- Debt collectors are legally allowed to call you on Sundays, Saturdays, and public holidays.

- While a single weekend call is legal, the Consumer Financial Protection Bureau notes that a pattern of concentrating calls on Sundays can be used as evidence of illegal harassment.

- Collection agencies staff weekend shifts specifically because they know consumers are more likely to be home, relaxed, and easier to catch off guard.

- Never make a small “good faith” payment just to end a Sunday call, as this can legally revive a dead debt.

- You can stop these calls immediately by verbally instructing the agent that weekends are an inconvenient time for you.

The Intrusion of a Weekend Collection Call

A phone ringing on a Sunday morning usually means a family member is calling to catch up. When you answer and hear the practiced voice of a debt collector instead, the intrusion feels incredibly personal. Sunday is supposed to be a day of rest, family time, or quiet recovery before the work week begins. Having an agency pierce that boundary feels like it should be against the law.

During my 12 years working inside third-party collection agencies, I heard this reaction from consumers constantly. They would answer the phone angry, demanding to know how we got away with calling them on the weekend. The reality is that the collections industry relies heavily on weekend dialer shifts. We knew exactly what we were doing, and we knew the law allowed us to do it.

If you just received a call on a Sunday and are searching for a clear answer on whether your rights were violated, you need to understand how the federal rules actually work. The law does not protect specific days of the week, but it does heavily regulate the timing and the pattern of those calls. Knowing where the boundary is drawn is the first step to taking your weekends back.

The Short Answer on Sunday and Holiday Calls

The first thing you need to know is that yes, debt collectors can legally call you on a Sunday. They can also call you on Saturdays, and they can call you on federal holidays.

When I was managing agents on the floor, we did not care what day of the week it was. The federal framework that governs our industry, known as the Fair Debt Collection Practices Act (FDCPA), does not designate any day of the calendar as off-limits by default. The assumption under the law is that collectors have a right to attempt to reach you.

When you look closely at the broader federal debt collection laws, you quickly realize that the rules are built around timing and frequency rather than specific days. However, the fact that Sunday calls are permitted does not give agencies a free pass to harass you. All the standard consumer protections apply just as strictly on a Sunday as they do on a Tuesday.

The Strict 8:00 a.m. to 9:00 p.m. Boundary

Inside a legitimate collection agency, the automated dialing system is programmed with a hard lock. It will not allow an agent to dial your number before 8:00 a.m. or after 9:00 p.m. in your local time zone. This is because the FDCPA explicitly assumes that any time outside this 13-hour window is inconvenient.

This rule is anchored to where you live, not where the collector is located. If an agency is in New York and you live in California, they must wait until 8:00 a.m. Pacific Time to dial your number.

If a collector bypasses this and calls you at 7:30 a.m. on a Sunday morning, the violation is not that they called on a weekend. The violation is the time. This is a strict liability issue. If you are experiencing calls outside of this window, you should review the exact steps to take when a debt collector calls outside allowed hours, because that behavior is highly actionable.

How the Seven-Call Limit Applies to Your Weekend

While the daily clock is a hard boundary, the dialer system is also tracking another metric: how often we hit your number over the course of the week. Under recent federal updates, a collector is presumed to be harassing you if they call you more than seven times within a rolling seven-day period regarding a specific debt.

This limit does not pause for the weekend. In fact, aggressive weekend dialing can burn through an agency’s legal allowance very quickly. For example, if an agent calls you three times on Saturday and four times on Sunday, they have hit their legal limit for the entire week in just 48 hours. They cannot legally call you again until that rolling seven-day window begins to clear.

Furthermore, if you actually answer the phone and speak to them on a Sunday, they are not legally permitted to call you again about that same debt for another seven days. If you want to understand the loopholes agencies use to get around this numeric limit, read the complete breakdown of the 7-in-7 call rule.

Digital Weekends: Texts and Emails on Sundays

The phone ringing is not the only way collectors reach out on weekends. Since the CFPB’s Regulation F took effect in late 2021, collection agencies are explicitly permitted to send text messages and emails to consumers.

Just like phone calls, these digital communications are perfectly legal on a Sunday. However, they come with their own strict requirements. Every text message or email must include a clear and simple opt-out instruction, such as “Reply STOP to cancel.”

One interesting loophole in the current law is how the 8:00 a.m. to 9:00 p.m. rule applies to digital messages. While courts generally agree that sending a text message at midnight is a violation, emails are sometimes treated differently because they do not “ring” in the same intrusive way. Still, if an agency is blowing up your phone with texts on a Sunday night, they are walking a very dangerous legal line. Whether they use a phone call, a text message, or an email, the communication channel changes but the strategy behind it remains exactly the same.

The Insider Reality of Weekend Dialer Shifts

Why do collectors call on Sundays in the first place? To a consumer, it feels aggressive and unnecessary. To an agency operations manager, it is simple math.

During the standard Monday through Friday workday, most consumers are at their jobs. If an agency calls a cell phone at 2:00 p.m. on a Wednesday, the chance of the consumer answering is statistically very low. If they do answer, they are usually at work, distracted, and unable to process a payment.

Weekends change that dynamic entirely. Consumers are home. They are more likely to pick up a ringing phone. More importantly, they are often in a relaxed state of mind, which means the sudden stress of a collection call hits much harder and often leads to faster capitulation.

“During my time managing the floor, Saturday morning and Sunday afternoon shifts were considered prime dialing time. We specifically saved our hardest-to-reach accounts for the weekend campaigns. A consumer who ignored us for a month straight on weekdays would almost always pick up the phone on a Sunday while watching a football game. We banked on that element of surprise.”

Collectors are trained to capitalize on the fact that you were not expecting a business call. The goal is to get you talking before you have time to pull up your financial records or think about your legal strategy.

The Sunday Payment Trap

Because weekend calls catch people off guard, they create the perfect environment for one of the most dangerous traps in the debt collection industry.

When your Sunday morning is interrupted by an aggressive collector, your immediate reaction is usually a strong desire to make the conversation end quickly. Collectors know this. They will often lower their demands, saying something like, “Just make a $50 good faith payment today, and we will close the file and stop bothering you this weekend.”

This sounds like a concession, but it is often a trap. If the debt they are calling about is old, it might be past the statute of limitations. This means they can no longer legally sue you for it. But in most states, making even a $1 payment restarts that legal clock from zero. By paying $50 just to get them off the phone on a Sunday, you may have unknowingly handed them the legal right to sue you for the entire thousands of dollars you owe on Monday morning.

What to Do in the First 60 Seconds of a Sunday Call

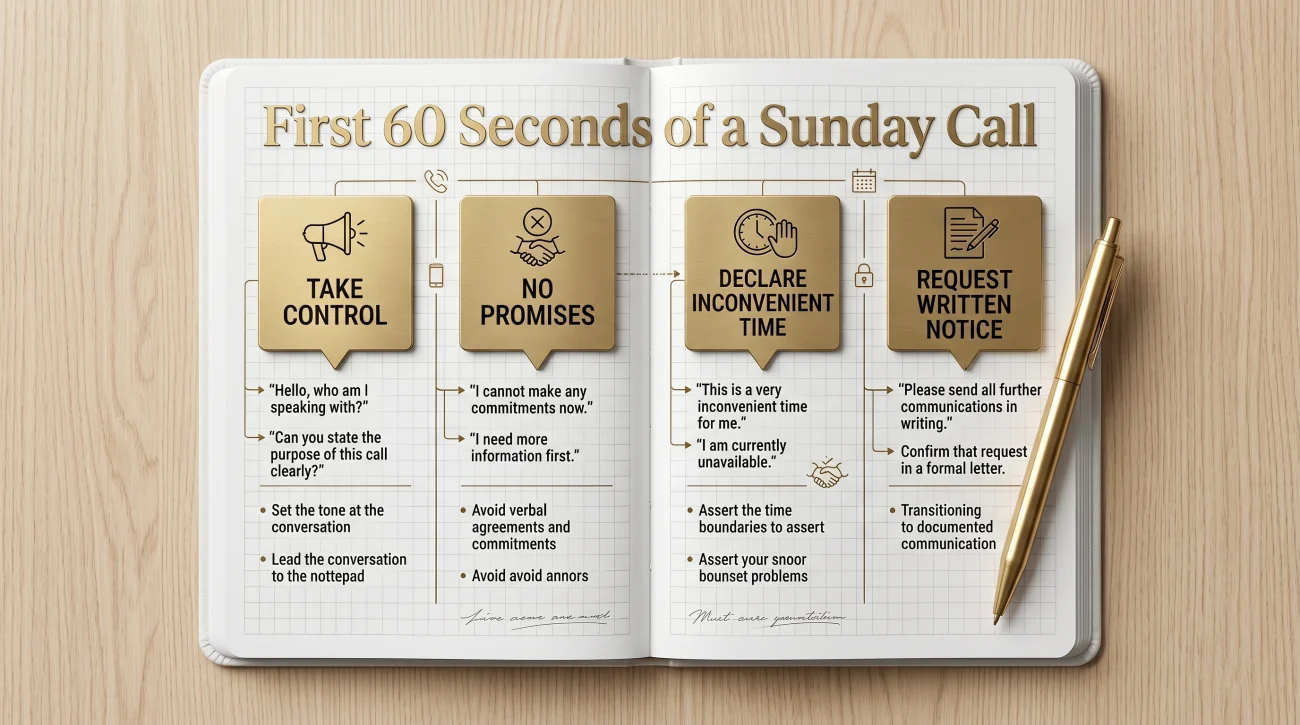

Handling a surprise call on your day off requires strict discipline. If you answer the phone and realize it is a collection agency, you must take control of the conversation immediately.

Do not try to explain your financial hardship, do not argue about the balance, and do not make any promises. Every word you say is being logged in their system.

“I am instructing you that Saturdays and Sundays are inconvenient times for me to receive phone calls. Do not call this number on weekends moving forward. Send any validation regarding this account to me in writing. Goodbye.”

By stating that weekends are an “inconvenient time,” you are invoking a specific right under the FDCPA. The collector must legally honor this restriction and stop weekend dialing. While a verbal request works for setting time restrictions, if you want to stop all contact entirely, you must do it in writing. You can review the full process for that in our guide on debt collector contact rules.

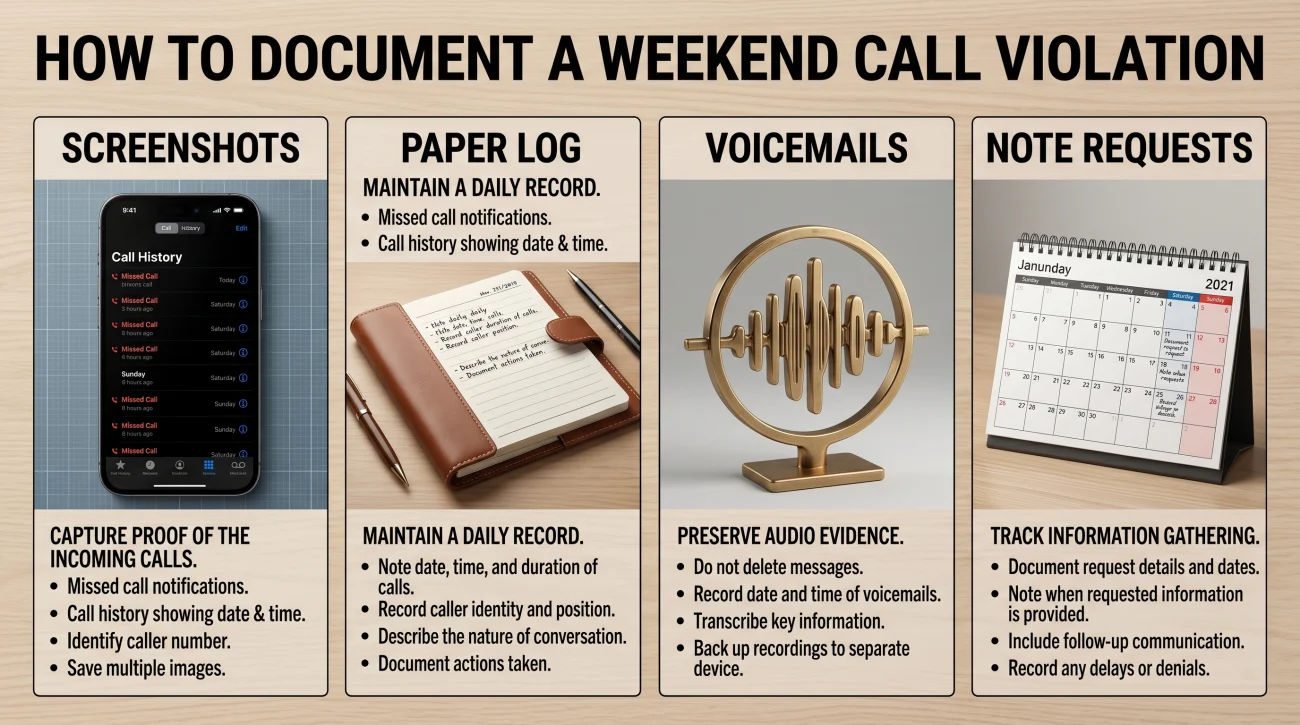

How to Actually Document a Weekend Violation

If you suspect an agency is weaponizing Sundays against you or calling outside legal hours, simply saying “they keep calling me on weekends” is not enough to build a case. You need concrete proof.

Start treating your phone like an evidence log:

- 📸 Take screenshots: The moment the call ends, take a screenshot of your phone’s call history showing the exact time, date, and caller ID.

- 📝 Start a paper log: Write down the date, the exact time in your local time zone, the name of the agency, and a brief summary of what was said.

- 📼 Save voicemails: Do not delete any messages they leave. Voicemails are prime evidence, especially if they fail to disclose they are a debt collector.

- 📌 Note your requests: Document the exact date and time you verbally told them weekends were inconvenient. If they call the following Sunday, you now have proof of an intentional violation.

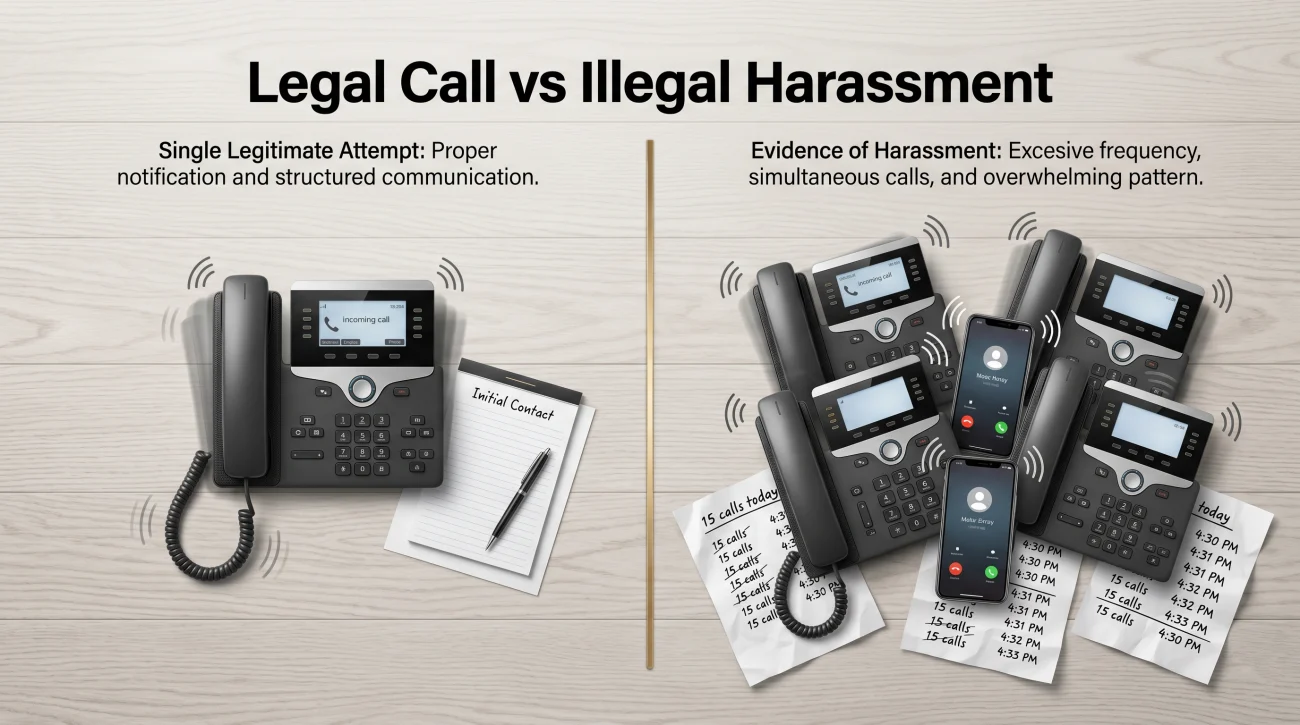

When Sunday Calling Becomes Illegal Harassment

While a standard Sunday call is legal, the Consumer Financial Protection Bureau addressed aggressive weekend calling directly in 2021. They explicitly noted that concentrating calls on days like Sundays or public holidays can be used as evidence of an intent to harass the consumer.

Pattern matters. If you are tracking your calls using the documentation steps above, you have a highly actionable case if you can prove any of the following:

Calling your number at 11:00 a.m. on a Sunday as part of a normal, randomized dialing rotation that spans the entire week.

Deliberately holding your account all week and exclusively blasting your phone on Sundays or holidays to maximize your distress.

Additionally, if they call you before 8:00 a.m. or call more than seven times in a rolling week, they have crossed a hard legal line. If your logs show these patterns and you need to evaluate whether you have a valid case for illegal harassment, a consumer protection attorney can use that exact documentation to hold them accountable.

Final Thoughts on Protecting Your Rest

A debt collector calling on a Sunday is using a calculated tactic. They are hoping you are relaxed, off guard, and willing to say whatever it takes to get them off the phone. Do not reward that strategy by making emotional decisions or panicking.

A Sunday call is just a call. It does not mean you are in more trouble than you were on Friday, and it does not mean a lawsuit is imminent. Log the time of the call, take control of the conversation immediately, and set your boundaries. You hold the power to dictate when a collector can speak to you, but you must be the one to enforce the rules.

❓ FAQ

📅 Can debt collectors call me on federal holidays?

Yes. The FDCPA treats federal holidays just like any other day. Unless you have specifically told them that holidays are an inconvenient time, they are legally permitted to call you.

⏰ What happens if a collector calls me at 7:00 a.m. on a Sunday?

This is a direct violation of federal law. Regardless of the day of the week, collectors cannot call before 8:00 a.m. in your local time zone. You should document the exact time and date of the call.

📱 Does a Sunday call count towards the 7-call weekly limit?

Absolutely. Every call attempt counts toward the limit of seven calls within a seven-day period, regardless of whether the attempt was made on a Tuesday or a Sunday.

💼 Can they call my workplace on a Sunday?

Yes, if your workplace is open and they do not have reason to know your employer prohibits such calls. However, if you have told them not to call your work, they must stop regardless of the day.

👨👩👧 Can a collector call my family members on a Sunday?

Yes, the rules for contacting third parties to obtain your location information apply equally on weekends. They are still restricted to calling that family member only one time.

✉️ Can they send text messages or emails on Sundays?

Yes, the 2021 Regulation F updates permit digital contact on weekends. However, every text and email must include a clear opt-out instruction. If a text arrives outside the standard 8:00 a.m. to 9:00 p.m. window, it may still constitute a timing violation.

⚖️ Is it harassment if they ONLY call me on Sundays?

It can be. The CFPB has noted that concentrating collection calls exclusively on days like Sundays or holidays can be viewed as an intentional pattern designed to harass or abuse the consumer.

📝 Should I pay a collector who calls on a Sunday?

You should never make a payment out of panic or simply to end a phone call. Making even a small payment can accidentally reset the statute of limitations on an old debt, reviving their ability to sue you.

🚫 Do I have to send a written letter to stop Sunday calls?

To declare weekends an “inconvenient time,” a verbal request is legally sufficient. However, to stop all communication across the board, you must send a formal cease and desist letter in writing.

The full FDCPA framework and the four areas where it matters most.

- Your legal rights when collectors call, write, or threaten to sue

- When they can call, what they cannot say, and how to make it stop

- How to identify FDCPA violations and what you can do with them

- Why the age of a debt determines what a collector can legally do

- Your right to demand proof before paying or acknowledging anything

Harassment is one thing. Lawsuits, garnishments, and frozen accounts are another.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.