- Yes, debt collectors can legally text you. The CFPB’s Regulation F explicitly permitted text messaging and email contact starting in late 2021.

- Every legitimate collection text must include a clear, simple way to opt out.

- Legitimate collectors will never ask you to pay via gift cards, cryptocurrency, or wire transfers via text message. If they do, it is a scam.

- Opting out revokes their permission to text you, but it does not erase the debt or stop them from calling or mailing you letters.

That Text Message Isn’t a Mistake: It’s the New Collection Standard

You are looking at your phone, staring at a text message from a number you do not recognize, claiming you owe a debt. If your first instinct is to assume it is a phishing scam or someone pulling a prank, you are not alone. For years, the idea of a debt collector sliding into your text messages felt completely off-limits. But the landscape of debt collection has shifted dramatically, and the short answer to the question “can debt collectors text you” is a definitive yes.

I spent 12 years inside third-party collection agencies and a national debt buyer. For most of my career, texting a consumer was considered a massive compliance risk. We simply did not do it. The legal gray areas were too broad, and the potential for federal violations was too high. But that all changed in late 2021. Today, text messaging is one of the fastest-growing contact methods in the industry.

If you are receiving text messages from a debt collector, you need to understand the strict rules they are required to follow, how to identify when a text crosses the line into a scam, and the exact steps to make the notifications stop.

The 2021 Regulation F Update: Why Your Phone is Suddenly Buzzing

To understand why you are suddenly getting debt collection texts, you have to look at the federal debt collection law framework, specifically the Fair Debt Collection Practices Act (FDCPA). When the FDCPA was written in 1977, text messages obviously did not exist. For decades, the law was interpreted through the lens of phone calls and physical mail.

In November 2021, the Consumer Financial Protection Bureau (CFPB) implemented a major update known as Regulation F. This update modernized the rules and explicitly authorized debt collectors to use electronic communications, including text messages and debt collection emails. The ambiguity was removed. Overnight, agencies that had been hesitant to text consumers began rolling out massive, automated text campaigns.

“From an operational standpoint inside an agency, texts are incredibly effective. A phone call can be ignored or sent to voicemail, but almost everyone looks at a text message within minutes of receiving it. It forces engagement without the immediate confrontation of a voice call. We knew that a well-timed text often generated a faster online payment than three weeks of dialer campaigns.”

However, this new permission slip came with a very strict set of boundaries. Collectors cannot simply text you whenever and however they want. They must follow a rigid compliance structure.

The Specific Rules Governing Debt Collection Texts

While the medium has changed, the underlying consumer protections have not. Debt collectors texting you are bound by the overall rules for collector communication, plus a few text-specific mandates.

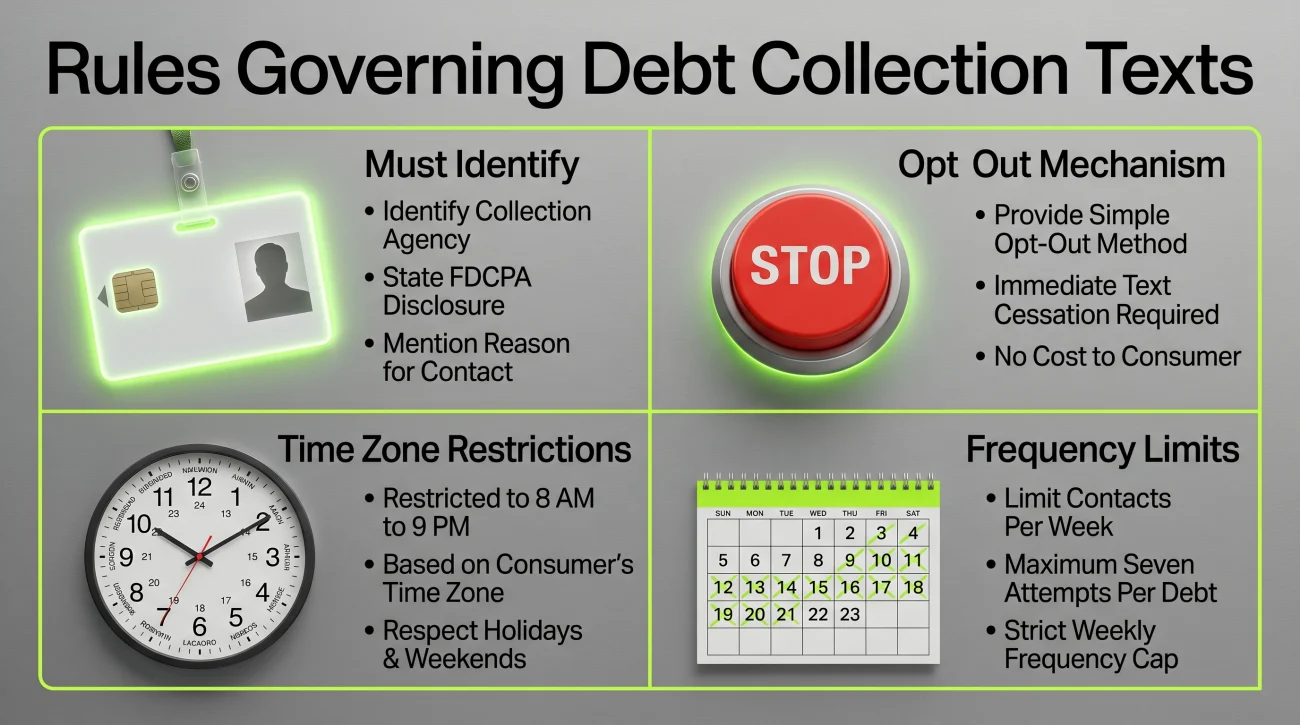

1. They Must Identify Themselves

A debt collector cannot send a vague, mysterious text that says, “Call us immediately regarding an urgent business matter.” Every text message must clearly identify that the communication is from a debt collector. This is part of the required “Mini-Miranda” disclosure.

2. The Mandatory Opt-Out Mechanism

This is the most critical rule under Regulation F: every single text message from a debt collector must include a clear, simple way for you to opt out of future text communications. If a collector sends you a text without providing a way to unsubscribe from that channel, they are breaking the law.

3. Time Zone Restrictions Still Apply

The FDCPA prohibits collectors from contacting you at inconvenient times or places, which is legally defined as before 8:00 a.m. or after 9:00 p.m. in your local time zone. This applies to text messages just as strictly as it applies to phone calls. A text message delivered to your phone at 11:30 p.m. is a documentable violation.

4. The Frequency Loophole

You might have heard of the “7-call rule,” which prevents a collector from calling you more than seven times in seven days about a specific debt. Interestingly, this numeric limit does not explicitly apply to text messages or emails. However, the overarching prohibition against harassment, oppression, and abuse still applies. If a collector texts you fifteen times in a single day, they are almost certainly crossing the line into FDCPA harassment. If this happens, you should immediately take screenshots of your text log showing the timestamps. This establishes a documented pattern of harassment that you can use in an FDCPA complaint or lawsuit.

What If the Text Is for a Debt That Isn’t Yours?

Many consumers receive debt collection texts addressed to someone else, often a person with the same name, or the previous owner of your cell phone number. Because debt is bought and sold in bulk portfolios, the phone numbers attached to accounts are frequently outdated or simply wrong.

If you receive a text for someone else’s debt, your instinct might be to reply and explain the mistake. Do not do this. Any engagement beyond a simple opt-out command can sometimes trigger the system to flag your number as “active,” leading to more calls and texts from other agents working the same file. Use the opt-out mechanism provided in the text. If the messages continue after that, it transitions from an administrative error into an actionable FDCPA violation.

How to Tell if a Debt Collection Text is Real or a Scam

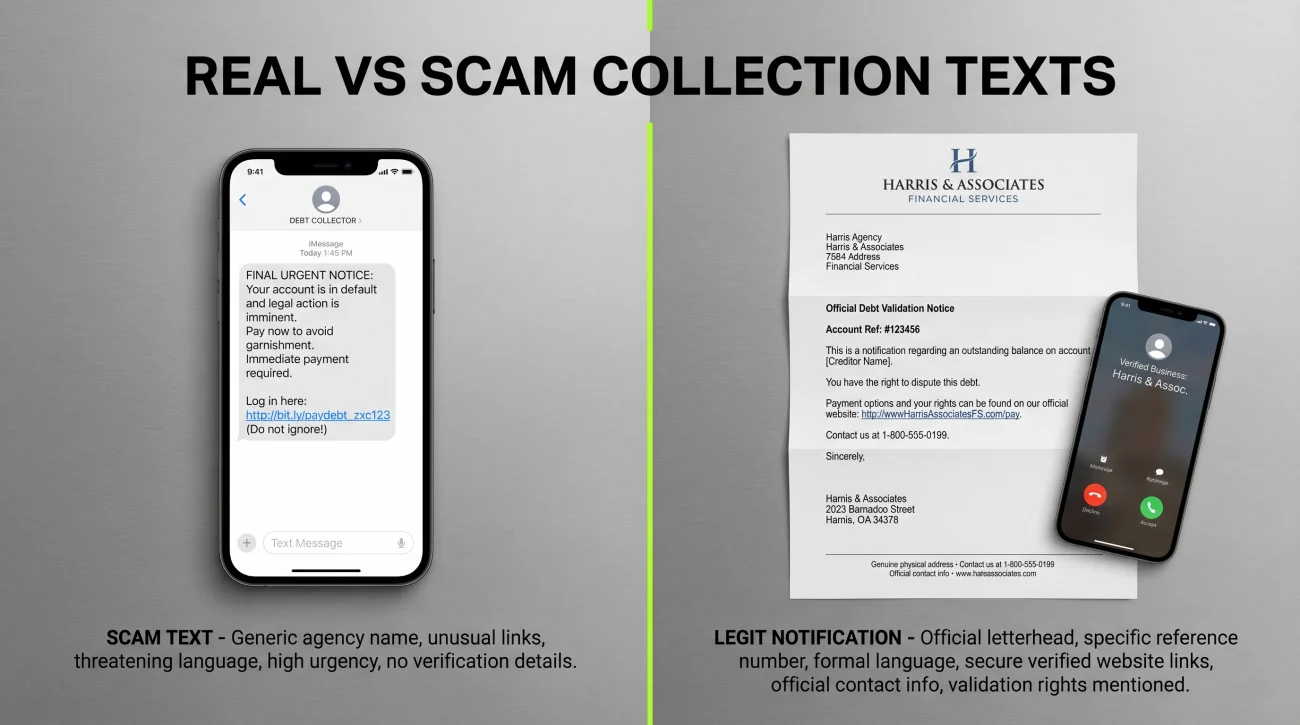

When an unexpected text demands payment, the first question most people ask is: “How do I know this isn’t a scammer trying to steal my information?” This is a highly valid concern. Because legitimate collectors are now texting, scammers use the exact same channel to impersonate them, hoping you will panic and click a malicious link.

In my experience, legitimate collection agencies are terrified of compliance audits. Their text messages are usually dry, formal, and strictly follow the regulatory script. Scammers, on the other hand, rely on urgency, threats, and emotional manipulation.

“URGENT: Legal action has been filed against you. An arrest warrant will be issued in 24 hours for unpaid debt. Click here immediately to pay via Apple gift card or Crypto to cancel the warrant: [suspicious link]”

“This is [Agency Name], a debt collector. We are attempting to collect a debt. Please call us at 800-555-0199 or visit [Secure Agency Website]. Reply STOP to opt out of text messages.”

Here are the definitive red flags that indicate a debt collection text message is actually a scam:

- ⚠️ Unusual Payment Methods: Legitimate collection agencies will never ask you to pay a debt using iTunes gift cards, CashApp, Zelle, cryptocurrency, or wire transfers. If a text demands payment through these untraceable methods, block the number immediately.

- ⚠️ Threats of Arrest: You cannot be arrested for unpaid consumer debt (like credit cards or medical bills) in the United States. Any text threatening jail time or police action is a scam.

- ⚠️ No Company Name Provided: Legitimate agencies must identify themselves. Scammers often use generic terms like “The Legal Department” or “Collection Bureau” without giving a specific, searchable corporate name.

- ⚠️ Sketchy Links: Be incredibly wary of clicking links in texts. A legitimate agency will direct you to a secure, professional web portal. Scammers use shortened URLs (like bit.ly) or websites with strange spellings to steal your personal information.

💡 Pro Tip: If you receive a text and you are unsure if it is real, do not click anything and do not reply. Instead, check your credit report. If the debt is legitimate, the original creditor or the collection agency should be listed there. Call the number on your credit report, not the number that texted you.

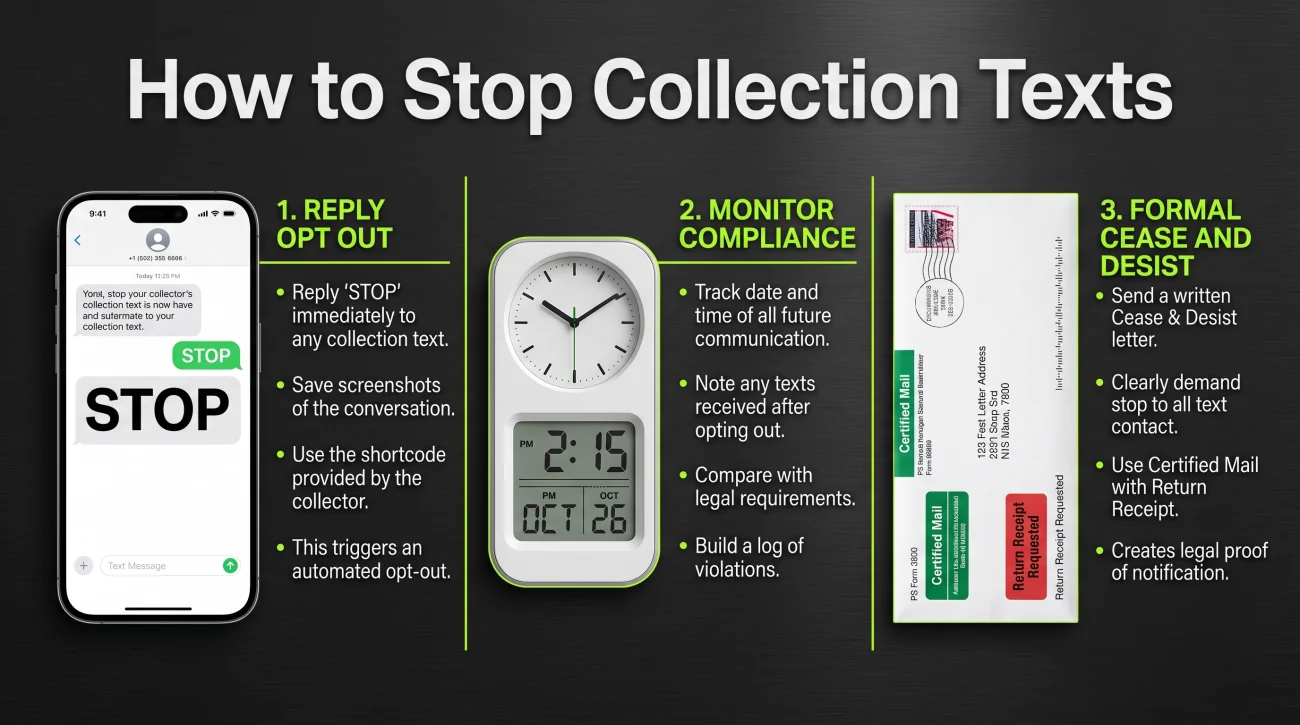

How to Stop Debt Collector Texts (Without Making Things Worse)

Whether you have verified the collector is legitimate or you simply want an unrecognized agency out of your inbox, you have absolute control over this channel. Regulation F made the opt-out process relatively straightforward.

The fastest method is to use the opt-out instruction provided in the text itself. In almost all cases, this means replying with a single word, usually “STOP.”

Action: Reply with the opt-out word + Document the time you sent it + Monitor for compliance

Once you send that text, their automated system should flag your number and remove it from their active SMS campaign list. From an insider perspective, understand that there is sometimes a slight system lag. Depending on how the agency processes their data batches, it might take a few hours for the system to fully update. They are permitted to send you one final text confirming that you have been opted out, but after that, the texts must cease entirely.

Key Point: Opting out only revokes their permission to contact you via text message. It does not mean you have opted out of phone calls, physical mail, or contacting you privately on social media. It also does not erase the debt.

If you want to stop all forms of communication, a text opt-out is not enough. You must send a written cease and desist request to stop all communication. This requires sending a formal letter via certified mail.

⚠️ Warning: Do not use the text thread to argue about the debt, explain your financial hardship, or demand proof. Anything you text back is recorded in the agency’s system and can be used as evidence that the phone number belongs to you and that you are engaging with the account. If you want to dispute the debt, do it in writing via physical mail.

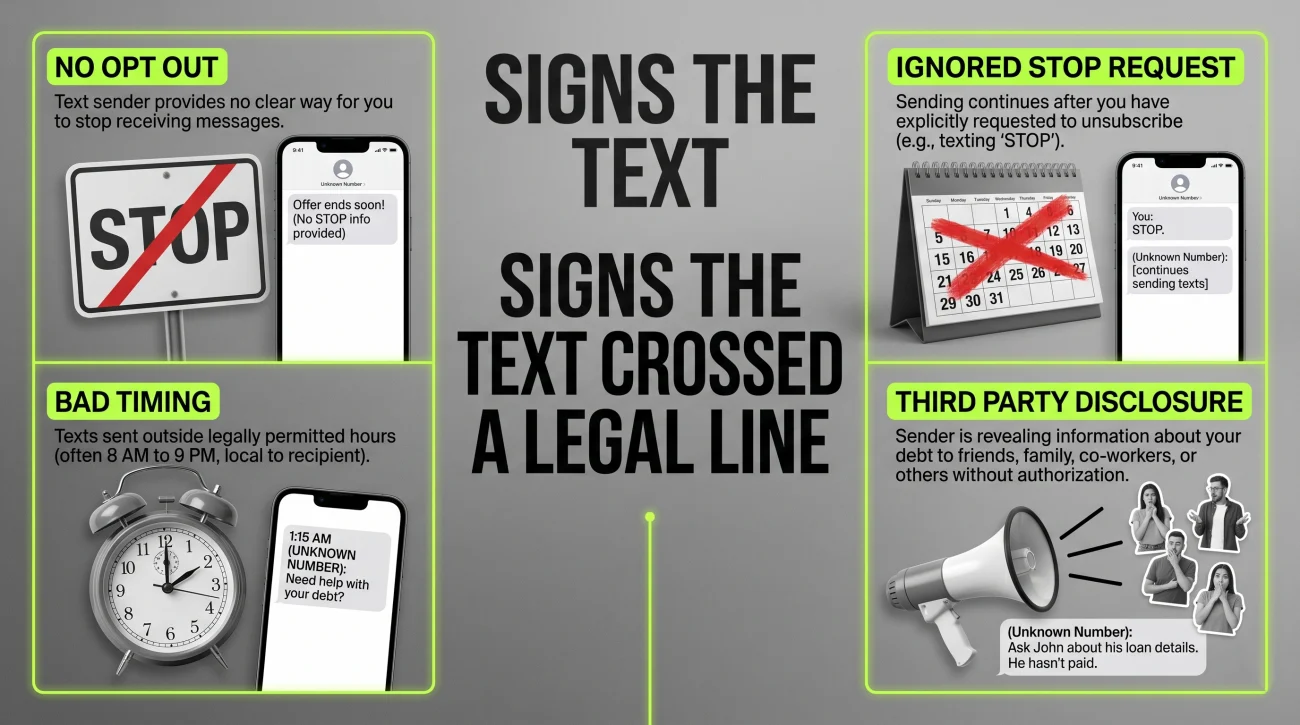

Signs the Text Message Has Crossed a Legal Line (And How to Document It)

Dealing with debt is stressful enough without a collector invading the space where you talk to your family and friends. While texting is legal, collectors frequently push the boundaries or execute their campaigns poorly, resulting in actionable violations.

You need to evaluate your situation immediately if you are experiencing any of the following:

- The collector sent a text that did not include an option to opt out.

- You followed their opt-out instruction, but the texts continued arriving days later. (A delay of a few hours is normal system lag; continued texts days later is a violation).

- The texts are arriving before 8:00 a.m. or after 9:00 p.m. in your local time zone.

- The text message included details about your debt, and it was sent to a shared family phone plan or a work phone. This is a critical third-party disclosure violation. Under the FDCPA, collectors are strictly prohibited from revealing your debt to anyone else. If your spouse or employer can read the debt notification on a shared device’s lock screen, the collector has crossed a major legal line.

How to Document Text Message Violations Correctly

If a collector commits a violation via text, do not just delete the thread out of frustration. You need to secure the evidence. Take screenshots immediately. Make sure your screenshots clearly capture the sender’s phone number at the top, the date and time the message was received, and the exact content of the text. Email these screenshots to yourself so you have a permanent, timestamped record outside of your phone.

If the contact you are receiving is crossing these boundaries, you need to evaluate what to do if you are dealing with debt collector harassment to understand your options for forcing them to back down.

Final Thoughts on Text Message Debt Collection

Your phone is your private space, and you ultimately decide who gets access to it. Federal law gives you the power to shut down debt collection texts instantly. Use that right to regain control, document any missteps the collector makes, and force the process back to formal written letters where you hold the legal advantage.

❓ FAQ

📱 Is it actually legal for a debt collector to text my cell phone?

Yes. Under the CFPB’s Regulation F, which took effect in late 2021, debt collectors are explicitly permitted to contact you via text message, provided they follow strict rules including identifying themselves and offering an opt-out option.

🛑 How do I make the debt collection texts stop completely?

You can stop texts by replying with the opt-out command provided in the message, usually “STOP.” The collector is legally required to honor this request. If they ignore it and continue texting, each subsequent message is a potential FDCPA violation.

🎣 How can I tell if a text from a debt collector is a scam?

Scam texts often threaten imminent arrest, demand payment via gift cards or cryptocurrency, fail to provide a verifiable company name, and include suspicious, shortened links. Legitimate collectors will identify themselves and provide standard payment portals.

🕰️ Can debt collectors text me late at night?

No. The time restrictions that apply to phone calls also apply to text messages. A debt collector cannot legally text you before 8:00 a.m. or after 9:00 p.m. in your local time zone.

💬 If I reply to a debt collector’s text, does it reset my statute of limitations?

It can. Depending on your state’s laws, replying to a text by acknowledging the debt or making a promise to pay can potentially restart the statute of limitations. This is why it is safer to only reply with the opt-out command or handle disputes via formal mail.

📨 Do debt collector texts count toward the 7-call rule?

No. The specific FDCPA rule that limits collectors to 7 phone calls within a 7-day period applies to voice calls, not text messages. However, sending an excessive number of texts can still be considered illegal harassment.

🔗 Should I click the link provided in a debt collection text?

You should never click a link in an unexpected text message. If you suspect the debt is real, independently look up the collection agency online or check your credit report to find their official contact information to verify the account safely.

📞 If I opt out of texts, will the debt collector stop calling me too?

No. Opting out of text messages only revokes their permission to use that specific channel. To stop all forms of communication (calls, letters, and emails), you must send a formal written cease and desist letter.

💼 Can a debt collector text my work cell phone?

Yes, unless they know or should reasonably know that it is a phone provided by your employer and that your employer prohibits such communications. If they text your work phone, reply with the opt-out command to cut off that channel.

👤 What should I do if the debt collection text is for someone else?

Do not reply to argue or explain the mistake. Simply use the opt-out command provided in the text. Engaging in a conversation can sometimes cause their system to flag your number as active, leading to more unwanted contact.

The full FDCPA framework and the four areas where it matters most.

- Your legal rights when collectors call, write, or threaten to sue

- When they can call, what they cannot say, and how to make it stop

- How to identify FDCPA violations and what you can do with them

- Why the age of a debt determines what a collector can legally do

- Your right to demand proof before paying or acknowledging anything

Harassment is one thing. Lawsuits, garnishments, and frozen accounts are another.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.