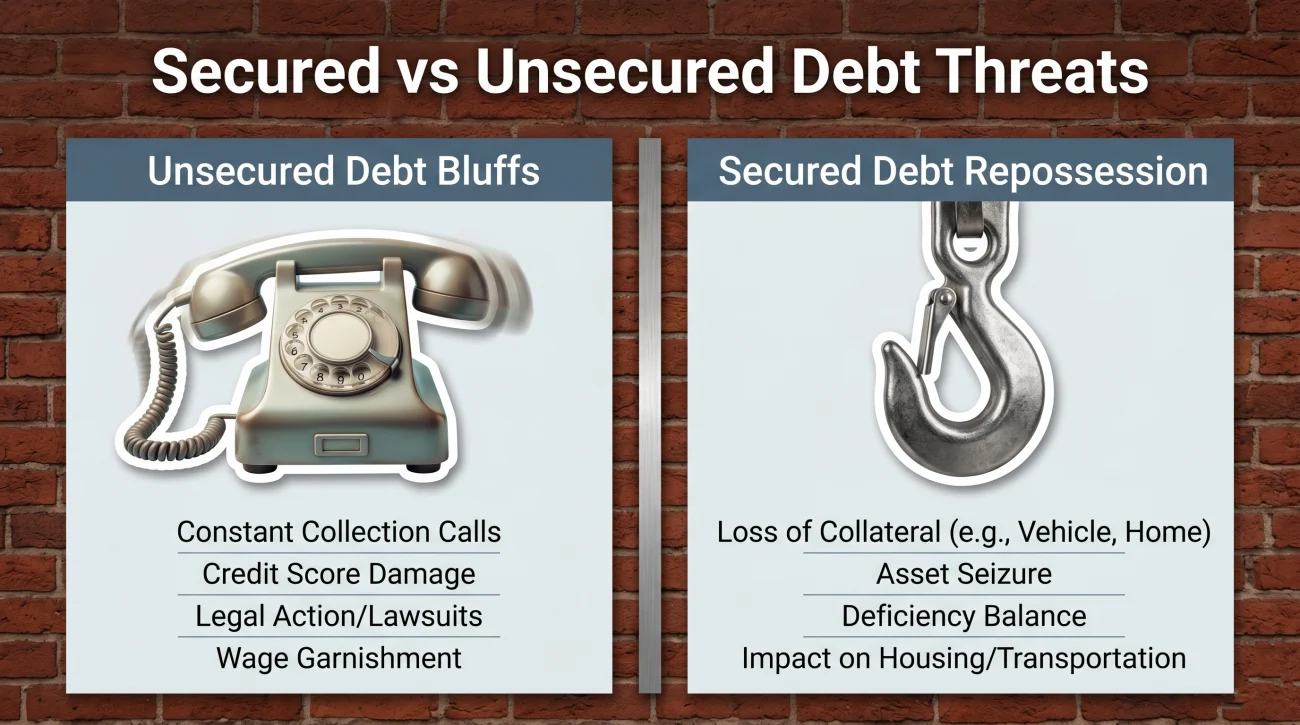

Secured Debt vs. Unsecured Debt: The One Exception

All of that said, there is one scenario where someone absolutely will show up, and it has nothing to do with bluffing. You must know exactly what type of debt you are dealing with, because the rules change completely if the debt is tied to physical property.

The vast majority of threats about sending someone to your house involve unsecured debt. This includes credit cards, medical bills, student loans, and payday loans. For these debts, there is no physical property for the creditor to take back. The threat of a visit is purely psychological.

However, if you are dealing with secured debt, someone absolutely will come to your house. Secured debt includes auto loans, title loans, and rent-to-own furniture. If you stop paying your car note, the lender will send a repossession agent to your home or workplace to take the vehicle. The repo agent is not there to ask you for a payment or discuss your account balance. They are there to take the collateral.

The collector on the phone threatening to send an investigator to your home is bluffing to scare you into making a payment.

The bank does not need to bluff. They will quietly send a tow truck to your driveway in the middle of the night to reclaim the vehicle.

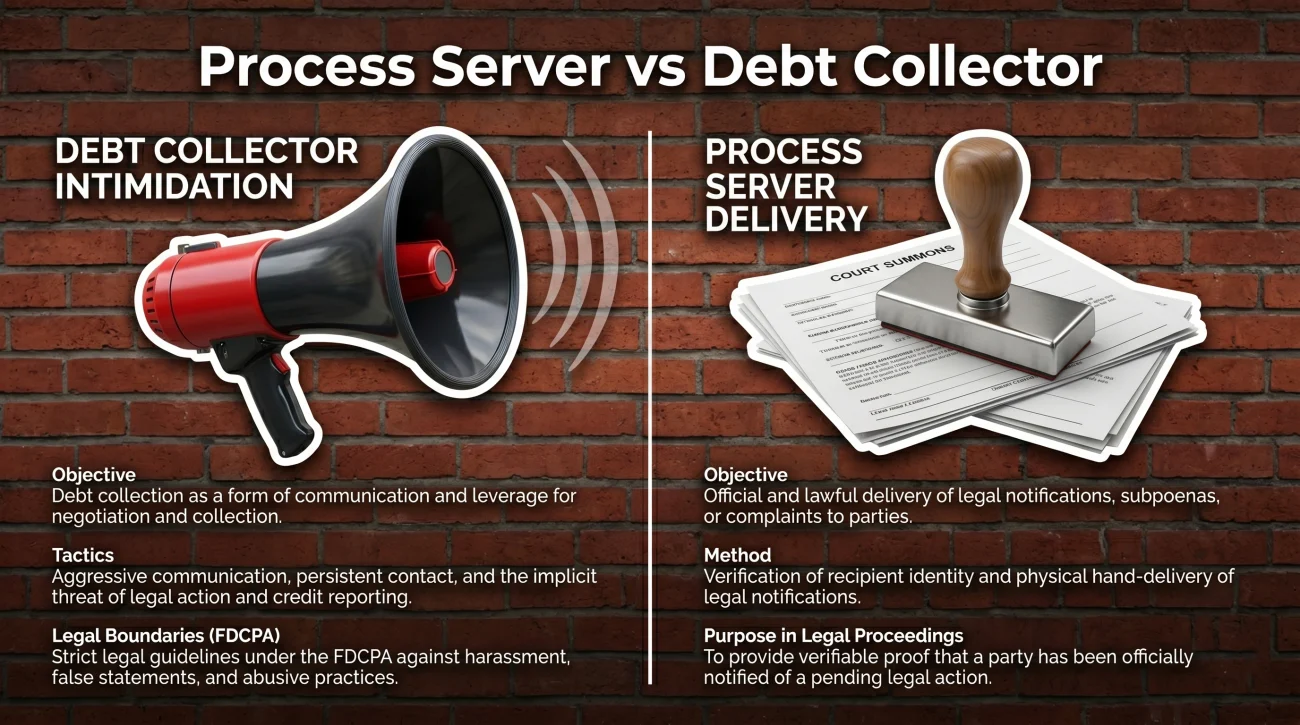

Process Server vs. Debt Collector: Know the Difference

This is where consumers get dangerously confused. While a debt collector is not going to show up at your house to ask for money, a process server absolutely will show up to deliver legal documents. You must understand the difference, because reacting to a process server the wrong way can ruin your finances.

A process server is not a debt collector. They are an independent courier, often licensed by the court or the state, whose only job is to physically hand you a lawsuit summons. They do not care about your debt, they do not want your money, and they have no authority to negotiate a settlement with you.

Why You Must Never Ignore a Process Server

If a debt collector decides to take legal action against you, they will file a lawsuit. The court requires that you be formally notified of this lawsuit. That notification is the summons, and the process server is the person bringing it to your door.

📌 Note: Hiding from a process server or refusing to open the door does not make the lawsuit go away. In many jurisdictions, if the server can prove they made a reasonable attempt to serve you, the judge will allow alternative service (like mailing it or leaving it with an adult relative). If you ignore the lawsuit entirely because you refused the papers, the collector will easily win a default judgment against you.

| The Visitor | Their Goal | Your Required Action |

|---|---|---|

| Debt Collector | To intimidate you into paying an unsecured debt | Do not engage. Send a written cease communication notice. |

| Repossession Agent | To physically secure collateral (your vehicle) | Remove personal items. Do not breach the peace. |

| Process Server | To deliver a court summons for a filed lawsuit | Accept the documents. Note the deadline. Contact a defense attorney. |

How to Respond to the Threat on the Phone

When an agent tells you they are dispatching someone to your location, your reaction dictates what happens next. If you panic, they know they have leverage. If you stay calm and call their bluff, they lose their primary weapon.

In the collection industry, we call this the “escalation script.” The agent wants you to believe that the situation is moving out of the call center and into your physical life. They will often use official-sounding but meaningless titles. They will say they are sending a “field investigator,” a “location specialist,” or an “asset verification officer.” These are just fabricated titles designed to sound like law enforcement.

When I coached people through this, the approach that consistently shut it down fastest went something like this.

Collector: “Since you are refusing to resolve this voluntarily, I am marking your file for field dispatch. An investigator will be sent to your home or place of employment tomorrow between 9 AM and 1 PM to verify your assets.”

You: “Are you a process server delivering a lawsuit summons?”

Collector: “I am a recovery agent, and the investigator will be there to secure the funds.”

You: “I know my rights under the FDCPA. You are not allowed to use false threats. I am requesting that all communication be in writing by mail. Do not call this number again, and do not contact me at my workplace.”

By asking if they are a process server, you immediately show that you understand the legal system. By instructing them not to call your workplace, you shut down their secondary leverage. You can learn more about why they frequently call your workplace and how to stop that specific tactic.

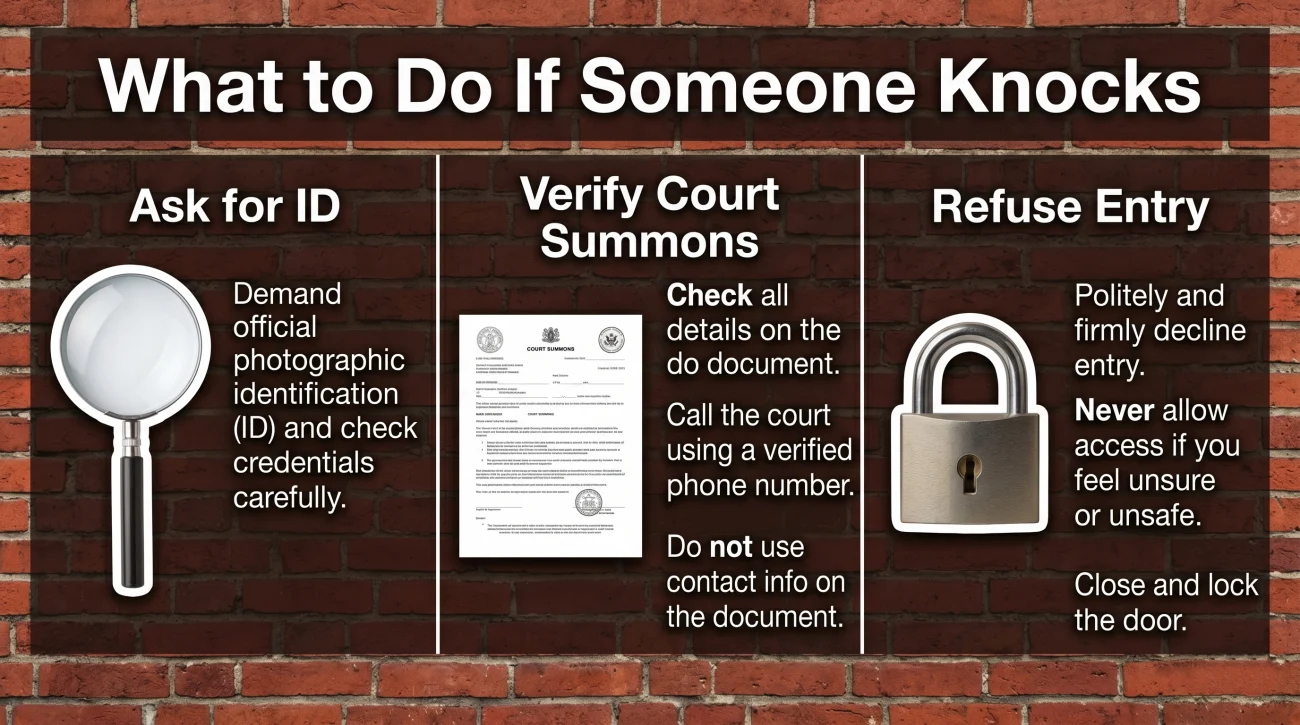

What to Do If Someone Actually Knocks on Your Door

Even though it is exceptionally rare for an unsecured debt collector to visit, you need a plan just in case. If someone knocks on your door and claims to be looking for you regarding a financial matter, follow these strict rules to protect yourself.

First, you have no legal obligation to open your door to a stranger. You do not have to answer questions. You do not have to confirm your identity through a closed door.

If you choose to speak to them through the door or a camera system, keep it brief and clinical.

- 📋 Step 1: Ask for identification. “Who are you and what company do you represent?”

- 📋 Step 2: Apply the same principle as on the phone. Ask if they are a process server delivering court documents. If they are, accept the paperwork. If they admit they are a debt collector asking for money, move immediately to step three.

- 📋 Step 3: Shut down verbal engagement. Say: “I do not discuss financial matters at my home. Leave your company’s mailing address in my mailbox and I will request validation in writing. Please leave my property immediately.”

💡 Pro Tip: Do not let a debt collector inside your home under any circumstances. Do not write them a check at the door. Do not confirm your banking information. Their presence at your door is an intimidation tactic. Paying them validates that the intimidation worked.

The FDCPA Violation: Threatening an Action They Will Not Take

This is the most important legal concept regarding doorstep threats. Under federal law, threatening to take an action a collector has no actual intention of taking is itself a violation.

Because third-party collection agencies have no actual infrastructure to send field agents to your home, a threat to do so is an empty threat. Making an empty threat to coerce a payment is a direct violation of federal law.

Key Point: The violation is not that they came to your house. The violation is that they told you they were coming when they never had any intention of doing so. They lied to cause emotional distress.

If an agent uses this tactic against you, you need to document it immediately. Write down the date, the time, the phone number they called from, the name the agent gave, and exactly what they said regarding the home visit. This documentation is essential if you decide to escalate the issue.

If you want to stop the agency from communicating entirely, sending a formal written request is your best option. You can read the exact process to legally stop debt collector calls using a cease and desist letter.

Signs the Home Visit Threat Has Crossed a Legal Line

Dealing with debt is stressful enough without feeling physically threatened in your own home. It is critical to recognize when a collector’s behavior moves from aggressive posturing into illegal harassment. If you are experiencing any of the following scenarios, the agency is likely violating federal law.

- ⚠️ The caller implied they were sending law enforcement or police to your home to arrest you for the debt. This is one of the most common escalations I heard on the floor, almost always deployed against older consumers who are less familiar with how civil debt works.

- ⚠️ The agent stated they were sending an “investigator” to speak with your neighbors about your whereabouts. I have seen collectors use this specifically to leverage the fear of public embarrassment.

- ⚠️ A collector actually showed up and refused to leave your property when instructed, or used abusive language at your door.

- ⚠️ The caller claimed to be a process server coming to your home, but no lawsuit has actually been filed against you.

- ⚠️ The agency is repeatedly calling and leaving voicemails threatening physical visits to extort immediate payment over the phone.

If you recognize these patterns, knowing the rules is no longer enough. You need to assess whether the abuse warrants professional intervention. A persistent pattern of false threats creates real legal leverage for the consumer. You should take a moment to evaluate if you are experiencing illegal harassment and explore your options for holding the agency accountable.

Final Thoughts: Controlling the Narrative

The threat of a home visit relies entirely on the element of surprise and the fear of public embarrassment. Once you understand the basic economics of why agencies stay on the phones, the threat evaporates.

If you receive this threat, treat it as what it is: a desperate attempt by a call center employee to force a payment. Document the conversation, refuse to be intimidated, and force the collector back into the written validation process. If a lawsuit is eventually filed, a legitimate process server will bring you the paperwork, and you can handle that through the proper legal channels. Until then, your front door remains yours, and debt collectors have no power over it.

For more details on frequency restrictions, you can check how many times they can legally call you before it becomes harassment.

❓ FAQ

🚪 Can a collection agency send someone to my house?

Technically yes, the FDCPA does not ban physical visits. However, for unsecured consumer debt like credit cards or medical bills, it is exceptionally rare due to travel costs and massive legal liability.

🚔 Can a debt collector bring the police to my house?

No. Unpaid consumer debt is a civil matter, not a criminal one. Debt collectors have no authority to involve local law enforcement, and police do not assist in collecting civil debts.

🚗 What if the debt is for a car loan I stopped paying?

Auto loans are secured debt. In this scenario, the lender will send a repossession agent to your home or workplace to take the vehicle. This is legal and highly likely to happen.

📜 How do I know if the person at my door is a process server?

A process server’s only job is to hand you legal documents regarding a filed lawsuit. They will not ask you for money, they will not negotiate a settlement, and they usually want to leave as quickly as possible.

🚫 Do I have to open the door for a debt collector?

No. You have no legal obligation to open your door, invite them inside, or answer their questions. You can simply ask them to leave their information in the mailbox and depart.

🗣️ Can a collector tell my neighbors about my debt?

Absolutely not. Disclosing your debt to a third party, including your neighbors, is a severe violation of the FDCPA. They can only contact a neighbor once to acquire your location information, and they cannot mention the debt.

⏰ What hours are collectors allowed to visit?

If a collector were to visit, they must obey the same time restrictions as phone calls. They cannot visit before 8:00 AM or after 9:00 PM in your local time zone.

🤥 Is it illegal for a collector to threaten a visit they won’t make?

Yes. Federal law prohibits empty threats. If a collector says they are sending someone to your home but has no real intention of doing so, that threat itself is a violation.

🛑 How do I legally ban a collector from my property?

You can tell them verbally to leave, which they must do. To prevent future contact, send a written cease and desist letter by certified mail to the collection agency.

📞 Should I call them back if they leave a note on my door?

Do not call them back immediately. Verify the name of the agency, check your credit report for the debt, and handle all communications by mail to maintain a written record and protect your rights.

The full FDCPA framework and the four areas where it matters most.

- Your legal rights when collectors call, write, or threaten to sue

- When they can call, what they cannot say, and how to make it stop

- How to identify FDCPA violations and what you can do with them

- Why the age of a debt determines what a collector can legally do

- Your right to demand proof before paying or acknowledging anything

Harassment is one thing. Lawsuits, garnishments, and frozen accounts are another.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.