- Since a major federal rule update in 2021, debt collectors are legally allowed to contact you through private direct messages on social media platforms like Facebook and Instagram.

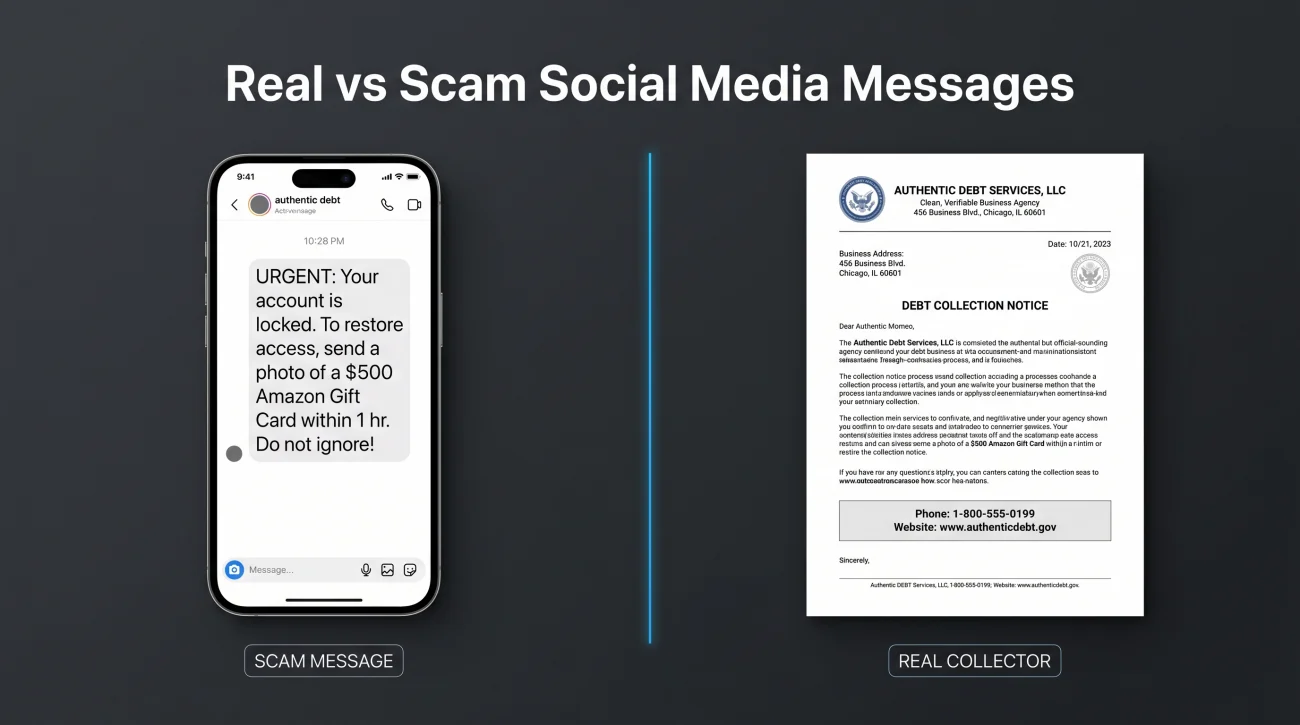

- Legitimate collectors must clearly identify themselves upfront. If an account asks for payment via gift cards or peer-to-peer apps, or threatens you with arrest via a direct message, it is almost certainly a scam.

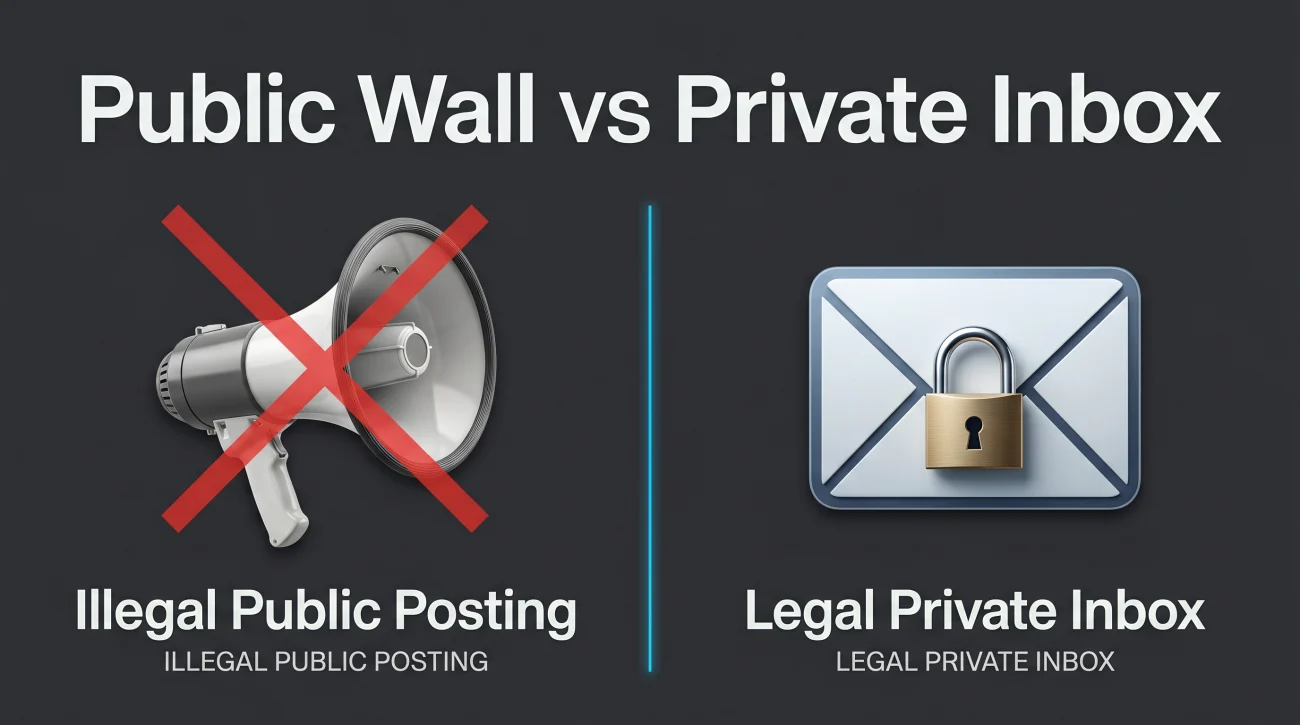

- Collectors are strictly prohibited from posting about your debt publicly on your timeline or in comment sections where other people can see it.

The Shock of a Social Media Message About Your Debt

You open Facebook or Instagram, check your message requests, and see a note from an unfamiliar account claiming you owe them money. For most people, the immediate reaction is panic, closely followed by suspicion. You probably assume your account has been hacked or that you are being targeted by a sophisticated scam. It feels incredibly invasive.

When I spent my twelve years working inside third-party collection agencies, we practically lived on the phones. We sent letters and we made calls. But as consumer habits changed and spam-blocking technology improved, reaching people over the phone became increasingly difficult.

In late 2021, the rules changed. Federal regulators explicitly opened the door for digital debt collection. It is now legal for a debt collector to slide into your direct messages.

However, the government did not give collectors a free pass to harass you online. There are incredibly strict boundaries regarding what a collector can do on social media, what they must say before they even try to connect with you, and how you can shut them down. My goal here is to help you figure out if the message you received is from a legitimate agency operating within the rules, or if you are dealing with a fraudster trying to steal your money.

Is This a Real Debt Collector or a Scam?

This is the most important question to answer before you reply, click any links, or provide any personal information. Because social media is so easily manipulated, it is a prime hunting ground for scammers posing as debt collectors.

Legitimate debt collection agencies are highly regulated businesses. They are terrified of compliance lawsuits. A real agency will follow a very specific, rigid script even in a direct message. Scammers, on the other hand, rely on fear and urgency to force you into making a mistake.

The account name is generic or hidden. The message demands immediate payment via CashApp, Zelle, cryptocurrency, or gift cards. They threaten to send the police to your house if you do not reply immediately. They send a link and tell you to “click here to stop the lawsuit.”

The message clearly identifies the name of the collection agency. It explicitly states that the communication is from a debt collector. It provides a verifiable physical address and a standard customer service phone number. It includes clear instructions on how to opt out of future digital messages.

If you receive a message that leans toward the scam side, do not engage. Do not argue with them, and absolutely do not click any links provided in the chat. Take a screenshot for your records, report the account to the platform, and block the user.

What the 2021 Regulation F Update Actually Did

The collection industry lobbied heavily for the right to reach consumers where they actually spend their time online. To understand how that happened, you have to look at the Consumer Financial Protection Bureau (CFPB). In November 2021, the CFPB rolled out an update known as Regulation F. This was the first major overhaul of the Fair Debt Collection Practices Act since the 1970s.

Before this update, the law was written for a world of landlines and physical mail. The internet created a massive grey area. Regulation F clarified that grey area by giving debt collectors explicit permission to use newer technologies to contact consumers. This update is the reason you might now receive a direct message on Twitter or Facebook.

Direct messaging is just one piece of the digital access granted during that rollout. Collectors were also given formal permission to reach out via other digital channels. If you are dealing with a broad pressure campaign, you should review the specific regulations around whether debt collectors are allowed to text your personal number and when they are permitted to send notices to your email inbox.

But getting access to your inbox did not mean the government erased the old rules. In fact, the oldest boundary in debt collection translated directly into the digital world.

The Public Wall vs. Private Inbox Rule

One of the most foundational rules in debt collection is that a collector cannot disclose your debt to a third party. They cannot tell your neighbors, your friends, or your coworkers that you owe money. When it comes to social media, this rule translates into a strict division between public and private spaces.

A debt collector is legally permitted to send you a private direct message. Only you have access to your inbox, so the privacy of the communication is theoretically maintained.

What they are absolutely prohibited from doing is posting anything public about your debt. They cannot leave a comment on your recent Instagram photo asking you to call their office. They cannot post on your Facebook wall. They cannot tag you in a public post on X (formerly Twitter). Doing anything that exposes your financial situation to your followers or friends is a severe violation of federal law.

The Friend Request Rule and Fake Profiles

Because many social media platforms filter messages from unknown accounts into a hidden “requests” folder, collectors often struggle to get their messages seen. To bypass this, a collector might try to send you a friend request or a connection invite first.

The law anticipated this tactic. If a debt collector attempts to connect with you or send a friend request, the request itself must clearly disclose that they are a debt collector. They cannot hide their identity until after you accept.

Furthermore, collectors cannot engage in “catfishing.” A debt collector cannot create a fake profile of an attractive person, an old high school acquaintance, or a generic business account just to trick you into accepting their request. I have seen rogue agents try to use multiple burner accounts to flood a consumer with requests, which is a massive compliance violation.

Misrepresenting their identity to gain access to your profile is not just deceptive. It is a violation that they cannot legally deny, simply because you have the digital proof sitting right in your screenshot folder.

Digital Skip Tracing: Can They Look at Your Public Profile?

Even if a collector never sends you a single message, they are almost certainly looking at your social media. In the collection industry, the process of locating a consumer and assessing their ability to pay is called “skip tracing.”

Many people think setting their Instagram or Facebook to “Private” makes them invisible. This is a common misconception. While it restricts your photos from public view, in most cases, a direct message request from a collector can still land in your hidden message folders.

But for everything you leave public, collectors treat it as fair game. Debt collectors routinely scour LinkedIn to find out where you work so they can prepare for potential wage garnishments. They monitor Facebook and Instagram to find your current city if your mail is bouncing back.

“In the later years of my career, skip tracers used social media constantly. We had dedicated software to scrub public profiles. If a consumer told us on the phone that they were completely broke and facing eviction, but they had just posted public photos of a brand new jet ski or a luxury vacation on Instagram, that account was immediately flagged for litigation review. We did not need to message you to use your social media against you.”

The reality is that your digital footprint often dictates how aggressively an agency will pursue you. There is no law against a collector looking at public information. This falls under the broader umbrella of rules dictating how and when a collector can make contact. If you have accounts in collections, the most practical immediate step you can take is to lock down your privacy settings across all platforms. Limit your audience to friends only and remove your current employer from your public bio.

The law gives collectors the right to look at your public life and the right to drop a message in your inbox. But it also gives you an absolute right to shut that digital door.

How to Stop Social Media Contact

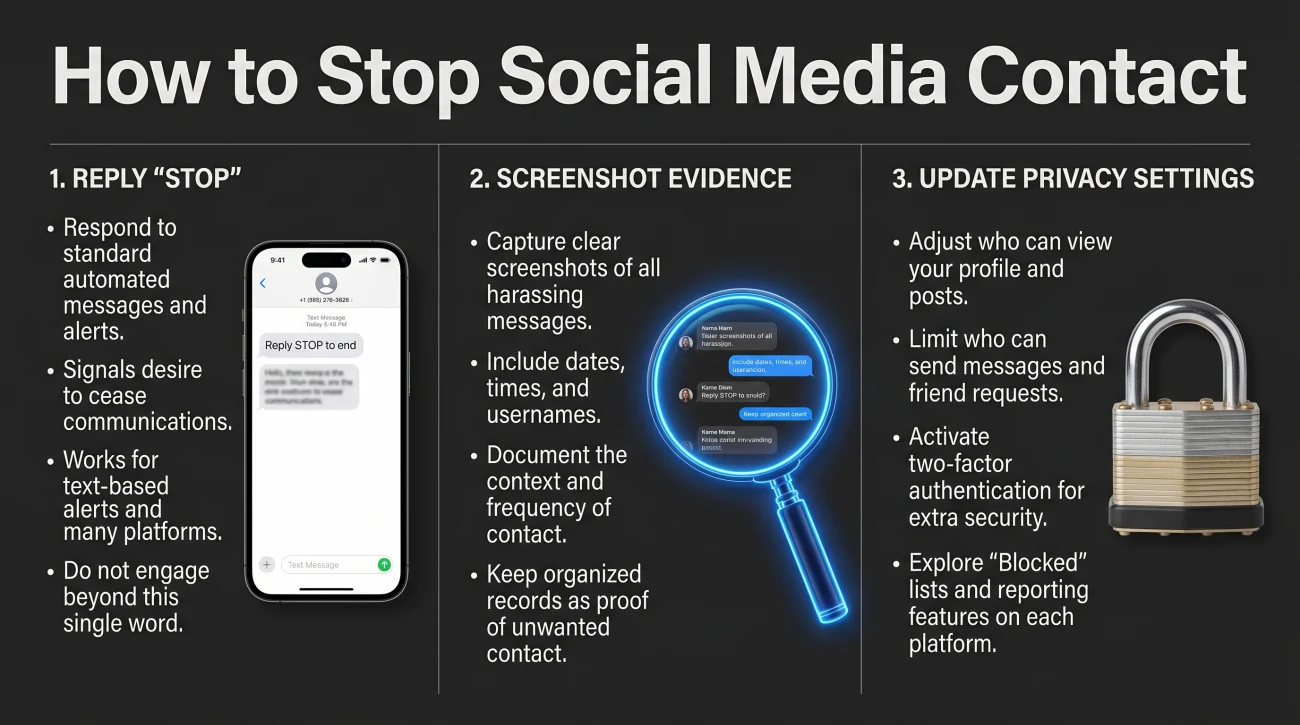

You do not have to tolerate collection attempts in your personal digital spaces. The law requires collectors to provide a simple, effective way for you to opt out of communications on that specific platform.

Platforms handle these messages differently. A LinkedIn InMail goes to your professional inbox, while Facebook filters unknown senders into a message requests folder. Regardless of the platform, the opt-out rule is exactly the same.

Legitimate messages will often include instructions like “Reply STOP to opt out of further messages on this platform.” If they do, simply reply with that exact word. Do not add commentary or argue about the debt. If they do not provide a specific prompt, you can still shut the communication down yourself by replying directly.

Sample Opt-Out Reply:

“I do not consent to receiving communications via social media. Cease all contact with me on this platform immediately.”

Once you send this, what happens next? Legitimate agencies use compliance software that immediately flags your account as “Do Not Contact” for that specific social channel. They do not have to send you a confirmation message, but the messages must stop immediately. Inside a reputable agency, if an agent messages someone who has explicitly opted out, that agent is usually written up or fired because the liability is so high. If a collector messages you again after you have opted out, that is a direct FDCPA violation, and you do not have to warn them twice.

While an opt-out message secures your digital inbox, keep in mind that opting out of Facebook messages does not automatically stop them from calling your phone or sending letters to your house. If your goal is to shut down all communication across every channel simultaneously, you will need to take a more formal approach. You can learn exactly how to force a collector to stop all contact by sending a written cease and desist letter.

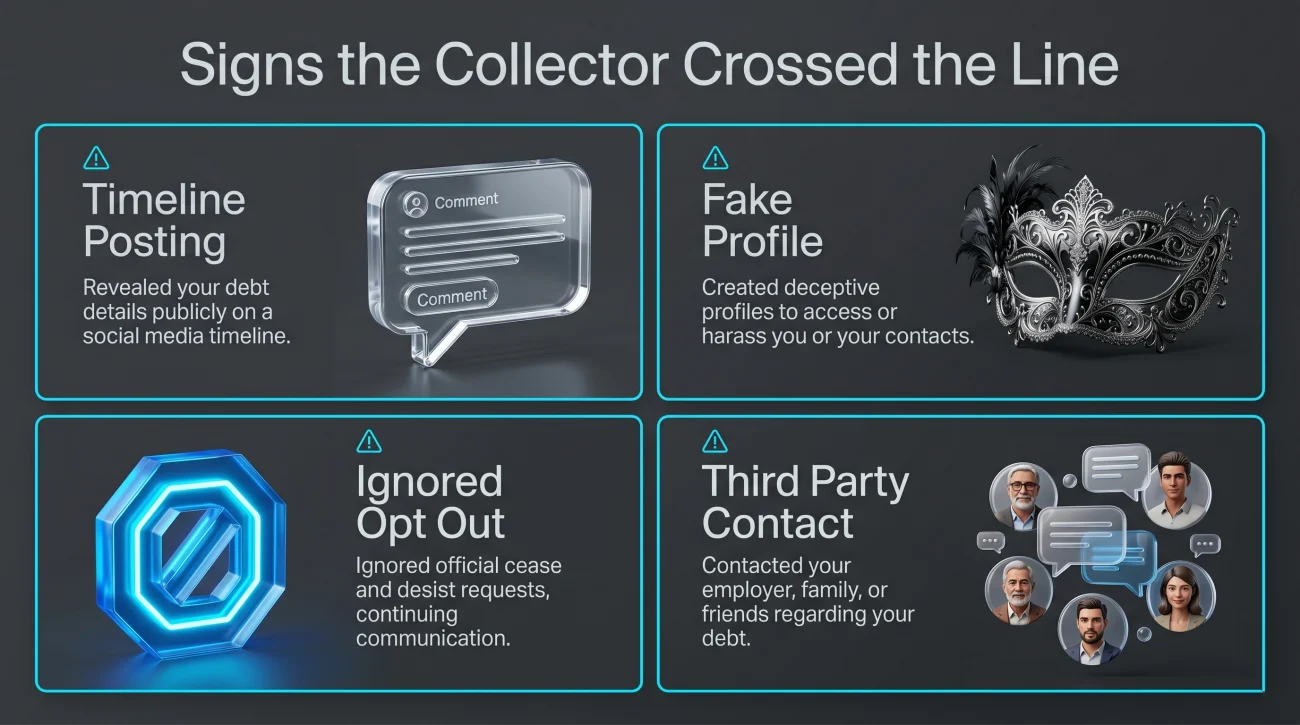

Signs a Legitimate Collector Crossed the Legal Line

Because digital collection is relatively new, many rogue agencies and individual collectors push the boundaries, hoping consumers do not know their rights. You need to recognize when a legitimate agency crosses from a nuisance into a documentable federal violation.

Assuming you are dealing with a real collection agency and not a scammer, they are actively breaking the law if:

- They made a public post on your timeline or replied to a public comment mentioning your debt.

- They sent a friend request without clearly disclosing that they are a debt collector trying to reach you.

- They continued to message you on the platform after you clearly replied with an opt-out request.

- They used multiple different accounts to bypass your blocks and continue messaging you.

- They contacted your friends, family members, or coworkers on social media to discuss your debt.

If this matches your experience, it is time to have a professional evaluate whether you have grounds to pursue a harassment claim. Collectors who break the rules on social media leave a digital paper trail that is incredibly easy to use against them in court.

Final Thoughts: Controlling Your Digital Boundaries

Getting a direct message from a debt collector feels like an invasion of your personal sanctuary. It is designed to catch you off guard and create a sense that there is nowhere to hide online.

Do not let the medium dictate your reaction. Take a breath, take a screenshot of the message, and handle it logically. In the collections industry, the consumers who panic are the ones who pay out of fear. The consumers who know the rules are the ones who hold the power. By maintaining your privacy settings and knowing how to properly shut down digital contact, you force the collector to play the game on your terms.

❓ FAQ

💬 Is it legal for a debt collector to message me on Facebook?

Yes. Under the CFPB Regulation F update in 2021, debt collectors are legally permitted to send you private direct messages on platforms like Facebook, provided they follow strict disclosure and privacy rules.

🛑 How do I stop a debt collector from messaging my social media?

You can reply directly to the message and explicitly state that you do not consent to being contacted on that platform. Legitimate collectors are legally required to honor that opt-out request immediately.

📢 Can a collection agency post on my public timeline?

Absolutely not. Debt collectors are strictly prohibited from making public posts, tagging you, or leaving comments about your debt where third parties, like your friends or family, can see them.

🕵️♂️ Are debt collectors allowed to look at my Instagram?

Yes. Any information you post publicly on the internet can be viewed by anyone, including debt collectors. They frequently use public social media profiles to verify your location or employment status.

🤝 Can a debt collector send me a friend request?

They can, but the law requires them to clearly disclose that they are a debt collector within the friend request itself. They cannot use a fake persona to trick you into accepting.

💸 A debt collector DM asked for CashApp, is that real?

This is almost certainly a scam. Legitimate collection agencies have secure payment portals and physical addresses. They do not demand immediate payment via peer-to-peer cash apps or gift cards through direct messages.

📱 Does blocking the account stop the collection?

Blocking the specific account stops that profile from messaging you, but it does not formally opt you out of digital communications, nor does it erase the underlying debt. Sending a formal opt-out reply is legally stronger.

📩 Do the same rules apply to LinkedIn?

Yes. LinkedIn is treated as a social media platform. A collector can send you a private InMail, but they cannot post publicly about your debt on your professional feed or contact your coworkers.

🤔 What if a collector messages my spouse on Facebook?

Under the FDCPA, a collector is generally allowed to communicate with your legal spouse about your debt. However, the same rules apply: the communication must be via private message, never public.

⚖️ Can I sue a debt collector for a Facebook message?

You cannot sue simply because they sent a private message. However, if they posted publicly, used a fake profile to trick you, or ignored your clear opt-out request, you may have grounds for an FDCPA lawsuit.

The full FDCPA framework and the four areas where it matters most.

- Your legal rights when collectors call, write, or threaten to sue

- When they can call, what they cannot say, and how to make it stop

- How to identify FDCPA violations and what you can do with them

- Why the age of a debt determines what a collector can legally do

- Your right to demand proof before paying or acknowledging anything

Harassment is one thing. Lawsuits, garnishments, and frozen accounts are another.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.