- The CFPB received approximately 207,800 debt collection complaints in 2024, nearly double the volume from the previous year.

- A staggering 45% of all complaints involved consumers who simply did not recognize the debt being collected, marking a 333% increase in this specific issue.

- Lawsuit threats are weaponized heavily: 59% of legal threat complaints involved claims of credit damage, while 14% involved threats to sue on expired, time-barred debt.

- Court data shows mass litigation is a revenue strategy, not a legal one. Up to 4.7 million debt collection cases were filed in 2022, with more than half resulting in default judgments because the consumer never showed up.

The Numbers Behind the Calls: A View from the Inside

Every year, regulatory agencies publish massive reports detailing how the financial industry operates. When the Consumer Financial Protection Bureau (CFPB) released its latest data, the headlines focused on a single, massive number: 207,800. That is how many debt collection complaints the agency received in 2024 alone.

If you have never worked inside a collection agency, that number looks like a regulatory failure. If you have spent twelve years on the collection floor, managing accounts and training new agents like I did, that number looks completely different. It looks exactly like the business model working as intended.

I spent years contributing to these numbers before I fully understood what they meant. When you are dialing hundreds of numbers a day, you do not see the macroeconomic trends. You just see the spreadsheet in front of you. But when you step back and look at the actual debt collection industry statistics 2024 has produced, the gap between what the law says and what happens on the phone becomes impossible to ignore.

This data does not just tell us that collectors are aggressive. It reveals a specific, measurable pattern of how debt is bought, how threats are weaponized, and how the court system has been turned into a volume processing center. Here is what the latest CFPB and court data actually says—and more importantly, what it means for you when the phone rings.

You Are Not the Only One Experiencing This

If you are reading this, there is a good chance you are dealing with a collection account right now. You might be staring at a letter from a company you have never heard of, claiming you owe thousands of dollars for a credit card you do not remember opening. Or perhaps your phone rings three times a day from different local area codes, and the person on the other end is heavily implying that your credit score is about to be ruined.

The immediate feeling is isolation. The collector’s job is to make you feel like you are the only person who has ever fallen behind, that you have fundamentally failed, and that the only way to make the pressure stop is to hand over your bank routing number immediately.

The numbers strip away that illusion. You are not an isolated case. You are a data point in an industrialized system. When you understand that nearly half a million other people are navigating the exact same aggressive scripts and questionable documentation this year, the phone calls lose their psychological edge. The pressure you feel is not a personal judgment; it is an engineered tactic designed to force a quick decision before you have time to understand your rights.

The 2024 Surge: 207,800 Complaints

The sheer volume of friction between consumers and collectors is difficult to overstate. According to the CFPB Consumer Response Annual Report released in May 2025, the agency took in approximately 207,800 complaints regarding debt collection over the course of 2024. To put that in perspective, that is nearly double the roughly 109,900 complaints received in 2023.

Debt collection now represents roughly 7% of all financial complaints the CFPB handles across the entire United States economy. That is a massive footprint for a single sector.

These are not just people complaining because they have to pay their bills. The CFPB does not log a complaint simply because a consumer is unhappy about owing money. These complaints represent documented instances where consumers felt a line was crossed—where the tactics used to extract payment violated federal standards.

Yet, from an operational standpoint, 207,800 is a fraction of reality. This number only represents the people who knew their rights, realized a violation had occurred, and took the time to navigate a federal website to report it. For every complaint logged, there are thousands of calls that ended with an intimidated consumer making a payment on a legally unenforceable debt.

The “I Do Not Know This Debt” Epidemic

If you dive into the categorization of the CFPB debt collection complaints 2024 data, one statistic overshadows everything else. A staggering 45% of all debt collection complaints involved debts that consumers explicitly said they did not recognize (CFPB Consumer Response Annual Report, 2025).

The category of “I do not know” increased by 333% compared to the prior two-year monthly average. This has become the single most prevalent complaint issue since the CFPB began collecting data in 2013.

To the average person, this sounds absurd. How can an entire industry be built on calling people about debts they do not even recognize? From inside a collection floor, however, the “unrecognized debt” problem is not surprising at all. It is the natural result of the debt buying ecosystem.

Why Documentation Degrades

When you sign up for a credit card, the original bank has your application, your signature, and years of your billing statements. If you default, they eventually charge off the account. But they rarely just walk away. They sell your account as part of a massive portfolio to a third-party debt buyer for pennies on the dollar.

That debt buyer might try to collect it, or they might sell it again. Portfolios are bought, split, and resold multiple times. With every transaction, the underlying documentation degrades.

“In the smaller agencies I worked for, we almost never had original account agreements. The account would reach my desk as nothing more than a single row on an Excel spreadsheet. I had a name, a last known address, a phone number, and a balance. I was calling people demanding $2,500, and I knew perfectly well that if they asked me to prove it with a signature, I couldn’t. My job was to get them to agree to pay before they thought to ask.”

By the time a collector at a third-tier agency is calling you, they are often operating entirely blind. They are attempting to collect a debt they cannot currently prove. The 333% surge in complaints about unrecognized debt perfectly mirrors this reality. Consumers are being harassed over spreadsheets, not verified legal contracts.

This is why understanding the framework of FDCPA protections is your strongest asset. The law requires them to validate the debt if you demand it. Their business model relies on you not knowing how to ask.

Threats by the Numbers

When documentation is weak, collectors rely on psychological leverage. The CFPB’s FDCPA Annual Report (released November 2025) provides a clinical breakdown of exactly what kinds of threats are being reported.

| Type of Threat Reported | Percentage of Legal Threat Complaints |

|---|---|

| Threats to damage or ruin consumer’s credit score | 59% |

| Threats to sue on time-barred (expired) debt | 14% |

| Being sued without proper notification of the lawsuit | 11% |

The 59% figure regarding credit damage is the blunt instrument of the industry. It works because credit scores govern modern life, dictating everything from housing to employment. However, the 14% statistic regarding threats to sue on old debt is far more insidious.

Every state has a statute of limitations (SOL) on debt collection. Once that clock runs out, a collector cannot legally sue you to force payment. However, it is not illegal for them to simply *ask* you to pay it. The violation occurs when they threaten legal action they cannot take.

Experienced collectors know how to walk right up to the edge of an illegal threat without crossing it. Instead of saying, “We will sue you tomorrow,” they say, “We are reviewing this account for next steps, and we want to resolve this voluntarily before it moves to another department.” The implication is clear, but the legal defense is plausible.

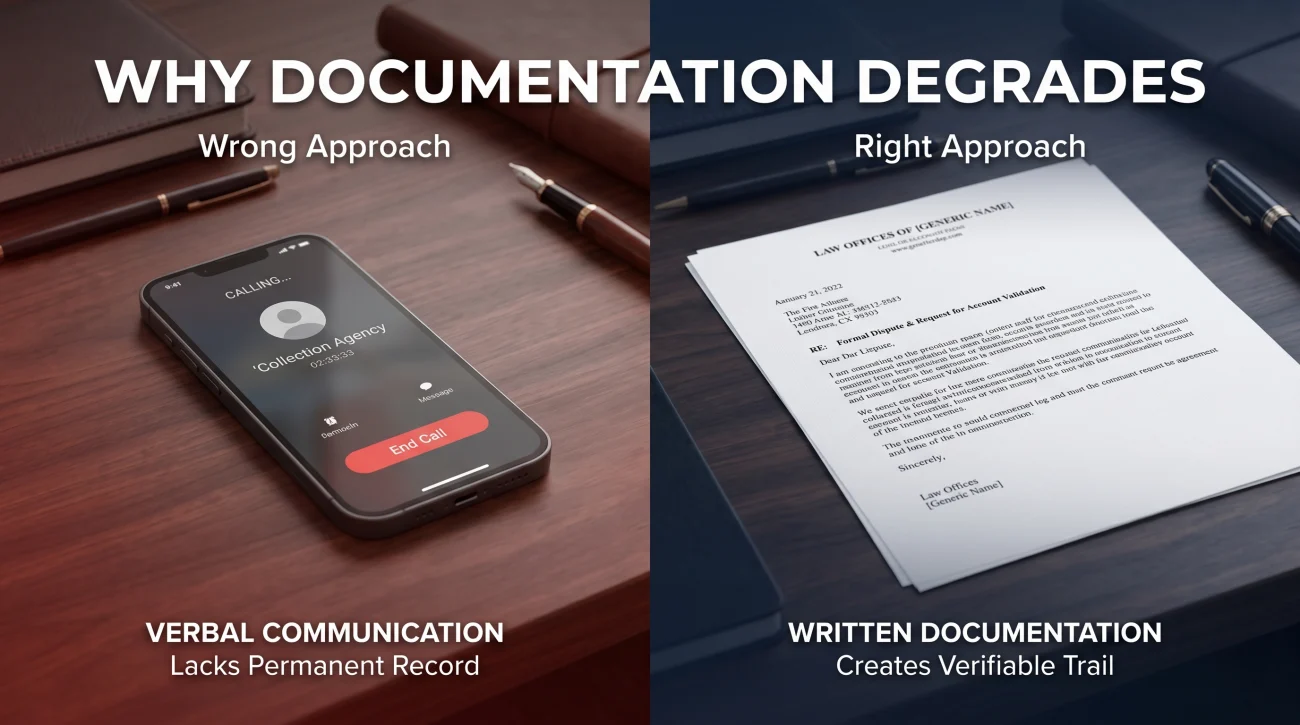

If you suspect a collector is using illegal threats or crossing the line with their communication tactics, keeping a strict log is essential. You have to document the abuse to fight it. If you want to know when their tactics cross the line into actionable violations, you need to understand exactly what the FDCPA restricts.

The Call Log Habit

To protect yourself from shifting narratives, you must build a documentation habit. Never rely on your memory of a high-stress phone call. Keep a notebook specifically for debt collection calls.

Date: October 14, 2025

Time: 2:15 PM

Collector Name/ID: ‘Mr. Davis’ (Refused to give last name)

Agency: Midland Credit Management

Number Called From: 800-555-0199

What was said: Stated that if I did not make a $50 payment today, my file would be marked as ‘refusal to cooperate’ and sent for ‘legal review.’

The Industrial Scale of Debt Collection Lawsuits

While many threats are empty, the actual volume of debt collection lawsuits filed in the United States is staggering. It has become a dominant feature of the civil justice system.

According to a comprehensive September 2025 analysis by the Pew Charitable Trusts, debt collection lawsuits have surged back to pre-pandemic highs. Up to 4.7 million debt collection cases were filed in 2022 alone.

This is not a story of local businesses trying to collect unpaid invoices. This is industrialized litigation driven by massive debt buyers. The data clearly shows that a tiny fraction of plaintiffs are dominating state court dockets.

In Connecticut, for example, the data revealed that just 10 plaintiffs account for an astonishing 80% of the entire debt collection docket. These plaintiffs are almost never the credit card company you originally signed a contract with. They are entities that purchase debt in bulk. One national debt buyer, LVNV Funding, increased its lawsuit filings by 350% between 2019 and 2024 in the state of Indiana alone (Pew Charitable Trusts, 2025).

This explains why the “I don’t recognize who is suing me” experience is so common. You are being sued by a financial holding company you have never done business with, represented by a law firm filing hundreds of identical complaints a day.

The Default Judgment Reality

Why would a company file millions of lawsuits if their documentation is often terrible? Because they do not expect you to ask for it. They expect you to ignore the paperwork.

The CFPB research confirms a brutal reality: more than half of all filed debt collection lawsuits lead to default judgments. A default judgment happens when a consumer is served with lawsuit papers and fails to file a formal response with the court. When you do not show up, the collector wins automatically, regardless of whether they actually had the evidence to prove you owed the money.

⚠️ Warning: Ignoring a court summons is the single most destructive mistake you can make. A default judgment allows a debt buyer to move from simply calling you to aggressively seizing your assets through wage garnishments and bank levies.

Only about 25% of consumers who are sued actually attend their court hearings or file a proper legal response. From the inside, this is the most important metric on the floor.

Key Point: Filing a hundred cases and expecting 75 defaults is not a legal strategy — it is a revenue strategy. The 25 who showed up were the variable in the equation, not the plan.

When I was reviewing accounts, we knew the default rate intimately. The business model of a high-volume debt buyer relies entirely on the assumption that the vast majority of defendants will simply surrender by inaction. If every consumer who was sued filed a proper answer demanding proof of the debt and the chain of title, the current economic model of the debt buying industry would collapse. It would be too expensive to litigate.

Understanding the automated court losses that fuel the industry is the first step in realizing that a lawsuit is not the end of the line—it is often a bluff calling for your silence.

Turning the Data Into a Defense Strategy

Reading these statistics should change how you interact with the industry. The 207,800 complaints and the 4.7 million lawsuits all point to the same fundamental truth: collectors operate on volume and speed. Your defense must be built on documentation and friction.

First, never assume the person on the phone has all the facts. Given that 45% of complaints involve unrecognized debt, you must force them to prove their claims in writing. A verbal dispute means nothing. You must send a written validation request within 30 days of their initial contact.

Second, recognize the artificial urgency. When a collector threatens imminent credit destruction or legal action if you do not pay by Friday, they are using psychological pressure to prevent you from researching your rights or checking the statute of limitations. Take a breath. Hang up the phone.

Finally, if the worst happens and a process server hands you a stack of papers, you cannot rely on the fact that the debt is old or the amount is wrong. The court does not know that unless you tell them. You must understand exactly what to file when served to prevent the automated default judgment they are counting on.

Final Thoughts on the Industry Data

The CFPB and court data from 2024 and 2025 paint a stark picture. We are dealing with an industry that generates hundreds of thousands of complaints, frequently pursues unrecognized debts, and relies heavily on default judgments to generate revenue. But looking at this data from the outside only gives you half the story.

The other half is realizing that this massive machine is surprisingly fragile when confronted with an informed consumer. The systems are designed to process the 75% of people who do not fight back. The moment you demand written validation, dispute a charge officially, or file an answer to a lawsuit, you drop out of their automated workflow. You become an expensive exception.

Do not let the sheer scale of the numbers intimidate you. The debt collection industry thrives on information asymmetry—they have the data, the skip tracing tools, and the call scripts. By understanding the actual statistics behind their methods, you take away their most powerful weapon: your own confusion.

❓ FAQ

📈 How many debt collection complaints does the CFPB receive?

In 2024, the CFPB received approximately 207,800 complaints regarding debt collection. This was nearly double the volume from 2023, making debt collection one of the most heavily complained-about financial sectors in the country.

🛑 What is the most common reason people complain about debt collectors?

According to the 2024 CFPB data, 45% of all complaints involved consumers stating they did not recognize the debt being collected. This is often due to the rapid buying and selling of old debt portfolios between agencies.

⚖️ How many debt collection lawsuits are filed every year?

A recent analysis by the Pew Charitable Trusts indicated that up to 4.7 million debt collection cases were filed in state courts in 2022, with filings surging back to pre-pandemic highs in 2024.

🏢 Who is actually filing most of these debt collection lawsuits?

The vast majority of lawsuits are not filed by original creditors like banks or hospitals. They are filed by a highly concentrated group of third-party debt buyers. In some states, just 10 debt buying companies account for 80% of all cases.

📉 What happens to most people who get sued by a debt collector?

More than half of all debt collection lawsuits result in a default judgment. This happens because the consumer fails to show up to court or file a formal answer. The debt buyer wins automatically, regardless of the evidence.

⏰ Are collectors legally allowed to threaten to sue me?

A collector can only threaten to sue if they actually intend to do so and if the debt is still within your state’s statute of limitations. Threatening to sue on a time-barred (expired) debt is a direct violation of the FDCPA.

🗣️ Can I stop a debt collector from calling my phone?

Yes. Under federal law, if you send a written cease and desist letter to the collection agency, they must stop communicating with you, except to confirm they are stopping or to notify you of a specific legal action.

🤷♂️ Why do I keep getting calls for a debt that isn’t mine?

The CFPB data shows this is a massive industry-wide issue. Debt portfolios are bought and sold multiple times, often causing original account documentation to degrade. Collectors frequently call people based on outdated, mixed-up, or incorrect spreadsheet data.

💰 Will a debt buyer actually sue me for a small amount like $500?

Yes, it happens frequently. Debt buyers operate on volume and scale. Because they rely heavily on default judgments—meaning they win automatically if you do not show up—suing for small balances can still be a highly profitable revenue strategy.

📝 What should I do if a collection agency I don’t recognize contacts me?

Never make a payment or give out personal information on the first call. Instead, demand a written debt validation letter. Under the FDCPA, they are legally required to provide proof that you owe the money and that they have the right to collect it.

Sources & References

The operational insights in this article are based on inside experience, contextualizing the following public data sets and reports:

Four areas of the collection process. Start wherever your situation applies.

Some situations have deadlines attached. These pages are written for those situations.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.