- Filing a debt collection lawsuit is rarely a personal or purely legal decision; it is an automated arithmetic problem run through a scoring model.

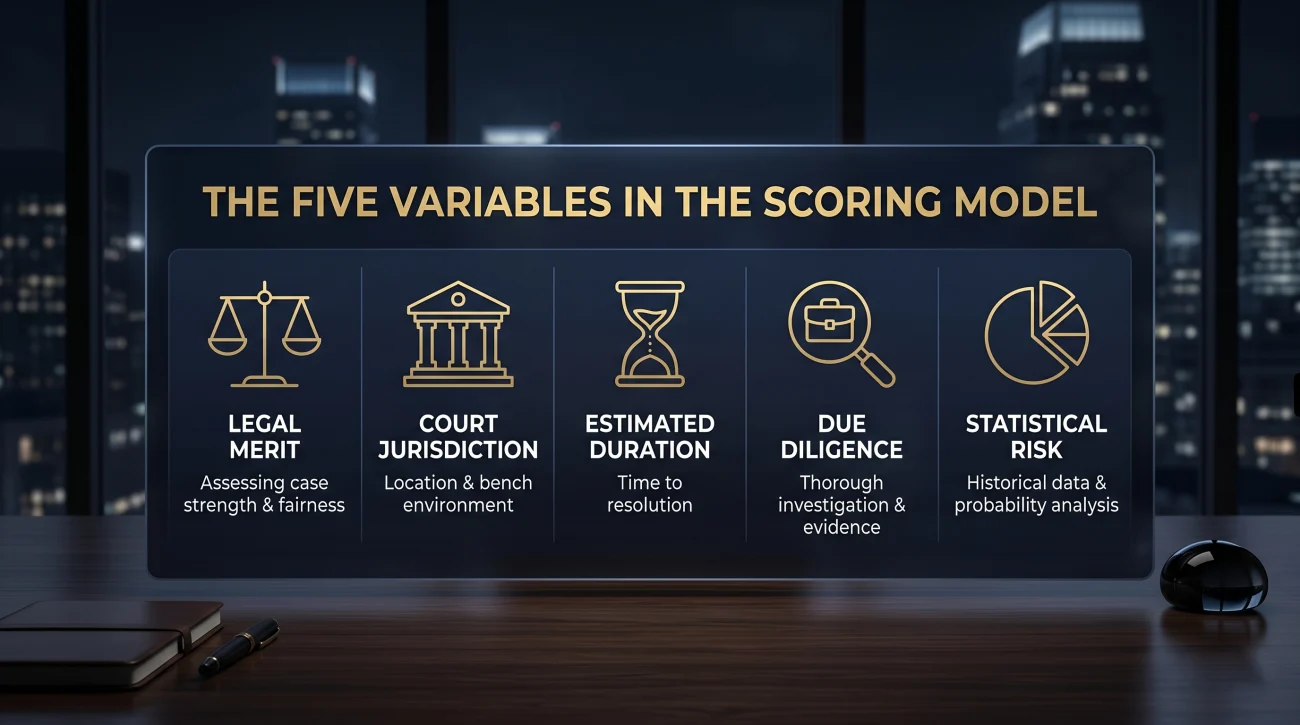

- Debt buyers evaluate five core variables before suing: account balance, state filing costs, remaining statute of limitations, known employment data, and the probability of a default judgment.

- Mass litigation relies on a massive expected default rate. The business model depends entirely on consumers failing to show up in court.

- Firms are accelerating their lawsuit volumes using automated tools and targeting specific states where filing fees are low and default rates are high.

- Filing a formal legal Answer breaks their automated math. Once you respond, the cost of litigating the case often exceeds the potential recovery, leading to favorable settlements or dismissals.

The Arithmetic Behind a Lawsuit

A court summons feels like a deeply personal legal judgment. But from inside a debt collection agency, the decision to sue rarely involves a lawyer sitting at a desk reviewing your financial history. It is simply an arithmetic problem.

I spent over a decade working on collection floors, and the hardest thing to explain is how mechanical the litigation process actually is. Consumers assume someone reviewed their file and actively chose to target them. That is almost never how it works.

Debt buyer law firms do not evaluate accounts individually. They run files through scoring models. A firm that files 5,000 cases per month cannot give each one personal attention. Instead, the scoring model does the heavy lifting, calculating whether the expected return on a specific account justifies the cost of a court filing fee.

Let me show you the math they use, and why understanding this formula is your best defense against a court summons.

Why Being Sued Feels Personal (But Is Not)

The most common reaction to receiving a court summons for a debt is panic, immediately followed by confusion. You might wonder why they targeted you. You might have friends with larger debts who never got sued, or you might have offered a payment plan a year ago that was rejected.

This confusion happens because you are looking at the situation as a human relationship. You see the debt as a personal failure or a temporary setback. The collector sees you as a row on a spreadsheet containing specific data points. If the data points align with their profitability threshold, the lawsuit is generated.

“I watched files come in and get triaged by a scoring model I was not supposed to see but eventually did. Accounts with current employer information got a different priority code than accounts with only an address. The person on the other end was not a person to the system. They were a set of variables.”

Understanding this disconnect is critical. When you realize that the lawsuit is a business calculation, you can stop feeling targeted and start attacking the math. The collector’s litigation decision relies heavily on you being too intimidated to fight back. To disrupt that outcome, you first have to understand exactly what the scoring model is looking for.

The Five Variables in the Lawsuit Scoring Model

Before an agency or a debt buyer’s legal network decides to spend money on court fees, the account must pass through a filter. While different firms use slightly different software, industry standard practice relies on five primary variables to determine if an account is worth taking to court.

1. The Account Balance Floor

Litigation costs money. Even in a streamlined, automated system, the plaintiff must pay court filing fees, process server fees, and overhead for the legal staff managing the docket. Because of this, very small balances are rarely worth the effort.

Industry data, supported by reporting from CBS News in October 2025, shows that most firms target minimum balances between $1,000 and $5,000. If you owe $400, the math often does not work. Spending $250 to recover $400 is bad business. However, there are exceptions based on the state you live in, which brings us to the next variable.

2. State Filing Costs and Court Type

Geography plays a massive role in whether you get sued. Filing a lawsuit in a small claims court with a $40 filing fee creates very different economics than filing in a civil court where the fee is $300. In states where small claims courts accept debt cases up to $15,000 or $20,000, volume litigation becomes extremely cost-effective.

Collectors know exactly which states and counties offer the cheapest path to a judgment. If you live in a jurisdiction with low barriers to entry for plaintiffs, the minimum balance required to trigger a lawsuit drops significantly.

3. The Statute of Limitations Window

Every state has a legal deadline for filing a debt collection lawsuit, known as the statute of limitations. This clock is a major driver of litigation urgency. A file with four years remaining on the clock is low urgency. The collection floor will continue to use standard phone and mail tactics to try and secure a payment.

However, a file with only five months left before the statute expires triggers an alarm in the system. The window is closing. If the debt buyer wants to extract value from that asset, they must file suit immediately. This is why many consumers experience years of silence followed by a sudden lawsuit right before the debt becomes legally too old to enforce.

4. The Skip Tracing Profile (The Asset Map)

Winning a lawsuit and getting a judgment is only half the battle for a debt collector. A judgment is just a piece of paper that says you owe the money. To actually get paid, they need leverage, which usually means wage garnishment or a bank levy.

This makes your skip tracing profile the deciding factor. If a collector’s database shows your current, verifiable place of employment, they are not just looking at a debtor; they are looking at an asset map. They know exactly where to send the garnishment order once they win. Conversely, if their data shows your only income is Social Security benefits, the scoring model drops your file to the bottom. Social Security is federally protected, making you largely judgment-proof, meaning a lawsuit would be a waste of their money.

5. Expected Default Probability

This is the most important variable of all. Mass-filing operations budget for a specific default rate. Based on published industry consumer research, debt buyers know that roughly 70 to 80 percent of consumers sued for a debt will never respond to the summons or show up in court.

When you do not respond, the collector wins automatically. This is called a default judgment. The entire volume litigation business model relies on this failure rate. They do not file 5,000 cases expecting to fight 5,000 trials. They file 5,000 cases expecting 4,000 automatic wins.

How Your Profile Looks to the System

To understand how this plays out in real time, look at how the variables combine to create high-risk and low-risk profiles for litigation.

| Variable | High Litigation Risk | Low Litigation Risk |

|---|---|---|

| Account Balance | Over $2,500 | Under $500 |

| Employment Data | Verified W-2 employer on file | Self-employed, unemployed, or SS income only |

| Statute of Limitations | Expiring within 6 to 12 months | Expired, or 3+ years remaining |

| Jurisdiction | Low filing fees, high default rates | High filing fees, strict documentation rules |

If your situation aligns with the “High Litigation Risk” column, you are a prime target for the scoring model. This does not mean you will definitely be sued, but it means the mathematical probability is significantly higher.

The Industrial Scale of Debt Buyer Lawsuits

To truly grasp how collectors decide who to sue, you have to look at the sheer scale of the operation. When I worked for a national debt buyer, we did not talk about individual defendants; we talked about state-level processing volume. We are not talking about local businesses taking a few non-paying customers to court. We are talking about Wall Street-backed financial entities processing human debt on an assembly line.

Recent court system analyses highlight just how aggressive this volume has become. In states where court data is transparent, a tiny fraction of plaintiffs dominate the entire civil docket. These are almost always debt buyers — companies that purchase portfolios of defaulted accounts from original creditors like credit card companies or hospitals for pennies on the dollar.

According to court docket tracking, volume filers like LVNV Funding have increased their lawsuit filings by massive margins over the last few years, sometimes spiking over 300 percent in specific regions like Indiana. This massive spike was not the result of a sudden wave of people deciding not to pay their bills. It was the result of an economic optimization. The scoring model discovered that Indiana offered a perfect storm: very low small-claims filing fees, high maximum balance thresholds, and streamlined paperwork that allowed bulk processing. It became a highly profitable testbed for volume filing.

This industrial scale is being pushed even further by technology. Recent judicial system reports have identified automated software and Artificial Intelligence as contributing factors to the surge in civil filings. These tools allow debt collection law firms to scrape data, populate templates, and file complaints faster and with less human oversight than ever before. The volume is not random; it is highly systematized.

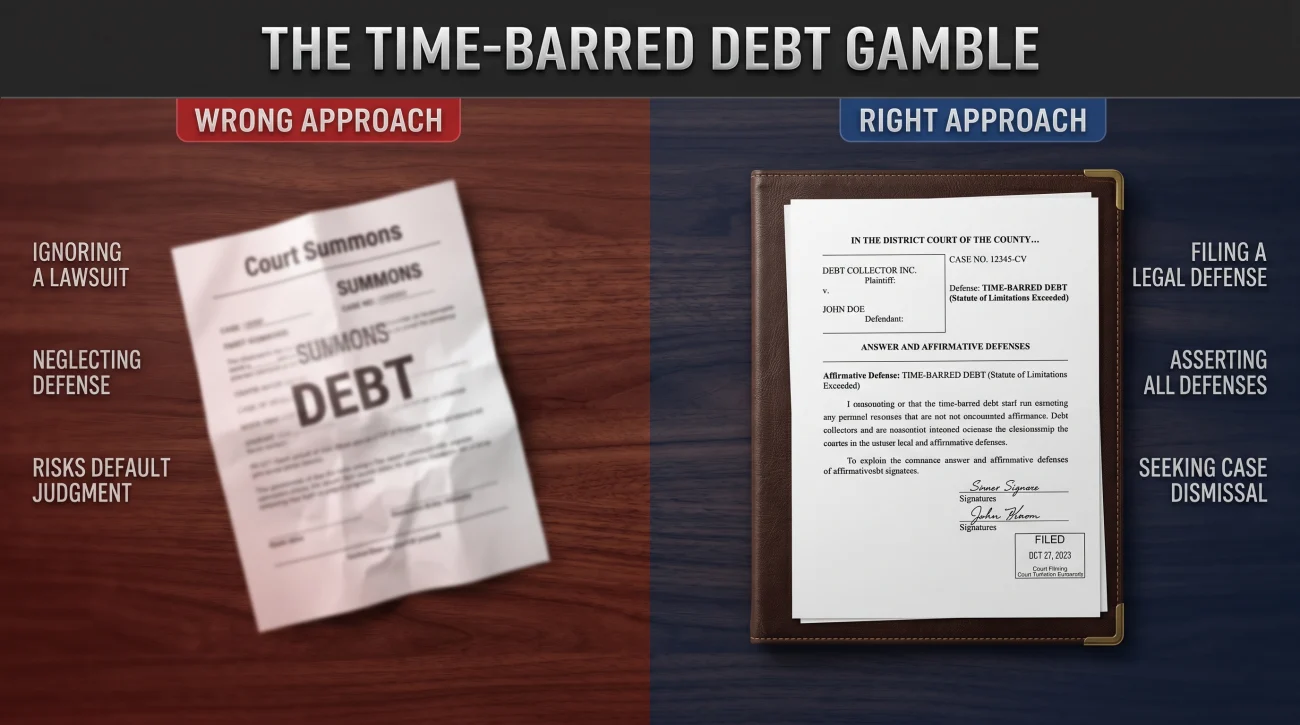

The Time-Barred Debt Gamble

Because the default rate is so high, some debt buyers run calculations that lead to legally questionable, or outright illegal, behavior. The most obvious example is the decision to sue on time-barred debt.

Time-barred debt is an account that has passed the statute of limitations. Legally, a collector cannot win a lawsuit on this debt if the consumer raises the expired statute as a defense. Knowing this, you might ask why a collector would waste money filing the suit.

I once watched a floor manager green-light a batch of 100 out-of-statute files for litigation. When I asked why we were spending money on dead accounts, he just pointed to the expected default rate. The math is brutal. They know that 80 percent of people will ignore the summons. The judge will grant a default judgment because the burden is on the consumer to point out that the debt is too old. The 20 people who actually show up and raise the defense will win, and the collector will simply dismiss those cases. But they walk away with 80 enforceable judgments on debts that were technically dead.

This practice is a severe FDCPA violation, but enforcement relies heavily on consumers knowing their rights and fighting back. If you suspect a collector is attempting this tactic, you must understand whether a debt collector can sue after the statute of limitations expires in your specific jurisdiction.

Many consumers ignore old debt thinking the collector knows they have no legal leg to stand on. This is a dangerous assumption. They do not need a strong case; they only need your silence.

Always assume a lawsuit is possible, even on weak claims. The only way to stop their gamble is to break their formula by responding formally.

What Happens When You Actually Respond

The entire debt collection litigation machine is built on the assumption of your absence. I saw hundreds of accounts flagged for litigation, and the moment a consumer filed a formal Answer, the file was immediately pulled from the automated track. When you actually participate in the process, their machine breaks down.

If you receive a summons and file a formal legal Answer with the court, you fundamentally change the arithmetic of the case. A filed Answer forces individual case evaluation. The automated scoring model can no longer process you. An actual attorney must now look at your file, review the documentation, and prepare for a hearing.

Suddenly, that $3,000 balance does not look so profitable. If the consumer is represented by counsel or raises a valid defense, the debt buyer has to produce actual evidence. They have to prove they own the debt, which is often difficult given the chain of title issues that debt buyers frequently face when accounts are sold multiple times.

Litigating a contested case costs thousands of dollars in attorney hours. Because of this, many debt buyer firms will offer highly favorable settlements, or voluntarily dismiss the case entirely, rather than spend the money to fight a prepared defendant in court. You can explore the exact strategies for fighting back by reviewing the most effective debt collection lawsuit defenses.

💡 Pro Tip: If you are served with papers, the absolute worst thing you can do is put them in a drawer and hope the problem goes away. Doing nothing is exactly what their financial model predicted you would do.

Final Thoughts on the Collector Litigation Decision

When you are targeted by a debt collection lawsuit, it is vital to separate your emotional reaction from the operational reality. You are not being sued because the original creditor is holding a grudge, or because a specific collector decided to make an example out of you. You are being sued because a software program looked at your balance, your zip code, and your estimated income, and determined that a $150 filing fee was a good investment.

Understanding the math gives you your power back. You know they are expecting you to default. You know they rely on cheap, undisputed victories. The moment you step into the process, you raise their costs and lower their expected return. If you have been served, do not let their math dictate your future. Take the time to learn exactly what steps to take when you are sued by a debt collector.

❓ FAQ

⚖️ What is the lowest amount a debt collector will sue for?

While there is no strict legal minimum, most debt buyers target balances above $1,000 to $1,500. However, in states with very low small claims court filing fees, they may sue for balances as low as $500 because the cost of litigation is minimal.

⏰ When do debt collectors usually decide to sue?

Lawsuits often happen at two distinct points: shortly after a debt buyer purchases a fresh portfolio of accounts with verified employment data, or right before the statute of limitations is about to expire, forcing them to act before they lose their legal rights.

📉 Why did a debt collector sue me but not my friend who owes more?

Your friend might not have verified employment data, or they might live in a state with higher court filing costs. The decision is based on a scoring model that calculates the probability of actually collecting the money after a judgment, not just the size of the balance.

🏢 Do original creditors sue as often as debt buyers?

Original creditors (like the bank that issued your credit card) do sue, but the vast majority of volume litigation is filed by third-party debt buyers who purchase accounts in bulk specifically to run them through mass-litigation models.

🛑 What makes a debt collector back out of a lawsuit?

The most common reason a collector drops a suit is when the consumer files a formal Answer denying the claim. Contested litigation is expensive, and if the debt buyer lacks the proper documentation to prove their case, they will often dismiss it rather than pay an attorney to fight.

👴 Will they sue me if my only income is Social Security?

Generally, collectors avoid suing consumers whose only income is Social Security because those funds are federally protected from garnishment. Filing a suit against someone who is mathematically judgment-proof is usually considered a waste of filing fees.

🤖 Is it true that AI is deciding who gets sued?

Yes. Instead of a human reviewing your file, firms use AI tools to scrape spreadsheets, automatically verify if your jurisdiction has low filing fees, and auto-generate the lawsuit complaint. This bypasses human legal review almost entirely, allowing a single firm to file thousands of cases a week.

📫 Can they sue me without sending a warning letter first?

Under the FDCPA, they must send you a validation notice within five days of their initial communication. However, there is no law stating they must send a specific “warning” before filing a lawsuit. The court summons itself is often the first formal legal notice you receive.

💰 Do collectors check my bank account before suing?

Collectors cannot view your specific bank account balances without a court order. However, they can pull soft credit inquiries to see your overall credit utilization, open accounts, and payment history to estimate whether you have the means to pay a judgment.

📝 What happens if I just ignore the lawsuit papers?

If you ignore the papers, the collector will ask the judge for a default judgment. Because you are not there to defend yourself, the judge will almost certainly grant it. Once they have a judgment, they can legally garnish your wages or freeze your bank account.

Sources & References

Four areas of the collection process. Start wherever your situation applies.

Some situations have deadlines attached. These pages are written for those situations.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.