- Debt collector scripts are not just random words; they are precision-engineered psychological tools designed to bypass your logical defenses.

- The “I am here to help you” reframe is a strategic tactic intended to position the collector as an ally while leading you toward a payment commitment.

- Specific phrases like “good faith payment” are often used to reset the statute of limitations or trigger the psychological principle of consistency.

- Understanding the empathy-validation-pivot sequence allows you to recognize when a collector is steering the conversation and provides the leverage to stop the game.

Behind the Headset: Why Every Word Is a Weapon

I didn’t learn the scripts I am about to show you from a consumer protection website. I learned them in a windowless training room on the third floor of a third-party collection agency. I remember the smell of stale coffee and the sound of fifty people dialing simultaneously, all reading from the same laminated binders. It was an environment built entirely on the science of linguistic pressure.

Later in my career, I was the person standing at the front of that room, teaching new hires how to use these exact lines to extract payments from people who were already struggling to keep their lights on. Most consumers assume a debt collector is just an angry person on the other end of a phone. In reality, a modern collector is more like a highly trained sales representative. They are equipped with a binder full of rebuttals, psychological triggers, and carefully phrased closes that have been tested and refined across millions of calls. They aren’t just talking to you; they are running a program on you.

I spent twelve years inside this industry, and I have seen how effective these scripts are when the person on the other end doesn’t know the game. In this guide, I am going to decode the psychology behind debt collector scripts tactics. We will look at the opening gambit, the “helpful ally” reframe, and the specific phrases designed to trap you. Once you understand the mechanism, the fear disappears, and you can take control of the interaction.

The Collector’s Ear: What We Heard in Your Silence

When I was sitting in that training room, we weren’t taught to listen to your problems. We were taught to listen for “vulnerabilities.” In the first thirty seconds of a call, an experienced collector is reading your reaction like a diagnostic chart. If your voice stutters when you verify your address, we know you are intimidated. If you let out a long, heavy sigh before answering a question, we know you are exhausted and likely to agree to a “small” payment just to end the call.

The scripts are designed to exploit these micro-reactions. When you hear a voice calling regarding an “important financial matter,” the silence that follows is exactly what we want. In that gap, your brain is racing through every mistake you have ever made. You are doing the psychological work for us. You are searching for an excuse, which gives us the opening to use a rebuttal.

The shame you feel is a tool. We were trained to recognize the moment that shame turned into compliance. If I could get you to lower your voice or apologize for your situation, I knew the script was working. The pressure you feel is not a reflection of your character; it is a calculated byproduct of my training. I wasn’t listening to understand your hardship; I was listening for the moment your logical defenses collapsed so I could pivot to a payment commitment.

The Opening Gambit: Urgency Without Specificity

The first thirty seconds of a collection call are the most critical. This is the “Opening Gambit,” where the collector establishes authority and creates a sense of mystery. They almost always use a variation of this script:

The Script:

“I’m calling regarding an important financial matter concerning your account. It’s important that you contact us as soon as possible to discuss your options.”

Notice what isn’t said. They don’t mention “debt,” “collections,” or the name of the original bank immediately. They use the word “important” twice. They call it a “financial matter.” This phrasing is chosen because it sounds official, perhaps even legal, but it doesn’t give you enough information to prepare a defense. The lack of specificity is intentional; it forces you to ask questions, which keeps you on the line.

The goal of this opening is to trigger curiosity and what psychologists call the “consistency principle.” By answering the call and staying on the line to find out what the “matter” is, you have already made a micro-commitment to engage with the collector. Once you are engaged, it is much harder to hang up.

“When I trained collectors, I told them to use a tone that was professionally concerned. If you sound too angry, the consumer hangs up. If you sound too nice, they don’t take it seriously. You want to sound like a doctor giving a bad diagnosis: serious, urgent, and authoritative.”

The “Helpful Ally” Reframe: Divide and Conquer

Once you verify your identity, the script shifts. The collector now knows you owe the money, and they want to make sure you don’t view them as the enemy. This is the most effective psychological tactic in the entire industry: the Reframe.

The Script:

“Look, I’m not the bad guy here. My job is to help you resolve this before it has to go to the next level. I want to see if we can find a way to clear this up today so you don’t have to worry about it anymore.”

This script is designed to divide your loyalty. The collector is positioning themselves as your ally against a vague, threatening “next level,” which usually means a legal department or a different agency. They are offering you a way out of the stress they just created. This works because of the principle of reciprocity: if the collector is “helping” you by holding the file, you feel a psychological obligation to “help” them by making a payment.

The “next level” is almost always left undefined. It is a shadow on the wall. In the industry, we knew that creating this type of implication was widely recognized as a compliance problem, yet it remains a staple of the script because it is so difficult for a consumer to prove. By keeping it vague, they allow your imagination to create the worst-case scenario. For a deeper look at the rules they are supposed to follow, review the foundational debt collection laws that govern these interactions.

📌 Note: The collector is never your ally. They are a paid representative of a company that purchased your debt for pennies on the dollar. Their only goal is to maximize the return on that investment.

The Settlement Math: The Leverage They Hide

One thing you will never hear in a script is the “Purchase Price” of your account. When I worked for a national debt buyer, we routinely purchased portfolios of credit card debt for anywhere from 3 to 10 cents on the dollar. This means your $2,000 balance was bought for roughly $60. The industrial scale of this profit margin is the best-kept secret in the business.

When a collector offers you a “one-time settlement” of 50% (or $1,000), they aren’t doing you a favor. They are attempting to generate a profit margin of over 1,500% on a single transaction. On the floor, a 50% settlement made me a hero to my manager, even though I was telling the consumer it was a “difficult exception” I had to fight for. We were taught to act as if we were arguing with the “back office” on your behalf, when in reality, the settlement was pre-approved by the software.

This information is your ultimate leverage. When you realize how little they paid for the right to call you, the “settlement window” feels a lot wider. If you want to know more about what to do when their tactics become abusive, you have to start by understanding the economics that fuel their aggression. They don’t need the full balance to make a massive profit; they just need you to believe they do.

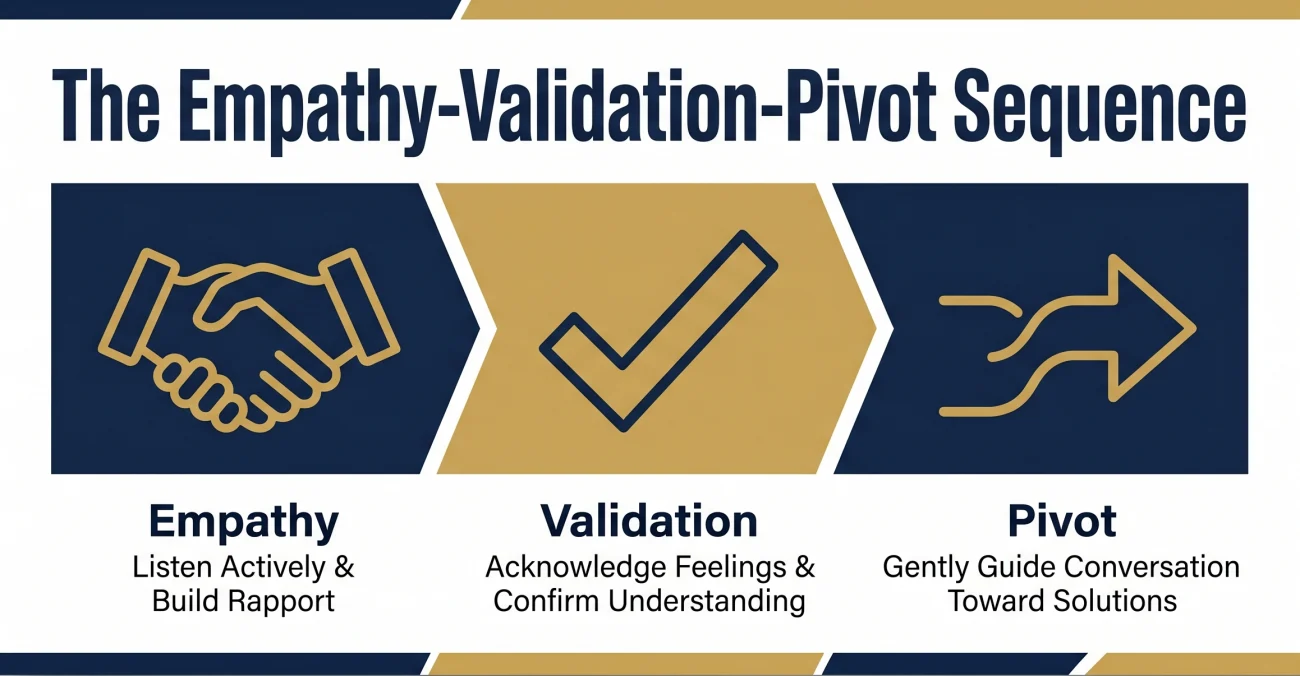

The Empathy-Validation-Pivot Sequence

If you explain that you are unemployed or have medical bills, a trained collector will not argue with you. Arguing creates resistance. Instead, they use a three-step sequence that feels like a conversation but is actually a steering mechanism designed to lead you to a payment portal.

Step 1: Empathy

The collector says, “I understand that’s been a very difficult situation for you.” This isn’t real empathy; it is a technique to lower your guard. If you feel heard, you are less likely to be defensive or hang up. It creates a temporary bond of trust.

Step 2: Validation

They follow up with, “I appreciate you being honest with me about that. Most people try to avoid us, but it’s clear you want to take care of your responsibilities.” This uses social proof. By telling you that you are one of the “good ones,” they are pressuring you to live up to that label by making a payment. It is the psychological hook that makes you want to prove your integrity.

Step 3: The Pivot

Finally, they pivot: “Because you’re being so cooperative, what I can do for you today is [Offer].” The Offer is always something that benefits the agency, like a small payment to hold the file. You can learn more about the protocol for handling an initial collection call to avoid falling into this trap.

Spending twenty minutes explaining your financial hardship to the collector, hoping they will “understand” and close the account.

Recognizing the pivot and stating: “I hear that you have options, but I am not making any payment decisions today. Please send a full validation notice in writing.”

The Third-Party Pressure Script

One of the most effective scripts in our training binders involved calling people who weren’t the debtor. We were trained to call neighbors, employers, or family members under the guise of “verifying location information.” This is often where the line between legal contact and harassment gets blurred.

The script was designed to stay technically within the lines while maximizing social pressure. We would say: “I’m calling for [Your Name] regarding a business matter. I have had trouble reaching them at their home number. Do you have a better way for me to contact them at their place of employment?”

The goal wasn’t to get the phone number. We usually already had it. The goal was to let your neighbor or boss know that “someone” was looking for you regarding a “business matter.” This creates a sense of public embarrassment. We knew that once a consumer felt their social circle was aware of the debt, they were much more likely to call us back and pay just to keep the calls from spreading. It is a form of broadcast shame. If you are experiencing this, you need to know how to stop debt collector calls legally.

The “Good Faith Payment” Trap

If you tell a collector you absolutely cannot pay the full balance, they will move to their fallback position: the good faith payment. This is the most dangerous phrase in the collection industry because it sounds so reasonable to a stressed consumer.

The Script:

“I understand you can’t do the full amount. But can you just do a $50 good faith payment today? It shows the office that you are trying, and it keeps the account from moving to the legal department.”

To the consumer, $50 sounds like a fair compromise to buy some peace and quiet. To the collector, that $50 is a massive win for two reasons that have nothing to do with the money itself. Analysis from industry training resources like PDCflow reveals that these micro-payments are used specifically to build psychological momentum and re-establish a payment habit.

First, it creates a commitment and consistency loop. Once you pay $50, you have admitted the debt is yours and that you have the means to pay something. It becomes much easier for them to get $100 from you next month because you have already identified yourself as a payer.

Second, and most critically, making a partial payment can restart the clock on the statute of limitations depending on the age of the debt and where you live. This means a debt that was about to become legally unenforceable is now “refreshed” for another several years. I have seen collectors high-five each other after getting a $5 payment because they knew they just regained the right to sue on a ten-year-old debt. It is vital that you understand how a partial payment restarts the statute of limitations before you agree to any good faith gesture.

The Scarcity Tactic: Artificial Deadlines

Collectors are trained to use “false scarcity” to force a quick decision. They know that if you have time to think, research your rights, or talk to a spouse, the odds of them getting a payment drop significantly. When I was training new hires, I told them that every hour a consumer spends off the phone is an hour they spend gaining leverage. The goal of the deadline is to cut that time off.

The Script:

“This settlement offer is only available until the end of the business day. If I don’t have a confirmation by 5:00 PM, I have to release this file back to the general queue, and I can’t guarantee this discount will still be there.”

This is almost always a lie. Collection agencies don’t have magical “Friday only” windows. They want to settle every day of the week. However, by creating a deadline, they stop you from looking at the bigger picture. You stop wondering if you should pay and start wondering how to pay before 5:00 PM. This lack of transparency is a recurring theme in the CFPB reports on unfair collection practices, which document thousands of complaints about high-pressure settlement tactics.

Key Point: No legitimate settlement offer expires in four hours. If they can take a settlement today, they can almost certainly take it next Tuesday. Take your time.

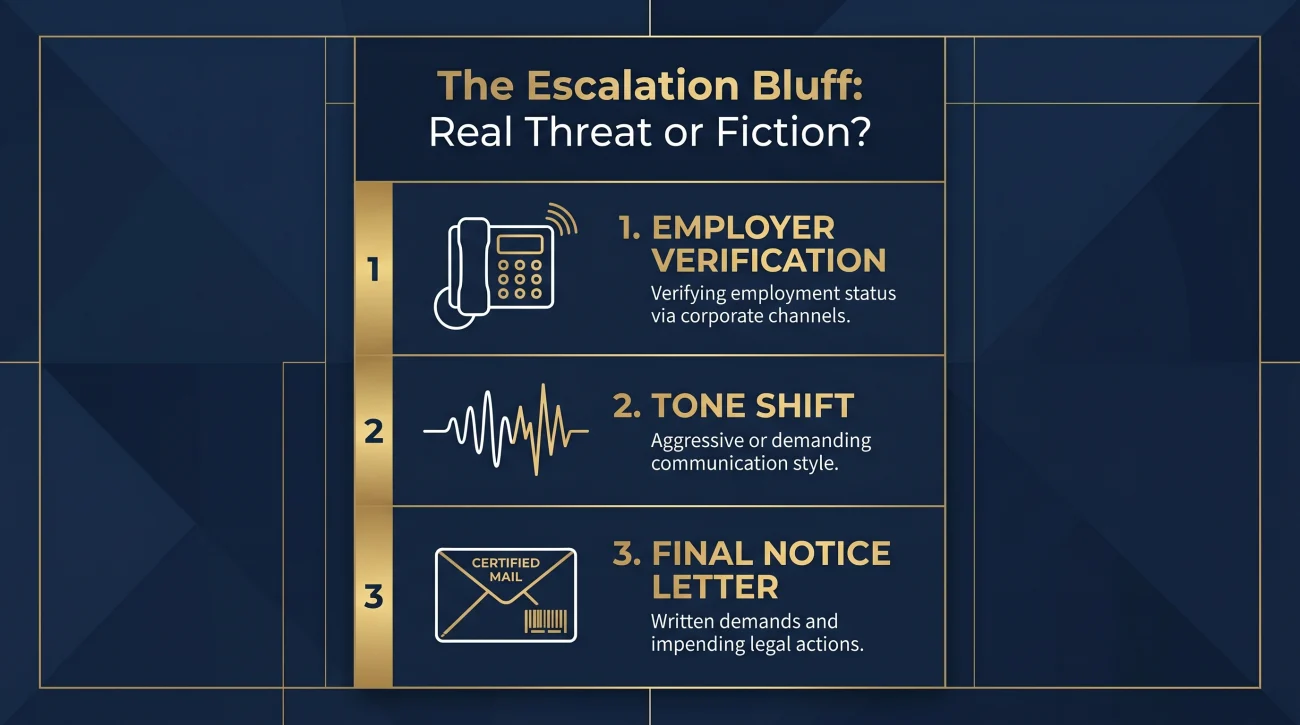

The Escalation Bluff: Real Threat or Fiction?

The “next level” or “legal review” threat is the most common bluff on the floor. But how do you know when it is real? From the inside, we looked for specific markers before a file was actually sent to a lawyer. If you haven’t seen these signs, the “legal” threat is likely just a script meant to boost urgency.

- Hard Employer Verification: If a collector suddenly stops asking about payments and starts calling your HR department to “verify employment status,” they are mapping your assets for a potential garnishment.

- The Tone Shift: When a collector stops using the “helpful ally” script and becomes cold and procedural, they may have been instructed to build a final contact log for a legal file.

- Final Notice Letter: Not just a regular bill, but a letter explicitly titled “Notice of Intent to Refer to Legal” sent via certified mail.

Most of the time, the “legal” threat is used in the first month of collection when the agency hasn’t even purchased the court costs yet. It is a cost-effective way to scare you into a payment without them spending a dime on filing fees. If they were actually suing you, you would be hearing from a process server, not a phone collector.

The “I Can’t Afford It” Rebuttal Tree

In the training binders I used, we had a section called the “Rebuttal Tree.” This section was particularly effective because it ensured the collector never had to “think”; they only had to “react.” For every excuse a consumer gave, there were three scripted responses designed to keep the conversation moving toward a payment. This is why the conversation feels so one-sided; you are fighting a tree that has been growing for decades. Each response is designed to pull more information out of you that can be used for skip tracing.

| Consumer Objection | The Scripted Rebuttal | The Real Goal |

|---|---|---|

| “I lost my job.” | “I’m sorry to hear that. Do you have any family members who could help you with a one-time settlement?” | To see if there are untapped assets outside of your personal income. |

| “I have medical bills.” | “I understand. If we could lower the monthly payment to something small, like $25, would that help?” | To get you into a payment loop and acknowledge the debt. |

| “I’m filing bankruptcy.” | “I see. Have you actually filed yet? Do you have a case number? Until then, we still need to resolve this.” | To verify if you are bluffing or if they need to stop collection immediately. |

The goal of the rebuttal is to keep the conversation going. As long as you are talking, they are winning. The moment you stop giving them information, their script breaks. This is why acknowledging a debt over the phone is so dangerous: you are feeding their rebuttal machine.

Consumer Counter-Scripts: How to Talk Back

The best way to break a collector’s script is to refuse to use the words they expect. If you use their vocabulary, you are playing on their home turf. Here is how to handle the most common script openings word-for-word. These are the responses we hated to hear because they ended our psychological leverage instantly.

You: “I am not verifying any information over the phone. If you have an account associated with this number, you must have an address on file. Please send all correspondence in writing.”

Collector: “I’m trying to help you keep this from going to the next level. Can you do a $50 good faith payment today?”

You: “I do not recognize this debt and I am not making any payment decisions today. I am requesting a full debt validation notice as required by federal law. Do not call me again until that is provided.”

By using these phrases, you stop being a “target” and start being a “compliance risk.” Collectors hate compliance risks because they take too much time and carry too much liability. Most will move on to an easier target that hasn’t challenged their authority.

Author Reflection: The Psychology of the Performance

I was good at these scripts. I knew exactly when to lower my voice to sound empathetic and when to sharpen my tone to create urgency. At the time, I viewed it as a professional skill, like a lawyer or a salesperson. I remember the feeling of sitting in the break room, checking the leaderboard, and realizing I had just talked three people into payments they couldn’t afford.

It took years for me to realize that the empathy I was taught to perform was a calculated deception. I wasn’t listening to Margaret or any other caller to understand them; I was listening for a weakness I could use to steer them toward a payment. The scripts are designed to erase the human on the other end and replace them with a set of variables. It turns a conversation into a transaction where the collector has all the cards.

When I left the industry, the first thing I did was start telling people to stop talking to collectors on the phone. The scripts only work if you stay in the arena. If you force the communication into writing, the psychological game ends. The collector cannot use an “empathy-validation-pivot” sequence in a letter. They have to provide facts, documentation, and proof. That is where you win.

What to Do When the Script Starts

The next time you answer the phone and realize it is a collector, don’t try to win the argument. You are playing on their home turf. Instead, follow these steps to break their script immediately:

- Stop the information flow: Do not explain your hardship, do not mention your job, and do not acknowledge that you owe the debt. Every piece of info you give is a new branch in their rebuttal tree.

- Demand the paper trail: Interrupt the script and say: “I am not discussing this over the phone. Please send a full debt validation notice and all supporting documentation to my address on file.”

- End the call: You don’t need their permission to hang up. Once you have made your request for written communication, the call is over. Hang up.

Final Thoughts on Collection Tactics

Debt collector scripts tactics are built on a simple foundation: the industry exploits your natural honesty to bypass your legal protections. These scripts are not meant to find a fair resolution; they are meant to find the fastest path to a payment commitment. When you move from being a “file” to an informed actor who demands written proof, you fundamentally change the math of the collection floor. You become too expensive to manipulate, and in this industry, being “expensive” is your best defense.

❓ FAQ

📞 Do debt collectors really have scripts for every situation?

Yes. Professional agencies use rebuttal trees that provide specific scripted responses for almost any excuse a consumer can give, from job loss to medical emergencies. They are trained to keep the conversation moving toward a payment no matter what you say.

🤝 Why do collectors act like they are my friend or trying to help me?

This is a tactic called “the reframe.” By acting as an ally, the collector reduces your defensiveness and uses the psychological principle of reciprocity to make you feel like you owe them a payment for their “effort” in helping you.

💸 What is a “good faith payment” and should I make one?

A good faith payment is a small amount meant to show you are cooperative. You should be extremely careful, as making a partial payment can restart the statute of limitations on an old debt, making you vulnerable to a lawsuit you otherwise could have avoided.

⏰ Is it true that a settlement offer expires by the end of the day?

Almost never. This is an artificial deadline designed to create false scarcity and force you to make a panicked decision before you can research your rights. Settlement offers are almost always available for longer than a few hours.

🗣️ Can a collector use my social media posts against me?

Yes. Collectors are trained to look for public posts that might reveal a new job, a promotion, or a major purchase. They use this information to update their asset map and decide if suing you is economically profitable.

🤫 Should I tell the collector why I can’t pay my bills?

No. Every detail you give is simply a new piece of data they can use to refine their rebuttals. It is better to state that you cannot pay and move the conversation to written validation.

🛡️ How do I break a debt collector’s psychological game?

The only way to win is to not play. Stop the verbal conversation immediately and demand that all communication be handled in writing. This removes their ability to use tone and urgency against you.

😤 Why do some collectors get angry or aggressive on the phone?

While most are trained to be professionally concerned, some use aggression to trigger fear. Fear is a powerful motivator for payment. Aggressive tactics are common in agencies with poor compliance monitoring.

🧾 What does “important financial matter” actually mean?

It is a vague scripted phrase designed to sound official and urgent without identifying the call as a debt collection attempt. It is intended to bypass your initial resistance to talking to a collector.

🛑 Can a collector legally lie to me to get a payment?

The law prohibits collectors from using false or misleading representations. However, many use shaded truths or implications that are difficult to prove as violations on a recorded call, such as vague threats about “legal review.”

Sources & References

The operational insights in this article are based on inside experience in collector training, contextualized by the following primary resources:

Four areas of the collection process. Start wherever your situation applies.

Some situations have deadlines attached. These pages are written for those situations.

- When collector behavior crosses the line the FDCPA was written to prevent

- What to do if a collector files suit after their calls have not worked

- What collectors can do to your wages once a judgment is entered

- How a bank levy works and which funds the law protects from seizure

- How to resolve the debt that collectors have been calling about

Disclosure: The content on this site reflects direct experience inside the debt collection industry and is grounded in federal law and regulation. It is informational in nature. Reading it does not constitute legal advice and does not create any professional relationship. If you are dealing with a lawsuit, a judgment, or a legal deadline, consult a licensed attorney in your state before acting.