- Debt collection lawsuits are not distributed randomly. Court data proves that a massive percentage of civil dockets are dominated by a handful of corporate debt buyers, not original creditors.

- Having multiple accounts in collections dramatically increases your risk. Consumers with five or more delinquent debts face a 35 percent lawsuit rate, compared to just 6 percent for those with a single debt.

- Geography matters. Debt buyers systematically target specific states where court filing fees are low and procedural hurdles are minimal, leading to massive surges in localized litigation.

- Before paying a filing fee, collectors run automated skip-tracing checks looking for W-2 employment or property ownership to ensure a judgment will actually be collectible.

- Timing is rarely random. Automated systems flag accounts 60 to 90 days before the statute of limitations expires, triggering massive batches of lawsuits on aging debt.

- Academic research reveals a severe racial disparity: Black and Hispanic borrowers are 52 percent more likely to experience a debt collection judgment than white and Asian borrowers, even when controlling for income and credit scores.

The Hidden Patterns of Debt Litigation

A court summons feels like a deeply personal legal judgment. But from inside a debt collection agency, the decision to sue rarely involves a lawyer sitting at a desk reviewing your financial history. It is simply an arithmetic problem.

During my years working for collection agencies and a national debt buyer, we knew internally that we filed lawsuits more frequently in certain states and against certain demographic profiles. We talked about processing volume, expected yield, and portfolio segmentation. The modern debt collection lawsuit is an industrial product, manufactured at scale, and aimed at specific targets based on statistical modeling.

If you have ever wondered who actually gets sued by debt collectors, you do not have to guess. The court data, federal surveys, and academic research have documented the patterns clearly. Here is what the data shows about how the industry chooses its targets, and what it means for you.

Why the Summons Feels Like a Personal Attack

Receiving a lawsuit summons for a debt is a jarring, isolating experience. For most people, it feels like they have been singled out for punishment. You might be struggling to keep up with four different credit cards, but only one company decides to take you to court. You might owe $2,000, while you know someone else who owes $15,000 and has never heard a word from a lawyer.

This inconsistency creates a tremendous amount of anxiety. Because it feels personal, consumers often try to solve it personally. They call the law firm begging for a break, or they assume the judge will look at their hardship and dismiss the case. But looking at a debt collection lawsuit as a personal dispute is the fastest way to lose.

Understanding that you are caught in a statistical net, rather than a personal vendetta, is the first step toward fighting back. To disrupt their outcome, you first have to understand exactly what the scoring model is looking for.

The Concentration of Filers: Who Is Doing the Suing?

The first myth the data breaks is the idea that your original creditor is the one taking you to court. While banks and hospitals do file lawsuits, the overwhelming majority of the civil court docket in the United States is dominated by a tiny fraction of companies you have likely never done business with.

According to an analysis of court data by the Pew Charitable Trusts, the concentration of plaintiffs is staggering. In Connecticut, for example, just 10 plaintiffs account for 80 percent of the entire debt collection docket. This is not an anomaly; it reflects a nationwide pattern where a handful of specialized debt buyers and their network of law firms monopolize the court system.

These entities purchase portfolios of defaulted accounts in bulk, often paying just pennies on the dollar. When a consumer receives a summons from one of these 10 mega-plaintiffs, their first reaction is often, “I do not recognize this company.” This confusion is a direct result of the industry’s structure. The companies filing the bulk of the lawsuits are not lenders; they are litigation factories.

The Geographic Surge: Why Your Zip Code Matters

The decision to sue is heavily influenced by state borders. Inside the industry, we frequently used the term “favorable jurisdictions.” We used it casually in meetings, but looking back, it was a sanitized way of describing a court system that was structurally working against consumers.

A favorable jurisdiction for a debt buyer is a state where court filing fees are exceptionally low, the maximum balance allowed in streamlined small-claims courts is high, and judges routinely grant automatic wins when consumers fail to appear. According to the Pew Charitable Trusts, in many of these jurisdictions, default judgment rates exceed 70 percent. That means in more than seven out of ten cases, the collector wins the full amount without ever having to present a shred of evidence. When a debt buyer identifies this kind of favorable jurisdiction, they flood it.

The data clearly illustrates this geographic targeting. Rather than steady, nationwide growth, lawsuits tend to spike dramatically in specific regions once debt buyers optimize their models for local court procedures. This geographic concentration proves that filing volume is driven more by the cost-efficiency of local courts than by random consumer default rates. If you live in a targeted state, your risk of being sued for a relatively small balance goes up exponentially.

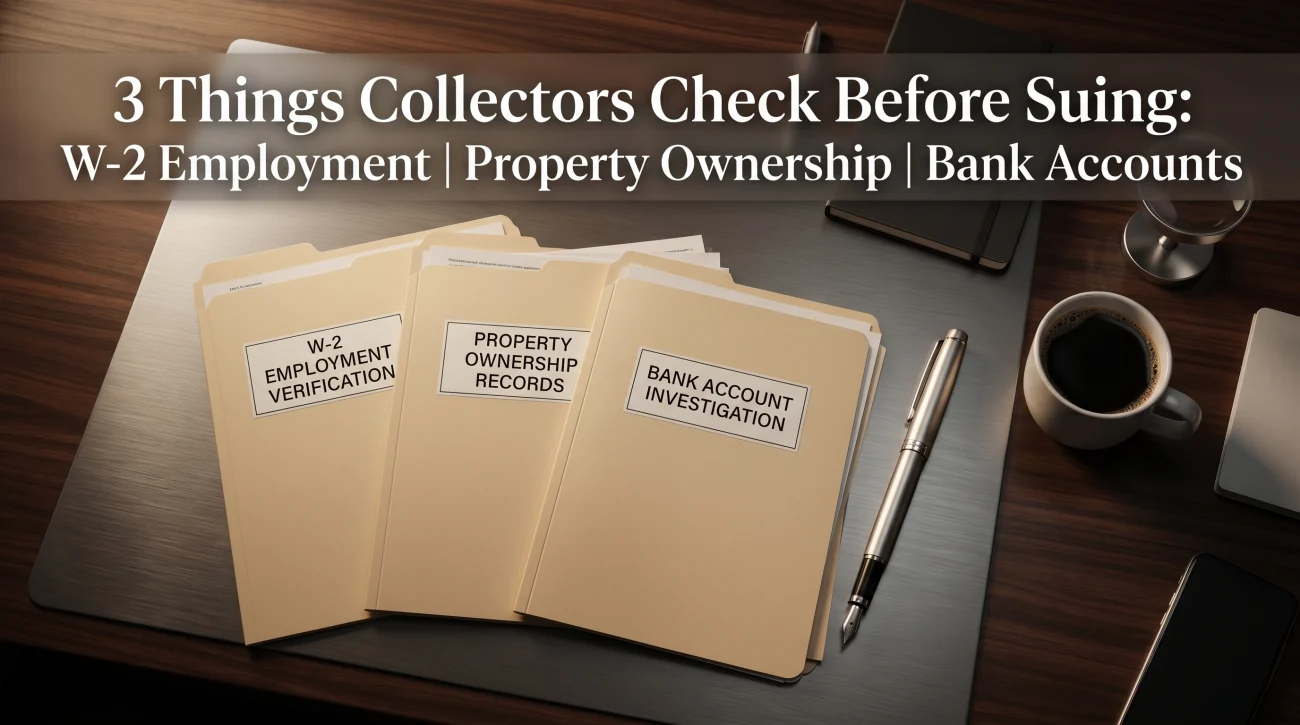

The Scoring Model: What Collectors Check Before Paying Filing Fees

If the geographic location works, the next filter is the individual consumer’s asset profile. Before a debt buyer spends a single dollar on court filing fees, they need to know if they can actually collect the money after winning a judgment. This is where the insider scoring process separates the actionable accounts from the dead ends.

Debt buyers do not just look at how much you owe; they look for post-judgment leverage. Using sophisticated skip-tracing databases, they scan for three main indicators:

- Active W-2 Employment: A verifiable employer means the collector can quickly execute a wage garnishment after securing a judgment.

- Property Ownership: Homeowners are prime targets because a collector can place a lien on the property, virtually guaranteeing a future payout if the home is ever sold or refinanced.

- Active Bank Account Indicators: Evidence of active checking accounts flags the file as a candidate for a bank levy.

If their system shows you only receive Social Security benefits (which are federally protected) and rent your home, you are generally considered “judgment-proof” at that specific moment. In those cases, even a massive $10,000 balance might be skipped for litigation because spending money to get an uncollectible piece of paper is bad business.

⚠️ Warning: Being “judgment-proof” today does not mean you are safe forever. Judgments can often be renewed for a decade or more. If you ever inherit money, get a higher-paying job, or buy property, that dormant judgment can suddenly be executed against you.

However, if the system flags active employment, the threshold for a lawsuit drops significantly. This explains the economics of small-balance lawsuits. People often wonder how it makes sense to sue over an $800 credit card debt. The math is simple: if a state’s small-claims filing fee is $50, and the expected default judgment rate is 70 percent, spending $50 to secure a garnished return of $800 is a highly profitable bet when executed thousands of times a month.

The 90-Day Warning: Why Suing on Aging Debt Happens So Fast

Another massive driver of lawsuit volume is the calendar. Many consumers are bewildered when they receive a court summons for a debt they have not heard about in four or five years. They assume the collector suddenly grew aggressive or a new manager took over their file.

In reality, it is a scheduled software trigger. Every state has a statute of limitations on debt, which dictates exactly how long a collector has to legally sue you. On a collection floor, accounts do not just quietly expire. The automated system is programmed to flag accounts 60 to 90 days before that legal deadline runs out.

Once flagged, these accounts are pulled off the standard calling floor and dumped directly into a litigation batch. The debt buyer knows this is their absolute last chance to legally force a payment. If they miss the deadline, the debt becomes “time-barred.” This timing mechanism is the primary reason why a consumer might experience years of total silence, followed by a sudden, urgent lawsuit right before the debt becomes too old to legally collect.

The Multiple Account Risk Factor

One of the most counterintuitive findings in consumer debt data relates to the number of accounts a person has in collections. You might assume that if someone has five or six accounts in default, debt collectors would view them as a lost cause and not bother spending money to sue them. The data proves the exact opposite.

According to consumer survey data compiled by the Consumer Financial Protection Bureau (CFPB), about 15 percent of all consumers contacted regarding a debt report being sued. However, that rate changes drastically based on the consumer’s level of distress:

- Consumers contacted about a single debt face a 6 percent lawsuit rate.

- Consumers contacted about five or more debts face a 35 percent lawsuit rate.

From an insider’s perspective, this makes perfect, ruthless sense. A consumer with one debt might have the resources to hire a lawyer and fight back. A consumer with five debts in collections is likely overwhelmed, exhausted by phone calls, and lacking the funds to mount a legal defense. The industry knows that the more overwhelmed a consumer is, the higher the probability that they will ignore the court summons, resulting in an automatic victory for the collector.

Many consumers assume collectors will see their multiple defaults and write them off as uncollectible. In reality, multiple defaults signal vulnerability.

If you have multiple accounts in collections, you fit the statistical profile for volume litigation. You must be prepared to respond formally to any legal notices.

The Hidden Reality: Racial Disparities in Debt Judgments

Perhaps the most sobering data regarding who actually gets sued involves demographics. For years, consumer advocates have argued that debt collection litigation disproportionately impacts minority communities. Recent, highly rigorous academic research has confirmed exactly how severe this disparity is.

A landmark 2024 paper published in the Journal of Banking and Finance analyzed a nationally representative panel of credit data from Experian, merged with racial and ethnic data from federal mortgage records covering mid-2013 to mid-2017. The findings were stark: Black and Hispanic borrowers are 52 percent more likely to experience a debt collection judgment than white and Asian borrowers.

Crucially, this 52 percent disparity remained even after controlling for personal income, credit scores, and levels of delinquent debt. This means the disparity is not simply a byproduct of differing delinquency rates. The machinery of volume litigation amplifies existing inequalities in the financial system, often by targeting specific zip codes or behavioral markers that correlate with systemic vulnerability.

The AI-Assisted Filing Machine

Because these targeting models proved so effective at finding the most profitable demographics and jurisdictions, the industry moved to scale them as rapidly as possible. This is where the technological acceleration begins. In the past, filing 5,000 lawsuits a month required a massive room full of paralegals manually checking spreadsheets, filling out complaint templates, and physically managing court dockets.

Today, that bottleneck has been eliminated. The National Center for State Courts (NCSC) highlighted this shift in a recent report, noting that contract case filings, the category that includes consumer debt collection, increased by 21 percent in 2022 and another 15 percent in 2023. The report hypothesized a key driver behind this surge: Artificial Intelligence.

AI tools and automated legal software are making it easier, faster, and infinitely cheaper for debt collection law firms to file complaints at scale. The software can scrape an Excel file of 10,000 purchased accounts, automatically verify which ones reside in favorable jurisdictions, auto-populate the court complaints, and electronically file them with the local clerk. The pattern that already concentrated filings against vulnerable consumers is now moving at the speed of automation.

What Consumers With High-Risk Profiles Need to Understand

If you fall into the categories the data identifies, such as living in a high-volume filing state, carrying multiple accounts in collections, or fitting the demographic profiles most impacted by judgments, you need to change your strategy. You cannot rely on flying under the radar.

The 35 percent lawsuit rate for consumers with five or more delinquent accounts is a massive red flag. If you are in this situation, your statistical profile matches the industry’s filing priority criteria perfectly. They are expecting you to be too overwhelmed to fight back, allowing them to secure a fast, cheap default judgment.

You break their statistical model by showing up. When you are served with papers, filing a formal, legally sound Answer fundamentally disrupts their automated process. It forces the law firm to spend human hours proving their case, which ruins the profit margin on the file. If you are facing this reality, this is the exact moment when legal consultation is most valuable. Do not hesitate to explore your options by consulting with a debt lawsuit attorney who understands how to leverage these defenses.

Final Thoughts on Lawsuit Data

The most empowering thing about court data and academic research is that it pulls back the curtain on an intimidating process. When you read the statistics, you realize that the debt collection legal machine is not an unstoppable force of justice; it is a highly optimized business model relying on predictable consumer behavior.

They target specific states because it is cheap. They target consumers with multiple debts because they expect them to surrender. They file massive volumes of cases because their financial models assume the vast majority of defendants will never respond. Once you understand who they sue and why, you understand exactly how to defend yourself. Learning the proper debt collection lawsuit defenses and understanding the steps to take when you are sued by a debt collector transforms you from a predictable statistic into a problem their model cannot easily solve.

❓ FAQ

📊 Is it common to be sued for a small debt?

Yes, especially if you live in a state with low small-claims court filing fees. Debt buyers regularly sue for balances under $1,000 if the cost to file the lawsuit is cheap and the default judgment rate is high.

🏢 Why don’t I recognize the company suing me?

The vast majority of debt lawsuits are filed by third-party debt buyers, not your original credit card company or hospital. These entities buy massive portfolios of defaulted accounts, meaning your debt was likely sold multiple times before a lawsuit was filed.

⚖️ Do debt collectors sue everyone who owes them money?

No. They use scoring models to determine who is worth suing. They look at your state’s filing costs, the statute of limitations, your active employment status, and your likelihood of defaulting in court. Only a percentage of accounts are selected for litigation.

🗺️ Does the state I live in affect my chances of being sued?

Absolutely. Debt buyers target “favorable jurisdictions” where court fees are low, procedural rules favor plaintiffs, and judges readily hand out default judgments. This leads to massive lawsuit surges in specific states.

🛑 What happens if I have multiple accounts in collections?

According to federal survey data, having five or more accounts in collections raises your chance of being sued to 35 percent. The industry targets multiple-account holders because they are statistically more likely to be overwhelmed and fail to appear in court.

🗂️ How do debt buyers file so many lawsuits so quickly?

They utilize automated legal software and AI tools. These systems scrape spreadsheets of purchased accounts, automatically verify if your jurisdiction has low filing fees, and auto-generate the lawsuit complaint. This bypasses human legal review almost entirely, allowing a single firm to file thousands of cases a week.

📈 Why am I being sued now after years of silence?

Lawsuits often spike right before the statute of limitations on your debt is about to expire. The debt buyer’s automated system flags the expiring account, usually 60 to 90 days out, and rushes a lawsuit to secure a judgment before they lose their legal right to collect.

🧑⚖️ Will showing up to court actually make a difference?

Yes. The entire debt buyer business model relies on you not showing up. When you file a formal Answer and contest the debt, you force them to spend money proving their case, which often leads to them offering a settlement or dropping the suit entirely.

📝 Can they get a judgment against me without me knowing?

They are legally required to serve you with a summons, but improper service (often called “sewer service”) happens frequently in volume litigation. If you do not respond because you never received the papers, the court will still grant them a default judgment.

💼 Should I hire a lawyer if I am sued by a debt buyer?

If you are facing a lawsuit from a volume debt buyer, consulting a consumer attorney is highly recommended. Debt buyers frequently lack the proper chain of title documentation to prove they own your debt, and an attorney knows exactly how to expose those flaws in court.

Sources & References

The data and patterns discussed in this article are derived from the following academic and institutional reports:

- 📌 Pew Charitable Trusts: “How Debt Collectors Are Transforming the Business of State Courts” (Court docket data analysis)

- 📌 Journal of Banking and Finance: “Racial Disparities in Debt Collection” (Analysis using Experian panel data, 2024)

- 📌 National Center for State Courts (NCSC): “Is GenAI revolutionizing court filings?” (Report on the surge in civil filings)

- 📌 Consumer Financial Protection Bureau (CFPB): Consumer Experiences With Debt Collection (Survey data regarding lawsuit rates)

- 📌 Journalists Resource: “With debt collection lawsuits rising, here’s what you need to know” (Review of debt collection lawsuit research)

Four areas of the collection process. Start wherever your situation applies.

Some situations have deadlines attached. These pages are written for those situations.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.