- Your Answer is the legal document that formally addresses the collector’s claims and stops them from winning automatically. It does not need to be a complex legal brief.

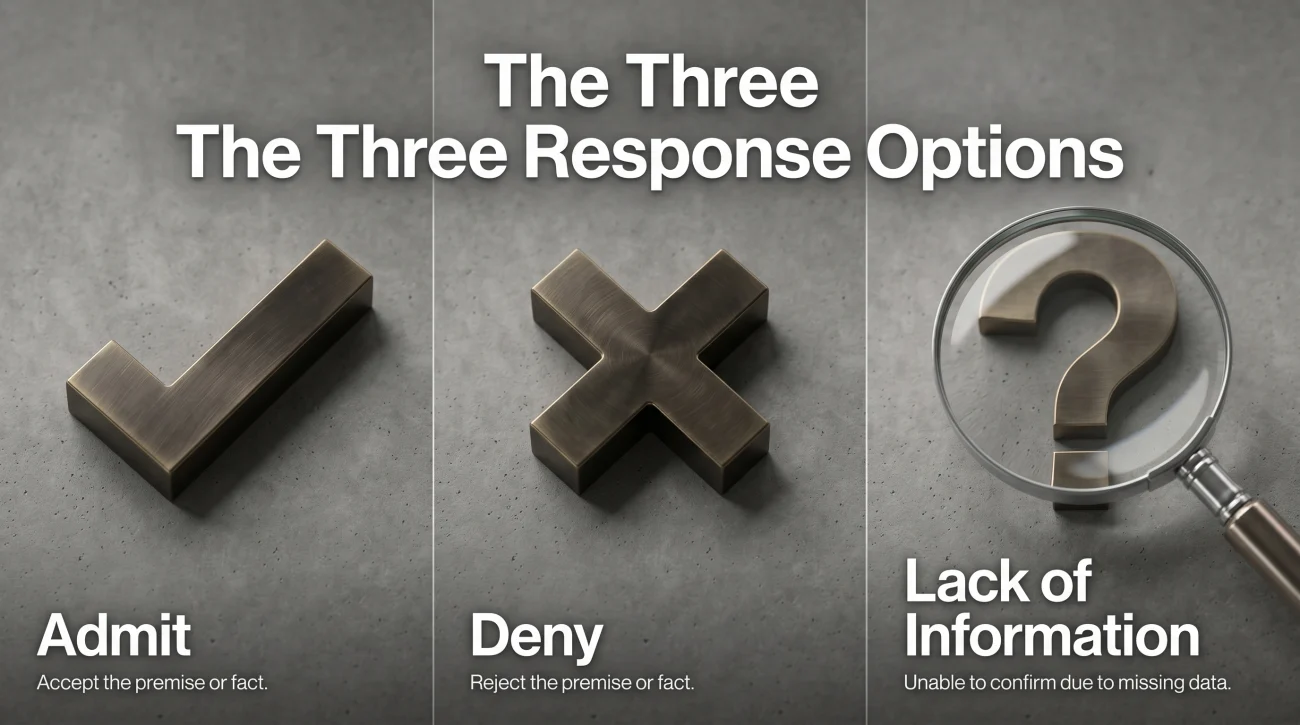

- For every numbered paragraph in the collector’s Complaint, you have three valid response options: Admit, Deny, or state that you lack sufficient information to admit or deny.

- Stating you “lack sufficient information” is a highly effective and fully legitimate response when a debt buyer sues you, as it forces them to prove their math and ownership.

- A “General Denial” is a shortcut statement denying all claims at once, but it comes with a massive trap: it does not automatically respond to Requests for Admissions.

- Never include emotional stories, payment offers, or confessions of debt in your Answer. Keep it factual, deny what you cannot verify, and file it before your deadline expires.

Overcoming the Blank Page Paralysis

You have been served with a court Summons, and you know you need to respond to avoid losing automatically. But staring at a blank document or a confusing legal form can be paralyzing. The collector’s attorneys are banking on that intimidation. They want you to believe that drafting a response requires a law degree so that you eventually give up.

It does not. During my 12 years in the debt collection industry, I personally reviewed thousands of consumer Answers during our collection litigation cycles. The most effective responses were rarely filled with complex legal citations. They were simple, direct, and mechanical. They simply moved down a checklist to deny our claims and forced us to prove our case.

Writing an Answer to a debt collection lawsuit is a straightforward task. You do not need to write a persuasive essay. Let’s break down exactly how to format this document, what specific language to use, and how to avoid the common mistakes that hand the collector an easy win.

The Five Basic Parts of Your Answer

While every state court has slight variations in formatting, a standard Answer document is universally composed of five basic sections. If your local court provides a fill-in-the-blank Answer form on their website, you will notice it follows this exact structure.

Your document must contain:

- The Caption: This is the header at the top of the page. It simply copies the information from the Complaint you received. It includes the name of the court, the Plaintiff (the company suing you), the Defendant (you), and the Case Number.

- The Responses: This is the core of the document. You will provide a specific, numbered response matching every numbered paragraph in the collector’s Complaint.

- Affirmative Defenses: A separate section where you list specific legal reasons why you should not have to pay the debt, such as the statute of limitations passing.

- Your Signature and Contact Info: You must sign and date the document, and provide your current mailing address so the court and the opposing attorney can reach you.

- The Certificate of Service: A short statement at the very end confirming that you mailed a copy of this Answer to the debt collector’s attorney. Many self-represented defendants skip this, but failing to formally notify the opposing attorney is a procedural error that can cause major issues with your filing.

The most intimidating part for consumers is the “Responses” section. People often freeze because they think they must prove their innocence in these paragraphs. That is a fundamental misunderstanding of how civil litigation works. The collector sued you. The burden of proof is entirely on them.

The Three Response Options (And Why the Third is Crucial)

When you look at the collector’s Complaint, you will see a list of numbered paragraphs. Some are simple facts (“Plaintiff is a business located in Texas”). Some are aggressive legal claims (“Defendant owes Plaintiff exactly $4,250.32 plus interest”).

In your Answer, you must respond to each numbered paragraph. For every single claim, you have exactly three valid options.

Option 1: Admit

You use this only when a statement is undeniably, 100% true, and you have independent verification of it. For example, if paragraph 1 says “Defendant is a resident of [Your County],” you would write: “Defendant admits the allegations in Paragraph 1.”

Option 2: Deny

You use this when a statement is factually false. If they claim you owe $10,000 but you know the credit limit on that card was only $1,000, you deny it. If they claim they are the lawful owner of your debt and you dispute their ownership, you deny it. You would write: “Defendant denies the allegations in Paragraph 2.”

Option 3: Lack of Sufficient Information (The Golden Ticket)

This is the most underused and misunderstood option available to consumers. The formal phrasing is: “Defendant lacks sufficient information or knowledge to admit or deny the allegations in Paragraph 3, and therefore denies them.”

Consumers often ask me if they are committing perjury by denying a debt they secretly know they probably owe. This fear paralyzes people. But you have to look at exactly what the debt buyer is claiming. They are not just claiming you had a credit card once. They are claiming they legally purchased the account, that they calculated the post-charge-off interest perfectly to the penny, and that they have the contractual right to sue you.

“When I managed accounts at a major debt buyer, I knew our documentation was often incomplete. If a consumer stated they ‘lacked sufficient information to verify’ our exact $5,432.18 balance claim, they were being completely truthful. They hadn’t seen our spreadsheets or our interest calculations. By using that response, they legally forced us to produce the math. Very often, we couldn’t.”

Unless the debt buyer attached a pristine, unbroken chain of ownership documents and a line-by-line accounting of every fee leading to their exact total, you genuinely do lack the information required to agree with their claims under oath. This response is fully legitimate, highly protective, and shifts the heavy lifting back to the collector.

The General Denial (And Its Major Blind Spot)

Depending on the specific rules of your state and local court, you may not have to write out a response to every single paragraph. Many jurisdictions allow what is called a General Denial.

A General Denial is a blanket statement that rejects all the plaintiff’s claims at once. It is a massive time-saver and is legally sufficient in many consumer debt cases. If you want to understand the full mechanics of a general denial, you will find it is the most common path self-represented defendants take.

Standard General Denial Language:

“Defendant generally denies each and every allegation contained in Plaintiff’s Complaint and demands strict proof thereof. Defendant reserves the right to assert additional affirmative defenses as information becomes available through discovery.”

This language efficiently tells the court: “I dispute this entire lawsuit, and I require the collector to prove everything they claim.” It accomplishes your primary goal of keeping the lawsuit actively contested.

The Critical Trap: Requests for Admissions

While a general denial is powerful, there is a dangerous trap hidden in how debt collection law firms package their lawsuits. I must warn you about this because it ruins countless winnable cases.

Sometimes, the collector will staple a secondary document to the back of the Complaint. This document is usually titled “Requests for Admissions.” It contains a list of statements, such as “Admit that you owe Plaintiff $4,200” or “Admit that you opened this account.”

A General Denial does NOT respond to Requests for Admissions.

If you file a general denial to the Complaint but completely ignore the attached Requests for Admissions, the court rules will automatically deem every ignored statement as “Admitted.” You will lose the case by default, even though you filed an Answer, because you technically admitted to owing the money by failing to respond to that specific discovery document.

If you see a document titled “Requests for Admissions” in your packet, you must respond to each of those statements individually (using the Deny or Lack of Information options) on a separate sheet of paper. You must understand how to handle debt collection discovery requests to ensure you do not fall into this auto-admission trap.

Adding Affirmative Defenses to Your Answer

Beyond how you respond to each claim, there is a second layer to your Answer that many people overlook entirely. After your paragraph responses (or your general denial), your Answer should include a section titled “Affirmative Defenses.”

An affirmative defense is essentially saying: “Even if everything the collector says is true, they still cannot win this lawsuit because of [Legal Reason].”

You do not need to write a long explanation or attach heavy evidence to your Answer at this stage. The goal right now is simply to list the defenses so you preserve your right to argue them later in front of the judge. If you fail to name a defense in your Answer, most courts will bar you from bringing it up at trial.

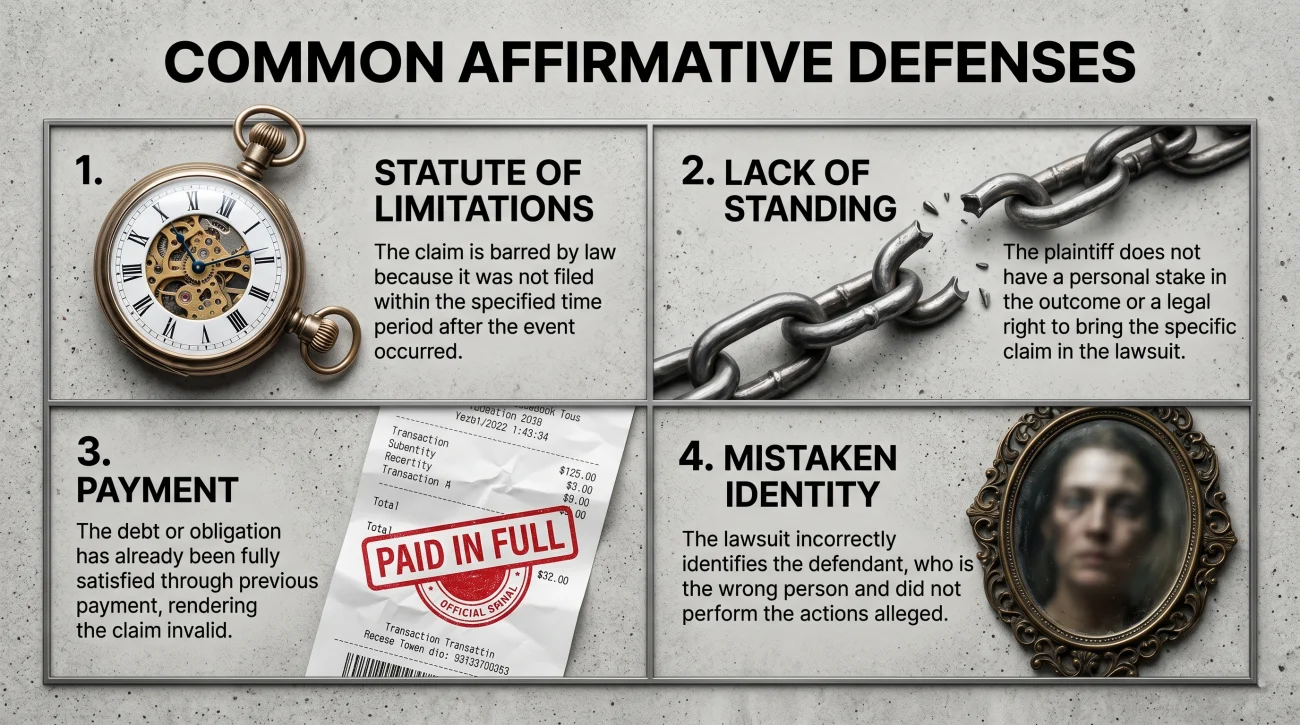

Common affirmative defenses to simply list include:

- Statute of Limitations: “Plaintiff’s claims are time-barred because the applicable statute of limitations has expired.” (Applies if your last payment was more than 3 to 6 years ago, depending on your state).

- Lack of Standing (Chain of Title): “Plaintiff lacks standing to sue because it has not demonstrated a complete and unbroken chain of assignment from the original creditor.” (Applies if you are being sued by a debt buyer you do not recognize, rather than your original bank).

- Payment or Accord and Satisfaction: “The alleged debt has already been paid or settled in full.” (Applies if you already paid this debt to a previous collector or settled it).

- Mistaken Identity: “Defendant is not the person who incurred the alleged debt.” (Applies if you are an authorized user, or if this account simply does not belong to you).

If you are unsure which apply to your specific situation, you should review the most effective affirmative defenses against debt buyers to see which ones match your case history. Listing the right defenses now gives you the leverage you need for the rest of the lawsuit.

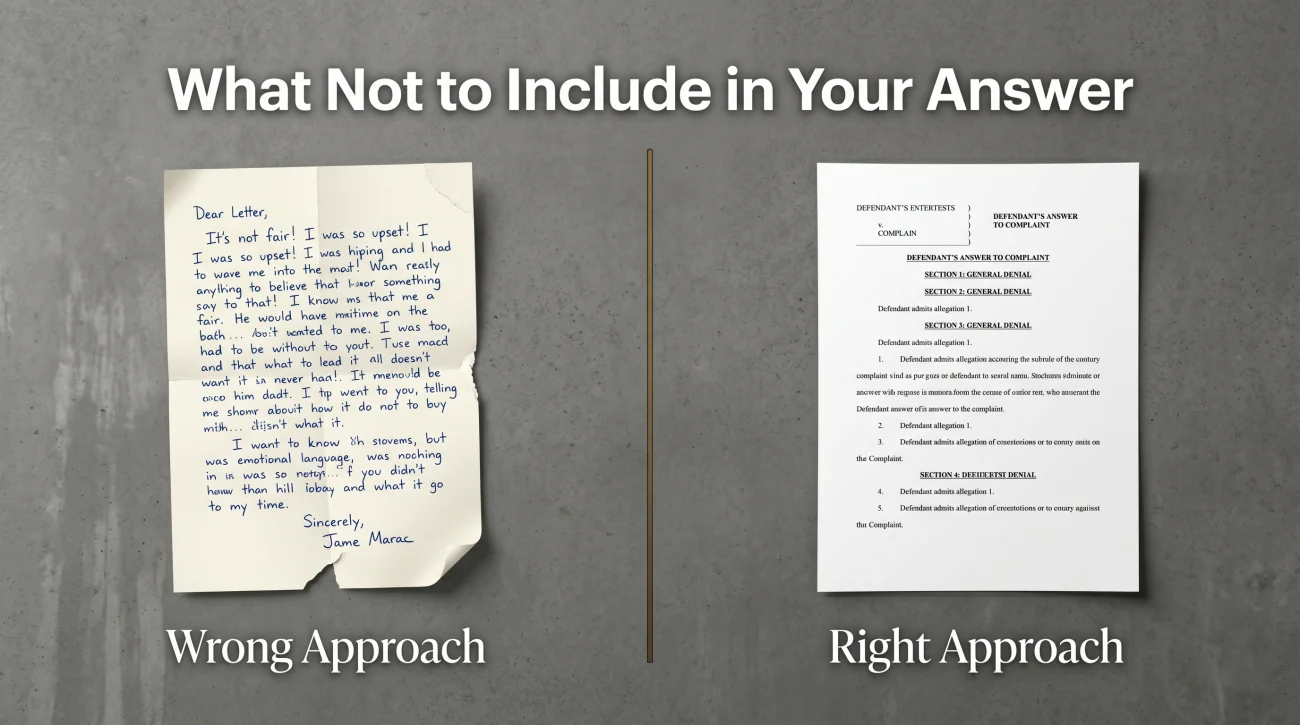

What NOT to Include: The Most Common Consumer Mistakes

Knowing what to leave out of your Answer is just as important as knowing what to include. Remember that the Answer is a public court document, and a copy goes directly to the attorney suing you. They will read it looking for any admission they can use against you.

When you write an emotional letter explaining why you could not pay, you are accidentally doing the debt buyer a massive favor. You are legally admitting that the debt is yours and that the balance is valid. You have just done their job for them. A judge cannot dismiss a lawsuit out of sympathy for your job loss. If you admit the debt is yours in your Answer, the judge must award the victory to the collector.

Furthermore, never include a settlement offer or a payment plan proposal inside your formal Answer document. Settlement negotiations should always be conducted separately, directly with the plaintiff’s attorney, after your protective Answer is already filed with the court.

Signs You Must File Now, Even If It Is Imperfect

Once you have avoided those fatal mistakes, your only remaining hurdle is time. Perfectionism is the enemy of survival in a debt lawsuit. You may be reading this feeling like you need another week to research your state’s specific case law or to find the perfect template. You likely do not have that kind of time.

You need to finalize a basic Answer and file it immediately if you recognize any of these warning signs:

- Your response deadline (as stated on the Summons) is fewer than 5 days away.

- You are still waiting to hear back from legal aid or an attorney, but the clock is running out.

- You want to negotiate a settlement, but the collector’s attorney is not returning your calls. (Filing an Answer forces them to take you seriously).

- You are unsure of all your defenses. (File a general denial now to keep the case open, and you can often amend your Answer or explore defenses during discovery).

If your situation is highly complex, involves a massive balance, or you have identified serious FDCPA violations by the collector, taking a moment to consult a qualified debt defense attorney is the safest route, as they can draft a highly strategic Answer on your behalf.

The Final Step: The Mechanics of Filing

Writing the Answer is only half the battle. A beautifully drafted document does absolutely nothing to protect you if it sits on your desk.

Once you have printed and signed your Answer, you must physically file it with the court clerk and mail a copy to the opposing attorney. Forgetting this mailing step is a technicality that can get your otherwise perfect response thrown out.

To ensure your document is legally recognized by the court and officially pauses the collector’s path to an automatic win, follow the precise steps for how to file your Answer and serve the collector before you consider the job done.

Final Thoughts: Keeping the Burden Where It Belongs

When you understand the true purpose of an Answer, the intimidation factor of a debt lawsuit drops significantly. Your job is not to prove you are innocent of a financial struggle. Your job is to make the plaintiff prove every single element of their legal claim using valid, admissible evidence.

Keep your response clean, factual, and devoid of emotion. Use the power of the denial, list your defenses, and get the document stamped by the court clerk. By filing a proper Answer, you transform yourself from an easy target into an active litigant, and that alone changes the entire dynamic of the case.

❓ FAQ

📝 Does my Answer have to be typed, or can I handwrite it?

Most courts strongly prefer typed documents for legibility, but many will accept neatly handwritten Answers if typed access is impossible. Always check if your specific county court offers a printed fill-in-the-blank form you can use.

⚖️ What if I actually owe the money? Should I still file an Answer?

Yes. Even if you recognize the account, you should file an Answer. The collector still has to prove they own the debt and calculated the amount correctly. Filing prevents an automatic loss and gives you time to negotiate a better settlement.

✉️ Can I just write a letter to the judge explaining my situation?

No. A letter explaining your financial hardship is not a legal defense and often acts as a confession. You must format your response as a formal Answer addressing the specific allegations in the Complaint.

💵 Does it cost money to file an Answer with the court?

It depends on the court. Some courts charge a filing fee (typically $20 to $100). However, if you cannot afford this, you can ask the clerk for a “fee waiver” application based on low income or financial hardship.

🕒 What happens if I make a mistake in my Answer?

Filing an imperfect Answer is always better than missing the deadline. In many jurisdictions, courts allow self-represented defendants to file an “Amended Answer” later if they discover new defenses during the discovery process.

🤥 Am I committing perjury if I deny a claim I am unsure about?

No. If you genuinely do not have the documentation to verify their exact balance calculation or their chain of ownership, stating that you lack sufficient information to admit or deny is the correct and truthful legal response.

📋 Do I need to attach evidence or documents to my Answer?

Generally, no. The Answer is just your formal response to their claims. You will have a chance to exchange evidence (like bank statements or letters) later during the discovery phase of the lawsuit.

🤝 Should I include my settlement offer in the Answer document?

No. Keep your settlement negotiations completely separate from your court filings. Contact the plaintiff’s attorney directly by phone or email to discuss settlement terms after your Answer is safely filed.

📬 Can I just mail the Answer to the debt collector directly?

No. The original document must be officially filed with the court clerk. You must then mail a copy of that filed Answer to the debt collector’s attorney to satisfy the legal requirement of service.

🛑 Does filing an Answer mean I have to go to a full trial?

Not necessarily. The vast majority of debt collection lawsuits settle long before a trial happens. Filing your Answer simply keeps your options open and forces the collector to the negotiating table.

What each stage of litigation requires and where your leverage sits.

- What the lawsuit process looks like from summons to judgment

- What to file, when to file it, and what happens if you do not

- The legal arguments that can defeat a debt collection lawsuit

- What a default judgment allows collectors to do and how to fight one

- How to negotiate a resolution once litigation has started

Once judgment is entered, collectors gain tools they did not have before.

- The FDCPA violations collectors commonly commit during the collection process

- How to respond to a debt lawsuit and what defenses are available to you

- How a judgment becomes a garnishment order on your paycheck

- When a collector uses a judgment to freeze your bank account instead

- How to settle before the judgment turns into something harder to stop

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.